Final - Dac Rto Multan 07-8 19.04.2010

Final - Dac Rto Multan 07-8 19.04.2010

You might also like

- Shree Karthik Papers Ltdvs Deputy Commissionerof Income TDocument4 pagesShree Karthik Papers Ltdvs Deputy Commissionerof Income TKaran GannaNo ratings yet

- CaselawsDocument5 pagesCaselawsRam PrasadNo ratings yet

- To Be Replied Within 24 HoursDocument24 pagesTo Be Replied Within 24 HoursIjaz AwanNo ratings yet

- Samar-I Electric Cooperative, Petitioner, vs. Commissioner of Internal Revenue, Respondent.Document18 pagesSamar-I Electric Cooperative, Petitioner, vs. Commissioner of Internal Revenue, Respondent.Maria Nicole Vaneetee100% (1)

- Session Paper - 6 (Questions & Answers), For Overall Discussion On Principles of Taxation of CLDocument3 pagesSession Paper - 6 (Questions & Answers), For Overall Discussion On Principles of Taxation of CLProgga MehnazNo ratings yet

- SEZ Units Continues To Be Exempt From MATDocument23 pagesSEZ Units Continues To Be Exempt From MATjaksandcoNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- 2023_07_15__2023__149_taxmann_com_169__Mumbai___Trib___31_03_2023__Vodafone_Idea_Ltd__vs__Assistant_CoDocument14 pages2023_07_15__2023__149_taxmann_com_169__Mumbai___Trib___31_03_2023__Vodafone_Idea_Ltd__vs__Assistant_Copoojasinghai0207No ratings yet

- Bhati Axa Life InsuranceDocument40 pagesBhati Axa Life InsuranceshashankNo ratings yet

- G.R. Nos. 198729-30 PDFDocument7 pagesG.R. Nos. 198729-30 PDFJerome CasasNo ratings yet

- Samar-I Electric Cooperative v. CIR (744 SCRA 459)Document9 pagesSamar-I Electric Cooperative v. CIR (744 SCRA 459)Karl MinglanaNo ratings yet

- 6 CIR-v - G.R.-No.-21680-81Document2 pages6 CIR-v - G.R.-No.-21680-81fallon caringtonNo ratings yet

- 167.SAMELCO-1 Vs CIRDocument11 pages167.SAMELCO-1 Vs CIRClyde KitongNo ratings yet

- DRRADocument2 pagesDRRAShahaan ZulfiqarNo ratings yet

- Cir Vs TaganitoDocument22 pagesCir Vs Taganitocarla maeNo ratings yet

- 15 04 16 Case2Document26 pages15 04 16 Case2tamanna.vkacaNo ratings yet

- Assessment Under The It ActDocument34 pagesAssessment Under The It ActbhanumaaaNo ratings yet

- 105 IMPSA Construction Corporation vs. CIR (CTA EB Case No. 685, May 24, 2011)Document10 pages105 IMPSA Construction Corporation vs. CIR (CTA EB Case No. 685, May 24, 2011)Alfred GarciaNo ratings yet

- Statement On Impact of Audit Qualifications For The Period Ended March 31, 2015 (Company Update)Document5 pagesStatement On Impact of Audit Qualifications For The Period Ended March 31, 2015 (Company Update)Shyam SunderNo ratings yet

- Citation: CDJ 1991 SC 262 Court: Case No: JudgesDocument15 pagesCitation: CDJ 1991 SC 262 Court: Case No: JudgesNomosvistasNo ratings yet

- Tolia AppealDocument7 pagesTolia Appealmau8684No ratings yet

- Deputy Director of Income TaxE I2 Vs The American IU2018111218165039195COM490153Document9 pagesDeputy Director of Income TaxE I2 Vs The American IU2018111218165039195COM490153Yashaswi KumarNo ratings yet

- Internal Circular (Restricted Circular For Office Use Only)Document16 pagesInternal Circular (Restricted Circular For Office Use Only)Manish K JadhavNo ratings yet

- Cta 2D CV 07000 D 2008jan09 RefDocument14 pagesCta 2D CV 07000 D 2008jan09 RefSharon AgapuyanNo ratings yet

