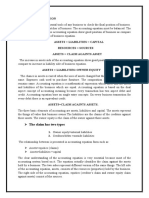

3 The Accounting Equation and How It Stays in Balance

3 The Accounting Equation and How It Stays in Balance

You might also like

- 3 How To Prepare A Balance SheetDocument4 pages3 How To Prepare A Balance Sheetapi-299265916100% (1)

- Financial Ratio AnalysisDocument4 pagesFinancial Ratio Analysisapi-299265916100% (1)

- 5 Adjusting Entries For Prepaid ExpenseDocument4 pages5 Adjusting Entries For Prepaid Expenseapi-299265916No ratings yet

- Accounting EquationDocument3 pagesAccounting EquationSittie Asiyah Dimaporo AbubacarNo ratings yet

- 2 Basic Accounting EquationDocument3 pages2 Basic Accounting EquationStarlette Kaye BadonNo ratings yet

- The Accounting Equation and How It Stays in BalanceDocument14 pagesThe Accounting Equation and How It Stays in BalanceLovely Mae LacasteNo ratings yet

- Chapter 3 Double Entry BookkeepingDocument16 pagesChapter 3 Double Entry BookkeepingNgoni Mukuku100% (2)

- Acc EqDocument5 pagesAcc EqBianca BgnNo ratings yet

- Summary of Videos Part II - Bano, Chariel PDocument3 pagesSummary of Videos Part II - Bano, Chariel PbanscharielNo ratings yet

- Double Entry AccountingDocument22 pagesDouble Entry AccountingLaten Cruxy100% (1)

- Basic Accounting EquationDocument3 pagesBasic Accounting EquationMaria Charise TongolNo ratings yet

- Accounting EquationDocument18 pagesAccounting EquationPradeep Gupta100% (1)

- Accounting EquationDocument4 pagesAccounting EquationCarlo Leandro LaronNo ratings yet

- Accounting EquationDocument10 pagesAccounting EquationYasmin khanNo ratings yet

- Accountancy Notes ch-3Document11 pagesAccountancy Notes ch-3Ansh JaiswalNo ratings yet

- Chapter II A For ManagersDocument46 pagesChapter II A For ManagersAsħîŞĥLøÝåNo ratings yet

- Properaite and Corporate Transaction AccountingDocument41 pagesProperaite and Corporate Transaction Accountingroheed100% (1)

- Accounting EquationDocument14 pagesAccounting Equationadane bayeNo ratings yet

- Chapter 3: Accruals and Deferrals AgendaDocument48 pagesChapter 3: Accruals and Deferrals AgendaWei DengNo ratings yet

- Double Entry SystemDocument5 pagesDouble Entry SystemSamiul HasanNo ratings yet

- Brand Generation College Dep't of Accounting and Financial: Basic Accounts Work Level IIDocument31 pagesBrand Generation College Dep't of Accounting and Financial: Basic Accounts Work Level IIhundegemechu68No ratings yet

- Definition of Certain Accounting TermsDocument4 pagesDefinition of Certain Accounting TermsAbhishek SachdevaNo ratings yet

- Accounting EquationDocument3 pagesAccounting EquationRowena DizonNo ratings yet

- When To Debit and Credit in AccountingDocument8 pagesWhen To Debit and Credit in Accountinguser31415No ratings yet

- Chapter OneDocument3 pagesChapter OneomerNo ratings yet

- Accounting Equation Service Business 6Document21 pagesAccounting Equation Service Business 6udayraj_vNo ratings yet

- 01 - Basic ConceptsDocument20 pages01 - Basic ConceptsSyed Mudussir HusainNo ratings yet

- Important Concepts ExplainedDocument4 pagesImportant Concepts ExplainedRamanaNo ratings yet

- Study Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Document19 pagesStudy Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Sandhra SethurajNo ratings yet

- Describe How The Following Business Transactions Affect The Three Elements of The AccountingDocument3 pagesDescribe How The Following Business Transactions Affect The Three Elements of The AccountingUserNo ratings yet

- FABM Q3 L3. SLeM 3 - A L+OEDocument15 pagesFABM Q3 L3. SLeM 3 - A L+OESophia MagdaraogNo ratings yet

- ACCT 1026 Lesson 3 PDFDocument11 pagesACCT 1026 Lesson 3 PDFAnnie RapanutNo ratings yet

- ACCT 1026 Lesson 3Document11 pagesACCT 1026 Lesson 3Daniel MadarangNo ratings yet

- Accounting Financial: General LedgerDocument8 pagesAccounting Financial: General LedgerSumeet KaurNo ratings yet

