Recording Procedures-Barangay Funds

Recording Procedures-Barangay Funds

You might also like

- Problem 3-9 Determining The Effects of Transactions On The Accounting EquationDocument1 pageProblem 3-9 Determining The Effects of Transactions On The Accounting EquationJaida CastilloNo ratings yet

- Barangay Financial Transactions Recording Procedures PresentationDocument20 pagesBarangay Financial Transactions Recording Procedures Presentationnelggkram82% (11)

- Pops Plan Workbook 18oct 2016Document44 pagesPops Plan Workbook 18oct 2016Cherry Bepitel100% (1)

- Prescribed Barangay FormsDocument54 pagesPrescribed Barangay FormsnelggkramNo ratings yet

- Ateneo Central Bar Operations 2007 Civil Law Summer ReviewerDocument24 pagesAteneo Central Bar Operations 2007 Civil Law Summer ReviewerMiGay Tan-Pelaez89% (9)

- Ateneo Central Bar Operations 2007 Civil Law Summer ReviewerDocument24 pagesAteneo Central Bar Operations 2007 Civil Law Summer ReviewerMiGay Tan-Pelaez89% (9)

- 56a - 21P Indemnity Bond Form (Taxpayer) (Final 08-08-20)Document1 page56a - 21P Indemnity Bond Form (Taxpayer) (Final 08-08-20)Alberto MartinezNo ratings yet

- Volume I (Operating Procedures)Document70 pagesVolume I (Operating Procedures)Warren JaraboNo ratings yet

- Volume I (Operating Procedures)Document73 pagesVolume I (Operating Procedures)Jay PabloNo ratings yet

- FY 2020 Budget Forum-LBM78Document85 pagesFY 2020 Budget Forum-LBM78Arman Bentain100% (1)

- Bgy Appropriations & Commitments Revised .5.8.07Document48 pagesBgy Appropriations & Commitments Revised .5.8.07AnnamaAnnama100% (1)

- Dardarat Budget NewDocument37 pagesDardarat Budget NewApril Joy Sumagit Hidalgo100% (1)

- Accounting For Barangay TransactionsDocument26 pagesAccounting For Barangay TransactionsDalrymple CasballedoNo ratings yet

- Brgy BudgetingDocument71 pagesBrgy BudgetingJing GraceNo ratings yet

- Republic of The Philippines Province of Camarines Sur Municipality of Ocampo Barangay Gatbo - O0oDocument26 pagesRepublic of The Philippines Province of Camarines Sur Municipality of Ocampo Barangay Gatbo - O0oCristina MelloriaNo ratings yet

- Republic Act No 10742Document19 pagesRepublic Act No 10742Rhuel MalquistoNo ratings yet

- Advisory Calendar of Barangay Mandatory DeliverablesDocument9 pagesAdvisory Calendar of Barangay Mandatory DeliverablesJo ReyesNo ratings yet

- SK Resolution Aprroving ABYIPDocument3 pagesSK Resolution Aprroving ABYIPBarangay JovellarNo ratings yet

- Barangay Budget Preparation 06-07-17Document132 pagesBarangay Budget Preparation 06-07-17Robert Tayam, Jr.0% (1)

- Sectoral StudiesDocument108 pagesSectoral StudiesIan Yoselle Narciso100% (1)

- AIP Blank Form 2020Document1 pageAIP Blank Form 2020Johara Soriano0% (1)

- DTP Narrative Template SampleDocument8 pagesDTP Narrative Template SampleBarangay Mabayo Morong Bataan100% (1)

- Annex C - Document Checklist DC1Document2 pagesAnnex C - Document Checklist DC1Christy Ledesma-Navarro100% (2)

- Cashbook: Deposit 2021Document5 pagesCashbook: Deposit 2021Yham Muleta AbordoNo ratings yet

- Bid Documents 2022Document17 pagesBid Documents 2022Arlene VillarosaNo ratings yet

