Download as pdf

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Trade Chart Patterns Like The Pros-Suri DuddellaDocument293 pagesTrade Chart Patterns Like The Pros-Suri DuddellaEl Cuz100% (12)

- Hit and Run TradingDocument170 pagesHit and Run Tradingmr.ajeetsingh97% (34)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The New Technical TraderDocument115 pagesThe New Technical Tradermr.ajeetsinghNo ratings yet

- Inner CircleDocument96 pagesInner Circlemr.ajeetsingh20% (5)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Mastering Adjusting Entries Testbank AnswersDocument6 pagesMastering Adjusting Entries Testbank AnswersGianna Chloe S Victoria75% (4)

- Predictive Indicators For Effective Trading Strategies - John Ehlers - MESA SoftwareDocument13 pagesPredictive Indicators For Effective Trading Strategies - John Ehlers - MESA SoftwareInterconti Ltd.100% (2)

- Simple and Consistent Fibonacci MethodDocument22 pagesSimple and Consistent Fibonacci MethodJackson TraceNo ratings yet

- MonicKorzecForexMKStrendlines PDFDocument130 pagesMonicKorzecForexMKStrendlines PDFPorfirio MorilloNo ratings yet

- Walker, Myles Wilson - How To Indentify High-Profit Elliott Wave Trades in Real Time PDFDocument203 pagesWalker, Myles Wilson - How To Indentify High-Profit Elliott Wave Trades in Real Time PDFPaul Celen100% (11)

- Bank Nifty Option Strategies BookletDocument28 pagesBank Nifty Option Strategies BookletMohit Jhanjee100% (1)

- Circular Entitled RN Lax And: LocalDocument6 pagesCircular Entitled RN Lax And: Localjoseph iii goNo ratings yet

- Truth About Fibonacci TradingDocument23 pagesTruth About Fibonacci Tradingmr.ajeetsingh100% (1)

- The Price Doctor Part-1Document9 pagesThe Price Doctor Part-1mr.ajeetsinghNo ratings yet

- Options Made EasyDocument116 pagesOptions Made Easymr.ajeetsingh100% (1)

- Scalping MethodsDocument4 pagesScalping Methodsmr.ajeetsingh100% (1)

- Teoria de FibonacciDocument31 pagesTeoria de FibonacciRamón Alfredo AmadoNo ratings yet

- Technical AnalysisDocument111 pagesTechnical Analysisapi-3803915100% (10)

- Option Trading StrategiesDocument59 pagesOption Trading StrategiesTarun Goel100% (4)

- 4 Hour MACD Forex StrategyDocument20 pages4 Hour MACD Forex Strategymr.ajeetsingh100% (1)

- Introduction To Managerial Accounting and Job Order Cost SystemsDocument57 pagesIntroduction To Managerial Accounting and Job Order Cost SystemsRajanNo ratings yet

- Cost-Volume-Profit Analysis: Study ObjectiveDocument12 pagesCost-Volume-Profit Analysis: Study ObjectiveGracelle Mae OrallerNo ratings yet

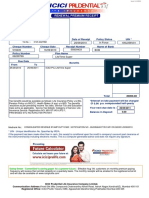

- ViewReport-icici Prem ReceiptDocument1 pageViewReport-icici Prem ReceiptPramod Shanker MathurNo ratings yet

- Adjustments of Final AccountsDocument10 pagesAdjustments of Final AccountsRahul JadhavNo ratings yet

- NUVAMADocument11 pagesNUVAMAcoureNo ratings yet

- Accounting Terms Cheat Sheet PDFDocument5 pagesAccounting Terms Cheat Sheet PDFBanzragch JamsranNo ratings yet

- Financial Management Problem SolutionsDocument5 pagesFinancial Management Problem SolutionsBobyNo ratings yet

- Full Download Taxation of Business Entities 2019 Edition 10th Edition Spilker Test BankDocument35 pagesFull Download Taxation of Business Entities 2019 Edition 10th Edition Spilker Test Bankmateorivu100% (36)

- Equitrans Midstream CompanyDocument7 pagesEquitrans Midstream CompanyMashaal FNo ratings yet

- Modified Du Pont DecompositionDocument7 pagesModified Du Pont DecompositionSurya PrakashNo ratings yet

- Oriental AromatDocument64 pagesOriental AromatVikrant DeshmukhNo ratings yet

- Substituted by The Income-Tax (6th Amendment) Rule, 2019, W.E.F. 5-11-2019Document5 pagesSubstituted by The Income-Tax (6th Amendment) Rule, 2019, W.E.F. 5-11-2019dpfsopfopsfhopNo ratings yet

- MGBLFinancial Statements 2017Document64 pagesMGBLFinancial Statements 2017TaneemNo ratings yet

- Taxation of Estates and TrustsDocument42 pagesTaxation of Estates and TrustsAngelica Joyce DyNo ratings yet

- Ya2022 - Format Tax Computation Trust BodyDocument4 pagesYa2022 - Format Tax Computation Trust BodyDaniel HaziqNo ratings yet

- LK Garuda Indonesia 31 Dec 2023Document138 pagesLK Garuda Indonesia 31 Dec 2023halimNo ratings yet

- Prepaid Expenses and Deferred Charges 1. Proper Authorization To IncurDocument4 pagesPrepaid Expenses and Deferred Charges 1. Proper Authorization To IncurJasmine Iris BautistaNo ratings yet

- Incomes Which Does Not Form Part of Total IncomeDocument5 pagesIncomes Which Does Not Form Part of Total IncomeRupesh 1312No ratings yet

- (CFA Foundation) Practice QuestionsDocument40 pages(CFA Foundation) Practice QuestionsNguyễn Kim NgânNo ratings yet

- CENRRDocument1 pageCENRRClarisse Labsan GudgadNo ratings yet

- FM402 Sugar CaseDocument11 pagesFM402 Sugar CaseDEV DUTT VASHIST 22111116No ratings yet

- 2nd Answer Keys PPT - Ia 2Document73 pages2nd Answer Keys PPT - Ia 2mia uyNo ratings yet

- Income Tax DigestsDocument6 pagesIncome Tax Digestsada mae santoniaNo ratings yet

- 9708 w14 QP 31 PDFDocument12 pages9708 w14 QP 31 PDFChandimaNo ratings yet

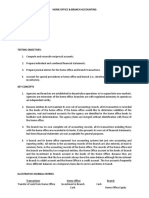

- Home Office Branch Accounting 2020 PDFDocument22 pagesHome Office Branch Accounting 2020 PDFJamaica DavidNo ratings yet

- PT Kirana - Jawaban QuizDocument2 pagesPT Kirana - Jawaban QuizJesselin VemberainNo ratings yet

- Mercia EIS Fund: Tax-Advantaged InvestmentsDocument33 pagesMercia EIS Fund: Tax-Advantaged InvestmentsdeanNo ratings yet

- ENI Annual Report 2013Document274 pagesENI Annual Report 2013lberetta2011No ratings yet