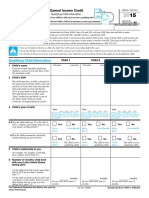

US Internal Revenue Service: F1040sei - 1999

US Internal Revenue Service: F1040sei - 1999

You might also like

- Tax Return 2022 Mardik MardikianDocument23 pagesTax Return 2022 Mardik Mardikianyusuf Fajar100% (4)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Elisagarza Taxes 2021Document16 pagesElisagarza Taxes 2021Illest Alive206100% (1)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- US Internal Revenue Service: F1040sei - 2004Document2 pagesUS Internal Revenue Service: F1040sei - 2004IRSNo ratings yet

- 2007 Schedule EICDocument2 pages2007 Schedule EICFileYourTaxesNow100% (3)

- Before You Begin:: Earned Income CreditDocument2 pagesBefore You Begin:: Earned Income CreditstylenzNo ratings yet

- US Internal Revenue Service: F1040sei - 2002Document2 pagesUS Internal Revenue Service: F1040sei - 2002IRSNo ratings yet

- US Internal Revenue Service: f8901 AccessibleDocument2 pagesUS Internal Revenue Service: f8901 AccessibleIRSNo ratings yet

- US Internal Revenue Service: F1040sei - 1994Document2 pagesUS Internal Revenue Service: F1040sei - 1994IRSNo ratings yet

- US Internal Revenue Service: f8839 - 2004Document2 pagesUS Internal Revenue Service: f8839 - 2004IRSNo ratings yet

- Child Tax Credit: (For Individuals Sent Here From The Form 1040 or 1040A Instructions)Document12 pagesChild Tax Credit: (For Individuals Sent Here From The Form 1040 or 1040A Instructions)IRSNo ratings yet

- f8901 AccessibleDocument2 pagesf8901 AccessibleAbhishekNo ratings yet

- US Internal Revenue Service: f8615 - 1999Document2 pagesUS Internal Revenue Service: f8615 - 1999IRSNo ratings yet

- US Internal Revenue Service: f1040sh - 2005Document2 pagesUS Internal Revenue Service: f1040sh - 2005IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1997Document2 pagesUS Internal Revenue Service: f8814 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2000Document2 pagesUS Internal Revenue Service: f8814 - 2000IRSNo ratings yet

- US Internal Revenue Service: F8453ol - 2005Document2 pagesUS Internal Revenue Service: F8453ol - 2005IRSNo ratings yet

- Schedule 21Document5 pagesSchedule 21rohina406No ratings yet

- US Internal Revenue Service: f8615 - 1997Document2 pagesUS Internal Revenue Service: f8615 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2005Document3 pagesUS Internal Revenue Service: f8814 - 2005IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2004Document3 pagesUS Internal Revenue Service: f8814 - 2004IRSNo ratings yet

- Instant Download PDF Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual Full ChapterDocument36 pagesInstant Download PDF Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual Full Chapternadjmolidbom100% (4)

- US Internal Revenue Service: f8814 - 2001Document2 pagesUS Internal Revenue Service: f8814 - 2001IRSNo ratings yet

- US Internal Revenue Service: f8615 - 2003Document1 pageUS Internal Revenue Service: f8615 - 2003IRSNo ratings yet

- Earned Income Credit-WorksheetDocument1 pageEarned Income Credit-Worksheetcam.guerreNo ratings yet

- US Internal Revenue Service: f8453 - 2004Document2 pagesUS Internal Revenue Service: f8453 - 2004IRSNo ratings yet

- US Internal Revenue Service: f8615 - 2002Document1 pageUS Internal Revenue Service: f8615 - 2002IRSNo ratings yet

- US Internal Revenue Service: f8812 - 1999Document2 pagesUS Internal Revenue Service: f8812 - 1999IRSNo ratings yet

- US Internal Revenue Service: f8812 - 2005Document2 pagesUS Internal Revenue Service: f8812 - 2005IRSNo ratings yet

