Download as pdf or txt

You might also like

- Indian and Modern Power SystemDocument53 pagesIndian and Modern Power SystemNRPP OPERATIONNo ratings yet

- Electricity Act and Regulatory FrameDocument75 pagesElectricity Act and Regulatory Frameucb2_ntpcNo ratings yet

- Power ScenarioDocument37 pagesPower ScenarioSupervisor CCCNo ratings yet

- Bec BagalkotDocument57 pagesBec BagalkotharishNo ratings yet

- ViceministroDocument21 pagesViceministroHivaNo ratings yet

- Indian Power Sector: India Has A FEDERAL Structure Electricity A Concurrent Subject - Both CentralDocument23 pagesIndian Power Sector: India Has A FEDERAL Structure Electricity A Concurrent Subject - Both CentralShubham GuptaNo ratings yet

- Energy Sector and InfrastructureDocument95 pagesEnergy Sector and InfrastructureDharmvirNo ratings yet

- Power Reg&EA2003 (Autosaved)Document104 pagesPower Reg&EA2003 (Autosaved)pintu ramNo ratings yet

- Sector PowerDocument4 pagesSector PowerLilanand ChaudharyNo ratings yet

- Energy Conservation (ESL 720)Document39 pagesEnergy Conservation (ESL 720)ashuteriNo ratings yet

- Indian Power Sector and RE - JMI - 2019Document74 pagesIndian Power Sector and RE - JMI - 2019AJKNo ratings yet

- Power Sector Scenario in India: Krishna Murari (009909) Dhiraj Arora (009915) Ranjan Kumar (009949) B.Subhakar (009910)Document38 pagesPower Sector Scenario in India: Krishna Murari (009909) Dhiraj Arora (009915) Ranjan Kumar (009949) B.Subhakar (009910)SamNo ratings yet

- Indian Power Sector and RE - JMI'19Document74 pagesIndian Power Sector and RE - JMI'19AJKNo ratings yet

- Power Generation Sectorin Pakistan by Research Publications DepartmentDocument1 pagePower Generation Sectorin Pakistan by Research Publications Departmentrameez ullahNo ratings yet

- System Operations Through National & Regional Load Dispatch CentresDocument47 pagesSystem Operations Through National & Regional Load Dispatch CentreshughcabNo ratings yet

- Group 9 - Electricity Act 2003Document20 pagesGroup 9 - Electricity Act 2003Kinshuk ChoukseyNo ratings yet

- IAS Trainee 20.01.2023Document42 pagesIAS Trainee 20.01.2023Chairman PUNo ratings yet

- Equipment Supply To Power Projects National Power Conference 2009Document58 pagesEquipment Supply To Power Projects National Power Conference 2009kartheekreNo ratings yet

- Energy Sector ReportDocument23 pagesEnergy Sector Reportrishabhluthra2003No ratings yet

- 1 - Demand Supply BalancingDocument37 pages1 - Demand Supply BalancingTaniyaNo ratings yet

- All About The EA2003Document44 pagesAll About The EA2003Sonal ChoudharyNo ratings yet

- Dist Scenario& IEact2003Document22 pagesDist Scenario& IEact2003gaurang1111No ratings yet

- Erc DPC Presn 031A01Document28 pagesErc DPC Presn 031A01Anh NguyễnNo ratings yet

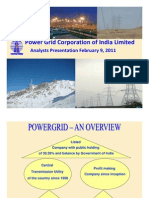

- Power Grid Corporation of India Limited: Analysts Presentation February 9, 2011Document18 pagesPower Grid Corporation of India Limited: Analysts Presentation February 9, 2011Amarpreet SinghNo ratings yet

- File 395Document88 pagesFile 395asim204No ratings yet

- Power Sector IndiaDocument54 pagesPower Sector IndiaIrfanNo ratings yet

- IEX Indian Power Sector Overview-130709Document57 pagesIEX Indian Power Sector Overview-130709ASHISHNo ratings yet

- Power Sector Indian ScenarioDocument98 pagesPower Sector Indian ScenarioJaganathan ChokkalingamNo ratings yet

- Annual Report (2007-08) - Ministry of PowerDocument204 pagesAnnual Report (2007-08) - Ministry of Powerabhikdb100% (1)

- MES Current Status and Opportunity in Electric Power Sector MyanmarDocument24 pagesMES Current Status and Opportunity in Electric Power Sector MyanmarAh KarNo ratings yet

- Utility OverviewDocument10 pagesUtility OverviewDon BunNo ratings yet

- 2007+ar P - 51 76Document26 pages2007+ar P - 51 76John Israel CorpusNo ratings yet

- EPIRA and Othe EE LawsDocument64 pagesEPIRA and Othe EE LawsjporangecubeNo ratings yet

