Download as ppt, pdf, or txt

You might also like

- List of Developer in DubaiDocument28 pagesList of Developer in Dubaiimad40% (5)

- Cordelia BLDocument2 pagesCordelia BLวรัญชิต โรจนอุฬารNo ratings yet

- The Shipbroker’s Working Knowledge: Dry Cargo Chartering in PracticeFrom EverandThe Shipbroker’s Working Knowledge: Dry Cargo Chartering in PracticeRating: 5 out of 5 stars5/5 (1)

- International Trade Law QuestionsDocument25 pagesInternational Trade Law QuestionsShivansh BansalNo ratings yet

- Sample Copy VOLCOADocument4 pagesSample Copy VOLCOATRn JasonNo ratings yet

- Back To Back LCDocument1 pageBack To Back LCJayant Nair0% (2)

- Export Process Flow-FCL PDFDocument8 pagesExport Process Flow-FCL PDFRonakkumar PatelNo ratings yet

- Facility Manager ResumeDocument6 pagesFacility Manager ResumeimadNo ratings yet

- International Trade FinanceDocument9 pagesInternational Trade FinanceChacha Donald Trump America waleNo ratings yet

- Letter of CreditDocument14 pagesLetter of CreditaulicyNo ratings yet

- Benefits Trade Finance Instruments Risk Mitigation and Capital AdequacyDocument56 pagesBenefits Trade Finance Instruments Risk Mitigation and Capital AdequacyJahongirNo ratings yet

- The Micro-Structure of International Trade: Exports and Imports A Typical Foreign Exchange TransactionDocument37 pagesThe Micro-Structure of International Trade: Exports and Imports A Typical Foreign Exchange TransactionShannon PereiraNo ratings yet

- Impor Export ChartDocument1 pageImpor Export ChartInaam DuggalNo ratings yet

- 3C07 2017-4-019 GNnanda T1 Bhs - InggrisDocument1 page3C07 2017-4-019 GNnanda T1 Bhs - InggrisGregurius DaniswaraNo ratings yet

- Export-Import FlowchartDocument1 pageExport-Import Flowchartwahyu hidayatNo ratings yet

- Letter of Credit Flow Based On SWIFT MTDocument20 pagesLetter of Credit Flow Based On SWIFT MTA. T. M. Anisur RabbaniNo ratings yet

- Transferable L/C Back To Back L/C: Oleh: Dr. Miftahul Huda, SH, LLMDocument11 pagesTransferable L/C Back To Back L/C: Oleh: Dr. Miftahul Huda, SH, LLMAmalia Izzati HanifahNo ratings yet

- Docs Papers For LCDocument23 pagesDocs Papers For LCRedwan RahmanNo ratings yet

- Documentary CreditDocument15 pagesDocumentary CreditArmantoCepongNo ratings yet

- Session. 25. Letters of Credit and Bank GuaranteesDocument30 pagesSession. 25. Letters of Credit and Bank GuaranteesHemant KawalkarNo ratings yet

- Quy Trình Hàng SEADocument4 pagesQuy Trình Hàng SEAVũMinhNo ratings yet

- Bill of LadingDocument14 pagesBill of Ladingmohammad arif dwiyantoNo ratings yet

- Prosedur Transaksi Impor & ExportDocument8 pagesProsedur Transaksi Impor & ExportGamescool ManiaNo ratings yet

- Chapter One: Introduction: 1.1 Project Title: Foreign Exchange Accounting SystemDocument36 pagesChapter One: Introduction: 1.1 Project Title: Foreign Exchange Accounting SystemSojeeb AhmedNo ratings yet

- ch03 Trade Process-2Document22 pagesch03 Trade Process-2PeleoneNo ratings yet

- Chapter 2 - Bill of LadingDocument54 pagesChapter 2 - Bill of LadingLương Trần Thủy TiênNo ratings yet

- Bills ofDocument8 pagesBills ofManish kumar chauhanNo ratings yet

- Foreign Exchange QuestionnaireDocument9 pagesForeign Exchange QuestionnaireMahadi HasanNo ratings yet