- US Internal Revenue Service: f8863 - 2005Document4 pagesUS Internal Revenue Service: f8863 - 2005IRSNo ratings yet

- Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual instant download all chapterDocument36 pagesIncome Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual instant download all chapterrussugillin26100% (2)

- US Internal Revenue Service: p972 - 2004Document16 pagesUS Internal Revenue Service: p972 - 2004IRSNo ratings yet

- U.S. Tax Return For Seniors Filing StatusDocument16 pagesU.S. Tax Return For Seniors Filing StatusJonathan Mahe100% (1)

- US Internal Revenue Service: f8814 - 1996Document2 pagesUS Internal Revenue Service: f8814 - 1996IRSNo ratings yet

- US Internal Revenue Service: f8615 - 1992Document2 pagesUS Internal Revenue Service: f8615 - 1992IRSNo ratings yet

- Unemployment Insurance Application: Filing InstructionsDocument12 pagesUnemployment Insurance Application: Filing InstructionsSylvester sampsonNo ratings yet

- US Internal Revenue Service: F1040sei - 1992Document2 pagesUS Internal Revenue Service: F1040sei - 1992IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1995Document2 pagesUS Internal Revenue Service: f8814 - 1995IRSNo ratings yet

- U.S. Tax Return For Seniors: Filing StatusDocument2 pagesU.S. Tax Return For Seniors: Filing StatusRemyan RNo ratings yet

- Norma 2021Document13 pagesNorma 2021Norma MichelNo ratings yet

- Vba 22 5490 AreDocument8 pagesVba 22 5490 AreAngelica Mae AcebedoNo ratings yet

- Dwnload Full Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual PDFDocument35 pagesDwnload Full Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual PDFseritahanger121us100% (12)

- Full Download Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions ManualDocument35 pagesFull Download Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manualisaacuru0ji100% (40)

- US Internal Revenue Service: f8814 - 1993Document2 pagesUS Internal Revenue Service: f8814 - 1993IRSNo ratings yet

- Federal Electronic Filing Instructions: Tax Year 2018Document13 pagesFederal Electronic Filing Instructions: Tax Year 2018Adonis TorrefielNo ratings yet

- Colon JuniorDocument36 pagesColon JuniorVicmali Papeleria Ciber50% (2)

- 4 Version K: Separation 1 of 2: BlackDocument2 pages4 Version K: Separation 1 of 2: BlackbaluNo ratings yet

- Tax Return 2021Document3 pagesTax Return 2021Mark ThomasNo ratings yet

- Imm 5501 eDocument1 pageImm 5501 eJMNo ratings yet

- 2020 Tax Return Documents (DERICK BROOKS A)Document2 pages2020 Tax Return Documents (DERICK BROOKS A)Patricia100% (2)

- US Internal Revenue Service: F8453ol - 2001Document2 pagesUS Internal Revenue Service: F8453ol - 2001IRSNo ratings yet

- US Internal Revenue Service: F8453ol - 2000Document2 pagesUS Internal Revenue Service: F8453ol - 2000IRSNo ratings yet

- 2021 Turbo Tax ReturnDocument4 pages2021 Turbo Tax ReturnEmonee WellsNo ratings yet

- Ssa 7162Document2 pagesSsa 7162grijalva100% (1)

- US Internal Revenue Service: f8812 - 2001Document2 pagesUS Internal Revenue Service: f8812 - 2001IRSNo ratings yet

- IRS Notice 1446Document1 pageIRS Notice 1446Courier JournalNo ratings yet

- US Internal Revenue Service: f8453 - 1996Document2 pagesUS Internal Revenue Service: f8453 - 1996IRSNo ratings yet

- US Internal Revenue Service: fw4s - 2005Document2 pagesUS Internal Revenue Service: fw4s - 2005IRSNo ratings yet

- Blank Schedule NRDocument2 pagesBlank Schedule NRtomislav javisNo ratings yet

- US Internal Revenue Service: f8814 - 1998Document2 pagesUS Internal Revenue Service: f8814 - 1998IRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

