Tetra Pak

Tetra Pak

You might also like

- Short Term Financial Management 3rd Edition Maness Test BankDocument5 pagesShort Term Financial Management 3rd Edition Maness Test Bankjuanlucerofdqegwntai100% (17)

- Beverage Technology PDFDocument168 pagesBeverage Technology PDFAniket100% (1)

- Project Report On Tetra Pak Manufacturing PlantDocument10 pagesProject Report On Tetra Pak Manufacturing PlantEIRI Board of Consultants and PublishersNo ratings yet

- Project Report On Fruit Juice and SmoothiesDocument9 pagesProject Report On Fruit Juice and SmoothiesEIRI Board of Consultants and PublishersNo ratings yet

- Chapter 1 Review of The Accounting CycleDocument13 pagesChapter 1 Review of The Accounting CycleLouriel MartinezNo ratings yet

- 2 - Tetra Pak Case HistoryDocument7 pages2 - Tetra Pak Case HistoryFabio ParisiNo ratings yet

- Tetra Pak Dairy Index Issue6 2013 PDFDocument22 pagesTetra Pak Dairy Index Issue6 2013 PDFSarah HernandezNo ratings yet

- Packaging For Beverages: Beverage Technology Soegijapranata Catholic UniversityDocument15 pagesPackaging For Beverages: Beverage Technology Soegijapranata Catholic UniversityMaura Yosefina MartanNo ratings yet

- Tetra Pak PresentationDocument14 pagesTetra Pak Presentationmterry04100% (4)

- FINALOLADocument18 pagesFINALOLABhavik LalaNo ratings yet

- Chapter 5-Statement of Cash Flows and Articulation: Multiple ChoiceDocument39 pagesChapter 5-Statement of Cash Flows and Articulation: Multiple ChoiceLeonardoNo ratings yet

- Gist of Important Judgments Relating To TDSDocument41 pagesGist of Important Judgments Relating To TDSAbishek SekarNo ratings yet

- SMEDA Fruit Juice ProcessingDocument41 pagesSMEDA Fruit Juice ProcessingImran Qasim Jora100% (1)

- Project Report On Fruit Juice of Mango, Orange, Sweet Lime, Lime, Pineapple Plant (1200 Ltr. Per Hour Capacity) in Tin CansDocument8 pagesProject Report On Fruit Juice of Mango, Orange, Sweet Lime, Lime, Pineapple Plant (1200 Ltr. Per Hour Capacity) in Tin CansEIRI Board of Consultants and Publishers100% (1)

- Packaging of BeveragesDocument10 pagesPackaging of BeveragesDarshan VartakNo ratings yet

- Rus SipDocument21 pagesRus SipkoolyarNo ratings yet

- Understanding Ambient Yoghurt: - Challenges and OpportunitiesDocument11 pagesUnderstanding Ambient Yoghurt: - Challenges and Opportunitieshuong2286No ratings yet

- Coconut Water: Global Trends, Sciences, Processing and Packaging TechnologyDocument34 pagesCoconut Water: Global Trends, Sciences, Processing and Packaging TechnologyĐivềphía Mặt Trời100% (1)

- Vitamin C Retention - White Paper RevisionDocument12 pagesVitamin C Retention - White Paper RevisionLeonardo SouzaNo ratings yet

- TA General1Document78 pagesTA General1Xuân Hòa NguyễnNo ratings yet

- Chilled Drinking Yoghurt: Complete Integrated LineDocument15 pagesChilled Drinking Yoghurt: Complete Integrated LineANDREW ONUNAKU100% (3)

- Tetra Pak Pernod RichardDocument56 pagesTetra Pak Pernod RichardDeepak ChoudharyNo ratings yet

- How To Control Stability in Plant Based BeveragesDocument3 pagesHow To Control Stability in Plant Based BeveragesHenk Meima100% (1)

- Mixed Fruit Jam Jelly Pickle MakingDocument6 pagesMixed Fruit Jam Jelly Pickle MakingKirtiKumar KasatNo ratings yet

- D3-4 Tea Extractors - June 2013Document24 pagesD3-4 Tea Extractors - June 2013Angga SukmaNo ratings yet

- Beverage Cip PerformanceDocument12 pagesBeverage Cip PerformancesambhavjoshiNo ratings yet

- 60TPH Tomato Paste Processing 2Document19 pages60TPH Tomato Paste Processing 2Nick Kim67% (3)

- S01E01-Lars-Goran-Jenny Tetra Pak Best Practice PDFDocument10 pagesS01E01-Lars-Goran-Jenny Tetra Pak Best Practice PDFKhemiri WajdiNo ratings yet

- Effective Management of Critical Contro PDFDocument5 pagesEffective Management of Critical Contro PDFĐivềphía Mặt TrờiNo ratings yet

- Tetra PakDocument25 pagesTetra PakArslan Aftab50% (2)

- Inplant Training Report-Coke2009Document80 pagesInplant Training Report-Coke2009patkiprashantNo ratings yet

- Beer ManufacturingDocument23 pagesBeer ManufacturingDivya AggarwalNo ratings yet

- 2020.01.21 Volka Foods - ShamsaDocument44 pages2020.01.21 Volka Foods - ShamsaShamsa kanwalNo ratings yet

- Tomato Paste and Fruit PulpDocument26 pagesTomato Paste and Fruit Pulppradip_kumarNo ratings yet

- Tetra Pak Long Life Milk Campaign - FinalDocument2 pagesTetra Pak Long Life Milk Campaign - FinalTayyab RazaNo ratings yet

- Final ProjectDocument52 pagesFinal ProjectIraj SohailNo ratings yet

- Tpps Cip HandbookDocument83 pagesTpps Cip HandbookJosé Eduardo VazNo ratings yet

- Uht PlantDocument49 pagesUht PlantAnjani Kumar Nagoriya100% (1)

- Milk PasteurizationDocument13 pagesMilk PasteurizationSofian NurjamalNo ratings yet

- Tba 19 MachineDocument12 pagesTba 19 Machinepab_guru33% (3)

- Bolstridge 2012Document37 pagesBolstridge 2012norodriguezv100% (1)

- 1 - 2. UHT Technology and PortfolioDocument14 pages1 - 2. UHT Technology and PortfolioNvt SsoNo ratings yet

- Confectionery Industry: Submitted By: M. Waqas Mahomood Roll No. 3236Document15 pagesConfectionery Industry: Submitted By: M. Waqas Mahomood Roll No. 3236Muhammad Sohail AkramNo ratings yet

- Tetra Therm Aseptic Visco SSHEDocument4 pagesTetra Therm Aseptic Visco SSHEsudheendracvkNo ratings yet

- Tomato Paste Processing Line CatalogueDocument23 pagesTomato Paste Processing Line CatalogueDan ManNo ratings yet

- Process Control Ing in Biscuits ManufacturingDocument6 pagesProcess Control Ing in Biscuits ManufacturingUdara Achintya BandaraNo ratings yet

- Dairy Aseptic SystemsDocument231 pagesDairy Aseptic SystemsVineet MakkerNo ratings yet

- FDST318Document149 pagesFDST318Karthikeyan Balakrishnan100% (1)

- Coconut Water Presentation For APCC-DOA Training Tetra Pak SingaporeDocument34 pagesCoconut Water Presentation For APCC-DOA Training Tetra Pak Singaporenerkysdone100% (1)

- Innovative: Åkerlund & Rausing Tetrahedron PackageDocument6 pagesInnovative: Åkerlund & Rausing Tetrahedron Packageravijangde10No ratings yet

- Tetra-Pak-7000-Litres-Aseptic-Tank-Vd-Buffering-Processing-Equipment 2Document2 pagesTetra-Pak-7000-Litres-Aseptic-Tank-Vd-Buffering-Processing-Equipment 2Frank valdezNo ratings yet

- Internship Report: Sumbitted ToDocument49 pagesInternship Report: Sumbitted ToSunil RAYALASEEMA GRAPHICSNo ratings yet

- Bajaj Processpack Limited Juice Packaging Machines & Juice Packaging EquipmentsDocument20 pagesBajaj Processpack Limited Juice Packaging Machines & Juice Packaging EquipmentsBajaj Process PackNo ratings yet

- Aseptic Packaging SystemsDocument10 pagesAseptic Packaging SystemsderdorNo ratings yet

- PET PreformsDocument7 pagesPET Preformsshahidul0No ratings yet

- UHT Theory LTHDocument36 pagesUHT Theory LTHthanhtl_hugolata100% (4)

- FAO Agbiz Handbook Milk Dairy ProductsDocument49 pagesFAO Agbiz Handbook Milk Dairy ProductsOsman Aita100% (1)

- TETRA PAK PackagingDocument25 pagesTETRA PAK PackagingVandana Bhat100% (2)

