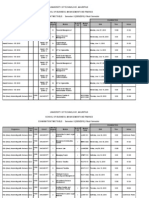

Citi SGP MKT Updt (Jun 2010)

Citi SGP MKT Updt (Jun 2010)

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Universalization of L'Oreal - SampleDocument3 pagesThe Universalization of L'Oreal - SampleKhushbu PalNo ratings yet

- Cantonese Idioms and What They MeanDocument3 pagesCantonese Idioms and What They MeanSG PropTalkNo ratings yet

- Savills - 2Q2015Document4 pagesSavills - 2Q2015SG PropTalkNo ratings yet

- HSR Report - 3 Oct 2014 (Narrowing CCR Vs OCR-RCR Spread)Document4 pagesHSR Report - 3 Oct 2014 (Narrowing CCR Vs OCR-RCR Spread)SG PropTalkNo ratings yet

- The Real Deals (22-11-2012)Document9 pagesThe Real Deals (22-11-2012)SG PropTalkNo ratings yet

- Asia Property Market Sentiment Report (H2) 2014Document141 pagesAsia Property Market Sentiment Report (H2) 2014SG PropTalkNo ratings yet

- Pine Grove Transactions (Aug 2011 - Aug 2014)Document10 pagesPine Grove Transactions (Aug 2011 - Aug 2014)SG PropTalkNo ratings yet

- Sky Vue: Media ReleaseDocument3 pagesSky Vue: Media ReleaseSG PropTalkNo ratings yet

- Sky Vue: Fact SheetDocument1 pageSky Vue: Fact SheetSG PropTalkNo ratings yet

- The Mews - BrochureDocument13 pagesThe Mews - BrochureSG PropTalkNo ratings yet

- Sembawang CottageDocument2 pagesSembawang CottageSG PropTalkNo ratings yet

- The Real Deals (25-10-2012)Document9 pagesThe Real Deals (25-10-2012)chow_ck6055No ratings yet

- Park View MansionDocument2 pagesPark View MansionSG PropTalkNo ratings yet

- Private Residential Property Transactions With Caveats LodgedDocument12 pagesPrivate Residential Property Transactions With Caveats LodgedSG PropTalkNo ratings yet

- The Real Deals (23-08-2012)Document9 pagesThe Real Deals (23-08-2012)SG PropTalkNo ratings yet

- The Real Deals (20-09-2012)Document10 pagesThe Real Deals (20-09-2012)SG PropTalkNo ratings yet

- The Real Deals (19-07-2012)Document9 pagesThe Real Deals (19-07-2012)SG PropTalkNo ratings yet

- Regent Canalside (Brochure)Document23 pagesRegent Canalside (Brochure)SG PropTalkNo ratings yet

- Personal BrandingDocument2 pagesPersonal BrandingRajan MahalingamNo ratings yet

- Answer Key Macroeconomics - ECO202 - UF3 - AUM Spring 2013 Online Quiz 1Document11 pagesAnswer Key Macroeconomics - ECO202 - UF3 - AUM Spring 2013 Online Quiz 1Mazuona Al100% (1)

- Basic Finance ConceptDocument4 pagesBasic Finance Conceptzain aliNo ratings yet

- MS PalembangDocument65 pagesMS PalembangAdrianus PramudhitaNo ratings yet

- Ibr2012 - Bric Focus FinalDocument10 pagesIbr2012 - Bric Focus FinalAnonymous 6OTxFCyPNo ratings yet

- Ministry of TourismDocument6 pagesMinistry of TourismHarshSuryavanshiNo ratings yet

- A Project Report On Whether The Decreasing Sales of Pizza Hut Can Be Increased Through Promotional ActivitiesDocument74 pagesA Project Report On Whether The Decreasing Sales of Pizza Hut Can Be Increased Through Promotional ActivitiesBabasab Patil (Karrisatte)100% (1)

- Cookbook-Key Lime PieDocument2 pagesCookbook-Key Lime PieDánielCsörfölyNo ratings yet

- Evolution of Investment BankingDocument2 pagesEvolution of Investment BankingAmritha AshokNo ratings yet

- Print Control PageDocument1 pagePrint Control Pagehemanth_kollipara100% (1)

- Cts Question Paper 27 JUNE 2005Document2 pagesCts Question Paper 27 JUNE 2005Janardhan DevaraNo ratings yet

- Advertising AppealDocument19 pagesAdvertising AppealSudhanshu SharmaNo ratings yet