Download as pdf or txt

You might also like

- Tax Return 2022 Mardik MardikianDocument23 pagesTax Return 2022 Mardik Mardikianyusuf Fajar100% (4)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Elisagarza Taxes 2021Document16 pagesElisagarza Taxes 2021Illest Alive206100% (1)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- US Internal Revenue Service: F1040sei - 2004Document2 pagesUS Internal Revenue Service: F1040sei - 2004IRSNo ratings yet

- 2007 Schedule EICDocument2 pages2007 Schedule EICFileYourTaxesNow100% (3)

- Before You Begin:: Earned Income CreditDocument2 pagesBefore You Begin:: Earned Income CreditstylenzNo ratings yet

- US Internal Revenue Service: F1040sei - 2002Document2 pagesUS Internal Revenue Service: F1040sei - 2002IRSNo ratings yet

- US Internal Revenue Service: f8901 AccessibleDocument2 pagesUS Internal Revenue Service: f8901 AccessibleIRSNo ratings yet

- US Internal Revenue Service: F1040sei - 1994Document2 pagesUS Internal Revenue Service: F1040sei - 1994IRSNo ratings yet

- US Internal Revenue Service: f8839 - 2004Document2 pagesUS Internal Revenue Service: f8839 - 2004IRSNo ratings yet

- Child Tax Credit: (For Individuals Sent Here From The Form 1040 or 1040A Instructions)Document12 pagesChild Tax Credit: (For Individuals Sent Here From The Form 1040 or 1040A Instructions)IRSNo ratings yet

- f8901 AccessibleDocument2 pagesf8901 AccessibleAbhishekNo ratings yet

- US Internal Revenue Service: f8615 - 1999Document2 pagesUS Internal Revenue Service: f8615 - 1999IRSNo ratings yet

- US Internal Revenue Service: f1040sh - 2005Document2 pagesUS Internal Revenue Service: f1040sh - 2005IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1997Document2 pagesUS Internal Revenue Service: f8814 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2000Document2 pagesUS Internal Revenue Service: f8814 - 2000IRSNo ratings yet

- US Internal Revenue Service: F8453ol - 2005Document2 pagesUS Internal Revenue Service: F8453ol - 2005IRSNo ratings yet

- Schedule 21Document5 pagesSchedule 21rohina406No ratings yet

- US Internal Revenue Service: f8615 - 1997Document2 pagesUS Internal Revenue Service: f8615 - 1997IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2005Document3 pagesUS Internal Revenue Service: f8814 - 2005IRSNo ratings yet

- US Internal Revenue Service: f8814 - 2004Document3 pagesUS Internal Revenue Service: f8814 - 2004IRSNo ratings yet

- Instant Download PDF Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual Full ChapterDocument36 pagesInstant Download PDF Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual Full Chapternadjmolidbom100% (4)

- US Internal Revenue Service: f8814 - 2001Document2 pagesUS Internal Revenue Service: f8814 - 2001IRSNo ratings yet

- US Internal Revenue Service: f8615 - 2003Document1 pageUS Internal Revenue Service: f8615 - 2003IRSNo ratings yet

- Earned Income Credit-WorksheetDocument1 pageEarned Income Credit-Worksheetcam.guerreNo ratings yet

- US Internal Revenue Service: f8453 - 2004Document2 pagesUS Internal Revenue Service: f8453 - 2004IRSNo ratings yet

- US Internal Revenue Service: f8615 - 2002Document1 pageUS Internal Revenue Service: f8615 - 2002IRSNo ratings yet

- US Internal Revenue Service: f8812 - 1999Document2 pagesUS Internal Revenue Service: f8812 - 1999IRSNo ratings yet

- US Internal Revenue Service: f8812 - 2005Document2 pagesUS Internal Revenue Service: f8812 - 2005IRSNo ratings yet

- US Internal Revenue Service: f8863 - 2005Document4 pagesUS Internal Revenue Service: f8863 - 2005IRSNo ratings yet

- Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual instant download all chapterDocument36 pagesIncome Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual instant download all chapterrussugillin26100% (2)

- US Internal Revenue Service: p972 - 2004Document16 pagesUS Internal Revenue Service: p972 - 2004IRSNo ratings yet

- U.S. Tax Return For Seniors Filing StatusDocument16 pagesU.S. Tax Return For Seniors Filing StatusJonathan Mahe100% (1)

- US Internal Revenue Service: f8814 - 1996Document2 pagesUS Internal Revenue Service: f8814 - 1996IRSNo ratings yet

- US Internal Revenue Service: f8615 - 1992Document2 pagesUS Internal Revenue Service: f8615 - 1992IRSNo ratings yet

- Unemployment Insurance Application: Filing InstructionsDocument12 pagesUnemployment Insurance Application: Filing InstructionsSylvester sampsonNo ratings yet

- US Internal Revenue Service: F1040sei - 1992Document2 pagesUS Internal Revenue Service: F1040sei - 1992IRSNo ratings yet

- US Internal Revenue Service: f8814 - 1995Document2 pagesUS Internal Revenue Service: f8814 - 1995IRSNo ratings yet

- U.S. Tax Return For Seniors: Filing StatusDocument2 pagesU.S. Tax Return For Seniors: Filing StatusRemyan RNo ratings yet

- Norma 2021Document13 pagesNorma 2021Norma MichelNo ratings yet

- Vba 22 5490 AreDocument8 pagesVba 22 5490 AreAngelica Mae AcebedoNo ratings yet

- Dwnload Full Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual PDFDocument35 pagesDwnload Full Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manual PDFseritahanger121us100% (12)

- Full Download Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions ManualDocument35 pagesFull Download Income Tax Fundamentals 2013 31st Edition Whittenburg Solutions Manualisaacuru0ji100% (40)

- US Internal Revenue Service: f8814 - 1993Document2 pagesUS Internal Revenue Service: f8814 - 1993IRSNo ratings yet

- Federal Electronic Filing Instructions: Tax Year 2018Document13 pagesFederal Electronic Filing Instructions: Tax Year 2018Adonis TorrefielNo ratings yet

- Colon JuniorDocument36 pagesColon JuniorVicmali Papeleria Ciber50% (2)

- 4 Version K: Separation 1 of 2: BlackDocument2 pages4 Version K: Separation 1 of 2: BlackbaluNo ratings yet

- Tax Return 2021Document3 pagesTax Return 2021Mark ThomasNo ratings yet

- Imm 5501 eDocument1 pageImm 5501 eJMNo ratings yet

- 2020 Tax Return Documents (DERICK BROOKS A)Document2 pages2020 Tax Return Documents (DERICK BROOKS A)Patricia100% (2)

- US Internal Revenue Service: F8453ol - 2001Document2 pagesUS Internal Revenue Service: F8453ol - 2001IRSNo ratings yet

- US Internal Revenue Service: F8453ol - 2000Document2 pagesUS Internal Revenue Service: F8453ol - 2000IRSNo ratings yet

- 2021 Turbo Tax ReturnDocument4 pages2021 Turbo Tax ReturnEmonee WellsNo ratings yet

- Ssa 7162Document2 pagesSsa 7162grijalva100% (1)

- US Internal Revenue Service: f8812 - 2001Document2 pagesUS Internal Revenue Service: f8812 - 2001IRSNo ratings yet

- IRS Notice 1446Document1 pageIRS Notice 1446Courier JournalNo ratings yet

- US Internal Revenue Service: f8453 - 1996Document2 pagesUS Internal Revenue Service: f8453 - 1996IRSNo ratings yet

- US Internal Revenue Service: fw4s - 2005Document2 pagesUS Internal Revenue Service: fw4s - 2005IRSNo ratings yet

- Blank Schedule NRDocument2 pagesBlank Schedule NRtomislav javisNo ratings yet

- US Internal Revenue Service: f8814 - 1998Document2 pagesUS Internal Revenue Service: f8814 - 1998IRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet