Umerchapra Global Fin Crisis-Can Islamic Finance Help

Umerchapra Global Fin Crisis-Can Islamic Finance Help

You might also like

- Tender of Payment OfferingDocument2 pagesTender of Payment OfferingJD Witchett100% (24)

- Financial Risk Management AssignmentDocument8 pagesFinancial Risk Management AssignmentM-Faheem AslamNo ratings yet

- Inside JobDocument5 pagesInside Jobpkb0% (1)

- The Financial System Limit: The world's real debt burdenFrom EverandThe Financial System Limit: The world's real debt burdenRating: 3.5 out of 5 stars3.5/5 (11)

- Zubair Hasan - Islamic BanksDocument19 pagesZubair Hasan - Islamic BanksCANDERA100% (1)

- Keven J. Wilcox, William Shepro Charged With Indirect Criminal Contempt, Fraud and ConspiracyDocument3 pagesKeven J. Wilcox, William Shepro Charged With Indirect Criminal Contempt, Fraud and ConspiracyChristopher Stoller EDNo ratings yet

- Series 65 101Document52 pagesSeries 65 101Cameron Killeen100% (3)

- Dealing With The Financial CrisisDocument8 pagesDealing With The Financial CrisisgreatbilalNo ratings yet

- Financial Derivatives: A Perceived ValueDocument20 pagesFinancial Derivatives: A Perceived ValueIvan MendesNo ratings yet

- Credit Risk Management in BanksDocument19 pagesCredit Risk Management in BanksMahmudur RahmanNo ratings yet

- Crisis Economics Nouriel RoubiniDocument1 pageCrisis Economics Nouriel Roubiniaquinas03No ratings yet

- Q: How Islamic Banking System Is Efficient Allocation of Resource?Document4 pagesQ: How Islamic Banking System Is Efficient Allocation of Resource?Dipto Kumar BiswasNo ratings yet

- Jurnal Bai Wafa2Document20 pagesJurnal Bai Wafa2PhupungPrasiwiNo ratings yet

- Regulation of Financial Markets Take Home ExamDocument22 pagesRegulation of Financial Markets Take Home ExamBrandon TeeNo ratings yet

- Islamic FinanceDocument2 pagesIslamic FinanceClarence DantisNo ratings yet

- The Future of Securitization: Born Free, But Living With More Adult SupervisionDocument7 pagesThe Future of Securitization: Born Free, But Living With More Adult Supervisionsss1453100% (1)

- The 2008 Financial CrisisDocument14 pagesThe 2008 Financial Crisisann3cha100% (1)

- En The Credit CrisisDocument3 pagesEn The Credit CrisisDubstep ImtiyajNo ratings yet

- Macro Prudential RegulationDocument8 pagesMacro Prudential RegulationcristinaovezeaNo ratings yet

- Inside Job - Financial Crisis Klara KomenDocument1 pageInside Job - Financial Crisis Klara KomenKlaraKomenNo ratings yet

- ProjectDocument7 pagesProjectmalik waseemNo ratings yet

- Pillai'S College OF Arts, Commerce and ScienceDocument14 pagesPillai'S College OF Arts, Commerce and Scienceamiit_pandey3503No ratings yet

- Allecks Juel R. Luchana Group No. 6 TTH 7:30Am-9:00Am The Crisis of CreditDocument3 pagesAllecks Juel R. Luchana Group No. 6 TTH 7:30Am-9:00Am The Crisis of CreditAllecks Juel LuchanaNo ratings yet

- Credit BoomDocument6 pagesCredit BoomumairmbaNo ratings yet

- Financial Intermediation and The Post-Crisis Financial SystemDocument32 pagesFinancial Intermediation and The Post-Crisis Financial SystemTina FrancisNo ratings yet

- Petrocapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Document4 pagesPetrocapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Capita1No ratings yet

- CCGL Asm1 WANG XINRUI 3036128298 2023Document4 pagesCCGL Asm1 WANG XINRUI 3036128298 2023XINRUI WANGNo ratings yet

- Sub Prime CrisisDocument17 pagesSub Prime CrisisrakheesinhaNo ratings yet

- Subprime Lending Is The Practice of Extending Credit To Borrowers With CertainDocument4 pagesSubprime Lending Is The Practice of Extending Credit To Borrowers With CertainPraffulla Chandra RayNo ratings yet