- Accounting ProjectDocument25 pagesAccounting ProjectLidianny CastilloNo ratings yet

- Week 1 - Accounting EquationDocument23 pagesWeek 1 - Accounting EquationJannyfaye RallecaNo ratings yet

- Accounting Equation: ModuleDocument13 pagesAccounting Equation: ModuleTushar SainiNo ratings yet

- Introduction To AccountingDocument2 pagesIntroduction To AccountingShahid MehmoodNo ratings yet

- Balance Sheet Analysis - TourismDocument10 pagesBalance Sheet Analysis - TourismMarieNo ratings yet

- Session 3 - ResumeDocument2 pagesSession 3 - ResumeVivi DuranNo ratings yet

- 11 Physics Notes Ch3Document29 pages11 Physics Notes Ch3Manish kumarNo ratings yet

- Introduction To Debits and CreditsDocument8 pagesIntroduction To Debits and CreditsMJ Dulin100% (1)

- Introduction To Debits and CreditsDocument16 pagesIntroduction To Debits and CreditsMeiRose100% (1)

- Acct 3Document12 pagesAcct 3Annie RapanutNo ratings yet

- FA1 Notes: (Business Transactions and Double Entry)Document24 pagesFA1 Notes: (Business Transactions and Double Entry)Waqas KhanNo ratings yet

- Financial Accounting & AnalysisDocument7 pagesFinancial Accounting & AnalysisMitaliNo ratings yet

- Accounting Adjusting EntryDocument20 pagesAccounting Adjusting EntryClemencia Masiba100% (1)

- Account TitlesDocument28 pagesAccount TitlesEfrelyn Grethel Baraya Alejandro100% (1)

- Lesson 1: Date Topics Activities or TasksDocument22 pagesLesson 1: Date Topics Activities or TasksKeeshia Mae Nashra ApilitNo ratings yet

- Accounting Equation For ACCADocument2 pagesAccounting Equation For ACCAtipu1sultan_1No ratings yet

- Double Entry Bookkeeping: 7 Step Guide To Processing Business AccountsDocument18 pagesDouble Entry Bookkeeping: 7 Step Guide To Processing Business AccountsChristy BascoNo ratings yet

- Fundamental Accounting Topic 3Document4 pagesFundamental Accounting Topic 3Hafiz AttaNo ratings yet

- SAP User Guide Accrual DeferalDocument48 pagesSAP User Guide Accrual DeferalwiwNo ratings yet

- Accounting Equation Lec 3rdDocument16 pagesAccounting Equation Lec 3rdWaqas KhanNo ratings yet

- Accounting EquationDocument23 pagesAccounting EquationGST TEAMNo ratings yet

- Individual Paper Accounting Equation Due 7-9-12Document6 pagesIndividual Paper Accounting Equation Due 7-9-12Constance Ben HamptonNo ratings yet

- Basic Accounting EquationDocument42 pagesBasic Accounting Equationlily smithNo ratings yet

- Accounting G10 - September 18, 2021Document4 pagesAccounting G10 - September 18, 2021wandeerNo ratings yet

- Accounting Equation: The Claim Has Two TypesDocument3 pagesAccounting Equation: The Claim Has Two TypesAmna YounasNo ratings yet

- Mba AssignmentsDocument8 pagesMba AssignmentsRamani RajNo ratings yet

- SSFABM1 ABM2000 Assignment1-3 ANSWERSDocument4 pagesSSFABM1 ABM2000 Assignment1-3 ANSWERSyannaNo ratings yet

- Teeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!From EverandTeeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!Rating: 2 out of 5 stars2/5 (1)

- Financial TableDocument9 pagesFinancial Tableapi-299265916No ratings yet

- 3 Income Statement ExamplesDocument3 pages3 Income Statement Examplesapi-299265916100% (1)

- 2 Income Statement FormatDocument3 pages2 Income Statement Formatapi-299265916No ratings yet

- 4 Revenue AccountsDocument1 page4 Revenue Accountsapi-299265916No ratings yet

- 2 Liability AccountsDocument2 pages2 Liability Accountsapi-299265916No ratings yet

- 5 Expense AccountsDocument2 pages5 Expense Accountsapi-299265916No ratings yet

- 2 Qualitative Characteristics of Financial InformationDocument2 pages2 Qualitative Characteristics of Financial Informationapi-299265916No ratings yet

- 6 Adjusting Entry For Depreciation ExpenseDocument3 pages6 Adjusting Entry For Depreciation Expenseapi-299265916No ratings yet

- 4 Accounting PrinciplesDocument3 pages4 Accounting Principlesapi-299265916No ratings yet

- Post-Closing Trial BalanceDocument4 pagesPost-Closing Trial Balanceapi-299265916100% (2)

- 1 Asset AccountsDocument3 pages1 Asset Accountsapi-299265916No ratings yet

- 2 How To Prepare A Statement of OwnerDocument4 pages2 How To Prepare A Statement of Ownerapi-299265916No ratings yet

- Reversing Entries Part 1Document3 pagesReversing Entries Part 1api-299265916100% (1)

- Closing EntriesDocument4 pagesClosing Entriesapi-299265916100% (1)

- 3 Standards of Ethical Conduct For Management AccountantsDocument2 pages3 Standards of Ethical Conduct For Management Accountantsapi-299265916No ratings yet

- 8 Adjusted Trial BalanceDocument3 pages8 Adjusted Trial Balanceapi-299265916100% (1)

- 1 How To Prepare An Income StatementDocument4 pages1 How To Prepare An Income Statementapi-299265916No ratings yet

- 7 Adjusting Entry For Bad Debts ExpenseDocument2 pages7 Adjusting Entry For Bad Debts Expenseapi-299265916No ratings yet

- 2 Adjusting Entry For Accrued RevenueDocument2 pages2 Adjusting Entry For Accrued Revenueapi-299265916No ratings yet

- 3 Adjusting Entry For Accrued ExpensesDocument2 pages3 Adjusting Entry For Accrued Expensesapi-299265916No ratings yet

- 2 Rules of Debit and CreditDocument3 pages2 Rules of Debit and Creditapi-2992659160% (1)

- 5 Journal Entries More ExamplesDocument4 pages5 Journal Entries More Examplesapi-299265916No ratings yet

- 6 Posting To The LedgerDocument3 pages6 Posting To The Ledgerapi-299265916No ratings yet

- 4 Journal EntriesDocument2 pages4 Journal Entriesapi-299265916No ratings yet

- 3 Chart of AccountsDocument3 pages3 Chart of Accountsapi-299265916No ratings yet

- 8 Correcting EntriesDocument3 pages8 Correcting Entriesapi-299265916No ratings yet

- 1 Understanding and Analyzing Business TransactionsDocument2 pages1 Understanding and Analyzing Business Transactionsapi-299265916No ratings yet

Download as pdf or txt

You might also like

- 3 How To Prepare A Balance SheetDocument4 pages3 How To Prepare A Balance Sheetapi-299265916100% (1)

- Financial Ratio AnalysisDocument4 pagesFinancial Ratio Analysisapi-299265916100% (1)

- 5 Adjusting Entries For Prepaid ExpenseDocument4 pages5 Adjusting Entries For Prepaid Expenseapi-299265916No ratings yet

- Accounting EquationDocument3 pagesAccounting EquationSittie Asiyah Dimaporo AbubacarNo ratings yet

- 2 Basic Accounting EquationDocument3 pages2 Basic Accounting EquationStarlette Kaye BadonNo ratings yet

- The Accounting Equation and How It Stays in BalanceDocument14 pagesThe Accounting Equation and How It Stays in BalanceLovely Mae LacasteNo ratings yet

- Chapter 3 Double Entry BookkeepingDocument16 pagesChapter 3 Double Entry BookkeepingNgoni Mukuku100% (2)

- Acc EqDocument5 pagesAcc EqBianca BgnNo ratings yet

- Summary of Videos Part II - Bano, Chariel PDocument3 pagesSummary of Videos Part II - Bano, Chariel PbanscharielNo ratings yet

- Double Entry AccountingDocument22 pagesDouble Entry AccountingLaten Cruxy100% (1)

- Basic Accounting EquationDocument3 pagesBasic Accounting EquationMaria Charise TongolNo ratings yet

- Accounting EquationDocument18 pagesAccounting EquationPradeep Gupta100% (1)

- Accounting EquationDocument4 pagesAccounting EquationCarlo Leandro LaronNo ratings yet

- Accounting EquationDocument10 pagesAccounting EquationYasmin khanNo ratings yet

- Accountancy Notes ch-3Document11 pagesAccountancy Notes ch-3Ansh JaiswalNo ratings yet

- Chapter II A For ManagersDocument46 pagesChapter II A For ManagersAsħîŞĥLøÝåNo ratings yet

- Properaite and Corporate Transaction AccountingDocument41 pagesProperaite and Corporate Transaction Accountingroheed100% (1)

