Download as docx, pdf, or txt

You might also like

- Lra Registration Fee Sample ComputationDocument10 pagesLra Registration Fee Sample ComputationrubydelacruzNo ratings yet

- PGBP New SlidesDocument40 pagesPGBP New SlidesSachin Jain100% (2)

- Fianl AccountsDocument10 pagesFianl AccountsVikram NaniNo ratings yet

- q6 TaxDocument13 pagesq6 Taxmajidpathan208No ratings yet

- Question On Income From Business and Profession 2Document9 pagesQuestion On Income From Business and Profession 2Ayush BholeNo ratings yet

- Chaper 1 - FS AuditDocument12 pagesChaper 1 - FS AuditLouie De La Torre60% (5)

- 11 Accountancy Notes Ch08 Financial Statements of Sole Proprietorship 02Document9 pages11 Accountancy Notes Ch08 Financial Statements of Sole Proprietorship 02Anonymous NSNpGa3T93100% (1)

- Income From BusinessDocument23 pagesIncome From Businesskhushi shahNo ratings yet

- 1cash Flow Ques1Document6 pages1cash Flow Ques1Dhir ChaubeyNo ratings yet

- Income TaxDocument31 pagesIncome TaxUday KumarNo ratings yet

- Advance AccountingDocument16 pagesAdvance AccountingMicro MaxxNo ratings yet

- Classification of AccountsDocument4 pagesClassification of AccountsMaria Kathreena Andrea AdevaNo ratings yet

- Financial Management - I (Practical Problems)Document9 pagesFinancial Management - I (Practical Problems)sameer_kini100% (1)

- Asifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-10 PDFDocument21 pagesAsifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-10 PDFaemanNo ratings yet

- Income From BusinessDocument8 pagesIncome From BusinessSuyash PrakashNo ratings yet

- Final AccountsDocument6 pagesFinal AccountsGaurav NahataNo ratings yet

- Chapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document26 pagesChapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din Sheryar100% (1)

- Proforma of Trading ADocument11 pagesProforma of Trading ASneha AgrawalNo ratings yet

- Bad Debt Provision NoteDocument2 pagesBad Debt Provision NoteHimank BhanotNo ratings yet

- Ja Accounts Provati 2012 Audit Opu Update2Document11 pagesJa Accounts Provati 2012 Audit Opu Update2Nasir UddinNo ratings yet

- CAPI Suggested June 2014Document25 pagesCAPI Suggested June 2014Meghraj AryalNo ratings yet

- IAS 7 - Statement of CashflowsDocument4 pagesIAS 7 - Statement of CashflowsTope JohnNo ratings yet

- FM09-CH 24Document16 pagesFM09-CH 24namitabijweNo ratings yet

- Questions Business IncomeDocument8 pagesQuestions Business IncomeMbeiza MariamNo ratings yet

- SurajDocument9 pagesSurajUjjwalNo ratings yet

- Chapter 11 Advacc 1 DayagDocument17 pagesChapter 11 Advacc 1 Dayagchangevela67% (6)

- FNSACC501 Provide Financial and Business Performance InformationDocument6 pagesFNSACC501 Provide Financial and Business Performance InformationDaranee TrakanchanNo ratings yet

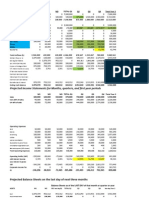

- Projected Income Statements For Months, Quarters, and First Year PeriodsDocument5 pagesProjected Income Statements For Months, Quarters, and First Year Periodssarakhan0622No ratings yet

- Solution AllDocument4 pagesSolution AllLanka SaikiranNo ratings yet

- Installment Sales Nov 2017#1Document3 pagesInstallment Sales Nov 2017#1Angel Alejo AcobaNo ratings yet

- BC Group 3 EXCELDocument7 pagesBC Group 3 EXCELSaharsh SaraogiNo ratings yet

- Corporate Income TaxDocument8 pagesCorporate Income TaxClaire BarbaNo ratings yet

- Financial ReportingDocument22 pagesFinancial Reportingmhel cabigonNo ratings yet

- JK Shah StudyMat-Paper 1-Advanced AccountingDocument518 pagesJK Shah StudyMat-Paper 1-Advanced AccountingSamyukt GNo ratings yet

- QuestionsDocument12 pagesQuestionsDolliejane MercadoNo ratings yet

- SuleeDocument8 pagesSuleefuadzeyniNo ratings yet

- CHAPTER 4 Consolidation Subse To Date of Acquisitio 2023Document12 pagesCHAPTER 4 Consolidation Subse To Date of Acquisitio 2023firaolmosisabonkeNo ratings yet

- IT AY 2022-23 Probs On PGBPDocument15 pagesIT AY 2022-23 Probs On PGBPmojesnandas9935No ratings yet

- Solutions For Cash Flow Sums OnlyDocument11 pagesSolutions For Cash Flow Sums OnlyS. GOWRINo ratings yet

- Problems On Cash Flow StatementsDocument12 pagesProblems On Cash Flow StatementsAnjali Mehta100% (1)

- Exercise (Final Accounts)Document14 pagesExercise (Final Accounts)Abhishek Bansal100% (1)

- J and J Medical ClinicDocument17 pagesJ and J Medical ClinicHarold Kent MendozaNo ratings yet

- Taxation: MD Mashiur Rahaman Robin KPMG-RRHDocument12 pagesTaxation: MD Mashiur Rahaman Robin KPMG-RRHZidan ZaifNo ratings yet

- Paper - 1: Financial Reporting Questions Ind AS 103Document30 pagesPaper - 1: Financial Reporting Questions Ind AS 103sam kapoorNo ratings yet

- Assignment: Topic: Financial Statement Analysis of National Bank of PakistanDocument28 pagesAssignment: Topic: Financial Statement Analysis of National Bank of PakistanSadaf AliNo ratings yet

- Financial Results & Limited Review Report For Dec 31, 2015 (Standalone) (Result)Document3 pagesFinancial Results & Limited Review Report For Dec 31, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Annual Report Project ExplanationDocument8 pagesAnnual Report Project Explanationmax mostNo ratings yet

- Cafe3871 2015 06 SupDocument4 pagesCafe3871 2015 06 SupThikundeko EdwardNo ratings yet

- Bba F&a Notes & ProbDocument5 pagesBba F&a Notes & ProbMouly ChopraNo ratings yet

- Introduction To Management AccountingDocument5 pagesIntroduction To Management AccountingDechen WangmoNo ratings yet

- Advanced Taxation and Strategic Tax Planning PDFDocument11 pagesAdvanced Taxation and Strategic Tax Planning PDFAnuk PereraNo ratings yet

- Life Time Fitness, Inc.: United States Securities and Exchange Commission Washington, D.C. 20549 FORM 10-QDocument33 pagesLife Time Fitness, Inc.: United States Securities and Exchange Commission Washington, D.C. 20549 FORM 10-Qpeterlee100No ratings yet

- Term Paper F-206Document2 pagesTerm Paper F-206samsuNo ratings yet

- J.K. Lasser's Small Business Taxes 2019: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2019: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Model Policies and Procedures for Not-for-Profit OrganizationsFrom EverandModel Policies and Procedures for Not-for-Profit OrganizationsNo ratings yet

- Your Order Is Finished!Document2 pagesYour Order Is Finished!Bharat MendirattaNo ratings yet

- Product and Brand Rlationships: - Olay, Lakme, NiveaDocument1 pageProduct and Brand Rlationships: - Olay, Lakme, NiveaBharat MendirattaNo ratings yet

- Eco Assngmnt 1Document4 pagesEco Assngmnt 1Bharat MendirattaNo ratings yet

- Understanding The Role of Fruit Juice in Indian Breakfast: Group 4Document12 pagesUnderstanding The Role of Fruit Juice in Indian Breakfast: Group 4Bharat MendirattaNo ratings yet

- Name Roll No. Year Tuition and Fee Bhavika Syal 231041 Year 1 - 2014-15 5.5 Year 2 - 2015-16 5.5 8.5Document3 pagesName Roll No. Year Tuition and Fee Bhavika Syal 231041 Year 1 - 2014-15 5.5 Year 2 - 2015-16 5.5 8.5Bharat MendirattaNo ratings yet

- Year Tution Fees Room and Boarding Transportation: Biman Debnath 231046 9% (SBI) 8 Lakhs P.A. From 2016Document3 pagesYear Tution Fees Room and Boarding Transportation: Biman Debnath 231046 9% (SBI) 8 Lakhs P.A. From 2016Bharat MendirattaNo ratings yet

- Session 7 Factor AnalysisDocument24 pagesSession 7 Factor AnalysisBharat MendirattaNo ratings yet

- Session 3: Sampling Design and ProceduresDocument20 pagesSession 3: Sampling Design and ProceduresBharat MendirattaNo ratings yet

- IDBI Federal - Registered CandidatesDocument3 pagesIDBI Federal - Registered CandidatesBharat MendirattaNo ratings yet

- Sno City Number of Outlets Number of Promo DaysDocument7 pagesSno City Number of Outlets Number of Promo DaysBharat MendirattaNo ratings yet

- Framework CSR 432015Document7 pagesFramework CSR 432015Bharat MendirattaNo ratings yet

- Homework Problems - Chi-Square Goodness-Of - FitDocument47 pagesHomework Problems - Chi-Square Goodness-Of - FitBharat Mendiratta100% (1)

- SigmaDocument9 pagesSigmaBharat MendirattaNo ratings yet

- Placement HighlightsDocument1 pagePlacement HighlightsBharat MendirattaNo ratings yet

- Calculation of Pension FundDocument3 pagesCalculation of Pension FundBharat MendirattaNo ratings yet

- 120 Resource November 1991 To November 2006Document174 pages120 Resource November 1991 To November 2006Bharat MendirattaNo ratings yet

- Session 1-2Document47 pagesSession 1-2Bharat MendirattaNo ratings yet

- End Term Schedule Img-8, Fmg23Document1 pageEnd Term Schedule Img-8, Fmg23Bharat MendirattaNo ratings yet