Download as pptx, pdf, or txt

You might also like

- Implied Volatility PDFDocument14 pagesImplied Volatility PDFAbbas Kareem SaddamNo ratings yet

- MFE Study GuideDocument17 pagesMFE Study Guideahpohy100% (1)

- Black Scholes DerivationDocument13 pagesBlack Scholes DerivationThomas SmithNo ratings yet

- Complete Binomial Models - 張森林教授講稿Document111 pagesComplete Binomial Models - 張森林教授講稿abin465No ratings yet

- 11.7 What Are The Formulas For U and D In: Terms of Volatility?Document13 pages11.7 What Are The Formulas For U and D In: Terms of Volatility?finscholarNo ratings yet

- Chapter 13 - The Black-Scholes-Merton ModelDocument28 pagesChapter 13 - The Black-Scholes-Merton ModelJean Pierre NaamanNo ratings yet

- Binomial TreesDocument25 pagesBinomial TreesJayash KaushalNo ratings yet

- Option Valuation ModelsDocument97 pagesOption Valuation ModelsParitoshNo ratings yet

- Option Pricing Using Binomial TreesDocument19 pagesOption Pricing Using Binomial TreesDhaka SylhetNo ratings yet

- Financial MathmaticsDocument7 pagesFinancial Mathmaticswuhanyan2000No ratings yet

- Problema 9 e 10Document8 pagesProblema 9 e 10pedrohminettoNo ratings yet

- Options Pricing Using Binomial TreesDocument12 pagesOptions Pricing Using Binomial TreesGouthaman Balaraman100% (10)

- Risk-Neutral Valuation: Steven SkienaDocument20 pagesRisk-Neutral Valuation: Steven SkienaSeenu SrinivasNo ratings yet

- MAFS5250 - Computational Methods For Pricing Structured ProductsDocument70 pagesMAFS5250 - Computational Methods For Pricing Structured ProductsBass1237No ratings yet

- Binomial Estimates U DDocument5 pagesBinomial Estimates U DMonash ParhwalNo ratings yet

- Financial Management Lecture 3 Valuation of SecuritiesDocument30 pagesFinancial Management Lecture 3 Valuation of SecuritiesTesfaye ejetaNo ratings yet

- Introduction To Binomial TreesDocument25 pagesIntroduction To Binomial Treesyty etytrfNo ratings yet

- Formulas TrymDocument44 pagesFormulas Trymmadelen.fredriksen97No ratings yet

- MAFS Topic 1Document151 pagesMAFS Topic 1Bass1237No ratings yet

- Amortized AnalysisDocument5 pagesAmortized AnalysisRahul DavidNo ratings yet

- FinMath Lecture 7 Black-ScholesDocument30 pagesFinMath Lecture 7 Black-ScholesavirgNo ratings yet

- Chapter 6 Option Pricing 2022 SDocument32 pagesChapter 6 Option Pricing 2022 SĐức Nam TrầnNo ratings yet

- Numerical Procedures (Hull Ch. 20, 8 Ed.) : Review of Chapter 12Document26 pagesNumerical Procedures (Hull Ch. 20, 8 Ed.) : Review of Chapter 12kenny013No ratings yet

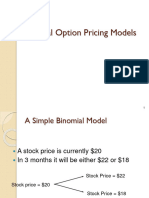

- A Simple Binomial Model: - A Stock Price Is Currently $20 - in Three Months It Will Be Either $22 or $18Document55 pagesA Simple Binomial Model: - A Stock Price Is Currently $20 - in Three Months It Will Be Either $22 or $18nasrullohNo ratings yet

- Session 9Document29 pagesSession 9Ramesh PowarNo ratings yet

- FE - Ch04 Binomial Tree ModelDocument22 pagesFE - Ch04 Binomial Tree ModelMohamed EddouniteNo ratings yet

- FE - Ch04 Binomial Tree ModelDocument21 pagesFE - Ch04 Binomial Tree ModelVishvendra SinghNo ratings yet

- Options - ValuationDocument37 pagesOptions - Valuationashu khetanNo ratings yet