- BDC Audit SGLGBDocument77 pagesBDC Audit SGLGBDILG LUPONNo ratings yet

- Office of The Sangguniang KabataanDocument4 pagesOffice of The Sangguniang KabataanParis DNNo ratings yet

- Annex A. LCPC WFP Form 001 CDocument1 pageAnnex A. LCPC WFP Form 001 CRhapNo ratings yet

- Laying The Foundation 1st 100 DaysDocument13 pagesLaying The Foundation 1st 100 DaysElias PolistoNo ratings yet

- Resolution No. 14 Realigned From Reading CenterDocument2 pagesResolution No. 14 Realigned From Reading CenterEileen Gerty ArceoNo ratings yet

- Barangay Development Council (BDC)Document2 pagesBarangay Development Council (BDC)sadzNo ratings yet

- Katarungang Pambarangay: By: Angelo S. Mahinay Enhanced By: Mlgoo Fidel M. NarismaDocument138 pagesKatarungang Pambarangay: By: Angelo S. Mahinay Enhanced By: Mlgoo Fidel M. NarismaMelvs NavarraNo ratings yet

- Dilg Memocircular 2019718 E4cdf5e7b2Document46 pagesDilg Memocircular 2019718 E4cdf5e7b2Elmalyn Olavera CarilloNo ratings yet

- Rbi Purok Luyan Registry of Barangay InhabitantsDocument38 pagesRbi Purok Luyan Registry of Barangay InhabitantsAldrin Dela CruzNo ratings yet

- The Municipal Budget ObservationDocument9 pagesThe Municipal Budget ObservationLoyd At AppleNo ratings yet

- Guidelines On The Appropriation, Release, PlanningDocument20 pagesGuidelines On The Appropriation, Release, PlanningCamila Anne GambanNo ratings yet

- Relevant Laws, Rules and Regulations For The Operations of SK'sDocument19 pagesRelevant Laws, Rules and Regulations For The Operations of SK'sLyndon G TimpugNo ratings yet

- Barangay Development CouncilDocument5 pagesBarangay Development CouncilJohny VillanuevaNo ratings yet

- Barangay FDPDocument17 pagesBarangay FDPCarlo Torres100% (1)

- SGLGDocument3 pagesSGLGNatacia100% (1)

- We Envision Barangay Cabraran Pequeño As A Unified and Peaceful Community. Promoting The Moral and Social Values of The Constituents and Responsive Barangay OfficialsDocument22 pagesWe Envision Barangay Cabraran Pequeño As A Unified and Peaceful Community. Promoting The Moral and Social Values of The Constituents and Responsive Barangay OfficialsGing F. Lumauig100% (1)

- Barangay Landican Annual Budget 2022Document25 pagesBarangay Landican Annual Budget 2022Maya AdovoNo ratings yet

- 2024 ADAC Audit AnnexesDocument57 pages2024 ADAC Audit Annexesdriezer23No ratings yet

- Office of The Punong Barangay Training DesignDocument5 pagesOffice of The Punong Barangay Training DesignLyka Abdullah TayuanNo ratings yet

- BUDGET AUTHORIZATION LECTURE-BARANGAYS-2020 - DesDocument66 pagesBUDGET AUTHORIZATION LECTURE-BARANGAYS-2020 - DesFernando ComedoyNo ratings yet

- Office of The Municipal Planning and Development CoordinatorDocument3 pagesOffice of The Municipal Planning and Development CoordinatorMark MagalonaNo ratings yet

- Utilization of 2018 SK FundsDocument2 pagesUtilization of 2018 SK FundsDavid Mikael Nava TaclinoNo ratings yet

- Internal Rules of Procedure SKDocument5 pagesInternal Rules of Procedure SKmanila dilgncr100% (2)

- The New Barangay Accounting SystemDocument10 pagesThe New Barangay Accounting SystemShekeinah Calingasan100% (1)

- Barangay Sto. Tomas: Office of The Punong Barangay Executive Order No. 23Document4 pagesBarangay Sto. Tomas: Office of The Punong Barangay Executive Order No. 23Jorge DanielleNo ratings yet