- Cta 2D CV 06710 D 2006jul31 Ass PDFDocument19 pagesCta 2D CV 06710 D 2006jul31 Ass PDFFlois SevillaNo ratings yet

- Penalty U/s 271 (1) (C) Case Reference Shree Nirmal Commercial Ltd. v. CitDocument39 pagesPenalty U/s 271 (1) (C) Case Reference Shree Nirmal Commercial Ltd. v. CitCAclubindiaNo ratings yet

- Dell International Services India PVT LTD Vs The IIL2022040522170528204COM311728Document30 pagesDell International Services India PVT LTD Vs The IIL2022040522170528204COM311728Rıtesha DasNo ratings yet

- 226 CIR v. Sony Philippines, IncDocument4 pages226 CIR v. Sony Philippines, IncclarkorjaloNo ratings yet

- CIR v. Next Mobile IncDocument9 pagesCIR v. Next Mobile IncMeg ReyesNo ratings yet

- 2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsDocument11 pages2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsAbhishek JainNo ratings yet

- CBK V CIRDocument7 pagesCBK V CIRAna BelleNo ratings yet

- Cir VS StiDocument6 pagesCir VS StiNaomiJean InotNo ratings yet

- Itat Nos 212Document8 pagesItat Nos 212Atul GoelNo ratings yet

- Incometax 29 09 2022Document3 pagesIncometax 29 09 2022nitishbhaskaran4No ratings yet

- Chapter 118Document26 pagesChapter 118Nitin SrivastavaNo ratings yet

- Pbcom vs. Cir 302 Scra 241Document11 pagesPbcom vs. Cir 302 Scra 241Clarinda MerleNo ratings yet

- Modern Imaging Solutions Case Tax FRDocument18 pagesModern Imaging Solutions Case Tax FRLykel LavillaNo ratings yet

- SM Land, Inc., Et Al. v. City of Manila, Et Al., G.R. No. 197151, October 22,2012Document13 pagesSM Land, Inc., Et Al. v. City of Manila, Et Al., G.R. No. 197151, October 22,2012d-fbuser-49417072No ratings yet

- R.kasi Vishwanathan & Bros. V Assist CIt (2014) 42 Taxmann - Com 176 Section 139 (5) - It 475-11 28.3.2016Document7 pagesR.kasi Vishwanathan & Bros. V Assist CIt (2014) 42 Taxmann - Com 176 Section 139 (5) - It 475-11 28.3.2016Prabhash ChandNo ratings yet

- आयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Document8 pagesआयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Saksham ShrivastavNo ratings yet

- CIR vs. Petron, G. R. No. 185568 (2012)Document14 pagesCIR vs. Petron, G. R. No. 185568 (2012)Aaron James PuasoNo ratings yet

- CIR vs. Transitions Optical, Inc., GR No. 227544, 22 November 2017Document14 pagesCIR vs. Transitions Optical, Inc., GR No. 227544, 22 November 2017Christopher ArellanoNo ratings yet

- 2022LHC4885Document8 pages2022LHC4885Shah Meer GichkiNo ratings yet

- 22 Team - Energy - Corp. - v. - Commissioner - of - Internal20210505-11-1jxu1oaDocument28 pages22 Team - Energy - Corp. - v. - Commissioner - of - Internal20210505-11-1jxu1oaKempetsNo ratings yet

- Rajesh Kumar Sharma - Submission Before ITAT - Penalty - 201617Document6 pagesRajesh Kumar Sharma - Submission Before ITAT - Penalty - 201617sssadangiNo ratings yet

- CIR v. Standard Chartered BankDocument11 pagesCIR v. Standard Chartered Bankf919No ratings yet

- CIR Vs ST. LukesDocument9 pagesCIR Vs ST. Lukesdolce gustoNo ratings yet

- PRADIPDocument7 pagesPRADIPGovindNo ratings yet

- 3 - CIR v. PetronDocument7 pages3 - CIR v. PetronJaysieMicabaloNo ratings yet

- CIR v. TRANSFIELD PHILIPPINESDocument16 pagesCIR v. TRANSFIELD PHILIPPINESFaustina del RosarioNo ratings yet

