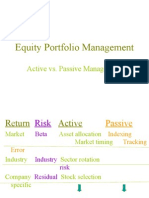

Active Portfolio Management

Active Portfolio Management

You might also like

- CH 09Document34 pagesCH 09Azhar SeptariNo ratings yet

- Trade Off Between Relevance and ReliabilityDocument1 pageTrade Off Between Relevance and ReliabilitylciimNo ratings yet

- FORT FrameworkDocument7 pagesFORT FrameworkAbhishek KumarNo ratings yet

- Align Technology IncDocument16 pagesAlign Technology IncAbhishek Kumar0% (1)

- Portfolio Selection & Asset AllocationDocument15 pagesPortfolio Selection & Asset AllocationNadea Fikrah RasuliNo ratings yet

- AEB14 SM CH17 v2Document31 pagesAEB14 SM CH17 v2RonLiu350% (1)

- The Information Approach To Decision UsefulnessDocument26 pagesThe Information Approach To Decision UsefulnessDiny Fariha ZakhirNo ratings yet

- Case 15-5 Xerox Corporation RecommendationsDocument6 pagesCase 15-5 Xerox Corporation RecommendationsgabrielyangNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument40 pagesFinancial Statement Analysis: K.R. SubramanyamRisky AlvinNo ratings yet

- Importance of Mutual FundsDocument14 pagesImportance of Mutual FundsMukesh Kumar SinghNo ratings yet

- Substantive Testing in The Revenue CycleDocument3 pagesSubstantive Testing in The Revenue CycleGeorgia FlorentinoNo ratings yet

- SAPM Portfolio RevisionDocument9 pagesSAPM Portfolio RevisionSpUnky RohitNo ratings yet

- Investment in Equities Versus Investment in Mutual FundDocument37 pagesInvestment in Equities Versus Investment in Mutual FundBob PanjabiNo ratings yet

- Bpe 34603 - LN 5 25 March 2019Document28 pagesBpe 34603 - LN 5 25 March 2019Irfan AzmanNo ratings yet

- Security Analysis and Portfolio Management: Master of Business AdministrationDocument80 pagesSecurity Analysis and Portfolio Management: Master of Business AdministrationSagar Paul'gNo ratings yet

- Portfolio Management ServicesDocument19 pagesPortfolio Management Serviceschawan_nikitaNo ratings yet

- Activity Based CostingDocument51 pagesActivity Based CostingAbdulyunus AmirNo ratings yet

- Scot ch07Document33 pagesScot ch07Diny Fariha ZakhirNo ratings yet

- Budgetary Control of IndiaDocument30 pagesBudgetary Control of IndiaNiks DujaniyaNo ratings yet

- Chapter 18 - Evaluating Investment PerformanceDocument62 pagesChapter 18 - Evaluating Investment PerformanceRavi PatelNo ratings yet

- Fundamental AnalysisDocument10 pagesFundamental AnalysisSaurabh Khurana100% (1)

- The Role of The AuditorDocument30 pagesThe Role of The AuditorALCIDES100% (1)

- The Measurement Approach To Decision UsefulnessDocument33 pagesThe Measurement Approach To Decision UsefulnessDiny Fariha ZakhirNo ratings yet

- Chapter 5 Portfolio Risk and Return Part IDocument25 pagesChapter 5 Portfolio Risk and Return Part ILaura StephanieNo ratings yet

- Legal Aspects of Project FinanceDocument9 pagesLegal Aspects of Project FinanceBlesson PerumalNo ratings yet

- Currency DerivativesDocument25 pagesCurrency DerivativesDarshitSejparaNo ratings yet

- Behavioral Finance and Technical AnalysisDocument18 pagesBehavioral Finance and Technical Analysispham terikNo ratings yet

- It Is A Stock Valuation Method - That Uses Financial and Economic Analysis - To Predict The Movement of Stock PricesDocument24 pagesIt Is A Stock Valuation Method - That Uses Financial and Economic Analysis - To Predict The Movement of Stock PricesAnonymous KN4pnOHmNo ratings yet

- Inter Psak 25Document28 pagesInter Psak 25vincent alvinNo ratings yet

- Cash Management ServicesDocument5 pagesCash Management ServicesMadhur AnandNo ratings yet

- Chapter 1 An Overview of The Investment ProcessDocument31 pagesChapter 1 An Overview of The Investment ProcessAbuzafar AbdullahNo ratings yet

