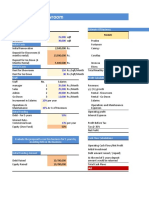

Example On Operating Lease and Finance Lease

Example On Operating Lease and Finance Lease

You might also like

- Bonnie Road ModelDocument14 pagesBonnie Road Modelmzhao8100% (1)

- Task 1 AnswerDocument9 pagesTask 1 AnswerSiddhant Aggarwal20% (5)

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2Yash JasaparaNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- Simple LBODocument16 pagesSimple LBOsingh0001No ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2deepika0% (1)

- Assumptions - : Amazon Cashflow & Profit ForecastDocument22 pagesAssumptions - : Amazon Cashflow & Profit Forecastlengyianchua206No ratings yet

- Basic Model-01Document6 pagesBasic Model-01Sambit SarkarNo ratings yet

- Financial Model Forecasting - Case StudyDocument15 pagesFinancial Model Forecasting - Case Study唐鹏飞No ratings yet

- Mg2451 Engineering Economics and Cost Analysis Questions and AnswersDocument11 pagesMg2451 Engineering Economics and Cost Analysis Questions and AnswersSenthil Kumar100% (1)

- Primus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungDocument26 pagesPrimus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungfmulyanaNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Primus AutomationDocument23 pagesPrimus AutomationhimanshusangaNo ratings yet

- Assignments of DR Reddy FranchiseDocument4 pagesAssignments of DR Reddy Franchiseshrish guptaNo ratings yet

- Phuket Beach Hotel - 2022Document10 pagesPhuket Beach Hotel - 2022Gavani Durga SaiNo ratings yet

- PGP25394 Keshav Sureka G CFDocument13 pagesPGP25394 Keshav Sureka G CFKeshavSurekaNo ratings yet

- LBO Assignment (AIM)Document20 pagesLBO Assignment (AIM)prachiNo ratings yet

- Franchise - CarDocument14 pagesFranchise - Carshrish guptaNo ratings yet

- Anta Forecast Template STD 2023Document8 pagesAnta Forecast Template STD 2023Ronnie KurtzbardNo ratings yet

- Phuket BeachDocument10 pagesPhuket BeachNepathya NmImsNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2tinothing01No ratings yet

- Assignment Capital BudgetingDocument29 pagesAssignment Capital BudgetingYasha Sahu0% (1)

- Case Primus AutomationDocument26 pagesCase Primus AutomationHeniNo ratings yet

- Assignment FSADocument5 pagesAssignment FSAbakerNo ratings yet

- Capital BudgetingDocument18 pagesCapital Budgetingteen agerNo ratings yet

- LeasingDocument14 pagesLeasingSana SarfarazNo ratings yet

- Red Chilli WorkingsDocument10 pagesRed Chilli WorkingsImran UmarNo ratings yet

- Current Ratio (Current Assets/current Liab) 1.3475324123Document4 pagesCurrent Ratio (Current Assets/current Liab) 1.3475324123Sukanta ChatterjeeNo ratings yet

- Existing Machine New Machine: Case 11.1: Ritesh Foundaries LimitedDocument2 pagesExisting Machine New Machine: Case 11.1: Ritesh Foundaries LimitedMukul KadyanNo ratings yet

- Profitability RatioDocument11 pagesProfitability RatioNicole Kate PorrasNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789No ratings yet

- SAS AirlineDocument9 pagesSAS AirlinejamilkhannNo ratings yet

- Assignment N3Document12 pagesAssignment N3Maiko KopadzeNo ratings yet

- ValuationDocument21 pagesValuationammarNo ratings yet

- Cash FlowsDocument11 pagesCash FlowsruicarhotmailcomNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2Art Euphoria100% (1)

- Is Excel Participant Samarth - Simplified v2Document9 pagesIs Excel Participant Samarth - Simplified v2samarth halliNo ratings yet

- Assigment 4 Tutor Financial Accounting II - Audry Martarini Putri - 210169622Document8 pagesAssigment 4 Tutor Financial Accounting II - Audry Martarini Putri - 210169622Oshin MenNo ratings yet

- Training Business Case Day 2Document13 pagesTraining Business Case Day 2amritakiranaaNo ratings yet