- Chapter 4 - Methods - SVDocument33 pagesChapter 4 - Methods - SVLê HiếuNo ratings yet

- Payment Metode: Letter of CreditDocument10 pagesPayment Metode: Letter of CreditmuhamadardigunawanNo ratings yet

- Bills of LadingDocument23 pagesBills of LadingNelson VargheseNo ratings yet

- ÔN Thanh Toán Quốc TếDocument17 pagesÔN Thanh Toán Quốc Tếandc20No ratings yet

- Export Pricing Strategies Marginal Cost PricingDocument33 pagesExport Pricing Strategies Marginal Cost PricingShamim Mahbub100% (1)

- 2020 NTP IP Chapter 3 4Document81 pages2020 NTP IP Chapter 3 4viet hoangNo ratings yet

- International PaymentDocument24 pagesInternational PaymentAgung WidyadnyanaNo ratings yet

- 2023 NTP IP Chapter 4Document30 pages2023 NTP IP Chapter 4Thư Phan Trần AnhNo ratings yet

- BCA Impor Product Material 2021-13 DesDocument10 pagesBCA Impor Product Material 2021-13 DesCalvinNo ratings yet

- 4 - Liner CharteringDocument32 pages4 - Liner CharteringLệ Mẫn TrầnNo ratings yet

- LECUTRA 5 Bill of Lading & Airway Bill ExplainedDocument18 pagesLECUTRA 5 Bill of Lading & Airway Bill ExplainedLaura PinedaNo ratings yet

- A Simplified Documentary Credit ProcedureDocument1 pageA Simplified Documentary Credit ProcedureМария НиколенкоNo ratings yet

- Role of LC in International Trade FinanceDocument17 pagesRole of LC in International Trade FinanceMuhammad Yasir92% (13)

- Verify UpdateDocument2 pagesVerify Updateyosmile0123No ratings yet

- International Trade Finance: Letter of CreditDocument14 pagesInternational Trade Finance: Letter of Creditkhabis007No ratings yet

- Bill of Lading For Ocean Transport or Multimodal TransportDocument2 pagesBill of Lading For Ocean Transport or Multimodal Transportyosmile0123No ratings yet

- CH11-7Ed The BillingAccounts ReceivableCash ReceiptsDocument32 pagesCH11-7Ed The BillingAccounts ReceivableCash ReceiptsMiftah FauziNo ratings yet

- Lecture 04 Bill of LadingDocument20 pagesLecture 04 Bill of Ladingchhenghuy81No ratings yet

- BL DomicanaDocument2 pagesBL DomicanaMETALORD CLNo ratings yet

- Role of LC in International Trade FinanceDocument18 pagesRole of LC in International Trade FinancePakassignmentNo ratings yet

- Episode 7 Terms - of - PaymentDocument54 pagesEpisode 7 Terms - of - PaymentJunhua CaiNo ratings yet

- 9.0financing Foreign TradeDocument35 pages9.0financing Foreign TradeNajwa SulaimanNo ratings yet

- EIM - Chapter 2Document33 pagesEIM - Chapter 2Đức Anh NguyễnNo ratings yet

- WWW - Pakassignment.Blo: Send Your Assignments and Projects To Be Displayed Here As Sample For Others atDocument52 pagesWWW - Pakassignment.Blo: Send Your Assignments and Projects To Be Displayed Here As Sample For Others atPakassignmentNo ratings yet

- Shipping and Customs Formalities For Import & Export ConsignmentsDocument4 pagesShipping and Customs Formalities For Import & Export ConsignmentsMM. HasanNo ratings yet

- Chapter 4 GDTMQT - SVDocument81 pagesChapter 4 GDTMQT - SVNguyễn Thị TâmNo ratings yet

- A Documentary CollectionDocument4 pagesA Documentary CollectionSyed Habib SultanNo ratings yet