- Facts About Tetra Pak CartonsDocument3 pagesFacts About Tetra Pak CartonsrunningpinoyNo ratings yet

- General Characteristics of Pectin. SolubilityDocument2 pagesGeneral Characteristics of Pectin. SolubilityAnonymous VIwig8iwNo ratings yet

- Tetra PakDocument20 pagesTetra PakAvi Sharma50% (2)

- Marketing Assignment: Ganna-RassDocument20 pagesMarketing Assignment: Ganna-Rassakshta agarwalNo ratings yet

- FinalDocument49 pagesFinalsachin100% (3)

- SecuritizationDocument5 pagesSecuritizationAnand Mishra100% (1)

- Tax Law Summary NotesDocument35 pagesTax Law Summary Noteskhushboo100% (1)

- Break Even AnalysisDocument2 pagesBreak Even AnalysisVille4everNo ratings yet

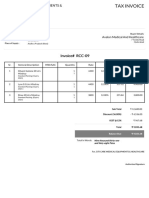

- Invoice# Invoice# RCC-09 RCC-09: Avalon Medical and HealthcareDocument1 pageInvoice# Invoice# RCC-09 RCC-09: Avalon Medical and HealthcareNaveed AbrarNo ratings yet

- Module 2 MoneyDocument78 pagesModule 2 Moneylord kwantoniumNo ratings yet

- $750,000 Sanctions Against Wells Fargo, Attorney June 2008lb - Nosek-Decision Massive Sanctions Download This Document For FreePrintMobileDocument18 pages$750,000 Sanctions Against Wells Fargo, Attorney June 2008lb - Nosek-Decision Massive Sanctions Download This Document For FreePrintMobile83jjmackNo ratings yet

- Quiz Week 2 SolnsDocument5 pagesQuiz Week 2 SolnsRiri FahraniNo ratings yet

- BDD Redevelopment - EnggDocument13 pagesBDD Redevelopment - Enggbalaeee123No ratings yet

- Chartered ClubDocument3 pagesChartered ClubkajshdiNo ratings yet

- Accounting Theory Project 1 - MayaDocument18 pagesAccounting Theory Project 1 - MayaDima AbdulhayNo ratings yet

- A Study On Financial Performance of Oil and Natural Gas Corporation ( (1) - OriginalDocument105 pagesA Study On Financial Performance of Oil and Natural Gas Corporation ( (1) - OriginalGupta AbhishekNo ratings yet

- Micro Lecture 4Document20 pagesMicro Lecture 4Sarvar SheikhNo ratings yet

- Financial Services: Topic: Tax Aspects of LeasingDocument10 pagesFinancial Services: Topic: Tax Aspects of LeasingSri NilayaNo ratings yet

- Afar Hedging Ja With AnswersDocument3 pagesAfar Hedging Ja With AnswersShigure KousakaNo ratings yet

- Ais Final QuizDocument5 pagesAis Final QuizClaudette ClementeNo ratings yet

- ASB3210 Exam 2020 With SolutionsDocument19 pagesASB3210 Exam 2020 With SolutionsSubmission PortalNo ratings yet

- Judicial Affidavit Collection of Sum of MoneyDocument4 pagesJudicial Affidavit Collection of Sum of Moneypatricia.aniya100% (2)

- Case Study: Renew Power: Group 4Document12 pagesCase Study: Renew Power: Group 4Nandish GuptaNo ratings yet

- DebenturesDocument28 pagesDebenturesdeepaksinghalNo ratings yet

- Annual Report Including With Notice of 30Th Annual General Meeting (AGM/EGM)Document240 pagesAnnual Report Including With Notice of 30Th Annual General Meeting (AGM/EGM)Shyam SunderNo ratings yet

- 69 - Radiowealth Finance Company v. Del Rosario (138739)Document5 pages69 - Radiowealth Finance Company v. Del Rosario (138739)Jessie Marie dela PeñaNo ratings yet

- FDI Project ReportDocument44 pagesFDI Project ReportPriyahemaniNo ratings yet

- Modification or Discharge of Debt in A Chapter 9 CaseDocument13 pagesModification or Discharge of Debt in A Chapter 9 CaseSnowdenKonanNo ratings yet

- VP Financial Planning Analysis in USA Resume John EffreinDocument2 pagesVP Financial Planning Analysis in USA Resume John EffreinJohnEffrein2No ratings yet

- SSC CGL Memory Based Test (2nd Dec 2022 Shift 1) (English)Document24 pagesSSC CGL Memory Based Test (2nd Dec 2022 Shift 1) (English)Siddhant JaybhayeNo ratings yet

Download as pdf or txt

You might also like

- Short Term Financial Management 3rd Edition Maness Test BankDocument5 pagesShort Term Financial Management 3rd Edition Maness Test Bankjuanlucerofdqegwntai100% (17)

- Beverage Technology PDFDocument168 pagesBeverage Technology PDFAniket100% (1)

- Project Report On Tetra Pak Manufacturing PlantDocument10 pagesProject Report On Tetra Pak Manufacturing PlantEIRI Board of Consultants and PublishersNo ratings yet

- Project Report On Fruit Juice and SmoothiesDocument9 pagesProject Report On Fruit Juice and SmoothiesEIRI Board of Consultants and PublishersNo ratings yet

- Chapter 1 Review of The Accounting CycleDocument13 pagesChapter 1 Review of The Accounting CycleLouriel MartinezNo ratings yet

- 2 - Tetra Pak Case HistoryDocument7 pages2 - Tetra Pak Case HistoryFabio ParisiNo ratings yet

- Tetra Pak Dairy Index Issue6 2013 PDFDocument22 pagesTetra Pak Dairy Index Issue6 2013 PDFSarah HernandezNo ratings yet

- Packaging For Beverages: Beverage Technology Soegijapranata Catholic UniversityDocument15 pagesPackaging For Beverages: Beverage Technology Soegijapranata Catholic UniversityMaura Yosefina MartanNo ratings yet

- Tetra Pak PresentationDocument14 pagesTetra Pak Presentationmterry04100% (4)

- FINALOLADocument18 pagesFINALOLABhavik LalaNo ratings yet

- Chapter 5-Statement of Cash Flows and Articulation: Multiple ChoiceDocument39 pagesChapter 5-Statement of Cash Flows and Articulation: Multiple ChoiceLeonardoNo ratings yet

- Gist of Important Judgments Relating To TDSDocument41 pagesGist of Important Judgments Relating To TDSAbishek SekarNo ratings yet

- SMEDA Fruit Juice ProcessingDocument41 pagesSMEDA Fruit Juice ProcessingImran Qasim Jora100% (1)

- Project Report On Fruit Juice of Mango, Orange, Sweet Lime, Lime, Pineapple Plant (1200 Ltr. Per Hour Capacity) in Tin CansDocument8 pagesProject Report On Fruit Juice of Mango, Orange, Sweet Lime, Lime, Pineapple Plant (1200 Ltr. Per Hour Capacity) in Tin CansEIRI Board of Consultants and Publishers100% (1)

- Packaging of BeveragesDocument10 pagesPackaging of BeveragesDarshan VartakNo ratings yet

- Rus SipDocument21 pagesRus SipkoolyarNo ratings yet

- Understanding Ambient Yoghurt: - Challenges and OpportunitiesDocument11 pagesUnderstanding Ambient Yoghurt: - Challenges and Opportunitieshuong2286No ratings yet

- Coconut Water: Global Trends, Sciences, Processing and Packaging TechnologyDocument34 pagesCoconut Water: Global Trends, Sciences, Processing and Packaging TechnologyĐivềphía Mặt Trời100% (1)

- Vitamin C Retention - White Paper RevisionDocument12 pagesVitamin C Retention - White Paper RevisionLeonardo SouzaNo ratings yet

- TA General1Document78 pagesTA General1Xuân Hòa NguyễnNo ratings yet

- Chilled Drinking Yoghurt: Complete Integrated LineDocument15 pagesChilled Drinking Yoghurt: Complete Integrated LineANDREW ONUNAKU100% (3)

- Tetra Pak Pernod RichardDocument56 pagesTetra Pak Pernod RichardDeepak ChoudharyNo ratings yet

- How To Control Stability in Plant Based BeveragesDocument3 pagesHow To Control Stability in Plant Based BeveragesHenk Meima100% (1)

- Mixed Fruit Jam Jelly Pickle MakingDocument6 pagesMixed Fruit Jam Jelly Pickle MakingKirtiKumar KasatNo ratings yet

- D3-4 Tea Extractors - June 2013Document24 pagesD3-4 Tea Extractors - June 2013Angga SukmaNo ratings yet

- Beverage Cip PerformanceDocument12 pagesBeverage Cip PerformancesambhavjoshiNo ratings yet

- 60TPH Tomato Paste Processing 2Document19 pages60TPH Tomato Paste Processing 2Nick Kim67% (3)

