Download as pdf or txt

You might also like

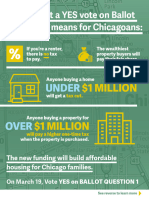

- BCHI24023 Explainer Infographic FINAL FPODocument2 pagesBCHI24023 Explainer Infographic FINAL FPORobert GarciaNo ratings yet

- Save-History Activity-Book FINAL Web SMDocument32 pagesSave-History Activity-Book FINAL Web SMHere & NowNo ratings yet

- Industrial Relations and Labour LawsDocument166 pagesIndustrial Relations and Labour Lawsvprakash797258% (31)

- Case Write Up 1Document4 pagesCase Write Up 1E learningNo ratings yet

- Nar / National Association of Realtors Code of Ethics - Pledge of PerformanceDocument1 pageNar / National Association of Realtors Code of Ethics - Pledge of PerformanceBruce W. McKinnon MBANo ratings yet

- Erik Prince of Blackwater - Redacted.Document86 pagesErik Prince of Blackwater - Redacted.lifeinthemixNo ratings yet

- Water Privatization in HaitiDocument8 pagesWater Privatization in HaitiAnil DonkersNo ratings yet

- Preservation & People (PM Newsletter), Spring 2002Document12 pagesPreservation & People (PM Newsletter), Spring 2002Preservation MassachusettsNo ratings yet

- KRCR-Newsroom@Sbgtv - Com 20180413 090432Document8 pagesKRCR-Newsroom@Sbgtv - Com 20180413 090432JoshNo ratings yet

- Almanacs 44454Document154 pagesAlmanacs 44454gorgeriderNo ratings yet

- Offender Orientation Handbook EnglishDocument146 pagesOffender Orientation Handbook EnglishbunnyhopNo ratings yet

- Ietan Story: Tribal Lobbyist FirmDocument8 pagesIetan Story: Tribal Lobbyist FirmOriginal PechangaNo ratings yet

- American Coin: A True Story of Betrayal, Gambling, and Murder in Las VegasFrom EverandAmerican Coin: A True Story of Betrayal, Gambling, and Murder in Las VegasNo ratings yet

- NFHA: Zip Code InequalityDocument84 pagesNFHA: Zip Code InequalitykgoradioNo ratings yet

- Albert Pike KKK AffililiationDocument13 pagesAlbert Pike KKK AffililiationMiguelNo ratings yet

- Fifteenth Congress of The Federation of OSEA Seventh MeetDocument5 pagesFifteenth Congress of The Federation of OSEA Seventh MeetKaylee SteinNo ratings yet

- Group List of Extra Scrutiny Targets by IRSDocument10 pagesGroup List of Extra Scrutiny Targets by IRSAnonymous kprzCiZNo ratings yet

- Principles of CopyrightsDocument81 pagesPrinciples of CopyrightskocherlakotapavanNo ratings yet

- Operation Uphold DemocracyDocument10 pagesOperation Uphold DemocracyguillemgnNo ratings yet

- Walton Development, Tanzania Jesuits & Grupo AlcoDocument10 pagesWalton Development, Tanzania Jesuits & Grupo AlcoDavid LangerNo ratings yet

- Senate Hearing, 107TH Congress - Native American Sacred PlacesDocument414 pagesSenate Hearing, 107TH Congress - Native American Sacred PlacesScribd Government DocsNo ratings yet

- Bell V Pappas DismissDocument25 pagesBell V Pappas DismissRobert GarciaNo ratings yet

- Real New Zealand HistoryDocument335 pagesReal New Zealand Historykitty katNo ratings yet

- Displace Resettle Rehabilitation Reparation Dev Final 13 MainDocument86 pagesDisplace Resettle Rehabilitation Reparation Dev Final 13 MainTran HamyNo ratings yet

- Plaintiff's Opposition On Preservation of Talc SamplesDocument26 pagesPlaintiff's Opposition On Preservation of Talc SamplesKirk HartleyNo ratings yet

- Texas Economic Development Handbook 2015Document259 pagesTexas Economic Development Handbook 2015deanacmooreNo ratings yet

- TX Citizen 7.23.15Document16 pagesTX Citizen 7.23.15TxcitizenNo ratings yet

- ThePurpleLotus - Wattigney InformationDocument6 pagesThePurpleLotus - Wattigney InformationDeepDotWeb.comNo ratings yet

- COVID Cannabis Banking TextDocument28 pagesCOVID Cannabis Banking TextMarijuana MomentNo ratings yet

- NYPIRG Report: Albany's Pay To Play CultureDocument33 pagesNYPIRG Report: Albany's Pay To Play Culturemichelle_breidenbachNo ratings yet

- 158th Field Artillery Official Extract No. 87Document10 pages158th Field Artillery Official Extract No. 87John JensonNo ratings yet

- Gentrification and Its Effects On Minority Communities - A Comparative Case Study of Four Global Cities: San Diego, San Francisco, Cape Town, and ViennaDocument24 pagesGentrification and Its Effects On Minority Communities - A Comparative Case Study of Four Global Cities: San Diego, San Francisco, Cape Town, and ViennaPremier PublishersNo ratings yet

- 2016 - Financial Disclosure Statement (Amended - 6/7/2017)Document10 pages2016 - Financial Disclosure Statement (Amended - 6/7/2017)juliabhaberNo ratings yet

- Let The Bloody Truth Be ToldDocument29 pagesLet The Bloody Truth Be Toldsualk14No ratings yet

- Ordaining LawsuitDocument20 pagesOrdaining LawsuitNewsChannel 9 StaffNo ratings yet

- Rolling Stone Lawsuit DismissalDocument23 pagesRolling Stone Lawsuit DismissalmashablescribdNo ratings yet

- Report On Affordable Housing in VirginiaDocument159 pagesReport On Affordable Housing in VirginiaDavid Cross100% (1)

- Email DocsDocument5 pagesEmail DocsTim BrownNo ratings yet

- Homeless Solutions Proposed StrategyDocument34 pagesHomeless Solutions Proposed StrategyRobert WilonskyNo ratings yet

- Kenard and Chelsea Burley vs. Horry County Police Dept. Lawsuit Document #1Document6 pagesKenard and Chelsea Burley vs. Horry County Police Dept. Lawsuit Document #1ABC15 NewsNo ratings yet

- Luna Firebaugh - The Border Crossed UsDocument24 pagesLuna Firebaugh - The Border Crossed UsMario OrospeNo ratings yet

- The Examination of TitubaDocument6 pagesThe Examination of Titubaapi-250242524No ratings yet

- 2020.05.19 DFEH Original Complaint (ABC) FINALDocument23 pages2020.05.19 DFEH Original Complaint (ABC) FINALeriq_gardner6833100% (2)

- Texas HousingDocument75 pagesTexas HousingsbondiolihpNo ratings yet

- Chicago Justice Project LawsuitDocument53 pagesChicago Justice Project LawsuitJohn DodgeNo ratings yet

- Corruption in Cook County - Anti-Corruption Report #3 - 2-18-2010Document33 pagesCorruption in Cook County - Anti-Corruption Report #3 - 2-18-2010Dorf Gould100% (1)

- DTES Vision For The 100 Block Final 1Document48 pagesDTES Vision For The 100 Block Final 1CTV Vancouver100% (1)

- Journal California Legal History Journal Housing in California Radkowski-PaperDocument66 pagesJournal California Legal History Journal Housing in California Radkowski-Paperjacque zidaneNo ratings yet

- 1977, 04-00 Sex Bias in The US CodeDocument239 pages1977, 04-00 Sex Bias in The US CodeRoland SladeNo ratings yet

- Redfin Filed Complaint PDFDocument76 pagesRedfin Filed Complaint PDFGeekWireNo ratings yet

- Antislavery Politics in Antebellum and Civil War America PDFDocument299 pagesAntislavery Politics in Antebellum and Civil War America PDFJorge ANo ratings yet

- Trakas LetterDocument3 pagesTrakas LetterMonica Celeste RyanNo ratings yet

- Election Grants LawsuitDocument46 pagesElection Grants LawsuitSarah LehrNo ratings yet

- Iron County Historical Society Newsletter - Spring 2014Document10 pagesIron County Historical Society Newsletter - Spring 2014IronCountyHistoricalNo ratings yet

- Revised Idaho Marijuana Legalization Ballot MeasureDocument23 pagesRevised Idaho Marijuana Legalization Ballot MeasureMarijuana MomentNo ratings yet

- City Limits Magazine, October 1988 IssueDocument24 pagesCity Limits Magazine, October 1988 IssueCity Limits (New York)No ratings yet