- BricsDocument22 pagesBricsRadhaNo ratings yet

- Indian Silk Promotion CouncilDocument22 pagesIndian Silk Promotion CouncilDEEPAKNo ratings yet

- Birch Paper Company Q. Which Bid Should Mr. Kenton Accept?Document2 pagesBirch Paper Company Q. Which Bid Should Mr. Kenton Accept?ruchika vartakNo ratings yet

- An Analysis of Grameen Bank and ASADocument45 pagesAn Analysis of Grameen Bank and ASAAye Nyein ThuNo ratings yet

- Tocopherol Concentrate, MixedDocument4 pagesTocopherol Concentrate, MixedBen ClarkeNo ratings yet

- SIP Project ReportDocument6 pagesSIP Project ReportHoney MehrotraNo ratings yet

- SBMF Examinations June 2010Document50 pagesSBMF Examinations June 2010van Dana kam'sNo ratings yet

- Chicken BiryaniDocument5 pagesChicken Biryaniarunrai78No ratings yet

- MonmouthDocument25 pagesMonmouthPerci LunarejoNo ratings yet

- Bank of Baroda: Particulars To Be Supplied by The Applicant For AdvancesDocument4 pagesBank of Baroda: Particulars To Be Supplied by The Applicant For AdvancesPiyush SharmaNo ratings yet

- SynopsisFormat Antra PitchDocument2 pagesSynopsisFormat Antra PitchKavit ThakkarNo ratings yet

- Sample Questions Set For Sap Fi CertificationDocument153 pagesSample Questions Set For Sap Fi CertificationPallavi Chawla100% (1)

- Pr-Food-And-Drink-Menu 4Document2 pagesPr-Food-And-Drink-Menu 4api-306627664No ratings yet

- What Is The Difference Between A High Side and Low Side DriverDocument2 pagesWhat Is The Difference Between A High Side and Low Side DriveranaqiaisyahNo ratings yet

- Assignment On LUX SoapDocument30 pagesAssignment On LUX SoapAhad Zaheen25% (4)

- CBSE Class 11 Accountancy WorksheetDocument3 pagesCBSE Class 11 Accountancy WorksheetyashNo ratings yet

- Acc Gr12 June 2009 Answer Sheets BlankDocument18 pagesAcc Gr12 June 2009 Answer Sheets BlankSam ChristieNo ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Universalization of L'Oreal - SampleDocument3 pagesThe Universalization of L'Oreal - SampleKhushbu PalNo ratings yet

- Cantonese Idioms and What They MeanDocument3 pagesCantonese Idioms and What They MeanSG PropTalkNo ratings yet

- Savills - 2Q2015Document4 pagesSavills - 2Q2015SG PropTalkNo ratings yet

- HSR Report - 3 Oct 2014 (Narrowing CCR Vs OCR-RCR Spread)Document4 pagesHSR Report - 3 Oct 2014 (Narrowing CCR Vs OCR-RCR Spread)SG PropTalkNo ratings yet

- The Real Deals (22-11-2012)Document9 pagesThe Real Deals (22-11-2012)SG PropTalkNo ratings yet

- Asia Property Market Sentiment Report (H2) 2014Document141 pagesAsia Property Market Sentiment Report (H2) 2014SG PropTalkNo ratings yet

- Pine Grove Transactions (Aug 2011 - Aug 2014)Document10 pagesPine Grove Transactions (Aug 2011 - Aug 2014)SG PropTalkNo ratings yet

- Sky Vue: Media ReleaseDocument3 pagesSky Vue: Media ReleaseSG PropTalkNo ratings yet

- Sky Vue: Fact SheetDocument1 pageSky Vue: Fact SheetSG PropTalkNo ratings yet

- The Mews - BrochureDocument13 pagesThe Mews - BrochureSG PropTalkNo ratings yet

- Sembawang CottageDocument2 pagesSembawang CottageSG PropTalkNo ratings yet

- The Real Deals (25-10-2012)Document9 pagesThe Real Deals (25-10-2012)chow_ck6055No ratings yet

- Park View MansionDocument2 pagesPark View MansionSG PropTalkNo ratings yet

- Private Residential Property Transactions With Caveats LodgedDocument12 pagesPrivate Residential Property Transactions With Caveats LodgedSG PropTalkNo ratings yet

- The Real Deals (23-08-2012)Document9 pagesThe Real Deals (23-08-2012)SG PropTalkNo ratings yet