- Accounting EquationDocument14 pagesAccounting Equationadane bayeNo ratings yet

- Chapter 3: Accruals and Deferrals AgendaDocument48 pagesChapter 3: Accruals and Deferrals AgendaWei DengNo ratings yet

- Double Entry SystemDocument5 pagesDouble Entry SystemSamiul HasanNo ratings yet

- Brand Generation College Dep't of Accounting and Financial: Basic Accounts Work Level IIDocument31 pagesBrand Generation College Dep't of Accounting and Financial: Basic Accounts Work Level IIhundegemechu68No ratings yet

- Definition of Certain Accounting TermsDocument4 pagesDefinition of Certain Accounting TermsAbhishek SachdevaNo ratings yet

- Accounting EquationDocument3 pagesAccounting EquationRowena DizonNo ratings yet

- When To Debit and Credit in AccountingDocument8 pagesWhen To Debit and Credit in Accountinguser31415No ratings yet

- Chapter OneDocument3 pagesChapter OneomerNo ratings yet

- Accounting Equation Service Business 6Document21 pagesAccounting Equation Service Business 6udayraj_vNo ratings yet

- 01 - Basic ConceptsDocument20 pages01 - Basic ConceptsSyed Mudussir HusainNo ratings yet

- Important Concepts ExplainedDocument4 pagesImportant Concepts ExplainedRamanaNo ratings yet

- Study Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Document19 pagesStudy Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Sandhra SethurajNo ratings yet

- Describe How The Following Business Transactions Affect The Three Elements of The AccountingDocument3 pagesDescribe How The Following Business Transactions Affect The Three Elements of The AccountingUserNo ratings yet

- FABM Q3 L3. SLeM 3 - A L+OEDocument15 pagesFABM Q3 L3. SLeM 3 - A L+OESophia MagdaraogNo ratings yet

- ACCT 1026 Lesson 3 PDFDocument11 pagesACCT 1026 Lesson 3 PDFAnnie RapanutNo ratings yet

- ACCT 1026 Lesson 3Document11 pagesACCT 1026 Lesson 3Daniel MadarangNo ratings yet

- Accounting Financial: General LedgerDocument8 pagesAccounting Financial: General LedgerSumeet KaurNo ratings yet

- Accounting ProjectDocument25 pagesAccounting ProjectLidianny CastilloNo ratings yet

- Week 1 - Accounting EquationDocument23 pagesWeek 1 - Accounting EquationJannyfaye RallecaNo ratings yet

- Accounting Equation: ModuleDocument13 pagesAccounting Equation: ModuleTushar SainiNo ratings yet

- Introduction To AccountingDocument2 pagesIntroduction To AccountingShahid MehmoodNo ratings yet

- Balance Sheet Analysis - TourismDocument10 pagesBalance Sheet Analysis - TourismMarieNo ratings yet

- Session 3 - ResumeDocument2 pagesSession 3 - ResumeVivi DuranNo ratings yet

- 11 Physics Notes Ch3Document29 pages11 Physics Notes Ch3Manish kumarNo ratings yet

- Introduction To Debits and CreditsDocument8 pagesIntroduction To Debits and CreditsMJ Dulin100% (1)

- Introduction To Debits and CreditsDocument16 pagesIntroduction To Debits and CreditsMeiRose100% (1)

- Acct 3Document12 pagesAcct 3Annie RapanutNo ratings yet

- FA1 Notes: (Business Transactions and Double Entry)Document24 pagesFA1 Notes: (Business Transactions and Double Entry)Waqas KhanNo ratings yet

- Financial Accounting & AnalysisDocument7 pagesFinancial Accounting & AnalysisMitaliNo ratings yet

- Accounting Adjusting EntryDocument20 pagesAccounting Adjusting EntryClemencia Masiba100% (1)

- Account TitlesDocument28 pagesAccount TitlesEfrelyn Grethel Baraya Alejandro100% (1)

- Lesson 1: Date Topics Activities or TasksDocument22 pagesLesson 1: Date Topics Activities or TasksKeeshia Mae Nashra ApilitNo ratings yet

- Accounting Equation For ACCADocument2 pagesAccounting Equation For ACCAtipu1sultan_1No ratings yet

- Double Entry Bookkeeping: 7 Step Guide To Processing Business AccountsDocument18 pagesDouble Entry Bookkeeping: 7 Step Guide To Processing Business AccountsChristy BascoNo ratings yet

- Fundamental Accounting Topic 3Document4 pagesFundamental Accounting Topic 3Hafiz AttaNo ratings yet

