Download as docx, pdf, or txt

You might also like

- Advanced Accounting Dayag Solution Manual PDFDocument234 pagesAdvanced Accounting Dayag Solution Manual PDFAnggë Crüz89% (9)

- E4-8 + P5-8Document4 pagesE4-8 + P5-8Oliviane Theodora Wenno100% (1)

- Accounting For Partnership and Corporation Solman Baysa Lupisan 2014 Chapter 2Document9 pagesAccounting For Partnership and Corporation Solman Baysa Lupisan 2014 Chapter 2Thamuz Lunox67% (3)

- Step 1: Transaction Analysis: Chapter 3: The 10-Steps in The Accounting CycleDocument16 pagesStep 1: Transaction Analysis: Chapter 3: The 10-Steps in The Accounting CycleSteffane Mae Sasutil100% (1)

- Test Bank Paccounting Information Systems Test Bank Paccounting Information SystemsDocument23 pagesTest Bank Paccounting Information Systems Test Bank Paccounting Information SystemsFrylle Kanz Harani PocsonNo ratings yet

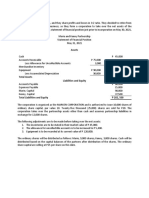

- Partnership FormationDocument13 pagesPartnership FormationPhilip Dan Jayson LarozaNo ratings yet

- SOALDocument2 pagesSOALjwtrmdhnNo ratings yet

- Formation TutorialDocument2 pagesFormation TutorialMegapoplocker MegapoplockerNo ratings yet

- Pakam, Khiezna E. Bsac-1b Assignment 3-FarDocument5 pagesPakam, Khiezna E. Bsac-1b Assignment 3-FarKhiezna PakamNo ratings yet

- Exercises On Formation of Partnership: Problem 1 Two Sole Proprietors Form A PartnershipDocument3 pagesExercises On Formation of Partnership: Problem 1 Two Sole Proprietors Form A PartnershipMa Lovely Bereño Moreno50% (4)

- AKD PB12-1B-dikonversiDocument3 pagesAKD PB12-1B-dikonversiNadyaNo ratings yet

- 1a Partnership FormationDocument8 pages1a Partnership FormationMark TaysonNo ratings yet

- Sample P-FDocument3 pagesSample P-FMYDMIOSYL ALABENo ratings yet

- Bajao-Activity 1-AccountingDocument21 pagesBajao-Activity 1-AccountingShen Calotes50% (2)

- PARTNERSHIP1Document27 pagesPARTNERSHIP1Christine Mae Mata100% (3)

- Chapter 2 ActivityDocument10 pagesChapter 2 ActivityBELARMINO LOUIE A.No ratings yet

- Partnership RequirementDocument6 pagesPartnership RequirementAlyssa Marie Miguel100% (1)

- 5Document3 pages5Janea Lorraine TanNo ratings yet

- FAR2 - Old Books and New Book - Incorp. ExamplesDocument5 pagesFAR2 - Old Books and New Book - Incorp. ExamplesMay BalangNo ratings yet

- Nature and Formation of A PartnershipDocument10 pagesNature and Formation of A PartnershipHans ManaliliNo ratings yet

- PArtnership FormationDocument6 pagesPArtnership FormationJasmine ActaNo ratings yet

- SOLMAN Chapter-2Document9 pagesSOLMAN Chapter-2Na JaeminNo ratings yet

- Tugas AKD 2 - 123 - Yanti GreceDocument3 pagesTugas AKD 2 - 123 - Yanti GreceSisilia RachelNo ratings yet

- Learning Task No.1Document3 pagesLearning Task No.1scryx bloodNo ratings yet

- Formation 2022 RDocument5 pagesFormation 2022 Rpamriri8No ratings yet

- Sample Problems Part FormDocument4 pagesSample Problems Part FormkenivanabejuelaNo ratings yet

- Chapter 5-1Document19 pagesChapter 5-1etaferaw beyeneNo ratings yet

- Name: Lecturer: Course Name: Course CodeDocument6 pagesName: Lecturer: Course Name: Course CodeJaredNo ratings yet

- To Record The Purchase of EquipmentDocument13 pagesTo Record The Purchase of EquipmentShane Nayah100% (1)

- Chapter 1 Practice ProblemsDocument5 pagesChapter 1 Practice ProblemsChristine Joyce SalvadorNo ratings yet

- ACC 201 Lesson Two - Conversion of Partnership To Limited Liability Companies-1Document4 pagesACC 201 Lesson Two - Conversion of Partnership To Limited Liability Companies-1Egede DavidNo ratings yet

- Formation Burgos RefozarDocument10 pagesFormation Burgos RefozarJasmine ActaNo ratings yet