- The Real Deals (20-09-2012)Document10 pagesThe Real Deals (20-09-2012)SG PropTalkNo ratings yet

- The Real Deals (19-07-2012)Document9 pagesThe Real Deals (19-07-2012)SG PropTalkNo ratings yet

- Regent Canalside (Brochure)Document23 pagesRegent Canalside (Brochure)SG PropTalkNo ratings yet

- Personal BrandingDocument2 pagesPersonal BrandingRajan MahalingamNo ratings yet

- Answer Key Macroeconomics - ECO202 - UF3 - AUM Spring 2013 Online Quiz 1Document11 pagesAnswer Key Macroeconomics - ECO202 - UF3 - AUM Spring 2013 Online Quiz 1Mazuona Al100% (1)

- Basic Finance ConceptDocument4 pagesBasic Finance Conceptzain aliNo ratings yet

- MS PalembangDocument65 pagesMS PalembangAdrianus PramudhitaNo ratings yet

- Ibr2012 - Bric Focus FinalDocument10 pagesIbr2012 - Bric Focus FinalAnonymous 6OTxFCyPNo ratings yet

- Ministry of TourismDocument6 pagesMinistry of TourismHarshSuryavanshiNo ratings yet

- A Project Report On Whether The Decreasing Sales of Pizza Hut Can Be Increased Through Promotional ActivitiesDocument74 pagesA Project Report On Whether The Decreasing Sales of Pizza Hut Can Be Increased Through Promotional ActivitiesBabasab Patil (Karrisatte)100% (1)

- Cookbook-Key Lime PieDocument2 pagesCookbook-Key Lime PieDánielCsörfölyNo ratings yet

- Evolution of Investment BankingDocument2 pagesEvolution of Investment BankingAmritha AshokNo ratings yet

- Print Control PageDocument1 pagePrint Control Pagehemanth_kollipara100% (1)

- Cts Question Paper 27 JUNE 2005Document2 pagesCts Question Paper 27 JUNE 2005Janardhan DevaraNo ratings yet

- Advertising AppealDocument19 pagesAdvertising AppealSudhanshu SharmaNo ratings yet

- BricsDocument22 pagesBricsRadhaNo ratings yet

- Indian Silk Promotion CouncilDocument22 pagesIndian Silk Promotion CouncilDEEPAKNo ratings yet

- Birch Paper Company Q. Which Bid Should Mr. Kenton Accept?Document2 pagesBirch Paper Company Q. Which Bid Should Mr. Kenton Accept?ruchika vartakNo ratings yet

- An Analysis of Grameen Bank and ASADocument45 pagesAn Analysis of Grameen Bank and ASAAye Nyein ThuNo ratings yet

- Tocopherol Concentrate, MixedDocument4 pagesTocopherol Concentrate, MixedBen ClarkeNo ratings yet

- SIP Project ReportDocument6 pagesSIP Project ReportHoney MehrotraNo ratings yet

- SBMF Examinations June 2010Document50 pagesSBMF Examinations June 2010van Dana kam'sNo ratings yet

- Chicken BiryaniDocument5 pagesChicken Biryaniarunrai78No ratings yet

- MonmouthDocument25 pagesMonmouthPerci LunarejoNo ratings yet

- Bank of Baroda: Particulars To Be Supplied by The Applicant For AdvancesDocument4 pagesBank of Baroda: Particulars To Be Supplied by The Applicant For AdvancesPiyush SharmaNo ratings yet

- SynopsisFormat Antra PitchDocument2 pagesSynopsisFormat Antra PitchKavit ThakkarNo ratings yet

- Sample Questions Set For Sap Fi CertificationDocument153 pagesSample Questions Set For Sap Fi CertificationPallavi Chawla100% (1)

- Pr-Food-And-Drink-Menu 4Document2 pagesPr-Food-And-Drink-Menu 4api-306627664No ratings yet

- What Is The Difference Between A High Side and Low Side DriverDocument2 pagesWhat Is The Difference Between A High Side and Low Side DriveranaqiaisyahNo ratings yet

- Assignment On LUX SoapDocument30 pagesAssignment On LUX SoapAhad Zaheen25% (4)

- CBSE Class 11 Accountancy WorksheetDocument3 pagesCBSE Class 11 Accountancy WorksheetyashNo ratings yet

- Acc Gr12 June 2009 Answer Sheets BlankDocument18 pagesAcc Gr12 June 2009 Answer Sheets BlankSam ChristieNo ratings yet