Download as pdf or txt

You might also like

- Mortgage Lab Signature AssignmentDocument3 pagesMortgage Lab Signature Assignmentapi-518277133No ratings yet

- Complaint Foreclosure With Restitution CoaDocument28 pagesComplaint Foreclosure With Restitution Coajoelacostaesq100% (1)

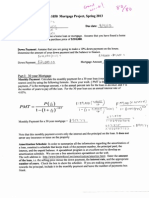

- Math 1050 Mortgage ProjectDocument5 pagesMath 1050 Mortgage Projectapi-278070559100% (1)

- Math 1050 ProjectDocument5 pagesMath 1050 Projectapi-316746947No ratings yet

- Alexander Van Dyke Math 1050 Project 2 - Mortgage CostsDocument5 pagesAlexander Van Dyke Math 1050 Project 2 - Mortgage Costsapi-233311543No ratings yet

- Math 1050 ProjectDocument5 pagesMath 1050 Projectapi-267005931No ratings yet

- Scan 1Document5 pagesScan 1api-253014327No ratings yet

- Buy A House Staci CobabeDocument4 pagesBuy A House Staci Cobabeapi-122605596No ratings yet

- Mortgage ProjectDocument5 pagesMortgage Projectapi-300458382No ratings yet

- Math 1050 Mortgage ProjectDocument5 pagesMath 1050 Mortgage Projectapi-317485992No ratings yet

- Img 20160504 0002 NewDocument5 pagesImg 20160504 0002 Newapi-285003644No ratings yet

- Img 20150804 0001Document5 pagesImg 20150804 0001api-273558871No ratings yet

- Math 1050 ProjectDocument5 pagesMath 1050 Projectapi-291900408No ratings yet

- Math1050 Mortgage ProjectDocument5 pagesMath1050 Mortgage Projectapi-218606359No ratings yet

- Mortgage Math 1050Document5 pagesMortgage Math 1050api-248061121No ratings yet

- MathDocument4 pagesMathapi-317213984No ratings yet

- Mortgage ProjectDocument5 pagesMortgage Projectapi-295873560No ratings yet

- Anthonyhepworthm 1050 MortgageprjctDocument5 pagesAnthonyhepworthm 1050 Mortgageprjctapi-289280166No ratings yet

- Penny Gwynn Math Project 2Document5 pagesPenny Gwynn Math Project 2api-272827235No ratings yet

- Math 1050 ProjectDocument5 pagesMath 1050 Projectapi-340276222No ratings yet

- Math Mortgage ProjectDocument6 pagesMath Mortgage Projectapi-240088823No ratings yet

- Mitchell Walker e Portfollio Mortgage ProjDocument5 pagesMitchell Walker e Portfollio Mortgage Projapi-275156411No ratings yet

- Sami Walker Math 1050 Mortgage ProjectDocument5 pagesSami Walker Math 1050 Mortgage Projectapi-275218566No ratings yet

- Mortgage ProjectDocument5 pagesMortgage ProjectwillmssherNo ratings yet

- Img 0003Document1 pageImg 0003api-240362059No ratings yet

- Img 0004Document1 pageImg 0004api-242216222No ratings yet

- Img 0001Document1 pageImg 0001api-242216222No ratings yet

- MP 1Document1 pageMP 1api-242203860No ratings yet

- Img 20150706 0007Document1 pageImg 20150706 0007api-288625007No ratings yet

- Project 2Document5 pagesProject 2api-246579738No ratings yet

- Img 20150706 0006Document1 pageImg 20150706 0006api-288625007No ratings yet

- MortgageprojectDocument5 pagesMortgageprojectapi-305916910No ratings yet

- Img 20150706 0003Document1 pageImg 20150706 0003api-288625007No ratings yet

- MortgagelabDocument5 pagesMortgagelabapi-232312177No ratings yet

- Final MortgageDocument5 pagesFinal Mortgageapi-301270815No ratings yet

- Img 20150706 0005Document1 pageImg 20150706 0005api-288625007No ratings yet

- Math 1050 Mortgage ProjectDocument5 pagesMath 1050 Mortgage Projectapi-2740249620% (1)

- Mortgage Project 1Document5 pagesMortgage Project 1api-284831231No ratings yet

- 1050 WordDocument6 pages1050 Wordapi-352291519No ratings yet

- Img 20150706 0004Document1 pageImg 20150706 0004api-288625007No ratings yet

- M1030-Buying A House - F16Document5 pagesM1030-Buying A House - F16Kaylah GolderNo ratings yet

- Math1050 - MortgagelabDocument5 pagesMath1050 - Mortgagelabapi-424955946No ratings yet

- R - IA - T: CF#T#F, G. Q/ici (Document1 pageR - IA - T: CF#T#F, G. Q/ici (api-240362059No ratings yet

- Math 1050 Mortgage Project: Show Work HereDocument5 pagesMath 1050 Mortgage Project: Show Work Hereapi-302479969No ratings yet

- M1050mortgagelab 1Document5 pagesM1050mortgagelab 1api-302779278No ratings yet

- ADM 2350 Winter 2014 Assign 1 RevDocument4 pagesADM 2350 Winter 2014 Assign 1 RevWall JohnNo ratings yet

- Img 20161025 0003Document1 pageImg 20161025 0003api-298901459No ratings yet

- Mortgage Project P 2Document1 pageMortgage Project P 2api-232442742No ratings yet

