Download as pdf or txt

You might also like

- The Shopping Center Industry in Mexico 2012Document128 pagesThe Shopping Center Industry in Mexico 2012Fabián SánchezNo ratings yet

- NAFTA - Final WordDocument31 pagesNAFTA - Final Wordanon_836461438100% (3)

- Commodity Prices and FP in LAC, Sinnott 2009Document41 pagesCommodity Prices and FP in LAC, Sinnott 2009Sui-Jade HoNo ratings yet

- Nafta Project by Asiya SiddiquiDocument18 pagesNafta Project by Asiya SiddiquiamirdonNo ratings yet

- Rade Policies and ProceduresDocument4 pagesRade Policies and ProceduresJessa ArellagaNo ratings yet

- 02046-Tpa Paper Feb02Document21 pages02046-Tpa Paper Feb02losangelesNo ratings yet

- EMEA Group11 MexicoDocument21 pagesEMEA Group11 MexicoRAJARSHI ROY CHOUDHURYNo ratings yet

- Comparative AccountingDocument27 pagesComparative AccountingIkaa RachmaNo ratings yet

- Flow of The ReportDocument5 pagesFlow of The ReportStephany ChanNo ratings yet

- The Impact of NAFTA On The United States: Mary E. Burfisher, Sherman Robinson and Karen ThierfelderDocument20 pagesThe Impact of NAFTA On The United States: Mary E. Burfisher, Sherman Robinson and Karen ThierfelderDominic NdegeNo ratings yet

- Case 1 - USA - China Trade RelationsDocument7 pagesCase 1 - USA - China Trade RelationsPeter ShahinianNo ratings yet

- NAFTA Decade of GrowthDocument44 pagesNAFTA Decade of GrowthPyotr WrangelNo ratings yet

- 2trade LiberalizationDocument14 pages2trade LiberalizationKTW gamingNo ratings yet

- Documentos de Política Económica: Banco Central de ChileDocument16 pagesDocumentos de Política Económica: Banco Central de ChileFernando LopezNo ratings yet

- Rules of Origin and Regional ContentDocument4 pagesRules of Origin and Regional ContentIftekharul Mahdi100% (1)

- "These Headwinds Have Really Concentrated On LatinDocument4 pages"These Headwinds Have Really Concentrated On Latinapi-308666826No ratings yet

- Overview of Canadian Agricultural Policy Systems: Richard R. BarichelloDocument23 pagesOverview of Canadian Agricultural Policy Systems: Richard R. BarichelloRizky Lutfi SNo ratings yet

- Presented By:-Usama Shahzad & Samreen ShaikhDocument32 pagesPresented By:-Usama Shahzad & Samreen Shaikhsamreen4087No ratings yet

- AssigmentktptDocument5 pagesAssigmentktptCherry KikoNo ratings yet

- Brazil's Financial Crisis & The Potential Aftershocks: World Agriculture & TradeDocument3 pagesBrazil's Financial Crisis & The Potential Aftershocks: World Agriculture & TradeAnup VermaNo ratings yet

- Argentina Economic CrisisDocument2 pagesArgentina Economic CrisisAnkita BhawsinkaNo ratings yet

- BelizeDocument3 pagesBelizeLabis Regine DaneNo ratings yet

- Running Head: THE U.S ECONOMY1Document10 pagesRunning Head: THE U.S ECONOMY1Hillary Musembi KinyamasyoNo ratings yet

- Nafta Project by - WASIF RAZA..Document17 pagesNafta Project by - WASIF RAZA..Wasif RazaNo ratings yet

- Strategic Alliances in Emerging Latin America: A View From Brazilian Chilean, and Mexican CompaniesDocument20 pagesStrategic Alliances in Emerging Latin America: A View From Brazilian Chilean, and Mexican CompanieskynthaNo ratings yet

- Dragonomics How Latin America Is Maximizing or Missing Out On China S International Development StrategyDocument328 pagesDragonomics How Latin America Is Maximizing or Missing Out On China S International Development StrategyJuan Felipe Estrada TrianaNo ratings yet

- China: Trade RelationsDocument10 pagesChina: Trade RelationsBrooke GallagherNo ratings yet

- Duty-Free Access To 60 Percent: Trade AgreementDocument2 pagesDuty-Free Access To 60 Percent: Trade AgreementtanyaNo ratings yet

- U.S. Debt: The Next Financial Crisis?: Journal of Economics, Finance and International BusinessDocument12 pagesU.S. Debt: The Next Financial Crisis?: Journal of Economics, Finance and International BusinessJhon ArriagaNo ratings yet

- Love It or Hate It: American Supremacy Is Sacrosanct (Against The Motion)Document33 pagesLove It or Hate It: American Supremacy Is Sacrosanct (Against The Motion)ajay786786No ratings yet

- Economic Commssion For Latin America and The Caribbean 11Document29 pagesEconomic Commssion For Latin America and The Caribbean 11vskywokervsNo ratings yet

- Brazil Trade Liberalization ProgramDocument18 pagesBrazil Trade Liberalization ProgramMoisés MotaNo ratings yet

- Why Isn Tmexico RichDocument33 pagesWhy Isn Tmexico RicharruchaNo ratings yet

- Running Head: The U.S Economy 1Document10 pagesRunning Head: The U.S Economy 1Hillary Musembi KinyamasyoNo ratings yet

- Summary Of "The Difficult International Insertion Of Latin America" By Enrique Iglesias: UNIVERSITY SUMMARIESFrom EverandSummary Of "The Difficult International Insertion Of Latin America" By Enrique Iglesias: UNIVERSITY SUMMARIESNo ratings yet

