Download as pdf or txt

You might also like

- NU - Urban Breach Handbook - TEBCDocument13 pagesNU - Urban Breach Handbook - TEBCiagaruNo ratings yet

- Hospital Management System SrsDocument71 pagesHospital Management System SrsYash Kapoor77% (13)

- Servicios en Red PDFDocument83 pagesServicios en Red PDF1312295841No ratings yet

- Banking FinanceDocument9 pagesBanking FinanceAstik TripathiNo ratings yet

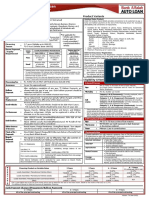

- Alfalah Auto Loan: Policy One PagerDocument1 pageAlfalah Auto Loan: Policy One PagerbilalasifNo ratings yet

- Customer Agreement Cash Management and Additional InformationDocument88 pagesCustomer Agreement Cash Management and Additional InformationRaul CruzNo ratings yet

- Money and Commercial BankingDocument8 pagesMoney and Commercial BankingMH SahirNo ratings yet

- Part Vi:Trust Receipts LawDocument5 pagesPart Vi:Trust Receipts LawThrees SeeNo ratings yet

- HofR Challenge To ACA DCT 5-12-16Document38 pagesHofR Challenge To ACA DCT 5-12-16John HinderakerNo ratings yet

- SecuritisationDocument74 pagesSecuritisationrohitpatil699No ratings yet

- U.S. V JPMorgan Chase 17-00347 (S.D.N.Y) (D.E. 8) Joint Consent OrderDocument15 pagesU.S. V JPMorgan Chase 17-00347 (S.D.N.Y) (D.E. 8) Joint Consent Orderlarry-612445No ratings yet

- Banking TermsDocument6 pagesBanking TermsvenkateshrachaNo ratings yet

- Are Student Loans Considered Revolving DebtsDocument3 pagesAre Student Loans Considered Revolving Debtsfemi adeNo ratings yet

- Banking Guide For Overseas TravelDocument20 pagesBanking Guide For Overseas TravelLagi Cabe100% (1)

- Off-Balance Sheet ActivitiesDocument21 pagesOff-Balance Sheet ActivitiesblahblahblueNo ratings yet

- Presentation Beneficial OwnershipDocument10 pagesPresentation Beneficial OwnershipNat AliaNo ratings yet

- Bank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoDocument3 pagesBank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoKyle PanlaquiNo ratings yet

- Chattel Mortgage LawDocument5 pagesChattel Mortgage LawApril Roween AranzaNo ratings yet

- Finance For Everyone Assignment Roahan 1099Document10 pagesFinance For Everyone Assignment Roahan 1099Natho100% (1)

- 8 Get Your Finances & Credit in OrderDocument15 pages8 Get Your Finances & Credit in OrdercropdownunderNo ratings yet

- Negotiable Instruments: Commercial PaperDocument45 pagesNegotiable Instruments: Commercial PaperSimranNo ratings yet

- 2P How Banks Create MoneyDocument28 pages2P How Banks Create MoneyNguyen Vu Thuc Uyen (K17 QN)No ratings yet

- Banks and Bank DetailsDocument3 pagesBanks and Bank DetailsDeepa KrishnamurthyNo ratings yet

- Financial LiteracyDocument7 pagesFinancial LiteracyRochelle Ann Galvez Gabaldon100% (1)

- Bills Discounting: Dr. Sarbesh Mishra, Finance AreaDocument9 pagesBills Discounting: Dr. Sarbesh Mishra, Finance AreaDr Sarbesh MishraNo ratings yet

- Characteristics of Negotiable InstrumentsDocument12 pagesCharacteristics of Negotiable InstrumentsSiddh Shah ⎝⎝⏠⏝⏠⎠⎠No ratings yet

- Deposit SlipDocument1 pageDeposit SlipHabibie GunawanNo ratings yet

- Training Material ContractsDocument308 pagesTraining Material ContractsRachel SibandaNo ratings yet

- Pooling & Service Agreement - 1Document241 pagesPooling & Service Agreement - 1Knowledge GuruNo ratings yet

- Rules On EvidenceDocument17 pagesRules On Evidenceneil_nailNo ratings yet

- Apple 424B2 For International BondDocument70 pagesApple 424B2 For International BondMike WuertheleNo ratings yet

