Download as docx, pdf, or txt

You might also like

- Wildcat Capital Case M&A Invesment Real EstateDocument7 pagesWildcat Capital Case M&A Invesment Real EstatePaco Colín8% (12)

- Bradley Bankert Official LetterDocument5 pagesBradley Bankert Official LetterMichael Henry100% (2)

- Problem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer ADocument37 pagesProblem 15-1 (AICPA Adapted) : Solution 15 - 1 Answer AAldrin Lozano87% (15)

- NPV Analysis SpreadsheetDocument16 pagesNPV Analysis SpreadsheetInformation should be FREE100% (1)

- Dussehra Offer! Full Package at Extended Discounted Price Rs.16040Document2 pagesDussehra Offer! Full Package at Extended Discounted Price Rs.16040Prasanna ManaviNo ratings yet

- DRM - Handouts (1) 2Document54 pagesDRM - Handouts (1) 2tanshlinkedinNo ratings yet

- Payoff Schedule Payoff Chart: Nifty at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: Nifty at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- Keafer Mfg. Cash BudgetDocument2 pagesKeafer Mfg. Cash BudgetElcah Myrrh LaridaNo ratings yet

- Technicals 12062008 RCHDocument4 pagesTechnicals 12062008 RCHapi-3862995No ratings yet

- Region Country Units Sold Unit PriceDocument4 pagesRegion Country Units Sold Unit PriceHannahNo ratings yet

- Pondi M LondiDocument6 pagesPondi M Londirishabhmishra77.rmNo ratings yet

- Varahi TradersDocument78 pagesVarahi TradersJAGDISH ZALANo ratings yet

- Payoff Schedule Payoff Chart: Nifty at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: Nifty at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- Payoff Schedule Payoff Chart: Nifty at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: Nifty at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- 30 PDFDocument2 pages30 PDFAKSHAYA AKSHAYANo ratings yet

- Short StrangleDocument2 pagesShort StrangleAKSHAYA AKSHAYANo ratings yet

- Binomial Valuation With Instant Tree BuilderDocument3 pagesBinomial Valuation With Instant Tree BuilderPrabhas TejaNo ratings yet

- How Many Units Do I Need To Sell To Breakeven?: Date: December 10, 2017Document1 pageHow Many Units Do I Need To Sell To Breakeven?: Date: December 10, 2017Danny SmithNo ratings yet

- Payoff Schedule Payoff Chart: Nifty at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: Nifty at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- Strategy Name Number of Option Legs Direction: Short Straddle 2 Market NeutralDocument5 pagesStrategy Name Number of Option Legs Direction: Short Straddle 2 Market NeutralRichard GregoryNo ratings yet

- Imovel Black Week 2022 ATÉ 7 DEZDocument2 pagesImovel Black Week 2022 ATÉ 7 DEZJefferson AlbuquerqueNo ratings yet

- Breakeven-Analysis 2Document1 pageBreakeven-Analysis 2walterNo ratings yet

- Frequency Distribution TableDocument4 pagesFrequency Distribution TableRosemarie GutualNo ratings yet

- Case Study CharlieDocument9 pagesCase Study CharlieHIMANSHU AGRAWALNo ratings yet

- Enter Expiry 4/9/2020 Enter Strike Price 9000 Long CallDocument4 pagesEnter Expiry 4/9/2020 Enter Strike Price 9000 Long CallSenthil KumarNo ratings yet

- HAF 213 Module 3 Example-1Document9 pagesHAF 213 Module 3 Example-1ekaarmstrong0No ratings yet

- Long Call Calendar Spread - 5paisa ArticleDocument4 pagesLong Call Calendar Spread - 5paisa ArticlepksNo ratings yet

- Risk Man. & Comp. SheetDocument10 pagesRisk Man. & Comp. Sheetaarmcourse1No ratings yet

- 40 PDFDocument2 pages40 PDFAKSHAYA AKSHAYANo ratings yet

- Payoff Schedule Payoff Chart: Nifty at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: Nifty at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- Airlines Katar Airlines Lusiana Airlines Go-Indio Spice Jet Indiana Airlines East-West Airlines Ethihad Emiritus Air MalayaDocument24 pagesAirlines Katar Airlines Lusiana Airlines Go-Indio Spice Jet Indiana Airlines East-West Airlines Ethihad Emiritus Air Malayamahesh kumarNo ratings yet

- PBOR Pension BenifitDocument9 pagesPBOR Pension Benifitशिवा यादव सोनूNo ratings yet