- Financial Project FinalDocument46 pagesFinancial Project FinalBunty ShahNo ratings yet

- Asset Substitution ProblemDocument1 pageAsset Substitution ProblemNitish BhayrauNo ratings yet

- Fin3 Midterm ExamDocument8 pagesFin3 Midterm ExamBryan Lluisma100% (1)

- Capital Budgeting TechniquesDocument48 pagesCapital Budgeting TechniquesMuslimNo ratings yet

- Guideline BBDocument33 pagesGuideline BBsalam3500935No ratings yet

- Manajemen Keuangan - Merger and Acquisition PDFDocument36 pagesManajemen Keuangan - Merger and Acquisition PDFvrieskaNo ratings yet

- Mutual Funds: BY: Adneya Audhi Roll: 12304Document20 pagesMutual Funds: BY: Adneya Audhi Roll: 12304Adneya AudhiNo ratings yet

- Tactical Decision MakingDocument25 pagesTactical Decision MakingNizam JewelNo ratings yet

- Strategic Cost Management (SCM) FrameworkDocument11 pagesStrategic Cost Management (SCM) FrameworkcallmeasthaNo ratings yet

- Chapter One: Mcgraw-Hill/IrwinDocument17 pagesChapter One: Mcgraw-Hill/Irwinteraz2810No ratings yet

- Financial For Non Financial CitibanamexDocument147 pagesFinancial For Non Financial CitibanamexRaúl ArellanoNo ratings yet

- Chapter 6 - Using Discounted Cash Flow Analysis To Make Investment DecisionsDocument14 pagesChapter 6 - Using Discounted Cash Flow Analysis To Make Investment DecisionsSheena Rhei Del RosarioNo ratings yet

- Notes - MARKETING - OF - FINANCIAL SERVICES - 2020Document69 pagesNotes - MARKETING - OF - FINANCIAL SERVICES - 2020Rozy SinghNo ratings yet

- SAPMDocument93 pagesSAPMSOUMIKNo ratings yet

- Investors Preferences Towards Equity Indiabulls 2011Document81 pagesInvestors Preferences Towards Equity Indiabulls 2011chaluvadiin100% (2)

- Chapter 21 Internal, Operation and Governmental AuditingDocument23 pagesChapter 21 Internal, Operation and Governmental AuditinghidaNo ratings yet

- Investment Management: - Asset Allocation DecisionDocument23 pagesInvestment Management: - Asset Allocation DecisionyebegashetNo ratings yet

- Chapter 2Document40 pagesChapter 2Farapple24No ratings yet

- Financial RiskDocument13 pagesFinancial RiskHitesh Pant50% (2)

- Futures and OptionsDocument42 pagesFutures and OptionsMallikarjun RaoNo ratings yet

- Aunjum, Abbas, SajidDocument8 pagesAunjum, Abbas, SajidJuan Pablo Restrepo QuinteroNo ratings yet

- Financial EngineeringDocument18 pagesFinancial Engineeringtanay-mehta-3589100% (1)

- Optimal Portfolio ConstructionDocument14 pagesOptimal Portfolio ConstructionvigneshwaranmoorthyNo ratings yet

- Security Analysis and Portfolio Management, Bond Market in India.Document26 pagesSecurity Analysis and Portfolio Management, Bond Market in India.Gagandeep Singh BangarNo ratings yet

- Investment Analysis and Portfolio Management: Eighth Edition by Frank K. Reilly & Keith C. BrownDocument56 pagesInvestment Analysis and Portfolio Management: Eighth Edition by Frank K. Reilly & Keith C. BrownPayal MehtaNo ratings yet

- 2007 Ny Chotai I7Document7 pages2007 Ny Chotai I7Matthew BrownNo ratings yet

- 6205 LectureDocument27 pages6205 Lectureapi-3699305No ratings yet

- 4 InventoryManagementDocument44 pages4 InventoryManagementPrateek HosamaniNo ratings yet

- Exercise of Standard Costing: Standard Cost For Product White DiamondDocument18 pagesExercise of Standard Costing: Standard Cost For Product White DiamondSandip BansalNo ratings yet

- Antecedent Verification ProcessDocument4 pagesAntecedent Verification ProcessAbhishek KumarNo ratings yet