- Monitoring The Functionality of Barangay Nutrition CouncilDocument1 pageMonitoring The Functionality of Barangay Nutrition CouncilJoseph VillafuerteNo ratings yet

- Office of The Sangguniang Barangay: Autonomous Region in Muslim Mindanao Municipality of Binidayan Barangay PicotaaanDocument7 pagesOffice of The Sangguniang Barangay: Autonomous Region in Muslim Mindanao Municipality of Binidayan Barangay PicotaaanAlianimamsampornaNo ratings yet

- GAD Accomplishment Report 2021Document16 pagesGAD Accomplishment Report 2021Edgar Sanchez EndozoNo ratings yet

- Irp New 2Document8 pagesIrp New 2Barangay CalliatNo ratings yet

- Annual Investment Program CY 2016Document125 pagesAnnual Investment Program CY 2016Carl100% (2)

- Barangay Budget PreparationDocument72 pagesBarangay Budget PreparationRjay's EscapadeNo ratings yet

- Steps in Crafting The SK Annual Budget 2020Document2 pagesSteps in Crafting The SK Annual Budget 2020Jaypee BucatcatNo ratings yet

- 2018 BDC Orientation Seminar Executive SummaryDocument8 pages2018 BDC Orientation Seminar Executive SummaryJerry CruzNo ratings yet

- Record of Estimated and Actual IncomeDocument14 pagesRecord of Estimated and Actual IncomeEdna Salvador LadieroNo ratings yet

- CSO SelectionDocument38 pagesCSO SelectionLindsey MarieNo ratings yet

- Barangay BudgetingDocument25 pagesBarangay BudgetingEarthAngel OrganicsNo ratings yet

- Citizens Charter PDFDocument343 pagesCitizens Charter PDFJunnieson BonielNo ratings yet

- Accounting Reports PreparationDocument23 pagesAccounting Reports Preparationcao.lilydawnfNo ratings yet

- Barangay Financial ManagementDocument40 pagesBarangay Financial ManagementAgnes FernandezNo ratings yet

- MEMO - AnnoucementDocument1 pageMEMO - AnnoucementMarliezel SardaNo ratings yet

- Public Policy Formulation SlidesDocument29 pagesPublic Policy Formulation SlidesMarliezel Sarda100% (1)

- Department of Budget and ManagementDocument2 pagesDepartment of Budget and ManagementMarliezel SardaNo ratings yet

- The ASEAN Economic CommunityDocument3 pagesThe ASEAN Economic CommunityMarliezel SardaNo ratings yet

- Corruption Affects Us AllDocument2 pagesCorruption Affects Us AllMarliezel SardaNo ratings yet

- Reaction Paper NO 1 - Martial Law (Final)Document7 pagesReaction Paper NO 1 - Martial Law (Final)Marliezel Sarda40% (5)

- Federalism Refers To The Mixed or Compound Mode of GovernmentDocument3 pagesFederalism Refers To The Mixed or Compound Mode of GovernmentMarliezel SardaNo ratings yet

- Jardine Davies vs. CaDocument2 pagesJardine Davies vs. CaMarliezel SardaNo ratings yet

- UOB Infinity User Guide (Admin and Services)Document39 pagesUOB Infinity User Guide (Admin and Services)TomNo ratings yet

- Chapter 2, Concept of MoneyDocument18 pagesChapter 2, Concept of Moneymiracle123No ratings yet

- Sugeeta Wifi BillDocument2 pagesSugeeta Wifi Billsachin.dudelaNo ratings yet

- Lesson 1 Cash and Cash EquivalentsDocument10 pagesLesson 1 Cash and Cash EquivalentsRica Lei N. DomingoNo ratings yet

- 187 State of Karnataka V Ecom Gill Coffee Trading PVT LTD 13 Mar 2023 463904Document7 pages187 State of Karnataka V Ecom Gill Coffee Trading PVT LTD 13 Mar 2023 463904Nithyananda N LNo ratings yet