- S01E01-Lars-Goran-Jenny Tetra Pak Best Practice PDFDocument10 pagesS01E01-Lars-Goran-Jenny Tetra Pak Best Practice PDFKhemiri WajdiNo ratings yet

- Effective Management of Critical Contro PDFDocument5 pagesEffective Management of Critical Contro PDFĐivềphía Mặt TrờiNo ratings yet

- Tetra PakDocument25 pagesTetra PakArslan Aftab50% (2)

- Inplant Training Report-Coke2009Document80 pagesInplant Training Report-Coke2009patkiprashantNo ratings yet

- Beer ManufacturingDocument23 pagesBeer ManufacturingDivya AggarwalNo ratings yet

- 2020.01.21 Volka Foods - ShamsaDocument44 pages2020.01.21 Volka Foods - ShamsaShamsa kanwalNo ratings yet

- Tomato Paste and Fruit PulpDocument26 pagesTomato Paste and Fruit Pulppradip_kumarNo ratings yet

- Tetra Pak Long Life Milk Campaign - FinalDocument2 pagesTetra Pak Long Life Milk Campaign - FinalTayyab RazaNo ratings yet

- Final ProjectDocument52 pagesFinal ProjectIraj SohailNo ratings yet

- Tpps Cip HandbookDocument83 pagesTpps Cip HandbookJosé Eduardo VazNo ratings yet

- Uht PlantDocument49 pagesUht PlantAnjani Kumar Nagoriya100% (1)

- Milk PasteurizationDocument13 pagesMilk PasteurizationSofian NurjamalNo ratings yet

- Tba 19 MachineDocument12 pagesTba 19 Machinepab_guru33% (3)

- Bolstridge 2012Document37 pagesBolstridge 2012norodriguezv100% (1)

- 1 - 2. UHT Technology and PortfolioDocument14 pages1 - 2. UHT Technology and PortfolioNvt SsoNo ratings yet

- Confectionery Industry: Submitted By: M. Waqas Mahomood Roll No. 3236Document15 pagesConfectionery Industry: Submitted By: M. Waqas Mahomood Roll No. 3236Muhammad Sohail AkramNo ratings yet

- Tetra Therm Aseptic Visco SSHEDocument4 pagesTetra Therm Aseptic Visco SSHEsudheendracvkNo ratings yet

- Tomato Paste Processing Line CatalogueDocument23 pagesTomato Paste Processing Line CatalogueDan ManNo ratings yet

- Process Control Ing in Biscuits ManufacturingDocument6 pagesProcess Control Ing in Biscuits ManufacturingUdara Achintya BandaraNo ratings yet

- Dairy Aseptic SystemsDocument231 pagesDairy Aseptic SystemsVineet MakkerNo ratings yet

- FDST318Document149 pagesFDST318Karthikeyan Balakrishnan100% (1)

- Coconut Water Presentation For APCC-DOA Training Tetra Pak SingaporeDocument34 pagesCoconut Water Presentation For APCC-DOA Training Tetra Pak Singaporenerkysdone100% (1)

- Innovative: Åkerlund & Rausing Tetrahedron PackageDocument6 pagesInnovative: Åkerlund & Rausing Tetrahedron Packageravijangde10No ratings yet

- Tetra-Pak-7000-Litres-Aseptic-Tank-Vd-Buffering-Processing-Equipment 2Document2 pagesTetra-Pak-7000-Litres-Aseptic-Tank-Vd-Buffering-Processing-Equipment 2Frank valdezNo ratings yet

- Internship Report: Sumbitted ToDocument49 pagesInternship Report: Sumbitted ToSunil RAYALASEEMA GRAPHICSNo ratings yet

- Bajaj Processpack Limited Juice Packaging Machines & Juice Packaging EquipmentsDocument20 pagesBajaj Processpack Limited Juice Packaging Machines & Juice Packaging EquipmentsBajaj Process PackNo ratings yet

- Aseptic Packaging SystemsDocument10 pagesAseptic Packaging SystemsderdorNo ratings yet

- PET PreformsDocument7 pagesPET Preformsshahidul0No ratings yet

- UHT Theory LTHDocument36 pagesUHT Theory LTHthanhtl_hugolata100% (4)

- FAO Agbiz Handbook Milk Dairy ProductsDocument49 pagesFAO Agbiz Handbook Milk Dairy ProductsOsman Aita100% (1)

- TETRA PAK PackagingDocument25 pagesTETRA PAK PackagingVandana Bhat100% (2)