- FM2 NumericalsDocument38 pagesFM2 NumericalsKamalakar ReddyNo ratings yet

- MFE NotesDocument10 pagesMFE NotesRohit SharmaNo ratings yet

- The Black and Scholes Option Pricing ModelDocument8 pagesThe Black and Scholes Option Pricing Modelshadrackmalika09No ratings yet

- Lecture Math20912 9 HandoutDocument9 pagesLecture Math20912 9 HandoutRimpy SondhNo ratings yet

- CH 2Document5 pagesCH 2z_k_j_vNo ratings yet

- Derivatives - 9 - BS Formula and Delta-HedgingDocument63 pagesDerivatives - 9 - BS Formula and Delta-HedgingHins LeeNo ratings yet

- Lognormal Random Walk and Ito LemmaDocument32 pagesLognormal Random Walk and Ito LemmaSilvia MassiNo ratings yet

- Chap 4 BMADocument38 pagesChap 4 BMAGaurav SainiNo ratings yet

- Local Vol Delta-HedgingDocument53 pagesLocal Vol Delta-HedgingVitaly Shatkovsky100% (2)

- The Black-Derman-Toy (BDT) TreeDocument4 pagesThe Black-Derman-Toy (BDT) TreeJohn SnowNo ratings yet

- Option ValuationsDocument29 pagesOption ValuationsArham Kumar JainBD21064No ratings yet

- GCIF - Parte II IIIDocument94 pagesGCIF - Parte II IIIJose Pinto de AbreuNo ratings yet

- Risk Neutral Valuation MethodDocument9 pagesRisk Neutral Valuation MethodRimpy SondhNo ratings yet

- Options On Assets Paying DividendsDocument13 pagesOptions On Assets Paying DividendsEduardo CuéllarNo ratings yet

- m339d Lecture Fourteen Binomial Option Pricing One Period PDFDocument9 pagesm339d Lecture Fourteen Binomial Option Pricing One Period PDFPriyanka ChampatiNo ratings yet

- MathFin L2Document13 pagesMathFin L2fwm949fwxrNo ratings yet

- The Black-Scholes ModelDocument42 pagesThe Black-Scholes Modelnaviprasadthebond9532No ratings yet

- − δT −rT − δT − δT − δT −rT − δTDocument10 pages− δT −rT − δT − δT − δT −rT − δTMurtaza QuettawalaNo ratings yet

- Put-Call Parity: - Put Option Value Can Be Computed Using Put-Call Parity Fiduciary Call Protective PutDocument30 pagesPut-Call Parity: - Put Option Value Can Be Computed Using Put-Call Parity Fiduciary Call Protective PutARYA SHETHNo ratings yet

- Chapter 8 Stock ValuationDocument35 pagesChapter 8 Stock ValuationHamza KhalidNo ratings yet

- Calibrate Implied VolDocument37 pagesCalibrate Implied VolALNo ratings yet

- EC3314 Spring Lecture 9Document36 pagesEC3314 Spring Lecture 9christina0107No ratings yet

- Multi Reference Credit DerivativesDocument7 pagesMulti Reference Credit DerivativesConstantin TheodorNo ratings yet

- International Portfolio DiversificationDocument34 pagesInternational Portfolio DiversificationGaurav KumarNo ratings yet

- 1 Parameterization of Binomial Models and Derivation of The Black-Scholes PDEDocument14 pages1 Parameterization of Binomial Models and Derivation of The Black-Scholes PDEhenry37302No ratings yet

- PengliudissDocument36 pagesPengliudissNehir IkizlerliNo ratings yet

- Assignment 4 (Sol.) : Reinforcement LearningDocument6 pagesAssignment 4 (Sol.) : Reinforcement Learningsimar rocksNo ratings yet

- MAFS5030 hw3Document4 pagesMAFS5030 hw3RajNo ratings yet

- Dornbsuh Model ExerciceDocument4 pagesDornbsuh Model Exerciceyouzy rkNo ratings yet

- Convergence Black-Scholes To BinomialDocument9 pagesConvergence Black-Scholes To BinomialLuis Hernandez100% (1)

- Complex Numbers (Trigonometry) Mathematics Question BankFrom EverandComplex Numbers (Trigonometry) Mathematics Question BankNo ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)