- The Greek MachineDocument13 pagesThe Greek Machineapi-466368071No ratings yet

- Dry Bulk ShippingDocument3 pagesDry Bulk ShippingTammam HassanNo ratings yet

- Pakistan Economy EssayDocument15 pagesPakistan Economy EssayAhmad SafiNo ratings yet

- 179848-Article Text-459072-1-10-20181119Document9 pages179848-Article Text-459072-1-10-20181119Oyebola Akin-DeluNo ratings yet

- CH 02Document36 pagesCH 02api-3804982100% (1)

- Management Information System at THE CITY BANK LIMITED BangladeshDocument17 pagesManagement Information System at THE CITY BANK LIMITED BangladeshSimmons Ozil67% (3)

- Foreign Exchange Market: Presentation OnDocument19 pagesForeign Exchange Market: Presentation OnKavya lakshmikanthNo ratings yet

- Impacts That Matter - Product Sustainability Overview - 54959 - PDFDocument4 pagesImpacts That Matter - Product Sustainability Overview - 54959 - PDFOptima StoreNo ratings yet

- Scheme of Examination Guru Gobind Singh Indraprastha University, Delhi Bachelor of Commerce (Hons.) Criteria For Internal AssessmentDocument43 pagesScheme of Examination Guru Gobind Singh Indraprastha University, Delhi Bachelor of Commerce (Hons.) Criteria For Internal AssessmentSarthak GoelNo ratings yet

- Project Justification: Increase OEEDocument21 pagesProject Justification: Increase OEEKaran Singh RaiNo ratings yet

- #1 - Inventory Turnover Ratio: One Accounting Period Cost of Goods SoldDocument5 pages#1 - Inventory Turnover Ratio: One Accounting Period Cost of Goods SoldMarie Frances SaysonNo ratings yet

- Agricultural and Rural Sociology Quiz 13 Des 2021 - Shafiyyah Ramadhani Arafa - 205040100111013Document5 pagesAgricultural and Rural Sociology Quiz 13 Des 2021 - Shafiyyah Ramadhani Arafa - 205040100111013Shafiyyah Ramadhani ArafaNo ratings yet

- EssayDocument10 pagesEssaySonu KumarNo ratings yet

- Course Title: Entrepreneurship and Enterprise DevelopmentDocument2 pagesCourse Title: Entrepreneurship and Enterprise DevelopmentDemeke GedamuNo ratings yet

- 205 Finance Market & Banking OperationsDocument10 pages205 Finance Market & Banking Operationsxonline022No ratings yet

- Answer To The Question No: 4.17: Summary InputDocument1 pageAnswer To The Question No: 4.17: Summary Inputtjarnob13No ratings yet

- Manager Project Financial Advertising in Chicago IL Resume Deborah KozieDocument2 pagesManager Project Financial Advertising in Chicago IL Resume Deborah KozieDeborah KozieNo ratings yet

- OD328840748510716100Document1 pageOD328840748510716100AkashNo ratings yet

- RDocument671 pagesRlinhtruong.31221024012No ratings yet

- A Ratio Analysis Report On FINALDocument34 pagesA Ratio Analysis Report On FINALArsal AliNo ratings yet

- Marketing NotesDocument4 pagesMarketing NotesChristineNo ratings yet

- Credit RatingDocument2 pagesCredit RatingSumesh MirashiNo ratings yet

- Annexure 1Document4 pagesAnnexure 1Jalaj JainNo ratings yet

- Mock Cpa Board Exams - Rfjpia r-12 - W.ansDocument17 pagesMock Cpa Board Exams - Rfjpia r-12 - W.anssamson jobNo ratings yet

- After Sales Services of Selected Car Insurance Companies - Chapter 1 5 - RevisedDocument68 pagesAfter Sales Services of Selected Car Insurance Companies - Chapter 1 5 - RevisedMariel AdventoNo ratings yet

- Woori Bank 2011 Annual ReportDocument210 pagesWoori Bank 2011 Annual ReportManpreet Singh RekhiNo ratings yet

- 'Acquaint With Economics' by Dr. Asad Ahmad - 0Document46 pages'Acquaint With Economics' by Dr. Asad Ahmad - 0Prakash ThulasidasNo ratings yet

- 9 Steps To Overcome Competition in Retail BusinessDocument3 pages9 Steps To Overcome Competition in Retail BusinessMarina IvanNo ratings yet

- Sales AgentsDocument3 pagesSales AgentsDavidCruzNo ratings yet