- Perspectives of The Pacific AllianceDocument10 pagesPerspectives of The Pacific AllianceGuadalupeNo ratings yet

- Agriculture Law: RL33620Document17 pagesAgriculture Law: RL33620AgricultureCaseLawNo ratings yet

- Mexico: Country Factfile: Page 1 of 3Document3 pagesMexico: Country Factfile: Page 1 of 3Jie RongNo ratings yet

- NMIMS Global Access School For Continuing Education (NGA-SCE) Course: International Business Internal Assignment Applicable For June 2020 ExaminationDocument10 pagesNMIMS Global Access School For Continuing Education (NGA-SCE) Course: International Business Internal Assignment Applicable For June 2020 ExaminationAnkit SharmaNo ratings yet

- The Mexican Economy: Persistent Problems and New Policy Issues in The Aftermath of Market ReformsDocument14 pagesThe Mexican Economy: Persistent Problems and New Policy Issues in The Aftermath of Market ReformsjavRGNo ratings yet

- NAFTA and The Mexican Economy: A Guide To The Winners, Losers, and Administrators of Free TradeDocument16 pagesNAFTA and The Mexican Economy: A Guide To The Winners, Losers, and Administrators of Free TradeJayKarimiNo ratings yet

- Trade in The AmericasDocument29 pagesTrade in The AmericastlzarateNo ratings yet

- The US Current Account DeficitDocument5 pagesThe US Current Account DeficitturbolunaticsNo ratings yet

- Destablizing An Unstable EconomyDocument20 pagesDestablizing An Unstable EconomyfahdaliNo ratings yet

- International Finance: Trade Deficits: Bad or Good?Document12 pagesInternational Finance: Trade Deficits: Bad or Good?Yuri Walter AkiateNo ratings yet

- The North American Economies After NAFTA: A Critical AppraisalDocument23 pagesThe North American Economies After NAFTA: A Critical AppraisalSam Sep A SixtyoneNo ratings yet

- New Trade Routes: Pact Takes Pragmatic Approach To IntegrationDocument4 pagesNew Trade Routes: Pact Takes Pragmatic Approach To IntegrationAlianzadelpacificoNo ratings yet

- 20-Business With Latin American CountriesDocument20 pages20-Business With Latin American Countriesfrediz79No ratings yet

- The Economic Consequences of Globalisation in The United StatesDocument28 pagesThe Economic Consequences of Globalisation in The United StatesAsli AbaciNo ratings yet

- Trade Policies in Developing CountriesDocument11 pagesTrade Policies in Developing CountriesHsu, Fang-YuNo ratings yet

- Immigration Trends After 20 Years of NAFTADocument35 pagesImmigration Trends After 20 Years of NAFTAborisNo ratings yet

- Comercio y FronteraDocument4 pagesComercio y FronteraSheila Castillo MartínezNo ratings yet

- Drug Trafficking and Its Impact On ColombiaDocument29 pagesDrug Trafficking and Its Impact On Colombiamartinr1990No ratings yet

- Growth Without Poverty Reduction: The Case of Costa RicaDocument8 pagesGrowth Without Poverty Reduction: The Case of Costa RicaCato InstituteNo ratings yet

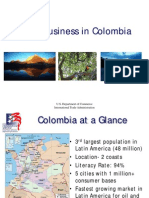

- Doing Business in Colombia September2012Document29 pagesDoing Business in Colombia September2012acmartineziiNo ratings yet

- REPORTDocument12 pagesREPORTMichael EvninNo ratings yet

- Nafta: International MarketingDocument13 pagesNafta: International Marketingbharat_agrawal_4No ratings yet

- International Journals Call For Paper HTTP://WWW - Iiste.org/journalsDocument12 pagesInternational Journals Call For Paper HTTP://WWW - Iiste.org/journalsAlexander DeckerNo ratings yet

- Summary Of "The American Crisis And The Persian Gulf War" By Pablo Pozzi: UNIVERSITY SUMMARIESFrom EverandSummary Of "The American Crisis And The Persian Gulf War" By Pablo Pozzi: UNIVERSITY SUMMARIESNo ratings yet

- Free Trade and Economic Integration in Latin America: The Evolution of a Common Market PolicyFrom EverandFree Trade and Economic Integration in Latin America: The Evolution of a Common Market PolicyNo ratings yet

- Agriculture Law: BeltzDocument36 pagesAgriculture Law: BeltzAgricultureCaseLawNo ratings yet

- Agriculture Law: CoblentzDocument22 pagesAgriculture Law: CoblentzAgricultureCaseLawNo ratings yet

- Agriculture Law: Wilson-BuzzDocument48 pagesAgriculture Law: Wilson-BuzzAgricultureCaseLawNo ratings yet

- Agriculture Law: NunezDocument10 pagesAgriculture Law: NunezAgricultureCaseLawNo ratings yet

- Agriculture Law: Harbison BiodiversityDocument20 pagesAgriculture Law: Harbison BiodiversityAgricultureCaseLawNo ratings yet

- Agriculture Law: Harbison BiodiversityDocument20 pagesAgriculture Law: Harbison BiodiversityAgricultureCaseLawNo ratings yet

- Agriculture Law: Endres SeedpurityDocument35 pagesAgriculture Law: Endres SeedpurityAgricultureCaseLawNo ratings yet

- Agriculture Law: GentryDocument5 pagesAgriculture Law: GentryAgricultureCaseLawNo ratings yet

- Agriculture Law: Dzur NuisanceimmunityDocument30 pagesAgriculture Law: Dzur NuisanceimmunityAgricultureCaseLawNo ratings yet

- Agriculture Law: McquaryDocument52 pagesAgriculture Law: McquaryAgricultureCaseLawNo ratings yet