- Invoice OD109172599294660000Document2 pagesInvoice OD109172599294660000Abhishek KumarNo ratings yet

- Nifty: Trading StrategiesDocument2 pagesNifty: Trading StrategiesAbhishek KumarNo ratings yet

- An Example of Attribute Based MDS Using Discriminant AnalysisDocument17 pagesAn Example of Attribute Based MDS Using Discriminant AnalysisAbhishek KumarNo ratings yet

- Chapter 10 Regression SlidesDocument46 pagesChapter 10 Regression SlidesAbhishek KumarNo ratings yet

- Anova and The Design of Experiments: Welcome To Powerpoint Slides ForDocument22 pagesAnova and The Design of Experiments: Welcome To Powerpoint Slides ForAbhishek KumarNo ratings yet

- Indian Institute of Management Indore: MT ET CP AssignmentDocument2 pagesIndian Institute of Management Indore: MT ET CP AssignmentAbhishek KumarNo ratings yet

- Practice Set-2Document7 pagesPractice Set-2Abhishek Kumar100% (2)

- INOX Leisure LTD., - Location ListDocument2 pagesINOX Leisure LTD., - Location ListAbhishek KumarNo ratings yet

- Marketing of ServicesDocument6 pagesMarketing of ServicesAbhishek KumarNo ratings yet

- BC Sec CDocument2 pagesBC Sec CAbhishek KumarNo ratings yet

- Nifty: Trading StrategiesDocument2 pagesNifty: Trading StrategiesAbhishek KumarNo ratings yet

- Pharmacy Service Improvement atDocument5 pagesPharmacy Service Improvement atAbhishek KumarNo ratings yet

- Daimler ChryslerDocument13 pagesDaimler ChryslerAbhishek KumarNo ratings yet

- GatiDocument13 pagesGatiAbhishek KumarNo ratings yet

- Summer Preparatory Session: Club KaizenDocument40 pagesSummer Preparatory Session: Club KaizenAbhishek KumarNo ratings yet

- 1) in Your Marketing Plan, What Elements Are Strategic and What Elements Are Tactical?Document2 pages1) in Your Marketing Plan, What Elements Are Strategic and What Elements Are Tactical?Abhishek KumarNo ratings yet

- GammonDocument13 pagesGammonAbhishek KumarNo ratings yet

Download as pdf or txt

You might also like

- CH 09Document34 pagesCH 09Azhar SeptariNo ratings yet

- Trade Off Between Relevance and ReliabilityDocument1 pageTrade Off Between Relevance and ReliabilitylciimNo ratings yet

- FORT FrameworkDocument7 pagesFORT FrameworkAbhishek KumarNo ratings yet

- Align Technology IncDocument16 pagesAlign Technology IncAbhishek Kumar0% (1)

- Portfolio Selection & Asset AllocationDocument15 pagesPortfolio Selection & Asset AllocationNadea Fikrah RasuliNo ratings yet

- AEB14 SM CH17 v2Document31 pagesAEB14 SM CH17 v2RonLiu350% (1)

- The Information Approach To Decision UsefulnessDocument26 pagesThe Information Approach To Decision UsefulnessDiny Fariha ZakhirNo ratings yet

- Case 15-5 Xerox Corporation RecommendationsDocument6 pagesCase 15-5 Xerox Corporation RecommendationsgabrielyangNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument40 pagesFinancial Statement Analysis: K.R. SubramanyamRisky AlvinNo ratings yet

- Importance of Mutual FundsDocument14 pagesImportance of Mutual FundsMukesh Kumar SinghNo ratings yet

- Substantive Testing in The Revenue CycleDocument3 pagesSubstantive Testing in The Revenue CycleGeorgia FlorentinoNo ratings yet

- SAPM Portfolio RevisionDocument9 pagesSAPM Portfolio RevisionSpUnky RohitNo ratings yet

- Investment in Equities Versus Investment in Mutual FundDocument37 pagesInvestment in Equities Versus Investment in Mutual FundBob PanjabiNo ratings yet

- Bpe 34603 - LN 5 25 March 2019Document28 pagesBpe 34603 - LN 5 25 March 2019Irfan AzmanNo ratings yet

- Security Analysis and Portfolio Management: Master of Business AdministrationDocument80 pagesSecurity Analysis and Portfolio Management: Master of Business AdministrationSagar Paul'gNo ratings yet

- Portfolio Management ServicesDocument19 pagesPortfolio Management Serviceschawan_nikitaNo ratings yet

- Activity Based CostingDocument51 pagesActivity Based CostingAbdulyunus AmirNo ratings yet

- Scot ch07Document33 pagesScot ch07Diny Fariha ZakhirNo ratings yet

- Budgetary Control of IndiaDocument30 pagesBudgetary Control of IndiaNiks DujaniyaNo ratings yet

- Chapter 18 - Evaluating Investment PerformanceDocument62 pagesChapter 18 - Evaluating Investment PerformanceRavi PatelNo ratings yet

- Fundamental AnalysisDocument10 pagesFundamental AnalysisSaurabh Khurana100% (1)

- The Role of The AuditorDocument30 pagesThe Role of The AuditorALCIDES100% (1)

- The Measurement Approach To Decision UsefulnessDocument33 pagesThe Measurement Approach To Decision UsefulnessDiny Fariha ZakhirNo ratings yet

- Chapter 5 Portfolio Risk and Return Part IDocument25 pagesChapter 5 Portfolio Risk and Return Part ILaura StephanieNo ratings yet

- Legal Aspects of Project FinanceDocument9 pagesLegal Aspects of Project FinanceBlesson PerumalNo ratings yet

- Currency DerivativesDocument25 pagesCurrency DerivativesDarshitSejparaNo ratings yet

- Behavioral Finance and Technical AnalysisDocument18 pagesBehavioral Finance and Technical Analysispham terikNo ratings yet

- It Is A Stock Valuation Method - That Uses Financial and Economic Analysis - To Predict The Movement of Stock PricesDocument24 pagesIt Is A Stock Valuation Method - That Uses Financial and Economic Analysis - To Predict The Movement of Stock PricesAnonymous KN4pnOHmNo ratings yet

- Inter Psak 25Document28 pagesInter Psak 25vincent alvinNo ratings yet

- Cash Management ServicesDocument5 pagesCash Management ServicesMadhur AnandNo ratings yet

- Chapter 1 An Overview of The Investment ProcessDocument31 pagesChapter 1 An Overview of The Investment ProcessAbuzafar AbdullahNo ratings yet

- Financial Project FinalDocument46 pagesFinancial Project FinalBunty ShahNo ratings yet

- Asset Substitution ProblemDocument1 pageAsset Substitution ProblemNitish BhayrauNo ratings yet

- Fin3 Midterm ExamDocument8 pagesFin3 Midterm ExamBryan Lluisma100% (1)

- Capital Budgeting TechniquesDocument48 pagesCapital Budgeting TechniquesMuslimNo ratings yet

- Guideline BBDocument33 pagesGuideline BBsalam3500935No ratings yet

- Manajemen Keuangan - Merger and Acquisition PDFDocument36 pagesManajemen Keuangan - Merger and Acquisition PDFvrieskaNo ratings yet

- Mutual Funds: BY: Adneya Audhi Roll: 12304Document20 pagesMutual Funds: BY: Adneya Audhi Roll: 12304Adneya AudhiNo ratings yet

- Tactical Decision MakingDocument25 pagesTactical Decision MakingNizam JewelNo ratings yet

- Strategic Cost Management (SCM) FrameworkDocument11 pagesStrategic Cost Management (SCM) FrameworkcallmeasthaNo ratings yet

- Chapter One: Mcgraw-Hill/IrwinDocument17 pagesChapter One: Mcgraw-Hill/Irwinteraz2810No ratings yet

- Financial For Non Financial CitibanamexDocument147 pagesFinancial For Non Financial CitibanamexRaúl ArellanoNo ratings yet

- Chapter 6 - Using Discounted Cash Flow Analysis To Make Investment DecisionsDocument14 pagesChapter 6 - Using Discounted Cash Flow Analysis To Make Investment DecisionsSheena Rhei Del RosarioNo ratings yet

- Notes - MARKETING - OF - FINANCIAL SERVICES - 2020Document69 pagesNotes - MARKETING - OF - FINANCIAL SERVICES - 2020Rozy SinghNo ratings yet

- SAPMDocument93 pagesSAPMSOUMIKNo ratings yet

- Investors Preferences Towards Equity Indiabulls 2011Document81 pagesInvestors Preferences Towards Equity Indiabulls 2011chaluvadiin100% (2)

