Download as pdf or txt

You might also like

- Activewear Case Study (Revised 2020) Shortened VersionDocument8 pagesActivewear Case Study (Revised 2020) Shortened VersionjajccNo ratings yet

- Fisher Wallace Labs - Chronic Pain Treatment InstructionManualDocument12 pagesFisher Wallace Labs - Chronic Pain Treatment InstructionManualRedDirt LoveGoddess100% (2)

- Infineon Technology Day: Door and HVAC Solutions and TrendsDocument37 pagesInfineon Technology Day: Door and HVAC Solutions and Trendsdeepaks4u123No ratings yet

- Cadbury CommiteeDocument5 pagesCadbury CommiteeAnkit Raj100% (2)

- Bluetooth ModuleHC 05 With Raspberry Pi PicoDocument3 pagesBluetooth ModuleHC 05 With Raspberry Pi Picoalexandre magnoNo ratings yet

- Introduction of FX Tiered Margining WLCsDocument3 pagesIntroduction of FX Tiered Margining WLCsnotaNo ratings yet

- Electroencephalography (Eeg) : Atarzyna Linowska Iotr Urka Warsaw University Warszawa, PolandDocument15 pagesElectroencephalography (Eeg) : Atarzyna Linowska Iotr Urka Warsaw University Warszawa, PolandNicholas DiazNo ratings yet

- Mosquito RepellantDocument7 pagesMosquito RepellantKatamba Rogers67% (3)

- Introduction - 2017 - Rhythmic Stimulation Procedures in Neuromodulation PDFDocument6 pagesIntroduction - 2017 - Rhythmic Stimulation Procedures in Neuromodulation PDFGeo MeNo ratings yet

- Freud's Mental Path To Profits PDFDocument4 pagesFreud's Mental Path To Profits PDFcepolNo ratings yet

- Power AmplifierDocument9 pagesPower Amplifiersamsularief03No ratings yet

- Dispersion Staining CardioidDarkfieldCondenser Clarke 12069Document7 pagesDispersion Staining CardioidDarkfieldCondenser Clarke 12069markoosNo ratings yet

- ISE DevelopingFXTradingStrategy 021108 PDFDocument63 pagesISE DevelopingFXTradingStrategy 021108 PDFDondee Sibulo AlejandroNo ratings yet

- RF Detector Using An Arduino PDFDocument3 pagesRF Detector Using An Arduino PDFBenjamin DoverNo ratings yet

- The Discovery of Schumann Resonance: CapacitorsDocument5 pagesThe Discovery of Schumann Resonance: Capacitorssagor sagorNo ratings yet

- Consumer NeuroScienceDocument16 pagesConsumer NeuroScienceBinaNo ratings yet

- Ch9 Dark FieldDocument6 pagesCh9 Dark FieldjozoceNo ratings yet

- The Scoon Machine RevisitedDocument30 pagesThe Scoon Machine Revisitedambertje12No ratings yet

- Understanding Bio ElectricityDocument5 pagesUnderstanding Bio ElectricityIonela100% (2)

- HT - Group Catalogue PDFDocument121 pagesHT - Group Catalogue PDFBhavani SankarNo ratings yet

- How To Design LED Signage and LED Matrix DisplaysDocument7 pagesHow To Design LED Signage and LED Matrix DisplaysRemon MagdyNo ratings yet

- Neuronetics Neurostar Tms System™ User Manual: ConfidentialDocument168 pagesNeuronetics Neurostar Tms System™ User Manual: ConfidentialJulian ReyesNo ratings yet

- Nano-Pulse ElectrolysisDocument4 pagesNano-Pulse ElectrolysisKaryadi DjayaNo ratings yet

- Allen Practice AnalogDocument23 pagesAllen Practice AnalogvarunjothishNo ratings yet

- Renaissance of HF DC RX YU1LMDocument30 pagesRenaissance of HF DC RX YU1LMjoedarockNo ratings yet

- Schumann Resonator - Fabio's Blog About ElectronicsDocument2 pagesSchumann Resonator - Fabio's Blog About ElectronicsStellaEstel0% (1)

- Money Market HedgingDocument3 pagesMoney Market HedgingTahir HafeezNo ratings yet

- Smart CardDocument15 pagesSmart CardAnonymous XZUyueNNo ratings yet

- RF Power DetectorsDocument43 pagesRF Power Detectorsromilg_1No ratings yet

- EmfDocument10 pagesEmfgoudsaab007100% (1)

- Signal Generator ManualDocument6 pagesSignal Generator ManualDave ShshNo ratings yet