- What Is A Subprime Mortgage?Document5 pagesWhat Is A Subprime Mortgage?Chigo RamosNo ratings yet

- Shadow Banking System ThesisDocument6 pagesShadow Banking System Thesispak0t0dynyj3100% (2)

- U.S. Sub-Prime Crisis & Its Global ConsequencesDocument33 pagesU.S. Sub-Prime Crisis & Its Global ConsequencesakkikhanejadevNo ratings yet

- Fitch Rating MethodologyDocument16 pagesFitch Rating Methodologyrash2014No ratings yet

- Mervyn King Speech On Too Big To FailDocument10 pagesMervyn King Speech On Too Big To FailCale SmithNo ratings yet

- Managing The Liquidity CrisisDocument8 pagesManaging The Liquidity CrisisRusdi RuslyNo ratings yet

- Danger of Hedge Funds: Economic and Political Weekly August 20, 2005Document6 pagesDanger of Hedge Funds: Economic and Political Weekly August 20, 2005Anand BansalNo ratings yet

- Fitch Rating MethodologyDocument16 pagesFitch Rating MethodologyPradikta FebranoNo ratings yet

- Understanding Securitization Role in Subprime Lending Evidence From Countrywide FinancialDocument14 pagesUnderstanding Securitization Role in Subprime Lending Evidence From Countrywide FinancialSandeepNo ratings yet

- The Due Diligence Model: A New Approach To The Problem of Odious DebtsDocument19 pagesThe Due Diligence Model: A New Approach To The Problem of Odious DebtsMateus RabeloNo ratings yet

- Agcapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Document4 pagesAgcapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Capita1No ratings yet

- The Myth of Financial ReformDocument6 pagesThe Myth of Financial ReformManharMayankNo ratings yet

- Crisis of CreditDocument4 pagesCrisis of CreditRaven PicorroNo ratings yet

- Why Economists and - Economies Should Love Islamic FinanceDocument24 pagesWhy Economists and - Economies Should Love Islamic FinancervotoyNo ratings yet

- BPEA Sachs1 2002-1Document28 pagesBPEA Sachs1 2002-1FacundoNo ratings yet

- GlobalcreditcrisisDocument3 pagesGlobalcreditcrisisFazulAXNo ratings yet

- The Sub-Prime Mortgage Crisis & DerivativesDocument10 pagesThe Sub-Prime Mortgage Crisis & DerivativesChen XinNo ratings yet

- 2010 09 RGE Steps We Must Take After Dodd FrankDocument2 pages2010 09 RGE Steps We Must Take After Dodd FrankgsnithinNo ratings yet

- Gaetano and Marimon (2020) - Breaking The Spell With Credit-Easing Self-Confirming CRDocument49 pagesGaetano and Marimon (2020) - Breaking The Spell With Credit-Easing Self-Confirming CRCamilo DomínguezNo ratings yet

- What If Nothing Is Risk Free?: SATURDAY, JULY 24, 2010Document11 pagesWhat If Nothing Is Risk Free?: SATURDAY, JULY 24, 2010priyankaaneja24gmailNo ratings yet

- Life Settlements and Longevity Structures: Pricing and Risk ManagementFrom EverandLife Settlements and Longevity Structures: Pricing and Risk ManagementNo ratings yet

- US Federal Reserve S97mishkDocument42 pagesUS Federal Reserve S97mishkYoucan B StreetsmartNo ratings yet

- Credit Derivatives - Basic Concepts Golaka C NathDocument19 pagesCredit Derivatives - Basic Concepts Golaka C NathGolaka NathNo ratings yet

- ChapraDocument14 pagesChaprasilvi dianaNo ratings yet

- "Misunderstanding Financial Crises", A Q&A With Gary Gorton - FT AlphavilleDocument7 pages"Misunderstanding Financial Crises", A Q&A With Gary Gorton - FT AlphavilleAloy31stNo ratings yet

- Is Private Credit A Systemic Risk?Document11 pagesIs Private Credit A Systemic Risk?papadopoulosstergios1No ratings yet

- Credit Default Swaps and GFC-C2D2Document5 pagesCredit Default Swaps and GFC-C2D2michnhiNo ratings yet

- Zarriz, Devine C. Bsa 1A Econ107Document3 pagesZarriz, Devine C. Bsa 1A Econ107Devine Zarriz IINo ratings yet