- Hertz Write UpDocument5 pagesHertz Write Uprishabh jainNo ratings yet

- Ias 36 Example Simple Impairment Test of CGU Based On Value in UseDocument7 pagesIas 36 Example Simple Impairment Test of CGU Based On Value in Usedevanand bhawNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Financial Statement AnalysisDocument28 pagesFinancial Statement AnalysisariefNo ratings yet

- Capital Budgeting SolutionDocument6 pagesCapital Budgeting SolutionAsad AliNo ratings yet

- Fundamental Analysis of Bosch (BOSCH LTD)Document6 pagesFundamental Analysis of Bosch (BOSCH LTD)Jeffry MahiNo ratings yet

- Lease Question and SolutionDocument7 pagesLease Question and Solutionsajedul100% (1)

- BUSM365 CH7 Student Version .XLSX 1Document14 pagesBUSM365 CH7 Student Version .XLSX 1Kesarapu Venkata ApparaoNo ratings yet

- Pepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsDocument28 pagesPepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsJulio CesarNo ratings yet

- NPV LesseeDocument6 pagesNPV Lesseekabirsharan4No ratings yet

- Horizontal and Vertical AnalysisDocument5 pagesHorizontal and Vertical AnalysisAshley Rouge Capati QuirozNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2animecommunity04No ratings yet

- NMIMS Global Access School For Continuing Education (NGA-SCE) Course: Financial AccountingDocument8 pagesNMIMS Global Access School For Continuing Education (NGA-SCE) Course: Financial AccountingMinaal KutriyaarNo ratings yet

- DCF Valuation-BDocument11 pagesDCF Valuation-BElsa100% (1)

- IS Excel Participant (Risit Savani) - Simplified v2Document9 pagesIS Excel Participant (Risit Savani) - Simplified v2risitsavaniNo ratings yet

- Evaluating The Firm'S Dividend PolicyDocument11 pagesEvaluating The Firm'S Dividend PolicyYash Aggarwal BD20073No ratings yet

- Ch08 - Principles of Capital InvestmentDocument7 pagesCh08 - Principles of Capital InvestmentStevin GeorgeNo ratings yet

- Operating Lease Converter: InputsDocument44 pagesOperating Lease Converter: InputsJosé Manuel EstebanNo ratings yet

- Financial ModellingDocument72 pagesFinancial ModellingAina MichaelNo ratings yet

- FRA Ratio AnalysisDocument4 pagesFRA Ratio AnalysisSrishTi RaiNo ratings yet

- Generate StatementDocument3 pagesGenerate StatementBHASKAR SEWA SANSTHANNo ratings yet

- Taxation I Lesson 1 and 2 Introduction TDocument13 pagesTaxation I Lesson 1 and 2 Introduction TApex LionheartNo ratings yet

- Dealing With COVID-19 - Best Business Practices 180320Document2 pagesDealing With COVID-19 - Best Business Practices 180320Jane SadakaNo ratings yet

- CH 1 - Kombinasi BisnisDocument29 pagesCH 1 - Kombinasi BisnisJulia Pratiwi ParhusipNo ratings yet

- Annual Income Tax ReturnDocument6 pagesAnnual Income Tax Returnirene deiparineNo ratings yet

- ch1 - InvestmentDocument38 pagesch1 - InvestmenthussamNo ratings yet

- The Journal Oct-Dec 2022Document106 pagesThe Journal Oct-Dec 2022zoey thakuriiNo ratings yet

- Priya Research Report Sbi - Dox..Document93 pagesPriya Research Report Sbi - Dox..Alok PandeyNo ratings yet

- Activity1 MidtermsDocument3 pagesActivity1 Midtermslil mixNo ratings yet

- Divide by Average Number of Shares OutstandingDocument11 pagesDivide by Average Number of Shares OutstandingJo FenNo ratings yet

- Quick and Dirty Interpretation of RatiosDocument4 pagesQuick and Dirty Interpretation of RatiosGauravNo ratings yet

- Economics of Money Banking and Financial Markets 1st Edition Mishkin Test BankDocument25 pagesEconomics of Money Banking and Financial Markets 1st Edition Mishkin Test BankKristinRichardsygci100% (66)

- Financial Planning Process: Lesson 3.1Document20 pagesFinancial Planning Process: Lesson 3.1Tin CabosNo ratings yet