- Long Range Spy Robot Using Internet of ThingsDocument11 pagesLong Range Spy Robot Using Internet of ThingsIJRASETPublicationsNo ratings yet

- VR Based Tele-Presence Robot Using Raspberry PiDocument6 pagesVR Based Tele-Presence Robot Using Raspberry PiIJRASETPublicationsNo ratings yet

- Design of Ultra Low Noise AmplifiersDocument10 pagesDesign of Ultra Low Noise AmplifiersRakotomalala Mamy TianaNo ratings yet

- Gamma CameraDocument26 pagesGamma CameraNishtha TanejaNo ratings yet

- BVP651 Led530-4s 830 Psu DX10 Alu SRG10 PDFDocument3 pagesBVP651 Led530-4s 830 Psu DX10 Alu SRG10 PDFRiska Putri AmirNo ratings yet

- What Is SMD LEDDocument17 pagesWhat Is SMD LEDMohammad FaisalNo ratings yet

- Main Seminar Pts (Bilogical Computers)Document32 pagesMain Seminar Pts (Bilogical Computers)eeshasinghNo ratings yet

- Submitted By: Rajat Garg C08541 EECE, 7th SemDocument22 pagesSubmitted By: Rajat Garg C08541 EECE, 7th Semrajatgarg90No ratings yet

- Understanding-Electric-Magnetic-Fields 2013Document16 pagesUnderstanding-Electric-Magnetic-Fields 2013marietaNo ratings yet

- HHHHHHHHHDocument21 pagesHHHHHHHHHjameswovelee7No ratings yet

- Microphone WikiDocument20 pagesMicrophone WikiRaymond O. EjercitoNo ratings yet

- Planar TransformerDocument16 pagesPlanar TransformerParag RekhiNo ratings yet

- Visualization of Magnetic Field Generated by PortaDocument6 pagesVisualization of Magnetic Field Generated by PortajuanNo ratings yet

- Shull V Sorkin Motion and Amended ComplaintDocument85 pagesShull V Sorkin Motion and Amended ComplaintTHROnlineNo ratings yet

- Fractal Antennas: Ahmed Kiani, 260059400 Syed Takshed Karim, 260063503 Serder Burak Solak, 260141304Document9 pagesFractal Antennas: Ahmed Kiani, 260059400 Syed Takshed Karim, 260063503 Serder Burak Solak, 260141304Richa SharmaNo ratings yet

- Yamaha RX v596 HTR 5250 RX v596rdsDocument76 pagesYamaha RX v596 HTR 5250 RX v596rdsFiliberto CaraballoNo ratings yet

- An Interview With Rife - Royal Rife Research - EuropeDocument35 pagesAn Interview With Rife - Royal Rife Research - EuropeWilian PereiraNo ratings yet

- Malaviya National Institute of Technology: Submitted byDocument22 pagesMalaviya National Institute of Technology: Submitted byArpit JakarNo ratings yet

- E CoreDocument68 pagesE CoreSaiman ShettyNo ratings yet

- To Simple Operations Like Addition and SubtractionDocument36 pagesTo Simple Operations Like Addition and SubtractionsonalighareNo ratings yet

- Elf Circuit DesignDocument5 pagesElf Circuit DesignKatja GoiteNo ratings yet

- Oscillator: Requirements For An OscillatorDocument19 pagesOscillator: Requirements For An OscillatorSauravAbidRahmanNo ratings yet

- Richard L. Davis - Non-Inductive ResistanceDocument10 pagesRichard L. Davis - Non-Inductive Resistancealexanderf_20No ratings yet

- Project Report On Dna Computing: Information Technology For ManagersDocument12 pagesProject Report On Dna Computing: Information Technology For Managersanshu002No ratings yet

- PHY321GE2 Medical Imaging PDFDocument19 pagesPHY321GE2 Medical Imaging PDFPathmathasNo ratings yet

- Can Resonant Oscillations of The Earth Ionosphere Influence The Human Brain BiorhythmDocument13 pagesCan Resonant Oscillations of The Earth Ionosphere Influence The Human Brain BiorhythmBryan Graczyk100% (1)

- Detecting Biodynamic Signals - (Part I) by Michael Theroux - Borderlands (Vol. 52)Document10 pagesDetecting Biodynamic Signals - (Part I) by Michael Theroux - Borderlands (Vol. 52)pomodoroNo ratings yet