- Has Finance Made The World RiskierDocument36 pagesHas Finance Made The World RiskierbbarooahNo ratings yet

- Group BFF5230 Workshop3Document4 pagesGroup BFF5230 Workshop3MeloNo ratings yet

- Alan Greenspan UpDocument14 pagesAlan Greenspan UpEric WhitfieldNo ratings yet

- Discussion Paper On Credit Guarantee SchemesDocument19 pagesDiscussion Paper On Credit Guarantee SchemesFierDaus MfmmNo ratings yet

- Misc SivDocument4 pagesMisc SivNuggets MusicNo ratings yet

- (Wiley Finance Series) Ciby Joseph - Advanced Credit Risk Analysis and Management-Wiley (2013) (1) (021-040) EsDocument41 pages(Wiley Finance Series) Ciby Joseph - Advanced Credit Risk Analysis and Management-Wiley (2013) (1) (021-040) EsGustavo Felipe Campos CarocaNo ratings yet

- Islamic EconomicsDocument73 pagesIslamic Economicsapi-3830416100% (2)

- Maqasid Shariah and Fiat MoneyDocument17 pagesMaqasid Shariah and Fiat MoneyCANDERANo ratings yet

- Ethico Moral Economic - Islamic Economic by Tozeef 2006Document21 pagesEthico Moral Economic - Islamic Economic by Tozeef 2006CANDERANo ratings yet

- Economics of ReligionDocument32 pagesEconomics of ReligionCANDERANo ratings yet

- Ali Shingjergji - The Impact of Macroeconomic Variabel On Non Performing LoansDocument5 pagesAli Shingjergji - The Impact of Macroeconomic Variabel On Non Performing LoansCANDERANo ratings yet

- Consumption in Islamic Economic by Zubair - Hasan06Document18 pagesConsumption in Islamic Economic by Zubair - Hasan06CANDERANo ratings yet

- Rifki Ismal - Assessing Moral Hazard Problem in Murabahah FinancingDocument12 pagesRifki Ismal - Assessing Moral Hazard Problem in Murabahah FinancingCANDERANo ratings yet

- Rendy Ho - Effectss of Capital-Asset Contraints On Commercial Bank Lending From 1990 To 1992Document44 pagesRendy Ho - Effectss of Capital-Asset Contraints On Commercial Bank Lending From 1990 To 1992CANDERANo ratings yet

- Factors Affecting Distribution of Agricultural CreditDocument3 pagesFactors Affecting Distribution of Agricultural CreditInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Leading Experts in Islamic FinanceDocument238 pagesLeading Experts in Islamic FinanceZX Lee100% (1)

- Problem 11&17Document12 pagesProblem 11&17Kaira GoNo ratings yet

- Accounting 0452 Revision Notes For The y PDFDocument48 pagesAccounting 0452 Revision Notes For The y PDFSiddarthNo ratings yet

- Flores v. SoDocument6 pagesFlores v. SoRaine VerdanNo ratings yet

- Case Counts PradnyaDocument15 pagesCase Counts PradnyaChaitali DegavkarNo ratings yet

- Chapter 1 Economics of Money, Banking, and Financial Markets (5th Cad. Ed.)Document27 pagesChapter 1 Economics of Money, Banking, and Financial Markets (5th Cad. Ed.)Edith KuaNo ratings yet

- RERDocument1 pageRERtherence jane blanco100% (1)

- Annexure 2 - Sample Financial Model TemplateDocument135 pagesAnnexure 2 - Sample Financial Model TemplateGurvinder SinghNo ratings yet

- Presentation IsfnDocument14 pagesPresentation IsfnAmirah ShukriNo ratings yet

- Nism X A - Investment Adviser Level 1 - Last Day Revision Test 3Document19 pagesNism X A - Investment Adviser Level 1 - Last Day Revision Test 3Nupur SharmaNo ratings yet

- Sample Sales Compensation PlanDocument12 pagesSample Sales Compensation PlanLisa Glover-GardinNo ratings yet

- "Customer Attitude Towards COMMERCIAL LOANDocument58 pages"Customer Attitude Towards COMMERCIAL LOANPulkit SachdevaNo ratings yet

- Final Seminar 4.Document9 pagesFinal Seminar 4.Punam GuptaNo ratings yet

- Bank ValuationDocument9 pagesBank ValuationHarshil SinghalNo ratings yet

- Prudencio V CaDocument2 pagesPrudencio V CaEinstein Newton100% (1)

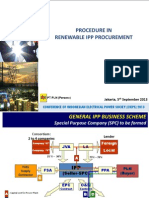

- IPP Procedure ConferenceDocument10 pagesIPP Procedure ConferencekongbengNo ratings yet

- CompensationDocument14 pagesCompensationAnshu SethiaNo ratings yet

- Defi, Community Staking and Liquidity Provider PlatformDocument8 pagesDefi, Community Staking and Liquidity Provider PlatformHoshang VermaNo ratings yet

- Karnataka Souharda Sahakari Act, 1997Document104 pagesKarnataka Souharda Sahakari Act, 1997Latest Laws TeamNo ratings yet

- Credit Transaction Case DigestDocument10 pagesCredit Transaction Case DigestMarco ArponNo ratings yet

- Pre-Shipment and Post-Shipment Finance of State Bank of India (Sbi)Document5 pagesPre-Shipment and Post-Shipment Finance of State Bank of India (Sbi)Rohit OberoiNo ratings yet

- Assigned Commissioner Ruling, Joined by A Co-Assigned Alj, Requesting Comments On Surcharge Options and ProposalsDocument22 pagesAssigned Commissioner Ruling, Joined by A Co-Assigned Alj, Requesting Comments On Surcharge Options and ProposalsL. A. PatersonNo ratings yet

- Income SourcesDocument35 pagesIncome Sourcesirina_nircaNo ratings yet

- Renewable 0 Energy 0 ReportDocument94 pagesRenewable 0 Energy 0 ReportTara Sinha100% (1)

- History of Laws On Insolvency and FRIADocument244 pagesHistory of Laws On Insolvency and FRIAShieldon Vic Senajon PinoonNo ratings yet

- Carlos V Mindoro SugarDocument2 pagesCarlos V Mindoro SugarKristine GarciaNo ratings yet

- Federal National Mortgage Association (Fannie Mae)Document5 pagesFederal National Mortgage Association (Fannie Mae)CinthyaNo ratings yet

- Autolock Box Concepts in r12Document21 pagesAutolock Box Concepts in r12devender_bharatha3284No ratings yet

Download as pdf or txt

You might also like

- Tender of Payment OfferingDocument2 pagesTender of Payment OfferingJD Witchett100% (24)

- Financial Risk Management AssignmentDocument8 pagesFinancial Risk Management AssignmentM-Faheem AslamNo ratings yet

- Inside JobDocument5 pagesInside Jobpkb0% (1)

- The Financial System Limit: The world's real debt burdenFrom EverandThe Financial System Limit: The world's real debt burdenRating: 3.5 out of 5 stars3.5/5 (11)

- Zubair Hasan - Islamic BanksDocument19 pagesZubair Hasan - Islamic BanksCANDERA100% (1)

- Keven J. Wilcox, William Shepro Charged With Indirect Criminal Contempt, Fraud and ConspiracyDocument3 pagesKeven J. Wilcox, William Shepro Charged With Indirect Criminal Contempt, Fraud and ConspiracyChristopher Stoller EDNo ratings yet

- Series 65 101Document52 pagesSeries 65 101Cameron Killeen100% (3)

- Dealing With The Financial CrisisDocument8 pagesDealing With The Financial CrisisgreatbilalNo ratings yet

- Financial Derivatives: A Perceived ValueDocument20 pagesFinancial Derivatives: A Perceived ValueIvan MendesNo ratings yet

- Credit Risk Management in BanksDocument19 pagesCredit Risk Management in BanksMahmudur RahmanNo ratings yet

- Crisis Economics Nouriel RoubiniDocument1 pageCrisis Economics Nouriel Roubiniaquinas03No ratings yet

- Q: How Islamic Banking System Is Efficient Allocation of Resource?Document4 pagesQ: How Islamic Banking System Is Efficient Allocation of Resource?Dipto Kumar BiswasNo ratings yet

- Jurnal Bai Wafa2Document20 pagesJurnal Bai Wafa2PhupungPrasiwiNo ratings yet

- Regulation of Financial Markets Take Home ExamDocument22 pagesRegulation of Financial Markets Take Home ExamBrandon TeeNo ratings yet