- Compensation From FundsDocument3 pagesCompensation From FundsylessinNo ratings yet

- Fraud Asuransi KesehatanDocument9 pagesFraud Asuransi KesehatanOlivia JosianaNo ratings yet

- Do-Did Mortgage Backed SecuritiesDocument1 pageDo-Did Mortgage Backed SecuritiesA. CampbellNo ratings yet

- Business Glossary SBADocument8 pagesBusiness Glossary SBADonald DuckNo ratings yet

- SF 424 (R&R) : Application For Federal AssistanceDocument32 pagesSF 424 (R&R) : Application For Federal AssistancebrunoNo ratings yet

- Characteristic of Bond: Financial Management 2Document4 pagesCharacteristic of Bond: Financial Management 2zarfarie aronNo ratings yet

- Assignments: Banking and FinanceDocument19 pagesAssignments: Banking and FinanceAamir Hussian100% (1)

- Assignment 5 - Wrongful DismissalDocument3 pagesAssignment 5 - Wrongful DismissalAraceli Gloria-Francisco100% (1)

- Instructions For Completing Form SI-100Document2 pagesInstructions For Completing Form SI-100ronin4uNo ratings yet

- BassDrill Alpha - Information MemorandumDocument90 pagesBassDrill Alpha - Information MemorandumAnbuNo ratings yet

- Eport:: Toxic Document Fallout ImpactsDocument21 pagesEport:: Toxic Document Fallout ImpactsRichard Franklin Kessler100% (1)

- Blocked Account Contract DetailsDocument13 pagesBlocked Account Contract Detailsshahzeel khanNo ratings yet

- What Is A BankDocument5 pagesWhat Is A BankmanojdunnhumbyNo ratings yet

- Treasury-International-Bill Ofexchange - BlankDocument3 pagesTreasury-International-Bill Ofexchange - BlankLee BosemanNo ratings yet

- Coinmint vs. Ashton Soniat Fraud CaseDocument8 pagesCoinmint vs. Ashton Soniat Fraud CaseDon HewlettNo ratings yet

- Topic ReviewDocument11 pagesTopic ReviewNguyen Thi Bich NgocNo ratings yet

- Banking LawsDocument33 pagesBanking LawsliboaninoNo ratings yet

- Offer or Tender of PerformanceDocument7 pagesOffer or Tender of PerformanceWeiNo ratings yet

- Money BankingDocument27 pagesMoney BankingParesh ShrivastavaNo ratings yet

- Warehouse Law, Trust Receipt (SPL)Document12 pagesWarehouse Law, Trust Receipt (SPL)Marjorie MayordoNo ratings yet

- Jorg Guido Hulsmann - Legal Tender Laws and Fractional Reserve Banking (2004)Document23 pagesJorg Guido Hulsmann - Legal Tender Laws and Fractional Reserve Banking (2004)Ragnar DanneskjoldNo ratings yet

- Investment Opportunities or A Study in The Context of BangladeshDocument12 pagesInvestment Opportunities or A Study in The Context of BangladeshOpen NokuNo ratings yet

- Illinois Freedom of Information Act (FOIA) : Frequently Asked Questions by The PublicDocument12 pagesIllinois Freedom of Information Act (FOIA) : Frequently Asked Questions by The PublicletscurecancerNo ratings yet

- Center For Economic Justice - Written Comments To TDIDocument13 pagesCenter For Economic Justice - Written Comments To TDITexas WatchNo ratings yet

- A Private Investor's Guide To GiltsDocument36 pagesA Private Investor's Guide To GiltsFuzzy_Wood_PersonNo ratings yet

- Econ 103 Money and Banking - Dr. Douglas Rice Week 14 Lecture - Asset-Backed SecuritiesDocument3 pagesEcon 103 Money and Banking - Dr. Douglas Rice Week 14 Lecture - Asset-Backed Securitiesvkapsz100% (1)

- Securitization SubprimeCrisisDocument5 pagesSecuritization SubprimeCrisisNiraj MohanNo ratings yet

- United States Savings Bonds: Jump To Navigation Jump To SearchDocument6 pagesUnited States Savings Bonds: Jump To Navigation Jump To SearchJonah100% (1)