- 168222-2013-First Lepanto Taisho Insurance Corp. V.Document3 pages168222-2013-First Lepanto Taisho Insurance Corp. V.John Kyle LluzNo ratings yet

- Ford PDFDocument3 pagesFord PDFAbhay DesaiNo ratings yet

- 2002 83 ITD 151 Delhi SB 2002 77 TTJ 387 Delhi SB 01 08 2002highlightedDocument12 pages2002 83 ITD 151 Delhi SB 2002 77 TTJ 387 Delhi SB 01 08 2002highlightedSnigdha MazumdarNo ratings yet

- Rhombus Energy v. CirDocument15 pagesRhombus Energy v. CirSteven TylerNo ratings yet

- Gateway Technolabs P LTDDocument4 pagesGateway Technolabs P LTDDayavanti Nilesh RanaNo ratings yet

- Perfetti Van Melle IndiaDocument18 pagesPerfetti Van Melle IndiaramitkatyalNo ratings yet

- G.R. No. 227544 Commissioner OF Internal REVENUE, Petitioner Transitions Optical Philippines, Inc., Respondent Decision Leonen, J.Document7 pagesG.R. No. 227544 Commissioner OF Internal REVENUE, Petitioner Transitions Optical Philippines, Inc., Respondent Decision Leonen, J.JaysonNo ratings yet

- Kme - Goa Sof - Ay 2023-24 - 06052024Document6 pagesKme - Goa Sof - Ay 2023-24 - 06052024anil.singh3131No ratings yet

- Mindanao Ii Geothermal Partnership VS CirDocument27 pagesMindanao Ii Geothermal Partnership VS CirAnthony Blaine Benels Domingo-MpaNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- S 0232 01Document50 pagesS 0232 01Shahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument7 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Slip 0232 01 2019Document513 pagesSlip 0232 01 2019Shahaan ZulfiqarNo ratings yet

- NO Marriage CertificateDocument5 pagesNO Marriage CertificateShahaan ZulfiqarNo ratings yet

- Para NO Cases Under Process Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and VerifiedDocument6 pagesPara NO Cases Under Process Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument7 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument5 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument6 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument6 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument6 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- 114 CasesDocument29 pages114 CasesShahaan ZulfiqarNo ratings yet

- Drra 12Document966 pagesDrra 12Shahaan ZulfiqarNo ratings yet

- 2011-12 - Dac 14.01.2020Document38 pages2011-12 - Dac 14.01.2020Shahaan ZulfiqarNo ratings yet

- 2017-18 - 17.08.2020 Multan Audit ReportDocument25 pages2017-18 - 17.08.2020 Multan Audit ReportShahaan ZulfiqarNo ratings yet

- 2013-14 - Multan 25112019Document47 pages2013-14 - Multan 25112019Shahaan ZulfiqarNo ratings yet

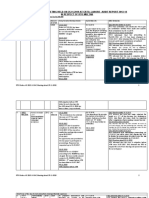

MINUTES OF DAC MEETING OF AUDIT REPORT 2007-08

IN RESPECT OF RTO, MULTAN (19-4-2010 AT LAHORE)

Excess Determination Of Refunds

39

4.1/245

Hyundai

Engineering &

Construction

Co.Ltd.

199798

Rs. 81,679,059/-

W.Paper 2007-08 VRI.MEETING 05 TO 10.4.2010 RTO MN

CONTESTD

Observation of the audit authority is

not admitted. Original assessment

for the charge year 1997-98 was

completed u/s 62 of the repealed

ordinance, 1979 on 14-07-1999 by

the

DCIT

Company

Circle

Peshawar creating refund of Rs.

27,199,383/- and refund voucher for

the same amount was issued on

12-11-1999 by the than assessing

officer.

Assessment was contested in

appeal which was set aside and

fresh assessment was finalized u/s

62/132 on 30-06-2001 at net loss of

(469,660,422). This assessment

was again revised u/s 62/135 on

30-06-2004 and income was

assessed at Rs. 168,412,272/therefore income tax was charged

accordingly. However the assessee

again filed appeal before the CIT

(A) Multan who through its

combined appellate order bearing

A.O No. 600 to 603 dated 14-122004 confirmed main additions

whereas certain additions of P&L

account were deleted or set aside.