- Islamic FinanceDocument2 pagesIslamic FinanceClarence DantisNo ratings yet

- The Future of Securitization: Born Free, But Living With More Adult SupervisionDocument7 pagesThe Future of Securitization: Born Free, But Living With More Adult Supervisionsss1453100% (1)

- The 2008 Financial CrisisDocument14 pagesThe 2008 Financial Crisisann3cha100% (1)

- En The Credit CrisisDocument3 pagesEn The Credit CrisisDubstep ImtiyajNo ratings yet

- Macro Prudential RegulationDocument8 pagesMacro Prudential RegulationcristinaovezeaNo ratings yet

- Inside Job - Financial Crisis Klara KomenDocument1 pageInside Job - Financial Crisis Klara KomenKlaraKomenNo ratings yet

- ProjectDocument7 pagesProjectmalik waseemNo ratings yet

- Pillai'S College OF Arts, Commerce and ScienceDocument14 pagesPillai'S College OF Arts, Commerce and Scienceamiit_pandey3503No ratings yet

- Allecks Juel R. Luchana Group No. 6 TTH 7:30Am-9:00Am The Crisis of CreditDocument3 pagesAllecks Juel R. Luchana Group No. 6 TTH 7:30Am-9:00Am The Crisis of CreditAllecks Juel LuchanaNo ratings yet

- Credit BoomDocument6 pagesCredit BoomumairmbaNo ratings yet

- Financial Intermediation and The Post-Crisis Financial SystemDocument32 pagesFinancial Intermediation and The Post-Crisis Financial SystemTina FrancisNo ratings yet

- Petrocapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Document4 pagesPetrocapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Capita1No ratings yet

- CCGL Asm1 WANG XINRUI 3036128298 2023Document4 pagesCCGL Asm1 WANG XINRUI 3036128298 2023XINRUI WANGNo ratings yet

- Sub Prime CrisisDocument17 pagesSub Prime CrisisrakheesinhaNo ratings yet

- Subprime Lending Is The Practice of Extending Credit To Borrowers With CertainDocument4 pagesSubprime Lending Is The Practice of Extending Credit To Borrowers With CertainPraffulla Chandra RayNo ratings yet

- What Is A Subprime Mortgage?Document5 pagesWhat Is A Subprime Mortgage?Chigo RamosNo ratings yet

- Shadow Banking System ThesisDocument6 pagesShadow Banking System Thesispak0t0dynyj3100% (2)

- U.S. Sub-Prime Crisis & Its Global ConsequencesDocument33 pagesU.S. Sub-Prime Crisis & Its Global ConsequencesakkikhanejadevNo ratings yet

- Fitch Rating MethodologyDocument16 pagesFitch Rating Methodologyrash2014No ratings yet

- Mervyn King Speech On Too Big To FailDocument10 pagesMervyn King Speech On Too Big To FailCale SmithNo ratings yet

- Managing The Liquidity CrisisDocument8 pagesManaging The Liquidity CrisisRusdi RuslyNo ratings yet

- Danger of Hedge Funds: Economic and Political Weekly August 20, 2005Document6 pagesDanger of Hedge Funds: Economic and Political Weekly August 20, 2005Anand BansalNo ratings yet

- Fitch Rating MethodologyDocument16 pagesFitch Rating MethodologyPradikta FebranoNo ratings yet

- Understanding Securitization Role in Subprime Lending Evidence From Countrywide FinancialDocument14 pagesUnderstanding Securitization Role in Subprime Lending Evidence From Countrywide FinancialSandeepNo ratings yet

- The Due Diligence Model: A New Approach To The Problem of Odious DebtsDocument19 pagesThe Due Diligence Model: A New Approach To The Problem of Odious DebtsMateus RabeloNo ratings yet

- Agcapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Document4 pagesAgcapita December 2011 Briefing - Counterparty Risk in Your Portfolio?Capita1No ratings yet

- The Myth of Financial ReformDocument6 pagesThe Myth of Financial ReformManharMayankNo ratings yet

- Crisis of CreditDocument4 pagesCrisis of CreditRaven PicorroNo ratings yet

- Why Economists and - Economies Should Love Islamic FinanceDocument24 pagesWhy Economists and - Economies Should Love Islamic FinancervotoyNo ratings yet