- Chapter 21 Internal, Operation and Governmental AuditingDocument23 pagesChapter 21 Internal, Operation and Governmental AuditinghidaNo ratings yet

- Investment Management: - Asset Allocation DecisionDocument23 pagesInvestment Management: - Asset Allocation DecisionyebegashetNo ratings yet

- Chapter 2Document40 pagesChapter 2Farapple24No ratings yet

- Financial RiskDocument13 pagesFinancial RiskHitesh Pant50% (2)

- Futures and OptionsDocument42 pagesFutures and OptionsMallikarjun RaoNo ratings yet

- Aunjum, Abbas, SajidDocument8 pagesAunjum, Abbas, SajidJuan Pablo Restrepo QuinteroNo ratings yet

- Financial EngineeringDocument18 pagesFinancial Engineeringtanay-mehta-3589100% (1)

- Optimal Portfolio ConstructionDocument14 pagesOptimal Portfolio ConstructionvigneshwaranmoorthyNo ratings yet

- Security Analysis and Portfolio Management, Bond Market in India.Document26 pagesSecurity Analysis and Portfolio Management, Bond Market in India.Gagandeep Singh BangarNo ratings yet

- Investment Analysis and Portfolio Management: Eighth Edition by Frank K. Reilly & Keith C. BrownDocument56 pagesInvestment Analysis and Portfolio Management: Eighth Edition by Frank K. Reilly & Keith C. BrownPayal MehtaNo ratings yet

- 2007 Ny Chotai I7Document7 pages2007 Ny Chotai I7Matthew BrownNo ratings yet

- 6205 LectureDocument27 pages6205 Lectureapi-3699305No ratings yet

- 4 InventoryManagementDocument44 pages4 InventoryManagementPrateek HosamaniNo ratings yet

- Exercise of Standard Costing: Standard Cost For Product White DiamondDocument18 pagesExercise of Standard Costing: Standard Cost For Product White DiamondSandip BansalNo ratings yet

- Antecedent Verification ProcessDocument4 pagesAntecedent Verification ProcessAbhishek KumarNo ratings yet

- Invoice OD109172599294660000Document2 pagesInvoice OD109172599294660000Abhishek KumarNo ratings yet

- Nifty: Trading StrategiesDocument2 pagesNifty: Trading StrategiesAbhishek KumarNo ratings yet

- An Example of Attribute Based MDS Using Discriminant AnalysisDocument17 pagesAn Example of Attribute Based MDS Using Discriminant AnalysisAbhishek KumarNo ratings yet

- Chapter 10 Regression SlidesDocument46 pagesChapter 10 Regression SlidesAbhishek KumarNo ratings yet

- Anova and The Design of Experiments: Welcome To Powerpoint Slides ForDocument22 pagesAnova and The Design of Experiments: Welcome To Powerpoint Slides ForAbhishek KumarNo ratings yet

- Indian Institute of Management Indore: MT ET CP AssignmentDocument2 pagesIndian Institute of Management Indore: MT ET CP AssignmentAbhishek KumarNo ratings yet

- Practice Set-2Document7 pagesPractice Set-2Abhishek Kumar100% (2)

- INOX Leisure LTD., - Location ListDocument2 pagesINOX Leisure LTD., - Location ListAbhishek KumarNo ratings yet

- Marketing of ServicesDocument6 pagesMarketing of ServicesAbhishek KumarNo ratings yet

- BC Sec CDocument2 pagesBC Sec CAbhishek KumarNo ratings yet

- Nifty: Trading StrategiesDocument2 pagesNifty: Trading StrategiesAbhishek KumarNo ratings yet

- Pharmacy Service Improvement atDocument5 pagesPharmacy Service Improvement atAbhishek KumarNo ratings yet

- Daimler ChryslerDocument13 pagesDaimler ChryslerAbhishek KumarNo ratings yet

- GatiDocument13 pagesGatiAbhishek KumarNo ratings yet

- Summer Preparatory Session: Club KaizenDocument40 pagesSummer Preparatory Session: Club KaizenAbhishek KumarNo ratings yet

- 1) in Your Marketing Plan, What Elements Are Strategic and What Elements Are Tactical?Document2 pages1) in Your Marketing Plan, What Elements Are Strategic and What Elements Are Tactical?Abhishek KumarNo ratings yet

- GammonDocument13 pagesGammonAbhishek KumarNo ratings yet