The taxpayer preferred 2nd appeal

before the learned ITAT, which was

decided vide ITA No. 323/LB/2005

dated

07-01-2008

whereby it has been directed that all

additions / add backs, which

remained the subject matter of

litigation earlier should be deleted.

To provide the

record to audit

and report

compliance by

30-9-2008

Record will be

produced at the

time of

verification.

Under

examination with

Audit

The DAC directed

the audit to verify

the contention of

the department

by 5-5-2010.

Meaning thereby declared version

of the taxpayer stands accepted.

Appeal effect has been given

resulting in loss of Rs. (23,587,158)

has been assessed creating further

refund of Rs. (17,000,938) vide IT30 dated

30-052008.

As regard observation regarding

incorrect issuance of refund for the

assessment year 2000-01 there is

no connection of this refund with the

refund of tax year 1997-98. Both

refunds issued on 12-11-1999 and

21-12-2006 are legally correct and

in accordance with law.

Audit

observation is on the basis of a

presumption which is un-wanted.

Photo stat copy of IT-30 dated 3005-2008 is enclosed. Audit Para

may be settled.

W.Paper 2007-08 VRI.MEETING 05 TO 10.4.2010 RTO MN

You might also like

- Shree Karthik Papers Ltdvs Deputy Commissionerof Income TDocument4 pagesShree Karthik Papers Ltdvs Deputy Commissionerof Income TKaran GannaNo ratings yet

- CaselawsDocument5 pagesCaselawsRam PrasadNo ratings yet

- To Be Replied Within 24 HoursDocument24 pagesTo Be Replied Within 24 HoursIjaz AwanNo ratings yet

- Samar-I Electric Cooperative, Petitioner, vs. Commissioner of Internal Revenue, Respondent.Document18 pagesSamar-I Electric Cooperative, Petitioner, vs. Commissioner of Internal Revenue, Respondent.Maria Nicole Vaneetee100% (1)

- Session Paper - 6 (Questions & Answers), For Overall Discussion On Principles of Taxation of CLDocument3 pagesSession Paper - 6 (Questions & Answers), For Overall Discussion On Principles of Taxation of CLProgga MehnazNo ratings yet

- SEZ Units Continues To Be Exempt From MATDocument23 pagesSEZ Units Continues To Be Exempt From MATjaksandcoNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- 2023_07_15__2023__149_taxmann_com_169__Mumbai___Trib___31_03_2023__Vodafone_Idea_Ltd__vs__Assistant_CoDocument14 pages2023_07_15__2023__149_taxmann_com_169__Mumbai___Trib___31_03_2023__Vodafone_Idea_Ltd__vs__Assistant_Copoojasinghai0207No ratings yet

- Bhati Axa Life InsuranceDocument40 pagesBhati Axa Life InsuranceshashankNo ratings yet

- G.R. Nos. 198729-30 PDFDocument7 pagesG.R. Nos. 198729-30 PDFJerome CasasNo ratings yet

- Samar-I Electric Cooperative v. CIR (744 SCRA 459)Document9 pagesSamar-I Electric Cooperative v. CIR (744 SCRA 459)Karl MinglanaNo ratings yet

- 6 CIR-v - G.R.-No.-21680-81Document2 pages6 CIR-v - G.R.-No.-21680-81fallon caringtonNo ratings yet

- 167.SAMELCO-1 Vs CIRDocument11 pages167.SAMELCO-1 Vs CIRClyde KitongNo ratings yet

- DRRADocument2 pagesDRRAShahaan ZulfiqarNo ratings yet

- Cir Vs TaganitoDocument22 pagesCir Vs Taganitocarla maeNo ratings yet

- 15 04 16 Case2Document26 pages15 04 16 Case2tamanna.vkacaNo ratings yet

- Assessment Under The It ActDocument34 pagesAssessment Under The It ActbhanumaaaNo ratings yet

- 105 IMPSA Construction Corporation vs. CIR (CTA EB Case No. 685, May 24, 2011)Document10 pages105 IMPSA Construction Corporation vs. CIR (CTA EB Case No. 685, May 24, 2011)Alfred GarciaNo ratings yet