- BPEA Sachs1 2002-1Document28 pagesBPEA Sachs1 2002-1FacundoNo ratings yet

- GlobalcreditcrisisDocument3 pagesGlobalcreditcrisisFazulAXNo ratings yet

- The Sub-Prime Mortgage Crisis & DerivativesDocument10 pagesThe Sub-Prime Mortgage Crisis & DerivativesChen XinNo ratings yet

- 2010 09 RGE Steps We Must Take After Dodd FrankDocument2 pages2010 09 RGE Steps We Must Take After Dodd FrankgsnithinNo ratings yet

- Gaetano and Marimon (2020) - Breaking The Spell With Credit-Easing Self-Confirming CRDocument49 pagesGaetano and Marimon (2020) - Breaking The Spell With Credit-Easing Self-Confirming CRCamilo DomínguezNo ratings yet

- What If Nothing Is Risk Free?: SATURDAY, JULY 24, 2010Document11 pagesWhat If Nothing Is Risk Free?: SATURDAY, JULY 24, 2010priyankaaneja24gmailNo ratings yet

- Life Settlements and Longevity Structures: Pricing and Risk ManagementFrom EverandLife Settlements and Longevity Structures: Pricing and Risk ManagementNo ratings yet

- US Federal Reserve S97mishkDocument42 pagesUS Federal Reserve S97mishkYoucan B StreetsmartNo ratings yet

- Credit Derivatives - Basic Concepts Golaka C NathDocument19 pagesCredit Derivatives - Basic Concepts Golaka C NathGolaka NathNo ratings yet

- ChapraDocument14 pagesChaprasilvi dianaNo ratings yet

- "Misunderstanding Financial Crises", A Q&A With Gary Gorton - FT AlphavilleDocument7 pages"Misunderstanding Financial Crises", A Q&A With Gary Gorton - FT AlphavilleAloy31stNo ratings yet

- Is Private Credit A Systemic Risk?Document11 pagesIs Private Credit A Systemic Risk?papadopoulosstergios1No ratings yet

- Credit Default Swaps and GFC-C2D2Document5 pagesCredit Default Swaps and GFC-C2D2michnhiNo ratings yet

- Zarriz, Devine C. Bsa 1A Econ107Document3 pagesZarriz, Devine C. Bsa 1A Econ107Devine Zarriz IINo ratings yet

- Has Finance Made The World RiskierDocument36 pagesHas Finance Made The World RiskierbbarooahNo ratings yet

- Group BFF5230 Workshop3Document4 pagesGroup BFF5230 Workshop3MeloNo ratings yet

- Alan Greenspan UpDocument14 pagesAlan Greenspan UpEric WhitfieldNo ratings yet

- Discussion Paper On Credit Guarantee SchemesDocument19 pagesDiscussion Paper On Credit Guarantee SchemesFierDaus MfmmNo ratings yet

- Misc SivDocument4 pagesMisc SivNuggets MusicNo ratings yet

- (Wiley Finance Series) Ciby Joseph - Advanced Credit Risk Analysis and Management-Wiley (2013) (1) (021-040) EsDocument41 pages(Wiley Finance Series) Ciby Joseph - Advanced Credit Risk Analysis and Management-Wiley (2013) (1) (021-040) EsGustavo Felipe Campos CarocaNo ratings yet

- Islamic EconomicsDocument73 pagesIslamic Economicsapi-3830416100% (2)

- Maqasid Shariah and Fiat MoneyDocument17 pagesMaqasid Shariah and Fiat MoneyCANDERANo ratings yet

- Ethico Moral Economic - Islamic Economic by Tozeef 2006Document21 pagesEthico Moral Economic - Islamic Economic by Tozeef 2006CANDERANo ratings yet

- Economics of ReligionDocument32 pagesEconomics of ReligionCANDERANo ratings yet

- Ali Shingjergji - The Impact of Macroeconomic Variabel On Non Performing LoansDocument5 pagesAli Shingjergji - The Impact of Macroeconomic Variabel On Non Performing LoansCANDERANo ratings yet

- Consumption in Islamic Economic by Zubair - Hasan06Document18 pagesConsumption in Islamic Economic by Zubair - Hasan06CANDERANo ratings yet

- Rifki Ismal - Assessing Moral Hazard Problem in Murabahah FinancingDocument12 pagesRifki Ismal - Assessing Moral Hazard Problem in Murabahah FinancingCANDERANo ratings yet