- Fig 1 - Transport Market Place - Direct Offer Work Flow DiagramDocument1 pageFig 1 - Transport Market Place - Direct Offer Work Flow Diagramzelalem fesshaNo ratings yet

- What Is A Bill of LadingDocument29 pagesWhat Is A Bill of LadingRicardo PirelaNo ratings yet

- Financing International TradeDocument19 pagesFinancing International TradeUmesh ChandraNo ratings yet

- Delivery Order ProcessDocument14 pagesDelivery Order ProcessAkanksha GanveerNo ratings yet

- 4 4提单的缮制与签发Document40 pages4 4提单的缮制与签发Romi Siham100% (1)

- Shipping Practice - With a Consideration of the Law Relating TheretoFrom EverandShipping Practice - With a Consideration of the Law Relating TheretoNo ratings yet

- The Forwarder´s Concern: An introduction into the marine liability of forwarders, carriers and warehousemen, the claims handling and the related insuranceFrom EverandThe Forwarder´s Concern: An introduction into the marine liability of forwarders, carriers and warehousemen, the claims handling and the related insuranceNo ratings yet

- D.B.D.Sampath: "Nandana", Harbour Road, Mirissa. Sri Lanka. Tel: +94 716256652, +94 412251677 EmailDocument7 pagesD.B.D.Sampath: "Nandana", Harbour Road, Mirissa. Sri Lanka. Tel: +94 716256652, +94 412251677 EmailimadNo ratings yet

- Descender Equipment AG 10 EN 341 CE 0158Document9 pagesDescender Equipment AG 10 EN 341 CE 0158imadNo ratings yet

- Facility Manager - Osman CVDocument5 pagesFacility Manager - Osman CVimadNo ratings yet

- Resume SourabhDocument3 pagesResume SourabhimadNo ratings yet

- Facilities & Operation ManagerDocument5 pagesFacilities & Operation Managerimad100% (1)

- Tony C Jose - Facilities & Estimations EngineerDocument4 pagesTony C Jose - Facilities & Estimations EngineerimadNo ratings yet

- Facility Manager - Updated Resume KhalidDocument3 pagesFacility Manager - Updated Resume KhalidimadNo ratings yet

- Mohit Bhalla CV 5Document2 pagesMohit Bhalla CV 5imadNo ratings yet

- 1001 Unbelievable Facts-Eng PDFDocument210 pages1001 Unbelievable Facts-Eng PDFAmol Deshpande100% (1)

- Mohamed Maged Resume - Facility Manager-5-2Document4 pagesMohamed Maged Resume - Facility Manager-5-2imadNo ratings yet

- Permission Letter To Exit A Machine From Hotel PremisesDocument1 pagePermission Letter To Exit A Machine From Hotel PremisesimadNo ratings yet

- 1000 Facts On Mammals (2002)Document226 pages1000 Facts On Mammals (2002)imadNo ratings yet

- Equipment Repair Maintennce - 2013Document1 pageEquipment Repair Maintennce - 2013imadNo ratings yet

- JAMMU & KASHMIR Policies 2012-2015Document35 pagesJAMMU & KASHMIR Policies 2012-2015imadNo ratings yet

- Impressions Services (P) LTD - Company CatalogDocument33 pagesImpressions Services (P) LTD - Company CatalogimadNo ratings yet

- Yhoo Q2 2012Document10 pagesYhoo Q2 2012TechCrunchNo ratings yet

- Incident Report WrittingDocument7 pagesIncident Report WrittingimadNo ratings yet

- G77Document26 pagesG77imadNo ratings yet

- SAARCDocument12 pagesSAARCimadNo ratings yet

- Kotler ASEAN - The Paradox of Globalization Vs LocalizationDocument39 pagesKotler ASEAN - The Paradox of Globalization Vs LocalizationimadNo ratings yet

- International OrganisationsDocument2 pagesInternational OrganisationsDeepak KumarNo ratings yet

- Easing World RestrictionsDocument2 pagesEasing World RestrictionsDeanne GuintoNo ratings yet