- Gann Intraday CalculatorDocument2 pagesGann Intraday CalculatorSanjay PuriNo ratings yet

- Statistics and Data Analysis Part - Eight Analysis of VarianceDocument46 pagesStatistics and Data Analysis Part - Eight Analysis of Variancehugohp71No ratings yet

- Written Assignment Unit 3 Principle of Finance 2Document2 pagesWritten Assignment Unit 3 Principle of Finance 27drk7yfbvjNo ratings yet

- Compensation and Rewards Management - Session 9-10Document12 pagesCompensation and Rewards Management - Session 9-10Daksh AnejaNo ratings yet

- Vaibhav Price 17-03-2024Document1 pageVaibhav Price 17-03-2024Aayat ChoudharyNo ratings yet

- Strategy Name Number of Option Legs Direction: Long Straddle 2 Market NeutralDocument4 pagesStrategy Name Number of Option Legs Direction: Long Straddle 2 Market NeutralAbhishek Kumar SinghNo ratings yet

- Airlines Katar Airlines Lusiana Airlines Go-Indio Spice Jet Indiana Airlines East-West Airlines Ethihad Emiritus Air MalayaDocument24 pagesAirlines Katar Airlines Lusiana Airlines Go-Indio Spice Jet Indiana Airlines East-West Airlines Ethihad Emiritus Air Malayamahesh kumarNo ratings yet

- FS&I Class 6 FEB 2023Document3 pagesFS&I Class 6 FEB 2023Sanskar saxenaNo ratings yet

- Proposal Kedubes Malaysia - ALT 1Document5 pagesProposal Kedubes Malaysia - ALT 1Mohd Mubarak ShamsuddinNo ratings yet

- Vehicle Prices 17 TH Aug 2021Document52 pagesVehicle Prices 17 TH Aug 2021AD ADNo ratings yet

- Payoff Schedule Payoff Chart: Nifty at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: Nifty at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- Strategy Name Number of Option Legs Direction: Long Straddle 2 Market NeutralDocument4 pagesStrategy Name Number of Option Legs Direction: Long Straddle 2 Market NeutralDivyansh GolyanNo ratings yet

- SMART 22 Aug 2016Document45 pagesSMART 22 Aug 2016siva kNo ratings yet

- Frequency Ranges: H5: 518.000-542.000 MHZDocument5 pagesFrequency Ranges: H5: 518.000-542.000 MHZJNo ratings yet

- Uji Reliabilitas DSK - KPD RiskaDocument3 pagesUji Reliabilitas DSK - KPD RiskaHari WijonarkoNo ratings yet

- Strategy Name Number of Option Legs Direction: Synthetic Call Two BullishDocument6 pagesStrategy Name Number of Option Legs Direction: Synthetic Call Two BullishShaan ThackerNo ratings yet

- Cash Flow WaterfallDocument8 pagesCash Flow WaterfallEmmanuelDasiNo ratings yet

- LeaseDocument6 pagesLeasevnprakash sharmaNo ratings yet

- Call BackspreadDocument2 pagesCall BackspreadAKSHAYA AKSHAYANo ratings yet

- Buy StraddleDocument2 pagesBuy StraddleAKSHAYA AKSHAYANo ratings yet

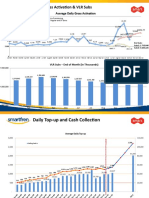

- Daily Gross Activation & VLR SubsDocument3 pagesDaily Gross Activation & VLR Subsdarwin.saragihNo ratings yet

- Payoff Schedule Payoff Chart: NIFTY at Expiry Net PayoffDocument2 pagesPayoff Schedule Payoff Chart: NIFTY at Expiry Net PayoffAKSHAYA AKSHAYANo ratings yet

- F9 - BPP - MOCK EXAM - QnsDocument10 pagesF9 - BPP - MOCK EXAM - QnsRaluca PanaitNo ratings yet

- Airlines Katar Airlines Lusiana Airlines Go-Indio Spice Jet Indiana Airlines East-West Airlines Ethihad Emiritus Air MalayaDocument29 pagesAirlines Katar Airlines Lusiana Airlines Go-Indio Spice Jet Indiana Airlines East-West Airlines Ethihad Emiritus Air Malayamahesh kumarNo ratings yet

- Formulae and Discount Tables: Professional Level Examination Financial ManagementDocument2 pagesFormulae and Discount Tables: Professional Level Examination Financial ManagementClaudine CjNo ratings yet