- Rendy Ho - Effectss of Capital-Asset Contraints On Commercial Bank Lending From 1990 To 1992Document44 pagesRendy Ho - Effectss of Capital-Asset Contraints On Commercial Bank Lending From 1990 To 1992CANDERANo ratings yet

- Factors Affecting Distribution of Agricultural CreditDocument3 pagesFactors Affecting Distribution of Agricultural CreditInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Leading Experts in Islamic FinanceDocument238 pagesLeading Experts in Islamic FinanceZX Lee100% (1)

- Problem 11&17Document12 pagesProblem 11&17Kaira GoNo ratings yet

- Accounting 0452 Revision Notes For The y PDFDocument48 pagesAccounting 0452 Revision Notes For The y PDFSiddarthNo ratings yet

- Flores v. SoDocument6 pagesFlores v. SoRaine VerdanNo ratings yet

- Case Counts PradnyaDocument15 pagesCase Counts PradnyaChaitali DegavkarNo ratings yet

- Chapter 1 Economics of Money, Banking, and Financial Markets (5th Cad. Ed.)Document27 pagesChapter 1 Economics of Money, Banking, and Financial Markets (5th Cad. Ed.)Edith KuaNo ratings yet

- RERDocument1 pageRERtherence jane blanco100% (1)

- Annexure 2 - Sample Financial Model TemplateDocument135 pagesAnnexure 2 - Sample Financial Model TemplateGurvinder SinghNo ratings yet

- Presentation IsfnDocument14 pagesPresentation IsfnAmirah ShukriNo ratings yet

- Nism X A - Investment Adviser Level 1 - Last Day Revision Test 3Document19 pagesNism X A - Investment Adviser Level 1 - Last Day Revision Test 3Nupur SharmaNo ratings yet

- Sample Sales Compensation PlanDocument12 pagesSample Sales Compensation PlanLisa Glover-GardinNo ratings yet

- "Customer Attitude Towards COMMERCIAL LOANDocument58 pages"Customer Attitude Towards COMMERCIAL LOANPulkit SachdevaNo ratings yet

- Final Seminar 4.Document9 pagesFinal Seminar 4.Punam GuptaNo ratings yet

- Bank ValuationDocument9 pagesBank ValuationHarshil SinghalNo ratings yet

- Prudencio V CaDocument2 pagesPrudencio V CaEinstein Newton100% (1)

- IPP Procedure ConferenceDocument10 pagesIPP Procedure ConferencekongbengNo ratings yet

- CompensationDocument14 pagesCompensationAnshu SethiaNo ratings yet

- Defi, Community Staking and Liquidity Provider PlatformDocument8 pagesDefi, Community Staking and Liquidity Provider PlatformHoshang VermaNo ratings yet

- Karnataka Souharda Sahakari Act, 1997Document104 pagesKarnataka Souharda Sahakari Act, 1997Latest Laws TeamNo ratings yet

- Credit Transaction Case DigestDocument10 pagesCredit Transaction Case DigestMarco ArponNo ratings yet

- Pre-Shipment and Post-Shipment Finance of State Bank of India (Sbi)Document5 pagesPre-Shipment and Post-Shipment Finance of State Bank of India (Sbi)Rohit OberoiNo ratings yet

- Assigned Commissioner Ruling, Joined by A Co-Assigned Alj, Requesting Comments On Surcharge Options and ProposalsDocument22 pagesAssigned Commissioner Ruling, Joined by A Co-Assigned Alj, Requesting Comments On Surcharge Options and ProposalsL. A. PatersonNo ratings yet

- Income SourcesDocument35 pagesIncome Sourcesirina_nircaNo ratings yet

- Renewable 0 Energy 0 ReportDocument94 pagesRenewable 0 Energy 0 ReportTara Sinha100% (1)

- History of Laws On Insolvency and FRIADocument244 pagesHistory of Laws On Insolvency and FRIAShieldon Vic Senajon PinoonNo ratings yet

- Carlos V Mindoro SugarDocument2 pagesCarlos V Mindoro SugarKristine GarciaNo ratings yet

- Federal National Mortgage Association (Fannie Mae)Document5 pagesFederal National Mortgage Association (Fannie Mae)CinthyaNo ratings yet

- Autolock Box Concepts in r12Document21 pagesAutolock Box Concepts in r12devender_bharatha3284No ratings yet