- Wind Energy 2Document26 pagesWind Energy 2DhammikaDharmasenaNo ratings yet

- Green Paper Vol-1 (V 2 January 12, 2015)Document37 pagesGreen Paper Vol-1 (V 2 January 12, 2015)humane28No ratings yet

- PTD ProjectDocument13 pagesPTD Project2K18/EE/026 ANGAD SINGH NAGINo ratings yet

- 02 Policy Regulatory Mechanisms Renewable Energy Integration in The Buildings SectorDocument21 pages02 Policy Regulatory Mechanisms Renewable Energy Integration in The Buildings SectorSubramaniam ChandrasekaranNo ratings yet

- Energy Systems of PakistanDocument95 pagesEnergy Systems of PakistanMuhammad Haris HamayunNo ratings yet

- Power Sector: Equity Research Report OnDocument31 pagesPower Sector: Equity Research Report OnMandar NavareNo ratings yet

- Electrical RegulationDocument73 pagesElectrical RegulationSuresh Zanwar0% (1)

- 2 - Emerging Market Scenario in Power Sector - Anoop SinghDocument15 pages2 - Emerging Market Scenario in Power Sector - Anoop SinghTapan Rishi BhatnagarNo ratings yet

- The Indian Power SectorDocument38 pagesThe Indian Power SectornbdvNo ratings yet

- Geothermal Power Development: Presentation To Institutional Investor Africa Investment ConferenceDocument16 pagesGeothermal Power Development: Presentation To Institutional Investor Africa Investment ConferenceKenya Ict BoardNo ratings yet

- Energy Crisis in NigeriaDocument9 pagesEnergy Crisis in NigeriaCharles Romeo Duru100% (1)

- Overview of Energy Systems in Northern CyprusDocument6 pagesOverview of Energy Systems in Northern CyprushaspyNo ratings yet

- Vietnam Wind Power Development Plan: Grid, Dppa and Renewable Energy PlanningDocument16 pagesVietnam Wind Power Development Plan: Grid, Dppa and Renewable Energy PlanningLuong Thu HaNo ratings yet

- Implementation of Energy Conservation Act and BEE Action PlanDocument33 pagesImplementation of Energy Conservation Act and BEE Action PlanRohan PrakashNo ratings yet

- Current Scenario of Electricity Sector in India and RestructuringDocument7 pagesCurrent Scenario of Electricity Sector in India and RestructuringIbon KatakiNo ratings yet

- Chapter One: 1.1 Background of The StudyDocument45 pagesChapter One: 1.1 Background of The StudysamNo ratings yet

- Countrywide Power Failure Inquiry Report by NEPRADocument29 pagesCountrywide Power Failure Inquiry Report by NEPRAfaarigNo ratings yet

- NTDC and CTBCM 10JAN2020 For UploadingOnWebDocument39 pagesNTDC and CTBCM 10JAN2020 For UploadingOnWebkinir88566No ratings yet

- 1 - PSA Lecture 1-2Document32 pages1 - PSA Lecture 1-2Irtaza MazharNo ratings yet

- Brief Report On NTPCDocument7 pagesBrief Report On NTPCChandra ShekharNo ratings yet

- Transmission in IndiaDocument36 pagesTransmission in IndiaMuhammad AdilNo ratings yet

- (Introduction To Grid Station Operation and Management) : Dr. Sasidharan SreedharanDocument99 pages(Introduction To Grid Station Operation and Management) : Dr. Sasidharan SreedharanSher AliNo ratings yet

- TP 53 Tariff Order & MYT ARR& ERC KINFRA-2008-09 To 2010-11Document26 pagesTP 53 Tariff Order & MYT ARR& ERC KINFRA-2008-09 To 2010-11Thejus RamachandranNo ratings yet

- Doubly-Fed Induction Generator PresentationDocument25 pagesDoubly-Fed Induction Generator PresentationDolcera100% (1)

- L7 Legislations and Policies Supporting DSM in IndiaDocument28 pagesL7 Legislations and Policies Supporting DSM in IndiaVaibhav BairathiNo ratings yet

- Nuclear Energy Now: Why the Time Has Come for the World's Most Misunderstood Energy SourceFrom EverandNuclear Energy Now: Why the Time Has Come for the World's Most Misunderstood Energy SourceNo ratings yet

- WP 2 Report Attetitudes Ownership and Use of Electric Vehicles A Review of LiteratureDocument48 pagesWP 2 Report Attetitudes Ownership and Use of Electric Vehicles A Review of LiteraturesridharkckNo ratings yet

- Breakthrough FactorDocument9 pagesBreakthrough FactorsridharkckNo ratings yet

- Progress in Next-Generation Photovoltaic DevicesDocument23 pagesProgress in Next-Generation Photovoltaic DevicessridharkckNo ratings yet

- Where Are We Today in y Research in Photovoltaics ?Document48 pagesWhere Are We Today in y Research in Photovoltaics ?sridharkckNo ratings yet

- 08dir RdiDocument114 pages08dir RdisridharkckNo ratings yet

- 2009 APMA ReportDocument2 pages2009 APMA ReportsridharkckNo ratings yet

- 44Document52 pages44sridharkckNo ratings yet

- Fuel Cells and Electrochemical Technology: Chemical Sciences & EngineeringDocument4 pagesFuel Cells and Electrochemical Technology: Chemical Sciences & EngineeringsridharkckNo ratings yet

- GEECLDocument1 pageGEECLsridharkckNo ratings yet

- CS20 12io1Document4 pagesCS20 12io1Raul E. SoliNo ratings yet

- CPX21146T Customer Information PacketDocument11 pagesCPX21146T Customer Information Packetrrobles011No ratings yet

- MANUAL SENSOR DE NIVEL sv115230Document2 pagesMANUAL SENSOR DE NIVEL sv115230Juan GuzmanNo ratings yet

- Maz8120 L PDFDocument5 pagesMaz8120 L PDFMarcelo DominguezNo ratings yet

- Construction & Operation of Some Simple Electrical Circuits: Name of The ExperimentDocument7 pagesConstruction & Operation of Some Simple Electrical Circuits: Name of The ExperimentSayeed MohammedNo ratings yet

- Sugna Electrical Shift ReportDocument11 pagesSugna Electrical Shift ReportAmbati Siva Kumar ReddyNo ratings yet

- Generator ProtectionDocument10 pagesGenerator ProtectionVirendra SinghNo ratings yet

- EQU - For Ex - ProtectaDocument2 pagesEQU - For Ex - ProtectaAkhilesh KumarNo ratings yet

- Srds Document 2 LatestDocument266 pagesSrds Document 2 LatestPhilvic Nkonga100% (1)

- Hybrid Electrical Vehicles and Its Environmental and Economical ImpactsDocument20 pagesHybrid Electrical Vehicles and Its Environmental and Economical ImpactsTesterNo ratings yet

- 521G, 621G, 721G, 821G, 921G, 1021G, 1121G Wheel Loader ElectricalDocument6 pages521G, 621G, 721G, 821G, 921G, 1021G, 1121G Wheel Loader ElectricalEl Perro100% (1)

- 421DG180A01Document51 pages421DG180A01Atiq_2909No ratings yet

- Instructions - Sun 12 16k sg01lp1 Eu - 240203 - enDocument48 pagesInstructions - Sun 12 16k sg01lp1 Eu - 240203 - enf789sgacanonNo ratings yet

- Electric Motor Boat ProjectDocument2 pagesElectric Motor Boat ProjectVinoth KumarNo ratings yet

- Electrification Using Decentralized Micro-Hydro PoDocument18 pagesElectrification Using Decentralized Micro-Hydro Posinamohammadali88No ratings yet

- 11kv RMU SpecDocument21 pages11kv RMU SpecHappi Gwegweni100% (2)

- Performance Evaluation of Proposed On-Grid Solar PV System: XXX-X-XXXX-XXXX-X/XX/$XX.00 ©20XX IEEEDocument11 pagesPerformance Evaluation of Proposed On-Grid Solar PV System: XXX-X-XXXX-XXXX-X/XX/$XX.00 ©20XX IEEEبلال شبیرNo ratings yet

- R6045e MavsDocument9 pagesR6045e MavsMUHAMMAD FAHMINo ratings yet

- S NubberDocument5 pagesS NubberSunilNo ratings yet

- Seminar Report On PLCCDocument17 pagesSeminar Report On PLCCsubhrajitNo ratings yet

- Residential Wiring GuideDocument31 pagesResidential Wiring Guidestingrae100% (2)

- Silent SentinelsDocument75 pagesSilent Sentinelscristian kelvinNo ratings yet

- Presco: Partial Discharge Measuring SystemsDocument17 pagesPresco: Partial Discharge Measuring SystemsRatheesh KumarNo ratings yet

- Electronic TransformersDocument32 pagesElectronic TransformersKhaled RabeaNo ratings yet

- Micom P591, P592, P593: Technical ManualDocument90 pagesMicom P591, P592, P593: Technical ManualMohd Izat KhuzaimiNo ratings yet

- General Requirements For Electrical InstallationDocument22 pagesGeneral Requirements For Electrical InstallationDomingo ParayaoanNo ratings yet

- S12 ManualDocument85 pagesS12 Manualวรพงษ์ กอชัชวาลNo ratings yet

- DazerDocument4 pagesDazerjhlaiNo ratings yet

- ETAP User GuideDocument4,762 pagesETAP User Guidebaskaranjay5502100% (11)

- 2019 09 - Data Sheet Smart Transport Zen 35 - ENDocument2 pages2019 09 - Data Sheet Smart Transport Zen 35 - ENYann ElhamNo ratings yet