- 5 Ga. Jur. UCC 4:3: 4:3. Draft or Bill of Exchange As Negotiable InstrumentDocument2 pages5 Ga. Jur. UCC 4:3: 4:3. Draft or Bill of Exchange As Negotiable InstrumentTheplaymaker508No ratings yet

- The Declaration of Independence: A Play for Many ReadersFrom EverandThe Declaration of Independence: A Play for Many ReadersNo ratings yet

- Safe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesFrom EverandSafe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesNo ratings yet

- 2nd Quarter Exam Gen MathDocument5 pages2nd Quarter Exam Gen Mathargie joy marie100% (1)

- VCH Pew w19 Cultural Responsiveness - Asian AmDocument17 pagesVCH Pew w19 Cultural Responsiveness - Asian Amapi-235454491No ratings yet

- APFBC JFMC EDC Operational Manual (Assam)Document119 pagesAPFBC JFMC EDC Operational Manual (Assam)poNo ratings yet

- 555 Timer DoctronicsDocument18 pages555 Timer DoctronicsGaneshVenkatachalamNo ratings yet

- Rustys 3inch Lift Kit Installation RK-300SP-XJDocument2 pagesRustys 3inch Lift Kit Installation RK-300SP-XJnorthernscribdNo ratings yet

- Banner Workflow Modeler OverviewDocument2 pagesBanner Workflow Modeler OverviewArshad HussainNo ratings yet

- Opatch Auto Fails With: Can't Locate Switch - PM in @INC (Doc ID 1915430.1)Document2 pagesOpatch Auto Fails With: Can't Locate Switch - PM in @INC (Doc ID 1915430.1)vnairajNo ratings yet

- Use To Show An Exact Time: - Two O'clock - Midnight / Noon - The Moment, EtcDocument3 pagesUse To Show An Exact Time: - Two O'clock - Midnight / Noon - The Moment, EtcKasira PammpersNo ratings yet

- Manual de Usuario Ph-MetroDocument16 pagesManual de Usuario Ph-Metrojuan alejandro moyaNo ratings yet

- ACN Micro Project-1Document23 pagesACN Micro Project-1ashutosh dudhaneNo ratings yet

- Aerofoam Tapes Catalogue PDFDocument32 pagesAerofoam Tapes Catalogue PDFChloe ChuengNo ratings yet

- ABC BraceletsDocument13 pagesABC BraceletsCintaNo ratings yet

- Nx-Osv 9000 Guide: Americas HeadquartersDocument58 pagesNx-Osv 9000 Guide: Americas HeadquartersBobNo ratings yet

- Company Registration PPT Module 5Document3 pagesCompany Registration PPT Module 5Anonymous uxd1ydNo ratings yet

- RAB Perkuatan Bank Permata JatinegaraDocument37 pagesRAB Perkuatan Bank Permata Jatinegarabastian hidayatullohNo ratings yet

- Lec006 - Measures of DispersionDocument42 pagesLec006 - Measures of DispersionTiee TieeNo ratings yet

- CIT, Kolkata V Smifs SecuritiesDocument4 pagesCIT, Kolkata V Smifs SecuritiesBar & BenchNo ratings yet

- MC 110Document5 pagesMC 110Rachel Erica Guillero BuesingNo ratings yet

- Made Easy-ECDocument33 pagesMade Easy-ECb prashanthNo ratings yet

- Rudolf Elmer's Complaint To The ECHR v. Jersey (Standard Bank)Document13 pagesRudolf Elmer's Complaint To The ECHR v. Jersey (Standard Bank)David LeloupNo ratings yet

- Marketing Project ON STPDocument20 pagesMarketing Project ON STPajay klumarNo ratings yet

- Demand ForecastingDocument20 pagesDemand ForecastingShahbaz Ahmed AfsarNo ratings yet

- New DOH Hospital Classifications 2015: GovernmentDocument3 pagesNew DOH Hospital Classifications 2015: GovernmentCatherine PurisimaNo ratings yet

- Servicemanual Panasonic kv-s2087 s1Document5 pagesServicemanual Panasonic kv-s2087 s1Ralf KöhlerNo ratings yet

- ACI Basic - LEARN WORK ITDocument12 pagesACI Basic - LEARN WORK ITravi kantNo ratings yet

- Chap 2Document6 pagesChap 2Renier FloresNo ratings yet

- Mikrotik Products PresentationDocument85 pagesMikrotik Products PresentationinnovativekaluNo ratings yet