You might also like

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

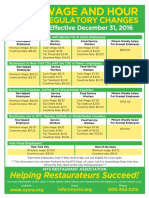

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Strategic Management Report On Wateen Telecom LTDDocument54 pagesStrategic Management Report On Wateen Telecom LTDfarhanfarhat67% (3)

- BacklogDocument8 pagesBacklogamitdesai92No ratings yet

- Betterteam Recruitment Plan Template 20201201Document2 pagesBetterteam Recruitment Plan Template 20201201Joyce SuaNo ratings yet

- Hannes Meyer's biographical essay explores the architect's workDocument52 pagesHannes Meyer's biographical essay explores the architect's worknisivocciaNo ratings yet

- 2020 Management Paper by Talvir SInghDocument202 pages2020 Management Paper by Talvir SInghSheetala HegdeNo ratings yet

- Registro Cosmetico EuropaDocument19 pagesRegistro Cosmetico EuropaMax J. B. SouzaNo ratings yet

- FETTY CAKE LTDDocument3 pagesFETTY CAKE LTDNGONIDZASHE G MUBAYIWANo ratings yet

- Aloha ConnectDocument2 pagesAloha ConnectJorgeNo ratings yet

- 1575 Tania SultanaDocument34 pages1575 Tania SultanaTania SultanaNo ratings yet

- Sales QuotationDocument1 pageSales QuotationTekbahadur SinghNo ratings yet

- Multiple Choice Problems Chapter 8Document12 pagesMultiple Choice Problems Chapter 8Dieter LudwigNo ratings yet

- School of Architecture, Building & Design: Highpark Suites, Kelana JayaDocument42 pagesSchool of Architecture, Building & Design: Highpark Suites, Kelana JayaZue Rai Fah100% (1)

- Theory Okhtein Assignment Nadine Mohamed Group 1Document8 pagesTheory Okhtein Assignment Nadine Mohamed Group 1ATLA ForeverNo ratings yet

- The New Context For Specialty CoffeeDocument8 pagesThe New Context For Specialty CoffeeSpecialtyCoffee100% (2)

- Job Specification and Job Description of Nestle Bangladesh - PREPARED FOR ASSIGNMENT ON JOB DESCRIPTION AND JOB Tamanna Parveen Eva (TPE Senior Lecturer - Course Hero PDFDocument12 pagesJob Specification and Job Description of Nestle Bangladesh - PREPARED FOR ASSIGNMENT ON JOB DESCRIPTION AND JOB Tamanna Parveen Eva (TPE Senior Lecturer - Course Hero PDFHumayun JavedNo ratings yet

- Asian Journal of Management Cases: Zainab Riaz, Lahore University of Management Sciences, PakistanDocument1 pageAsian Journal of Management Cases: Zainab Riaz, Lahore University of Management Sciences, PakistanbhagavathamhNo ratings yet

- Kevin O'LearyDocument4 pagesKevin O'LearyRichard WoottonNo ratings yet

- Calculating conversion values and bond prices of convertible bondsDocument2 pagesCalculating conversion values and bond prices of convertible bondsDebarnob SarkarNo ratings yet

- Minimum Wages in MaharashtraDocument6 pagesMinimum Wages in MaharashtrasalapeNo ratings yet

- Monetary Policy Statement October 2020Document2 pagesMonetary Policy Statement October 2020African Centre for Media ExcellenceNo ratings yet

- Wallfort - 29 April 2022Document24 pagesWallfort - 29 April 2022Utsav LapsiwalaNo ratings yet

- The Most Important Cities of AustraliaDocument3 pagesThe Most Important Cities of AustraliaLudovica BonessiNo ratings yet

- Woodsmith - Vol 41, No 246, 2019Document72 pagesWoodsmith - Vol 41, No 246, 2019reivnax100% (1)

- Student RequirementsDocument7 pagesStudent RequirementsYANNA CABANGONNo ratings yet

- Municipality of San Clemente - Citizens CharterDocument155 pagesMunicipality of San Clemente - Citizens CharterFree FlixnetNo ratings yet

- Will The Internet Destroy The News MediaDocument20 pagesWill The Internet Destroy The News MediaJoshua GansNo ratings yet

- Contemporary Logistics in China - Interconnective Channels and Collaborative Sharing-SprDocument216 pagesContemporary Logistics in China - Interconnective Channels and Collaborative Sharing-SprTrainer Ayoub Al AjroudiNo ratings yet

- Handbook For The NEBOShDocument83 pagesHandbook For The NEBOShAndi RahamantoNo ratings yet

- Quizzes Compilation TaxationDocument11 pagesQuizzes Compilation TaxationHads LunaNo ratings yet

- BASICS OF INSURANCE - Question & AnswersDocument14 pagesBASICS OF INSURANCE - Question & Answersjeganrajraj100% (2)