- Statement On Impact of Audit Qualifications For The Period Ended March 31, 2015 (Company Update)Document5 pagesStatement On Impact of Audit Qualifications For The Period Ended March 31, 2015 (Company Update)Shyam SunderNo ratings yet

- Citation: CDJ 1991 SC 262 Court: Case No: JudgesDocument15 pagesCitation: CDJ 1991 SC 262 Court: Case No: JudgesNomosvistasNo ratings yet

- Tolia AppealDocument7 pagesTolia Appealmau8684No ratings yet

- Deputy Director of Income TaxE I2 Vs The American IU2018111218165039195COM490153Document9 pagesDeputy Director of Income TaxE I2 Vs The American IU2018111218165039195COM490153Yashaswi KumarNo ratings yet

- Internal Circular (Restricted Circular For Office Use Only)Document16 pagesInternal Circular (Restricted Circular For Office Use Only)Manish K JadhavNo ratings yet

- Cta 2D CV 07000 D 2008jan09 RefDocument14 pagesCta 2D CV 07000 D 2008jan09 RefSharon AgapuyanNo ratings yet

- Cta 2D CV 06710 D 2006jul31 Ass PDFDocument19 pagesCta 2D CV 06710 D 2006jul31 Ass PDFFlois SevillaNo ratings yet

- Penalty U/s 271 (1) (C) Case Reference Shree Nirmal Commercial Ltd. v. CitDocument39 pagesPenalty U/s 271 (1) (C) Case Reference Shree Nirmal Commercial Ltd. v. CitCAclubindiaNo ratings yet

- Dell International Services India PVT LTD Vs The IIL2022040522170528204COM311728Document30 pagesDell International Services India PVT LTD Vs The IIL2022040522170528204COM311728Rıtesha DasNo ratings yet

- 226 CIR v. Sony Philippines, IncDocument4 pages226 CIR v. Sony Philippines, IncclarkorjaloNo ratings yet

- CIR v. Next Mobile IncDocument9 pagesCIR v. Next Mobile IncMeg ReyesNo ratings yet

- 2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsDocument11 pages2023 150 Taxmann Com 227 Rajasthan 30 10 2018 Principal Commissioner of Income Tax VsAbhishek JainNo ratings yet

- CBK V CIRDocument7 pagesCBK V CIRAna BelleNo ratings yet

- Cir VS StiDocument6 pagesCir VS StiNaomiJean InotNo ratings yet

- Itat Nos 212Document8 pagesItat Nos 212Atul GoelNo ratings yet

- Incometax 29 09 2022Document3 pagesIncometax 29 09 2022nitishbhaskaran4No ratings yet

- Chapter 118Document26 pagesChapter 118Nitin SrivastavaNo ratings yet

- Pbcom vs. Cir 302 Scra 241Document11 pagesPbcom vs. Cir 302 Scra 241Clarinda MerleNo ratings yet

- Modern Imaging Solutions Case Tax FRDocument18 pagesModern Imaging Solutions Case Tax FRLykel LavillaNo ratings yet

- SM Land, Inc., Et Al. v. City of Manila, Et Al., G.R. No. 197151, October 22,2012Document13 pagesSM Land, Inc., Et Al. v. City of Manila, Et Al., G.R. No. 197151, October 22,2012d-fbuser-49417072No ratings yet

- R.kasi Vishwanathan & Bros. V Assist CIt (2014) 42 Taxmann - Com 176 Section 139 (5) - It 475-11 28.3.2016Document7 pagesR.kasi Vishwanathan & Bros. V Assist CIt (2014) 42 Taxmann - Com 176 Section 139 (5) - It 475-11 28.3.2016Prabhash ChandNo ratings yet

- आयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Document8 pagesआयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Saksham ShrivastavNo ratings yet

- CIR vs. Petron, G. R. No. 185568 (2012)Document14 pagesCIR vs. Petron, G. R. No. 185568 (2012)Aaron James PuasoNo ratings yet

- CIR vs. Transitions Optical, Inc., GR No. 227544, 22 November 2017Document14 pagesCIR vs. Transitions Optical, Inc., GR No. 227544, 22 November 2017Christopher ArellanoNo ratings yet