- SolutionsDocument30 pagesSolutionsNitesh AgrawalNo ratings yet

- Part 1Document2 pagesPart 1api-282191219No ratings yet

- Math 1050 Mortgage ProjectDocument7 pagesMath 1050 Mortgage Projectapi-253957931No ratings yet

- KWK 4th Append DDocument6 pagesKWK 4th Append DAnonymous O5asZmNo ratings yet

- Img 0002Document1 pageImg 0002api-242216222No ratings yet

- Mortgage Project PDFDocument9 pagesMortgage Project PDFapi-302132755No ratings yet

- Mortgage Lab Reflective WritingDocument5 pagesMortgage Lab Reflective Writinghailey richmanNo ratings yet

- Chap 1 MathscapeDocument31 pagesChap 1 MathscapeHarry LiuNo ratings yet

- Time Value MoneyDocument9 pagesTime Value MoneySharmin ReulaNo ratings yet

- UpdatedCollegeAlgebraProjectBOLS3 11Document5 pagesUpdatedCollegeAlgebraProjectBOLS3 11shirazasadNo ratings yet

- Rental-Property Profits: A Financial Tool Kit for LandlordsFrom EverandRental-Property Profits: A Financial Tool Kit for LandlordsNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- Q.V. Ramirez Vs CA - MamugayDocument1 pageQ.V. Ramirez Vs CA - MamugayIan Van MamugayNo ratings yet

- What Is An Amortization Schedule?Document7 pagesWhat Is An Amortization Schedule?Godfrey KakalaNo ratings yet

- Credit Transactions - PNB Vs MallorcaDocument2 pagesCredit Transactions - PNB Vs MallorcaJp tan britoNo ratings yet

- Do American Consumers Need A Financial Protection Agency?: E: 2.4 Kevin MeskillDocument6 pagesDo American Consumers Need A Financial Protection Agency?: E: 2.4 Kevin MeskillKevinNo ratings yet

- AnubhavbaseratepptDocument12 pagesAnubhavbaseratepptChandan SinghNo ratings yet

- Subprime Mortgage CrisisDocument41 pagesSubprime Mortgage CrisisRinkesh ShrishrimalNo ratings yet

- Personal Loan ProjectDocument7 pagesPersonal Loan ProjectSudhakar GuntukaNo ratings yet

- FA19-BCS-152 Suleman SohailDocument5 pagesFA19-BCS-152 Suleman SohailNew Age Electronics OfficialNo ratings yet

- F038-Deed of Sale With Assumption of MortgageDocument2 pagesF038-Deed of Sale With Assumption of MortgageMark Jhon PasamonNo ratings yet

- CH 05Document40 pagesCH 05saeed75.ksaNo ratings yet

- Amortization ScheduleDocument8 pagesAmortization ScheduleCamoColtonNo ratings yet

- Formula Gen MathDocument2 pagesFormula Gen MathGod SerenaNo ratings yet

- Good Short Basic Guide To CMBS Conduit Loans 4PgDocument4 pagesGood Short Basic Guide To CMBS Conduit Loans 4PgKapil Agrawal0% (1)

- FINACC1 3rd LQDocument3 pagesFINACC1 3rd LQco230154No ratings yet

- Sample 1 PDFDocument45 pagesSample 1 PDFChicagoCitizens EmpowermentGroupNo ratings yet

- Quiz 3 Chapter 6 Multiple Choice - F2020 - BBDocument10 pagesQuiz 3 Chapter 6 Multiple Choice - F2020 - BBHeba OmarNo ratings yet

- 85Document58 pages85damnrod23100% (1)

- Loan Agreement Document of $100,000.00 USDDocument3 pagesLoan Agreement Document of $100,000.00 USDUniverse Loan Company LimtedNo ratings yet

- Check List For Creation of MortgageDocument2 pagesCheck List For Creation of MortgageAmmy MaverickNo ratings yet

- Aurora Loan Services, LLC, V. Judith Mendes Da CostaDocument5 pagesAurora Loan Services, LLC, V. Judith Mendes Da CostaForeclosure Fraud100% (1)

- Amortization and Sinking FundsDocument46 pagesAmortization and Sinking FundssaneconNo ratings yet

- BPLR & Base RateDocument25 pagesBPLR & Base Ratemermaid20052002No ratings yet

- Mortgage Broker Fee AgreementDocument2 pagesMortgage Broker Fee AgreementRohit WankhedeNo ratings yet

- CIBIL - 1st FEB, '23 PDFDocument38 pagesCIBIL - 1st FEB, '23 PDFSamir Kumar DashNo ratings yet

- Simple Loan Calculator: Loan Values Loan SummaryDocument11 pagesSimple Loan Calculator: Loan Values Loan Summarysanju sanjuNo ratings yet

- Birla Institute of Management Technology Case Study Report On Structuring Credit Lines For A BorrowerDocument3 pagesBirla Institute of Management Technology Case Study Report On Structuring Credit Lines For A Borrowerlavish mehtaNo ratings yet

- Simple Interest Loan CalculatorDocument44 pagesSimple Interest Loan CalculatorAMITSSSSNo ratings yet

- CH 14 Utang Wesel & Hipotek KiesoDocument19 pagesCH 14 Utang Wesel & Hipotek KiesoAlamsyah Arga100% (1)

- SBI Maxgain-AdvantageDocument5 pagesSBI Maxgain-Advantageavabhyankar9393No ratings yet