- Ch5 Currency Derivatives (FX Management Tools)Document4 pagesCh5 Currency Derivatives (FX Management Tools)Aditya ChoudharyNo ratings yet

- Multinational Financial Management 10th Edition Shapiro Solutions ManualDocument15 pagesMultinational Financial Management 10th Edition Shapiro Solutions Manualcoactiongaleaiyan100% (27)

- 02 TCHE414 L1 ExchangeRate Forstudent3Document20 pages02 TCHE414 L1 ExchangeRate Forstudent3Ngo Thi Hanh NguyenNo ratings yet

- Ge Acctg 7Document5 pagesGe Acctg 7ezraelydanNo ratings yet

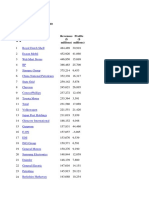

- TOP500frtune PDFDocument19 pagesTOP500frtune PDFVikas RNo ratings yet

- The Vega Food Company-FerrerDocument5 pagesThe Vega Food Company-FerrerHector Lim0% (1)

- Dir ReportDocument34 pagesDir ReportRupasinghNo ratings yet

- Introduction To Accounting HandoutDocument2 pagesIntroduction To Accounting HandoutJeysel CarpioNo ratings yet

- FilipinoDocument80 pagesFilipinoJolo NavajasNo ratings yet

- Iiarf Cbok Responding To Fraud Risk October 2015 PDFDocument28 pagesIiarf Cbok Responding To Fraud Risk October 2015 PDFMāhmõūd ĀhmēdNo ratings yet

- ESOPDocument8 pagesESOPKiran GvNo ratings yet

- Business Structures Advantages and Disadvantages of Common Business StructuresDocument2 pagesBusiness Structures Advantages and Disadvantages of Common Business StructuresShariBarry123No ratings yet

- Notes of Formation of CompaniesDocument8 pagesNotes of Formation of Companiesjosh mukwendaNo ratings yet

- BRC (Company Law - Group 6)Document13 pagesBRC (Company Law - Group 6)UditaNo ratings yet

- DERIVATIVESDocument30 pagesDERIVATIVESAyanda MabuthoNo ratings yet

- George Ty, The Man Behind Metrobank'S SuccessDocument7 pagesGeorge Ty, The Man Behind Metrobank'S SuccessKing LopezNo ratings yet

- Reforming Company LawDocument550 pagesReforming Company LawBISEKONo ratings yet

- Answers To PTP - Final - Syllabus 2012 - Dec 2014 - Set 1Document22 pagesAnswers To PTP - Final - Syllabus 2012 - Dec 2014 - Set 1prashansha kumudNo ratings yet

- Business Law & RegulationDocument2 pagesBusiness Law & RegulationAshley Kate HapeNo ratings yet

- Fortune Park Hotels Limited PDFDocument14 pagesFortune Park Hotels Limited PDFNiranjanNo ratings yet

- Board Structure & Directors - BECGDocument32 pagesBoard Structure & Directors - BECGVaidehi Shukla100% (1)

- Lecture 09 - Dual-Listed Company ArbitrageDocument32 pagesLecture 09 - Dual-Listed Company ArbitrageecondocsNo ratings yet

- SEBI (ICDR) Regulations, 2018Document45 pagesSEBI (ICDR) Regulations, 2018Vikas Vohra, Corporate BabaNo ratings yet

- Company Compliances For StartupsDocument6 pagesCompany Compliances For StartupsKrishnendu BhattacharyyaNo ratings yet

- Hedging Using OptionsDocument66 pagesHedging Using Optionsmehtarushab89% (9)

- QUIZ C4 Sec. 35-58 CORP. NAME - Set-A True or FalseDocument1 pageQUIZ C4 Sec. 35-58 CORP. NAME - Set-A True or FalseLyka mae LabadanNo ratings yet

- Compiled By: Pankaj GargDocument29 pagesCompiled By: Pankaj GargB GANAPATHYNo ratings yet

- Week 2 & 3 Scope of Corporate LawDocument28 pagesWeek 2 & 3 Scope of Corporate LawMatinJavedNo ratings yet

- Case 5-1Document4 pagesCase 5-1fitriNo ratings yet

- Quantitative Finance PDFDocument4 pagesQuantitative Finance PDFaishNo ratings yet

- Tavakoli GSDocument3 pagesTavakoli GSZerohedge100% (2)

- 23 Castillo V Balinghasay, GR No. 150976, October 18, 2004Document11 pages23 Castillo V Balinghasay, GR No. 150976, October 18, 2004Edgar Calzita AlotaNo ratings yet