- 2022LHC4885Document8 pages2022LHC4885Shah Meer GichkiNo ratings yet

- 22 Team - Energy - Corp. - v. - Commissioner - of - Internal20210505-11-1jxu1oaDocument28 pages22 Team - Energy - Corp. - v. - Commissioner - of - Internal20210505-11-1jxu1oaKempetsNo ratings yet

- Rajesh Kumar Sharma - Submission Before ITAT - Penalty - 201617Document6 pagesRajesh Kumar Sharma - Submission Before ITAT - Penalty - 201617sssadangiNo ratings yet

- CIR v. Standard Chartered BankDocument11 pagesCIR v. Standard Chartered Bankf919No ratings yet

- CIR Vs ST. LukesDocument9 pagesCIR Vs ST. Lukesdolce gustoNo ratings yet

- PRADIPDocument7 pagesPRADIPGovindNo ratings yet

- 3 - CIR v. PetronDocument7 pages3 - CIR v. PetronJaysieMicabaloNo ratings yet

- CIR v. TRANSFIELD PHILIPPINESDocument16 pagesCIR v. TRANSFIELD PHILIPPINESFaustina del RosarioNo ratings yet

- 168222-2013-First Lepanto Taisho Insurance Corp. V.Document3 pages168222-2013-First Lepanto Taisho Insurance Corp. V.John Kyle LluzNo ratings yet

- Ford PDFDocument3 pagesFord PDFAbhay DesaiNo ratings yet

- 2002 83 ITD 151 Delhi SB 2002 77 TTJ 387 Delhi SB 01 08 2002highlightedDocument12 pages2002 83 ITD 151 Delhi SB 2002 77 TTJ 387 Delhi SB 01 08 2002highlightedSnigdha MazumdarNo ratings yet

- Rhombus Energy v. CirDocument15 pagesRhombus Energy v. CirSteven TylerNo ratings yet

- Gateway Technolabs P LTDDocument4 pagesGateway Technolabs P LTDDayavanti Nilesh RanaNo ratings yet

- Perfetti Van Melle IndiaDocument18 pagesPerfetti Van Melle IndiaramitkatyalNo ratings yet

- G.R. No. 227544 Commissioner OF Internal REVENUE, Petitioner Transitions Optical Philippines, Inc., Respondent Decision Leonen, J.Document7 pagesG.R. No. 227544 Commissioner OF Internal REVENUE, Petitioner Transitions Optical Philippines, Inc., Respondent Decision Leonen, J.JaysonNo ratings yet

- Kme - Goa Sof - Ay 2023-24 - 06052024Document6 pagesKme - Goa Sof - Ay 2023-24 - 06052024anil.singh3131No ratings yet

- Mindanao Ii Geothermal Partnership VS CirDocument27 pagesMindanao Ii Geothermal Partnership VS CirAnthony Blaine Benels Domingo-MpaNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- S 0232 01Document50 pagesS 0232 01Shahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument7 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Slip 0232 01 2019Document513 pagesSlip 0232 01 2019Shahaan ZulfiqarNo ratings yet

- NO Marriage CertificateDocument5 pagesNO Marriage CertificateShahaan ZulfiqarNo ratings yet

- Para NO Cases Under Process Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and VerifiedDocument6 pagesPara NO Cases Under Process Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument7 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument5 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument6 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument6 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- Para No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedDocument6 pagesPara No Amount Pointed Out by Audit Amount Charged But Not Recovered Amount Recovered and Verified Amount Recovered But Un-VerifiedShahaan ZulfiqarNo ratings yet

- 114 CasesDocument29 pages114 CasesShahaan ZulfiqarNo ratings yet

- Drra 12Document966 pagesDrra 12Shahaan ZulfiqarNo ratings yet

- 2011-12 - Dac 14.01.2020Document38 pages2011-12 - Dac 14.01.2020Shahaan ZulfiqarNo ratings yet

- 2017-18 - 17.08.2020 Multan Audit ReportDocument25 pages2017-18 - 17.08.2020 Multan Audit ReportShahaan ZulfiqarNo ratings yet

- 2013-14 - Multan 25112019Document47 pages2013-14 - Multan 25112019Shahaan ZulfiqarNo ratings yet