- Ketan Parekh ScamDocument9 pagesKetan Parekh ScamKetan VichareNo ratings yet

- Questions MCQDocument15 pagesQuestions MCQRaj TakhtaniNo ratings yet

- Jim 1000 RC 6Document29 pagesJim 1000 RC 6Bảo ThiênNo ratings yet

- Case: Cenabal (A) Time Period: 12 July 2006 Protagonist: Jennifer Macdonald, The Owner of CenabalDocument3 pagesCase: Cenabal (A) Time Period: 12 July 2006 Protagonist: Jennifer Macdonald, The Owner of CenabalROSE AUGUSTINE CHERUKARA 2227044No ratings yet

- Yecondev MidtermDocument13 pagesYecondev MidtermRaven VeranaNo ratings yet

- IRDA Agent Exam Sample Paper 1Document12 pagesIRDA Agent Exam Sample Paper 1Awdhesh SoniNo ratings yet

- LAW Partnership Act 1932Document10 pagesLAW Partnership Act 1932ritesh2030No ratings yet

- BramDocument2 pagesBramIshidaUryuuNo ratings yet

- Health Ensure Floater - Policy Schedule: Proposer DetailsDocument3 pagesHealth Ensure Floater - Policy Schedule: Proposer DetailsValand NileshNo ratings yet

- Cash Discount: What Is A Cash Discount? Definition of Cash DiscountDocument12 pagesCash Discount: What Is A Cash Discount? Definition of Cash DiscountHumanityNo ratings yet

- Northcentral University Assignment Cover Sheet: LearnerDocument15 pagesNorthcentral University Assignment Cover Sheet: LearnerMorcy Jones100% (1)

- Course Syllabus - Investment ManagementDocument4 pagesCourse Syllabus - Investment ManagementDJ Gonzales100% (1)

- Revele - Key Metrics WhitepaperDocument18 pagesRevele - Key Metrics WhitepaperMansour TurkiNo ratings yet

- Tender Form For Dematerialised SharesDocument2 pagesTender Form For Dematerialised Sharessen chandanNo ratings yet

- ABM BFW6 M 9 RevisedDocument21 pagesABM BFW6 M 9 Revised30 Odicta, Justine AnneNo ratings yet

- 112380-237973 20190331 PDFDocument5 pages112380-237973 20190331 PDFKutty KausyNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Bonnie Road ModelDocument14 pagesBonnie Road Modelmzhao8100% (1)

- Task 1 AnswerDocument9 pagesTask 1 AnswerSiddhant Aggarwal20% (5)

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2Yash JasaparaNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Ezz Steel Financial AnalysisDocument31 pagesEzz Steel Financial Analysismohamed ashorNo ratings yet

- Simple LBODocument16 pagesSimple LBOsingh0001No ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2deepika0% (1)

- Assumptions - : Amazon Cashflow & Profit ForecastDocument22 pagesAssumptions - : Amazon Cashflow & Profit Forecastlengyianchua206No ratings yet

- Basic Model-01Document6 pagesBasic Model-01Sambit SarkarNo ratings yet

- Financial Model Forecasting - Case StudyDocument15 pagesFinancial Model Forecasting - Case Study唐鹏飞No ratings yet

- Mg2451 Engineering Economics and Cost Analysis Questions and AnswersDocument11 pagesMg2451 Engineering Economics and Cost Analysis Questions and AnswersSenthil Kumar100% (1)

- Primus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungDocument26 pagesPrimus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungfmulyanaNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Primus AutomationDocument23 pagesPrimus AutomationhimanshusangaNo ratings yet

- Assignments of DR Reddy FranchiseDocument4 pagesAssignments of DR Reddy Franchiseshrish guptaNo ratings yet

- Phuket Beach Hotel - 2022Document10 pagesPhuket Beach Hotel - 2022Gavani Durga SaiNo ratings yet

- PGP25394 Keshav Sureka G CFDocument13 pagesPGP25394 Keshav Sureka G CFKeshavSurekaNo ratings yet

- LBO Assignment (AIM)Document20 pagesLBO Assignment (AIM)prachiNo ratings yet

- Franchise - CarDocument14 pagesFranchise - Carshrish guptaNo ratings yet

- Anta Forecast Template STD 2023Document8 pagesAnta Forecast Template STD 2023Ronnie KurtzbardNo ratings yet

- Phuket BeachDocument10 pagesPhuket BeachNepathya NmImsNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2tinothing01No ratings yet