- ch12 Problem Set CDocument2 pagesch12 Problem Set CMutiara TenriNo ratings yet

- Afar Assign 1Document8 pagesAfar Assign 1버니 모지코No ratings yet

- Answer KeyDocument10 pagesAnswer KeyEvelina Del RosarioNo ratings yet

- Partnership Dissolution: Accounting EntriesDocument4 pagesPartnership Dissolution: Accounting EntriesTawanda Tatenda HerbertNo ratings yet

- Solvay Adv Acc Exercises Case 4A - Auckland (Business - Combination) (Exam of 2003)Document4 pagesSolvay Adv Acc Exercises Case 4A - Auckland (Business - Combination) (Exam of 2003)lolaNo ratings yet

- HandOut No. 3 ParCor Partnership DissolutionDocument9 pagesHandOut No. 3 ParCor Partnership Dissolutionnatalie clyde matesNo ratings yet

- Partnership FormationDocument6 pagesPartnership FormationXajimarie StylesNo ratings yet

- 1712 Acct6174 Tmba TK4-W10-S15-R2 Team2Document7 pages1712 Acct6174 Tmba TK4-W10-S15-R2 Team2Adzinta Syamsa100% (1)

- Problem 4Document6 pagesProblem 4Peachy Rose TorenaNo ratings yet

- ACC 100 Partnership FormationDocument3 pagesACC 100 Partnership FormationAlfred DalaganNo ratings yet

- 1 Chapter 1 Partnership FormationDocument16 pages1 Chapter 1 Partnership FormationJymldy EnclnNo ratings yet

- Ansay, Allyson Charissa T - Activity 2Document3 pagesAnsay, Allyson Charissa T - Activity 2カイ みゆき100% (1)

- Afar 1 Module - Topic 4Document10 pagesAfar 1 Module - Topic 4mallarijhoana21No ratings yet

- Partnership Formation - Activity PDFDocument2 pagesPartnership Formation - Activity PDFWilliam TabuenaNo ratings yet

- Incomplete RecordsDocument11 pagesIncomplete Recordscaltonmbowe07No ratings yet

- Chapter 2 Practice KEYDocument17 pagesChapter 2 Practice KEYmartinmuebejayiNo ratings yet

- ReviewerDocument15 pagesReviewerALMA MORENANo ratings yet

- Activity 1. Partnership Formation Books of Roces: Bryle Jay P. Lape BSA-IIIDocument5 pagesActivity 1. Partnership Formation Books of Roces: Bryle Jay P. Lape BSA-IIIBryle Jay Lape40% (5)

- ACCCOB Garcia - Learning Module 2 1Document54 pagesACCCOB Garcia - Learning Module 2 1Sid Damien TanNo ratings yet

- Accounting QuizDocument5 pagesAccounting QuizLloyd Lameon0% (1)

- Partnership FormationDocument5 pagesPartnership FormationIce Voltaire Buban GuiangNo ratings yet

- CH 12 - SolutionDocument50 pagesCH 12 - SolutionMuhammad RehmanNo ratings yet

- Partnership RequirementDocument6 pagesPartnership RequirementLeanah TorioNo ratings yet

- FoA2 Week 2 Lesson and HW 3Document8 pagesFoA2 Week 2 Lesson and HW 3Christine Joyce MagoteNo ratings yet

- PricewaterhouseCoopers' Guide to the New Tax RulesFrom EverandPricewaterhouseCoopers' Guide to the New Tax RulesNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsFrom EverandA Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Il Cantante 2013 - FinanceDocument21 pagesIl Cantante 2013 - FinanceOliviane Theodora WennoNo ratings yet

- Kunci Jawaban Modul AKL Bu Iin - OlivethewennoDocument17 pagesKunci Jawaban Modul AKL Bu Iin - OlivethewennoOliviane Theodora WennoNo ratings yet

- English - Are You Normal? Part 1Document7 pagesEnglish - Are You Normal? Part 1Oliviane Theodora WennoNo ratings yet

- English - Are You Normal? PresentationDocument13 pagesEnglish - Are You Normal? PresentationOliviane Theodora WennoNo ratings yet

- 21-22 - Assignment - FOH - Part 2Document4 pages21-22 - Assignment - FOH - Part 2Oliviane Theodora WennoNo ratings yet

- Assignment For Meeting 7-10 - Accounting For CorporationDocument11 pagesAssignment For Meeting 7-10 - Accounting For CorporationOliviane Theodora WennoNo ratings yet

- 15-16-17-18 - Assignment - Long Term LiabilitiesDocument7 pages15-16-17-18 - Assignment - Long Term LiabilitiesOliviane Theodora WennoNo ratings yet

- 1-2 - Assignment - Current and Contingent LiabilitiesDocument6 pages1-2 - Assignment - Current and Contingent LiabilitiesOliviane Theodora Wenno0% (1)

- Mintzberg's 10 Managerial RolesDocument3 pagesMintzberg's 10 Managerial RolesOliviane Theodora Wenno100% (2)