- Margin NumericalDocument5 pagesMargin NumericalBhavya SinghNo ratings yet

- Bought Back Profit From Buyback Spot Profit/loss Profit/loss From Futures Total Profit LossDocument2 pagesBought Back Profit From Buyback Spot Profit/loss Profit/loss From Futures Total Profit LossrahulNo ratings yet

- A Study of Marketing Benefits and Challenges of E-Commerce An Emerging Economy (With Special Reference of Myntra)Document72 pagesA Study of Marketing Benefits and Challenges of E-Commerce An Emerging Economy (With Special Reference of Myntra)opsteam.turnaround2No ratings yet

- MC Cambell Enterprises: Proposal Submitted byDocument12 pagesMC Cambell Enterprises: Proposal Submitted byCarlos SDNo ratings yet

- French Morning WorkDocument24 pagesFrench Morning WorkhongNo ratings yet

- Chapter Eight The Theory and Estimation of Cost: Relevant and Irrelevant CostsDocument23 pagesChapter Eight The Theory and Estimation of Cost: Relevant and Irrelevant Costsnatalie clyde matesNo ratings yet

- MGT 162 Group Assignments 25Document20 pagesMGT 162 Group Assignments 25MUHAMMAD FAUZAN ABU BAKARNo ratings yet

- History of Vivo 123Document14 pagesHistory of Vivo 123VenkateshKonda100% (2)

- Bonobos'sblue-Oceanstrategy in Theu.s.Document2 pagesBonobos'sblue-Oceanstrategy in Theu.s.Khin Myo ThanNo ratings yet

- Form 1.0 2020 PBB Denr Xi Revised BJ Dav SurDocument11 pagesForm 1.0 2020 PBB Denr Xi Revised BJ Dav SurLeo Artemio PuertosNo ratings yet

- Industrial VisitDocument8 pagesIndustrial VisitmarySibiliaNo ratings yet

- DPR Selwa 02.07.2020Document22 pagesDPR Selwa 02.07.2020ravibelavadiNo ratings yet

- Cargo Arrival Notice: Consignee NotifyDocument2 pagesCargo Arrival Notice: Consignee NotifySRIKANTH VENKAMAMIDINo ratings yet

- When in Doubt Blame The Accountants Said Mathew Ingram inDocument2 pagesWhen in Doubt Blame The Accountants Said Mathew Ingram inLet's Talk With HassanNo ratings yet

- JP 4-0 Joint Logistic 18jun2008Document124 pagesJP 4-0 Joint Logistic 18jun2008Bryan FenclNo ratings yet

- Bài tập nhóm online PDFDocument2 pagesBài tập nhóm online PDFVY NGUYEN THI THUYNo ratings yet

- Aircon Company Profile PDFDocument15 pagesAircon Company Profile PDFOsama RizwanNo ratings yet

- Chapter 1editedDocument13 pagesChapter 1editedMuktar jiboNo ratings yet

- 05 - Labour Law Trade UnionDocument3 pages05 - Labour Law Trade UnionBhavya RayalaNo ratings yet

- Learnovate Ecommerce - Finance InternDocument9 pagesLearnovate Ecommerce - Finance Internyash kumar nayakNo ratings yet

- OD123541630427671000Document1 pageOD123541630427671000rahulamarpur2661No ratings yet

- Scaling Your Business For Success: Overnight Successes Are Not Always "Overnight"Document6 pagesScaling Your Business For Success: Overnight Successes Are Not Always "Overnight"Invoice Out 2No ratings yet

- 写作申请信Document5 pages写作申请信ewa9wwn1100% (1)

- Index NumbersDocument6 pagesIndex Numberskaziba stephenNo ratings yet

- Balance ConfirmationDocument11 pagesBalance Confirmationeastern arteqaNo ratings yet

- Module 4 - Notes ReceivableDocument22 pagesModule 4 - Notes ReceivableJennalyn S. GanalonNo ratings yet

- Supplement EbookDocument24 pagesSupplement Ebooksimplemax32No ratings yet

- DIGEST-5. Bank of America v. American Realty Corp.Document3 pagesDIGEST-5. Bank of America v. American Realty Corp.Karl EstavillaNo ratings yet

- Marketing Across Cultures cw2Document19 pagesMarketing Across Cultures cw2api-518143243No ratings yet

- WTO, IMF and World BankDocument4 pagesWTO, IMF and World BanktallalbasahelNo ratings yet