- Assignment Capital BudgetingDocument29 pagesAssignment Capital BudgetingYasha Sahu0% (1)

- Case Primus AutomationDocument26 pagesCase Primus AutomationHeniNo ratings yet

- Assignment FSADocument5 pagesAssignment FSAbakerNo ratings yet

- Capital BudgetingDocument18 pagesCapital Budgetingteen agerNo ratings yet

- LeasingDocument14 pagesLeasingSana SarfarazNo ratings yet

- Red Chilli WorkingsDocument10 pagesRed Chilli WorkingsImran UmarNo ratings yet

- Current Ratio (Current Assets/current Liab) 1.3475324123Document4 pagesCurrent Ratio (Current Assets/current Liab) 1.3475324123Sukanta ChatterjeeNo ratings yet

- Existing Machine New Machine: Case 11.1: Ritesh Foundaries LimitedDocument2 pagesExisting Machine New Machine: Case 11.1: Ritesh Foundaries LimitedMukul KadyanNo ratings yet

- Profitability RatioDocument11 pagesProfitability RatioNicole Kate PorrasNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789No ratings yet

- SAS AirlineDocument9 pagesSAS AirlinejamilkhannNo ratings yet

- Assignment N3Document12 pagesAssignment N3Maiko KopadzeNo ratings yet

- ValuationDocument21 pagesValuationammarNo ratings yet

- Cash FlowsDocument11 pagesCash FlowsruicarhotmailcomNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2Art Euphoria100% (1)

- Is Excel Participant Samarth - Simplified v2Document9 pagesIs Excel Participant Samarth - Simplified v2samarth halliNo ratings yet

- Assigment 4 Tutor Financial Accounting II - Audry Martarini Putri - 210169622Document8 pagesAssigment 4 Tutor Financial Accounting II - Audry Martarini Putri - 210169622Oshin MenNo ratings yet

- Training Business Case Day 2Document13 pagesTraining Business Case Day 2amritakiranaaNo ratings yet

- Hertz Write UpDocument5 pagesHertz Write Uprishabh jainNo ratings yet

- Ias 36 Example Simple Impairment Test of CGU Based On Value in UseDocument7 pagesIas 36 Example Simple Impairment Test of CGU Based On Value in Usedevanand bhawNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Financial Statement AnalysisDocument28 pagesFinancial Statement AnalysisariefNo ratings yet

- Capital Budgeting SolutionDocument6 pagesCapital Budgeting SolutionAsad AliNo ratings yet

- Fundamental Analysis of Bosch (BOSCH LTD)Document6 pagesFundamental Analysis of Bosch (BOSCH LTD)Jeffry MahiNo ratings yet

- Lease Question and SolutionDocument7 pagesLease Question and Solutionsajedul100% (1)

- BUSM365 CH7 Student Version .XLSX 1Document14 pagesBUSM365 CH7 Student Version .XLSX 1Kesarapu Venkata ApparaoNo ratings yet

- Pepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsDocument28 pagesPepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsJulio CesarNo ratings yet

- NPV LesseeDocument6 pagesNPV Lesseekabirsharan4No ratings yet

- Horizontal and Vertical AnalysisDocument5 pagesHorizontal and Vertical AnalysisAshley Rouge Capati QuirozNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2animecommunity04No ratings yet

- NMIMS Global Access School For Continuing Education (NGA-SCE) Course: Financial AccountingDocument8 pagesNMIMS Global Access School For Continuing Education (NGA-SCE) Course: Financial AccountingMinaal KutriyaarNo ratings yet

- DCF Valuation-BDocument11 pagesDCF Valuation-BElsa100% (1)

- IS Excel Participant (Risit Savani) - Simplified v2Document9 pagesIS Excel Participant (Risit Savani) - Simplified v2risitsavaniNo ratings yet

- Evaluating The Firm'S Dividend PolicyDocument11 pagesEvaluating The Firm'S Dividend PolicyYash Aggarwal BD20073No ratings yet

- Ch08 - Principles of Capital InvestmentDocument7 pagesCh08 - Principles of Capital InvestmentStevin GeorgeNo ratings yet

- Operating Lease Converter: InputsDocument44 pagesOperating Lease Converter: InputsJosé Manuel EstebanNo ratings yet

- Financial ModellingDocument72 pagesFinancial ModellingAina MichaelNo ratings yet