- Facts About Tetra Pak CartonsDocument3 pagesFacts About Tetra Pak CartonsrunningpinoyNo ratings yet

- General Characteristics of Pectin. SolubilityDocument2 pagesGeneral Characteristics of Pectin. SolubilityAnonymous VIwig8iwNo ratings yet

- Tetra PakDocument20 pagesTetra PakAvi Sharma50% (2)

- Marketing Assignment: Ganna-RassDocument20 pagesMarketing Assignment: Ganna-Rassakshta agarwalNo ratings yet

- FinalDocument49 pagesFinalsachin100% (3)

- SecuritizationDocument5 pagesSecuritizationAnand Mishra100% (1)

- Tax Law Summary NotesDocument35 pagesTax Law Summary Noteskhushboo100% (1)

- Break Even AnalysisDocument2 pagesBreak Even AnalysisVille4everNo ratings yet

- Invoice# Invoice# RCC-09 RCC-09: Avalon Medical and HealthcareDocument1 pageInvoice# Invoice# RCC-09 RCC-09: Avalon Medical and HealthcareNaveed AbrarNo ratings yet

- Module 2 MoneyDocument78 pagesModule 2 Moneylord kwantoniumNo ratings yet

- $750,000 Sanctions Against Wells Fargo, Attorney June 2008lb - Nosek-Decision Massive Sanctions Download This Document For FreePrintMobileDocument18 pages$750,000 Sanctions Against Wells Fargo, Attorney June 2008lb - Nosek-Decision Massive Sanctions Download This Document For FreePrintMobile83jjmackNo ratings yet

- Quiz Week 2 SolnsDocument5 pagesQuiz Week 2 SolnsRiri FahraniNo ratings yet

- BDD Redevelopment - EnggDocument13 pagesBDD Redevelopment - Enggbalaeee123No ratings yet

- Chartered ClubDocument3 pagesChartered ClubkajshdiNo ratings yet

- Accounting Theory Project 1 - MayaDocument18 pagesAccounting Theory Project 1 - MayaDima AbdulhayNo ratings yet

- A Study On Financial Performance of Oil and Natural Gas Corporation ( (1) - OriginalDocument105 pagesA Study On Financial Performance of Oil and Natural Gas Corporation ( (1) - OriginalGupta AbhishekNo ratings yet

- Micro Lecture 4Document20 pagesMicro Lecture 4Sarvar SheikhNo ratings yet

- Financial Services: Topic: Tax Aspects of LeasingDocument10 pagesFinancial Services: Topic: Tax Aspects of LeasingSri NilayaNo ratings yet

- Afar Hedging Ja With AnswersDocument3 pagesAfar Hedging Ja With AnswersShigure KousakaNo ratings yet

- Ais Final QuizDocument5 pagesAis Final QuizClaudette ClementeNo ratings yet

- ASB3210 Exam 2020 With SolutionsDocument19 pagesASB3210 Exam 2020 With SolutionsSubmission PortalNo ratings yet

- Judicial Affidavit Collection of Sum of MoneyDocument4 pagesJudicial Affidavit Collection of Sum of Moneypatricia.aniya100% (2)

- Case Study: Renew Power: Group 4Document12 pagesCase Study: Renew Power: Group 4Nandish GuptaNo ratings yet

- DebenturesDocument28 pagesDebenturesdeepaksinghalNo ratings yet

- Annual Report Including With Notice of 30Th Annual General Meeting (AGM/EGM)Document240 pagesAnnual Report Including With Notice of 30Th Annual General Meeting (AGM/EGM)Shyam SunderNo ratings yet

- 69 - Radiowealth Finance Company v. Del Rosario (138739)Document5 pages69 - Radiowealth Finance Company v. Del Rosario (138739)Jessie Marie dela PeñaNo ratings yet

- FDI Project ReportDocument44 pagesFDI Project ReportPriyahemaniNo ratings yet

- Modification or Discharge of Debt in A Chapter 9 CaseDocument13 pagesModification or Discharge of Debt in A Chapter 9 CaseSnowdenKonanNo ratings yet

- VP Financial Planning Analysis in USA Resume John EffreinDocument2 pagesVP Financial Planning Analysis in USA Resume John EffreinJohnEffrein2No ratings yet

- SSC CGL Memory Based Test (2nd Dec 2022 Shift 1) (English)Document24 pagesSSC CGL Memory Based Test (2nd Dec 2022 Shift 1) (English)Siddhant JaybhayeNo ratings yet