- Is WTO A Rich Man's Club - AbhinandanDocument16 pagesIs WTO A Rich Man's Club - AbhinandanAbhinandan NarayanNo ratings yet

- WTO Dispute Settlement Mechanism: A Critical Analysis: (Type The Document Subtitle)Document18 pagesWTO Dispute Settlement Mechanism: A Critical Analysis: (Type The Document Subtitle)siddharth pandeyNo ratings yet

- Birla CenturyDocument1 pageBirla CenturyPrashantNo ratings yet

- The HeckscherDocument6 pagesThe HeckscherLad Rahul LadNo ratings yet

- International Trade - Group Assignment - Summer 2022Document3 pagesInternational Trade - Group Assignment - Summer 2022Shanju ShanthanNo ratings yet

- Sunvik Steels PVT LTD Pre-Feasibility Report: ProductionDocument1 pageSunvik Steels PVT LTD Pre-Feasibility Report: ProductionKendra TerryNo ratings yet

- Specificic Requested Info For NED - ReviewedDocument4 pagesSpecificic Requested Info For NED - ReviewedRaphael MashapaNo ratings yet

- Air India MergerDocument9 pagesAir India MergershrutimaitNo ratings yet

- Econ4415 International TradeDocument5 pagesEcon4415 International TradeTanya SinghNo ratings yet

- Pure TheoryDocument3 pagesPure TheoryAshima MishraNo ratings yet

- International Organization Notes CompleteDocument3 pagesInternational Organization Notes Completeapi-328061525100% (1)

- UK General One PagerDocument1 pageUK General One PagerMuhammad HarisNo ratings yet

- VNT Step 3 Manuel MuñozDocument14 pagesVNT Step 3 Manuel Muñozedinsonrios93No ratings yet

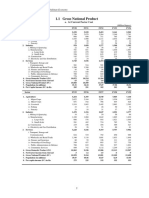

- 1.1 Gross National Product: Handbook of Statistics On Pakistan EconomyDocument23 pages1.1 Gross National Product: Handbook of Statistics On Pakistan EconomyAlysaad LasiNo ratings yet

- Module 1 International Trade and WTODocument26 pagesModule 1 International Trade and WTOMEHAK ZAIDINo ratings yet

- Cotton Value ChainDocument185 pagesCotton Value ChainTemesgen RegassaNo ratings yet

- Wto PPT Mana.Document14 pagesWto PPT Mana.Manaram JangidNo ratings yet

- Freight Out or Delivery Expenses or TransportationDocument4 pagesFreight Out or Delivery Expenses or TransportationMichelle GoNo ratings yet

- Quotation Freight Import LCL Asean, China, Busan, TaiwanDocument1 pageQuotation Freight Import LCL Asean, China, Busan, TaiwanfurqonNo ratings yet

- Advantages of Multinational CompaniesDocument20 pagesAdvantages of Multinational CompaniesPraveen Kumar PiarNo ratings yet

- 2 Test - Chapter 2 - World Trade, An Overview - Quizlet SOLUTIONDocument5 pages2 Test - Chapter 2 - World Trade, An Overview - Quizlet SOLUTIONMia KulalNo ratings yet

- Guide To Measuring Global Production 2015.120 137Document20 pagesGuide To Measuring Global Production 2015.120 137Florentina Viorica GheorgheNo ratings yet

- Valuation of Rules and Certificates of Origin For SME Export Process From PeruDocument16 pagesValuation of Rules and Certificates of Origin For SME Export Process From PeruLaís Marques100% (1)

- Bill of LadingDocument8 pagesBill of LadingMalik Asad MalikNo ratings yet

- CDCS Supporting Documentation - in Basket 2Document4 pagesCDCS Supporting Documentation - in Basket 2sreeks456100% (1)

- bài tập unit 4Document5 pagesbài tập unit 4Hiền PhạmNo ratings yet

- Middle East June 11 Full 1307632987869Document2 pagesMiddle East June 11 Full 1307632987869kennethnacNo ratings yet