- FRA Ratio AnalysisDocument4 pagesFRA Ratio AnalysisSrishTi RaiNo ratings yet

- Generate StatementDocument3 pagesGenerate StatementBHASKAR SEWA SANSTHANNo ratings yet

- Taxation I Lesson 1 and 2 Introduction TDocument13 pagesTaxation I Lesson 1 and 2 Introduction TApex LionheartNo ratings yet

- Dealing With COVID-19 - Best Business Practices 180320Document2 pagesDealing With COVID-19 - Best Business Practices 180320Jane SadakaNo ratings yet

- CH 1 - Kombinasi BisnisDocument29 pagesCH 1 - Kombinasi BisnisJulia Pratiwi ParhusipNo ratings yet

- Annual Income Tax ReturnDocument6 pagesAnnual Income Tax Returnirene deiparineNo ratings yet

- ch1 - InvestmentDocument38 pagesch1 - InvestmenthussamNo ratings yet

- The Journal Oct-Dec 2022Document106 pagesThe Journal Oct-Dec 2022zoey thakuriiNo ratings yet

- Priya Research Report Sbi - Dox..Document93 pagesPriya Research Report Sbi - Dox..Alok PandeyNo ratings yet

- Activity1 MidtermsDocument3 pagesActivity1 Midtermslil mixNo ratings yet

- Divide by Average Number of Shares OutstandingDocument11 pagesDivide by Average Number of Shares OutstandingJo FenNo ratings yet

- Quick and Dirty Interpretation of RatiosDocument4 pagesQuick and Dirty Interpretation of RatiosGauravNo ratings yet

- Economics of Money Banking and Financial Markets 1st Edition Mishkin Test BankDocument25 pagesEconomics of Money Banking and Financial Markets 1st Edition Mishkin Test BankKristinRichardsygci100% (66)

- Financial Planning Process: Lesson 3.1Document20 pagesFinancial Planning Process: Lesson 3.1Tin CabosNo ratings yet

- Ketan Parekh ScamDocument9 pagesKetan Parekh ScamKetan VichareNo ratings yet

- Questions MCQDocument15 pagesQuestions MCQRaj TakhtaniNo ratings yet

- Jim 1000 RC 6Document29 pagesJim 1000 RC 6Bảo ThiênNo ratings yet

- Case: Cenabal (A) Time Period: 12 July 2006 Protagonist: Jennifer Macdonald, The Owner of CenabalDocument3 pagesCase: Cenabal (A) Time Period: 12 July 2006 Protagonist: Jennifer Macdonald, The Owner of CenabalROSE AUGUSTINE CHERUKARA 2227044No ratings yet

- Yecondev MidtermDocument13 pagesYecondev MidtermRaven VeranaNo ratings yet

- IRDA Agent Exam Sample Paper 1Document12 pagesIRDA Agent Exam Sample Paper 1Awdhesh SoniNo ratings yet

- LAW Partnership Act 1932Document10 pagesLAW Partnership Act 1932ritesh2030No ratings yet

- BramDocument2 pagesBramIshidaUryuuNo ratings yet

- Health Ensure Floater - Policy Schedule: Proposer DetailsDocument3 pagesHealth Ensure Floater - Policy Schedule: Proposer DetailsValand NileshNo ratings yet

- Cash Discount: What Is A Cash Discount? Definition of Cash DiscountDocument12 pagesCash Discount: What Is A Cash Discount? Definition of Cash DiscountHumanityNo ratings yet

- Northcentral University Assignment Cover Sheet: LearnerDocument15 pagesNorthcentral University Assignment Cover Sheet: LearnerMorcy Jones100% (1)

- Course Syllabus - Investment ManagementDocument4 pagesCourse Syllabus - Investment ManagementDJ Gonzales100% (1)

- Revele - Key Metrics WhitepaperDocument18 pagesRevele - Key Metrics WhitepaperMansour TurkiNo ratings yet

- Tender Form For Dematerialised SharesDocument2 pagesTender Form For Dematerialised Sharessen chandanNo ratings yet

- ABM BFW6 M 9 RevisedDocument21 pagesABM BFW6 M 9 Revised30 Odicta, Justine AnneNo ratings yet

- 112380-237973 20190331 PDFDocument5 pages112380-237973 20190331 PDFKutty KausyNo ratings yet