- SAP User Guide Accrual DeferalDocument48 pagesSAP User Guide Accrual DeferalwiwNo ratings yet

- Accounting Equation Lec 3rdDocument16 pagesAccounting Equation Lec 3rdWaqas KhanNo ratings yet

- Accounting EquationDocument23 pagesAccounting EquationGST TEAMNo ratings yet

- Individual Paper Accounting Equation Due 7-9-12Document6 pagesIndividual Paper Accounting Equation Due 7-9-12Constance Ben HamptonNo ratings yet

- Basic Accounting EquationDocument42 pagesBasic Accounting Equationlily smithNo ratings yet

- Accounting G10 - September 18, 2021Document4 pagesAccounting G10 - September 18, 2021wandeerNo ratings yet

- Accounting Equation: The Claim Has Two TypesDocument3 pagesAccounting Equation: The Claim Has Two TypesAmna YounasNo ratings yet

- Mba AssignmentsDocument8 pagesMba AssignmentsRamani RajNo ratings yet

- SSFABM1 ABM2000 Assignment1-3 ANSWERSDocument4 pagesSSFABM1 ABM2000 Assignment1-3 ANSWERSyannaNo ratings yet

- Teeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!From EverandTeeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!Rating: 2 out of 5 stars2/5 (1)

- Financial TableDocument9 pagesFinancial Tableapi-299265916No ratings yet

- 3 Income Statement ExamplesDocument3 pages3 Income Statement Examplesapi-299265916100% (1)

- 2 Income Statement FormatDocument3 pages2 Income Statement Formatapi-299265916No ratings yet

- 4 Revenue AccountsDocument1 page4 Revenue Accountsapi-299265916No ratings yet

- 2 Liability AccountsDocument2 pages2 Liability Accountsapi-299265916No ratings yet

- 5 Expense AccountsDocument2 pages5 Expense Accountsapi-299265916No ratings yet

- 2 Qualitative Characteristics of Financial InformationDocument2 pages2 Qualitative Characteristics of Financial Informationapi-299265916No ratings yet

- 6 Adjusting Entry For Depreciation ExpenseDocument3 pages6 Adjusting Entry For Depreciation Expenseapi-299265916No ratings yet

- 4 Accounting PrinciplesDocument3 pages4 Accounting Principlesapi-299265916No ratings yet

- Post-Closing Trial BalanceDocument4 pagesPost-Closing Trial Balanceapi-299265916100% (2)

- 1 Asset AccountsDocument3 pages1 Asset Accountsapi-299265916No ratings yet

- 2 How To Prepare A Statement of OwnerDocument4 pages2 How To Prepare A Statement of Ownerapi-299265916No ratings yet

- Reversing Entries Part 1Document3 pagesReversing Entries Part 1api-299265916100% (1)

- Closing EntriesDocument4 pagesClosing Entriesapi-299265916100% (1)

- 3 Standards of Ethical Conduct For Management AccountantsDocument2 pages3 Standards of Ethical Conduct For Management Accountantsapi-299265916No ratings yet

- 8 Adjusted Trial BalanceDocument3 pages8 Adjusted Trial Balanceapi-299265916100% (1)

- 1 How To Prepare An Income StatementDocument4 pages1 How To Prepare An Income Statementapi-299265916No ratings yet

- 7 Adjusting Entry For Bad Debts ExpenseDocument2 pages7 Adjusting Entry For Bad Debts Expenseapi-299265916No ratings yet

- 2 Adjusting Entry For Accrued RevenueDocument2 pages2 Adjusting Entry For Accrued Revenueapi-299265916No ratings yet

- 3 Adjusting Entry For Accrued ExpensesDocument2 pages3 Adjusting Entry For Accrued Expensesapi-299265916No ratings yet

- 2 Rules of Debit and CreditDocument3 pages2 Rules of Debit and Creditapi-2992659160% (1)

- 5 Journal Entries More ExamplesDocument4 pages5 Journal Entries More Examplesapi-299265916No ratings yet

- 6 Posting To The LedgerDocument3 pages6 Posting To The Ledgerapi-299265916No ratings yet

- 4 Journal EntriesDocument2 pages4 Journal Entriesapi-299265916No ratings yet

- 3 Chart of AccountsDocument3 pages3 Chart of Accountsapi-299265916No ratings yet

- 8 Correcting EntriesDocument3 pages8 Correcting Entriesapi-299265916No ratings yet

- 1 Understanding and Analyzing Business TransactionsDocument2 pages1 Understanding and Analyzing Business Transactionsapi-299265916No ratings yet