Download as ppt, pdf, or txt

You might also like

- Residential Status AssignmentDocument4 pagesResidential Status AssignmentSimran Kaur Khurana100% (1)

- Exemption From Custom DutyDocument13 pagesExemption From Custom DutyAbhinav PrasadNo ratings yet

- Jamia Millia Islamia: Project On Salaries (Session-2018-2019)Document21 pagesJamia Millia Islamia: Project On Salaries (Session-2018-2019)Harshit AgarwalNo ratings yet

- Taxation Law Assignment 1Document13 pagesTaxation Law Assignment 1Aditya PandeyNo ratings yet

- Tax Law Salary PDFDocument38 pagesTax Law Salary PDFabcNo ratings yet

- Ombudsman/Lokpal/Lokayukta and Central Vigilance CommissionDocument108 pagesOmbudsman/Lokpal/Lokayukta and Central Vigilance CommissionRozy MataniaNo ratings yet

- Customs DutyDocument8 pagesCustoms DutyRanvids100% (1)

- Income From Other SourcesDocument16 pagesIncome From Other SourcesRewant MehraNo ratings yet

- The Doctrine of Pith and SubstanceDocument6 pagesThe Doctrine of Pith and SubstanceRathin BanerjeeNo ratings yet

- Right To Strike in Legal Profession - 10th SemDocument10 pagesRight To Strike in Legal Profession - 10th SemtheamitnaNo ratings yet

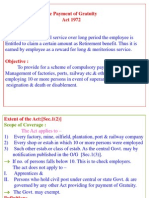

- The Payment of Gratuity Act 1972Document8 pagesThe Payment of Gratuity Act 1972Binny SinghNo ratings yet

- Assessment ProcedureDocument26 pagesAssessment ProcedureRohit Gupta100% (1)

- Income From House PropertyDocument26 pagesIncome From House Propertyraaziq100% (1)

- Faculty of Law: Jamia Millia IslamiaDocument18 pagesFaculty of Law: Jamia Millia IslamiaSwati KritiNo ratings yet

- CommissionDocument16 pagesCommissionMohiuddin KhanNo ratings yet

- Penology & VictimologyDocument17 pagesPenology & VictimologySaksham SharmaNo ratings yet

- Investigation of Affairs of A CompanyDocument18 pagesInvestigation of Affairs of A CompanyGufran KhanNo ratings yet

- International Labour Standards and Its Implementation in IndiaDocument9 pagesInternational Labour Standards and Its Implementation in IndiaDebasish NandaNo ratings yet

- Tax Law ProjectDocument24 pagesTax Law ProjectDeepesh SinghNo ratings yet

- Executing Courts Cpc-ProjectDocument14 pagesExecuting Courts Cpc-Projectkuldeep Roy SinghNo ratings yet

- Residential Status and Tax Incidence: Dr. Niti SaxenaDocument11 pagesResidential Status and Tax Incidence: Dr. Niti SaxenaYusufNo ratings yet

- Basis of Charge and Scope of TotalDocument24 pagesBasis of Charge and Scope of TotalSujithNo ratings yet

- Corporate Law IIDocument19 pagesCorporate Law IIIMRAN ALAMNo ratings yet

- Labour Law 2 PDFDocument24 pagesLabour Law 2 PDFShubham MishraNo ratings yet

- Residuary Powers of Parliament of IndiaDocument7 pagesResiduary Powers of Parliament of IndiaLeena SinghNo ratings yet

- Taxation Law ProjectDocument9 pagesTaxation Law ProjectPrince RajNo ratings yet

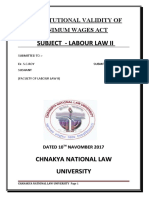

- Constitutional Validity of Minimum Wages ActDocument23 pagesConstitutional Validity of Minimum Wages ActNitish Kumar NaveenNo ratings yet

- Study On Freedom of Speech & Expression On MediaDocument20 pagesStudy On Freedom of Speech & Expression On MediaRAKESH KUMAR BAROINo ratings yet

- Chapter 5 Income of Other Persons Included in Assessee S Total IncomeDocument8 pagesChapter 5 Income of Other Persons Included in Assessee S Total IncomeRaj Pati SundiNo ratings yet

- Company Law Board and NCLTDocument13 pagesCompany Law Board and NCLTHritwick PurwarNo ratings yet

- Various Tax Authorities Under The Income TaxDocument18 pagesVarious Tax Authorities Under The Income TaxHardik SabbarwalNo ratings yet

- Standing Order - Labour LawDocument39 pagesStanding Order - Labour LawArunVermaNo ratings yet

- Income From Other SourcesDocument5 pagesIncome From Other SourcesGovarthanan NarasimhanNo ratings yet

- Minimum Wages Act Marked QuestionsDocument14 pagesMinimum Wages Act Marked Questionssohel alamNo ratings yet

- Income Under The Head Salary2Document142 pagesIncome Under The Head Salary2OnlineNo ratings yet

- Labour Law 3rd YearDocument20 pagesLabour Law 3rd YearAman SinghNo ratings yet

- The MRTP ActDocument4 pagesThe MRTP ActKuber BishtNo ratings yet

- Taxation Law ProjectDocument15 pagesTaxation Law Projectraj vardhan agarwalNo ratings yet

- JJURISDocument21 pagesJJURISAditya Singh100% (1)

- Winding Up of A Company: Paradigm Change in View of Insolvency and Bankruptcy CodeDocument15 pagesWinding Up of A Company: Paradigm Change in View of Insolvency and Bankruptcy CodeTaruna Shandilya100% (1)

- Concept and Interpretation of StatuteDocument17 pagesConcept and Interpretation of StatuteMohd AqibNo ratings yet

- Quasi Judicial Funtion of Administrative BodiesDocument18 pagesQuasi Judicial Funtion of Administrative BodiesSwati KritiNo ratings yet

- Money Bills in INDIADocument2 pagesMoney Bills in INDIAKumar AbhishekNo ratings yet

- Double Taxation ReliefDocument10 pagesDouble Taxation ReliefJeeva Antony VictoriaNo ratings yet

- Salient Features of Water Act, Air Act and Wildlife Protection ActDocument7 pagesSalient Features of Water Act, Air Act and Wildlife Protection ActRishabh DuttaNo ratings yet

- Income Tax AuthorityDocument15 pagesIncome Tax AuthorityMahin HasanNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, LucknowDocument14 pagesDr. Ram Manohar Lohiya National Law University, LucknowbhanwatiNo ratings yet

- Tax Law AssignmentDocument17 pagesTax Law AssignmentadibaNo ratings yet

- Decree and OrderDocument15 pagesDecree and OrderSajjan SharmaNo ratings yet

- Indra Sawhney v. Union of IndiaDocument15 pagesIndra Sawhney v. Union of IndiaDrago DoomNo ratings yet

- Taxing Power PDFDocument54 pagesTaxing Power PDFShravani BhardwajNo ratings yet

- Taxation Law ProjectDocument16 pagesTaxation Law ProjectAtinNo ratings yet

- Assignment On GST CouncilDocument4 pagesAssignment On GST CouncilSimran Kaur KhuranaNo ratings yet

- Competition Law Assignment by Ritika ShriwastavDocument18 pagesCompetition Law Assignment by Ritika ShriwastavSaurabh KumarNo ratings yet

- Environmental Law ProjectDocument28 pagesEnvironmental Law ProjectAmit VikramNo ratings yet

- Distribution of Tax RevenuesDocument9 pagesDistribution of Tax RevenuesSahajPuriNo ratings yet

- Insurance Regulatory and Development Authority (Irda) : A Law of Insurance Project OnDocument5 pagesInsurance Regulatory and Development Authority (Irda) : A Law of Insurance Project OnAnju PanickerNo ratings yet

- Hamza Tax Law 2Document18 pagesHamza Tax Law 2Ahmed ShujaNo ratings yet

- Minimum Wages Act - 1948Document8 pagesMinimum Wages Act - 1948Shaji Mullookkaaran100% (3)

- Martial Law in India: Historical, Comparative and Constitutional PerspectiveFrom EverandMartial Law in India: Historical, Comparative and Constitutional PerspectiveNo ratings yet

- Tax Planning and Management: Unit - IV Wealth Tax-Part-1 (Basics)Document55 pagesTax Planning and Management: Unit - IV Wealth Tax-Part-1 (Basics)anmoldeepsinghNo ratings yet

- Financial PlanDocument9 pagesFinancial PlananmoldeepsinghNo ratings yet

- Dupage County Technology ParkDocument27 pagesDupage County Technology ParkanmoldeepsinghNo ratings yet

- Deduction of Tax at SourceDocument23 pagesDeduction of Tax at SourceanmoldeepsinghNo ratings yet

- Accounting Standard 1: By: Manju Asht Lfbaa LPU PhagwaraDocument19 pagesAccounting Standard 1: By: Manju Asht Lfbaa LPU PhagwaraanmoldeepsinghNo ratings yet

- Shaikh Zahid Mukhtar V State of MaharashtraDocument245 pagesShaikh Zahid Mukhtar V State of MaharashtraBar & BenchNo ratings yet

- PLP Revision PDFDocument162 pagesPLP Revision PDFHedley Horler (scribd)No ratings yet

- PKWT Vs PWTTDocument6 pagesPKWT Vs PWTTTatak Bay AhmedNo ratings yet

- Ombudsman December 28 2007Document2 pagesOmbudsman December 28 2007Frank GallagherNo ratings yet

- The 2012 Philip C. Jessup Internaional Law Moot Court CompetitionDocument48 pagesThe 2012 Philip C. Jessup Internaional Law Moot Court Competitionprakash nanjanNo ratings yet

- 231-Arches v. Bellosillo G.R. No. L-23534 May 16, 1967Document2 pages231-Arches v. Bellosillo G.R. No. L-23534 May 16, 1967Jopan SJNo ratings yet

- Jardeleza v. Sereno Main Decision by Justice Jose Catral MendozaDocument35 pagesJardeleza v. Sereno Main Decision by Justice Jose Catral MendozaHornbook Rule100% (1)

- City of New York v. Baycrest Manor, Inc., No. D49668 (N.Y.A.D. Nov. 15, 2017)Document13 pagesCity of New York v. Baycrest Manor, Inc., No. D49668 (N.Y.A.D. Nov. 15, 2017)RHTNo ratings yet

- 2 Chemphil V CADocument4 pages2 Chemphil V CAGiancarlo Fernando0% (1)

- Annual Maintenance Contract: (LOG YOUR CALL AT TOLL FREE NO.: 1800-103-3854)Document7 pagesAnnual Maintenance Contract: (LOG YOUR CALL AT TOLL FREE NO.: 1800-103-3854)Priyam SrivastavNo ratings yet

- Tutorial Evidence 1 - Expert OpinionDocument13 pagesTutorial Evidence 1 - Expert OpinionNatasya ZulkifliNo ratings yet

- Gadia vs. SykesDocument5 pagesGadia vs. SykesmyschNo ratings yet

- MAQUIRAN, Azalea Marie S. 2015-0230Document2 pagesMAQUIRAN, Azalea Marie S. 2015-0230LeaNo ratings yet

- Rhode Island State Police - NEW ICE 287 (G) MOA (10/15/09)Document20 pagesRhode Island State Police - NEW ICE 287 (G) MOA (10/15/09)J CoxNo ratings yet

- Advanced Banking Law May 2010 Main PaperDocument3 pagesAdvanced Banking Law May 2010 Main PaperBasilio MaliwangaNo ratings yet

- Ford LetterDocument2 pagesFord LetterNew York PostNo ratings yet

- Adm. Case No. 492. September 5, 1967. Olegaria Blanza and Maria Pasion, ComplainantsDocument5 pagesAdm. Case No. 492. September 5, 1967. Olegaria Blanza and Maria Pasion, ComplainantsJoVic2020No ratings yet

- 18 Uscs - 2252Document3 pages18 Uscs - 2252Michael Lowe, Attorney at LawNo ratings yet

- OLE PH1 enDocument9 pagesOLE PH1 enbskienhvqyNo ratings yet

- (Rethinking Peace and Conflict Studies) Birgit Bräuchler (Auth.) - The Cultural Dimension of Peace - Decentralization and Reconciliation in Indonesia-Palgrave Macmillan UK (2015) PDFDocument277 pages(Rethinking Peace and Conflict Studies) Birgit Bräuchler (Auth.) - The Cultural Dimension of Peace - Decentralization and Reconciliation in Indonesia-Palgrave Macmillan UK (2015) PDFDepartemen Ilmu Politik FISIP UINo ratings yet

- Frequently Asked Questions About Rajya SabhaDocument22 pagesFrequently Asked Questions About Rajya SabhaPrithviraj SanningannavarNo ratings yet

- G.R. No. 186439Document7 pagesG.R. No. 186439Vin QuintoNo ratings yet

- Habeas Data: A Shield Against Terror: Biola, N. Josef Mari C. Special Proceedings - 3C 2016400052 Judge WaganDocument4 pagesHabeas Data: A Shield Against Terror: Biola, N. Josef Mari C. Special Proceedings - 3C 2016400052 Judge WaganN Josef BiolaNo ratings yet

- 72 PagesDocument72 pages72 PagesJaylou BobisNo ratings yet

- Internship ReportDocument4 pagesInternship ReportSilent Watcher100% (1)

- Agent StandardDocument16 pagesAgent StandardTran MaithoaNo ratings yet

- Scott V Cottrill Sexual AbuseDocument11 pagesScott V Cottrill Sexual Abusehooman ighaniNo ratings yet

- District: Sri S/o Sri. 32Document3 pagesDistrict: Sri S/o Sri. 32venugopal murthyNo ratings yet

- Mortgage and Pledge - Legal FormsDocument36 pagesMortgage and Pledge - Legal FormsRM MallorcaNo ratings yet

- Government of Pakistan Ministry of Human RightsDocument3 pagesGovernment of Pakistan Ministry of Human RightsAbdul raufNo ratings yet