- bANK mANAGEMENTDocument111 pagesbANK mANAGEMENTSwati SharmaNo ratings yet

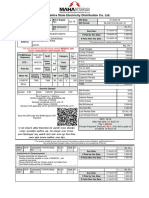

- Maharashtra State Electricity Distribution Co. LTD.: For Any Queries On This Bill Please Contact MSEDCL CallDocument1 pageMaharashtra State Electricity Distribution Co. LTD.: For Any Queries On This Bill Please Contact MSEDCL Callkishor chandaliyaNo ratings yet

- TheProcure To PayCyclebyChristineDoxeyDocument6 pagesTheProcure To PayCyclebyChristineDoxeyrajus_cisa6423No ratings yet

- Total Statement SummaryDocument4 pagesTotal Statement SummaryIia AdvertisementsNo ratings yet

- COMLAW3 Module1 Negotiable Instruments Law A PrimerDocument21 pagesCOMLAW3 Module1 Negotiable Instruments Law A PrimerAccounting 201No ratings yet

- Interview Capsule For Ibps RRB Sbi Po Ibps Po Ibps So 2023Document19 pagesInterview Capsule For Ibps RRB Sbi Po Ibps Po Ibps So 2023z09y68dhptNo ratings yet

- LANDBANK Weaccess Terms and ConditionsDocument4 pagesLANDBANK Weaccess Terms and ConditionsSabang High School (Region IV-B - Oriental Mindoro)No ratings yet

- L Uk Proc Wfa030 JDC 001 Gwi Job Data ChangeDocument32 pagesL Uk Proc Wfa030 JDC 001 Gwi Job Data Changeعادل بشير بٹھNo ratings yet

- The Federal Reserve System: Its Purposes and Functions 1939Document33 pagesThe Federal Reserve System: Its Purposes and Functions 1939Trey Sells100% (1)

- Account Statement PDFDocument12 pagesAccount Statement PDFChetan TNNo ratings yet

- 2 - Important Case Laws Important Case Laws On The Negotiable Instruments Act - Sec.138 CasesDocument30 pages2 - Important Case Laws Important Case Laws On The Negotiable Instruments Act - Sec.138 CasesAshish DavessarNo ratings yet

- Final AccountsDocument12 pagesFinal AccountsXander Tabuzo100% (1)

- Easy Pay Slip PDFDocument1 pageEasy Pay Slip PDFChanchal SharmaNo ratings yet

- Job Profile PWD PDFDocument32 pagesJob Profile PWD PDFJitender KumarNo ratings yet

- 157a PDFDocument24 pages157a PDFmedia boxNo ratings yet

- Commercial BanksDocument7 pagesCommercial BanksMahealaniPerezNo ratings yet

- GST ChallanDocument2 pagesGST ChallanRonak PataniNo ratings yet

- Fargo ND Civil Asset RecordsDocument75 pagesFargo ND Civil Asset RecordsDustin GawrylowNo ratings yet

- Circular Memo On Online RoW Portal 03.09.2022Document39 pagesCircular Memo On Online RoW Portal 03.09.2022Special Cell VMCNo ratings yet

- Lesson 3Document3 pagesLesson 3Adrian MarfilNo ratings yet

- Bcoc 131Document5 pagesBcoc 131Anamika T AnilNo ratings yet

- Mas 12 Working Capital ManagementDocument11 pagesMas 12 Working Capital ManagementDexanne BulanNo ratings yet

- Far Quick Notes and Test Bank PDFDocument72 pagesFar Quick Notes and Test Bank PDFFujikoNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Problem 3-9 Determining The Effects of Transactions On The Accounting EquationDocument1 pageProblem 3-9 Determining The Effects of Transactions On The Accounting EquationJaida CastilloNo ratings yet

- Barangay Financial Transactions Recording Procedures PresentationDocument20 pagesBarangay Financial Transactions Recording Procedures Presentationnelggkram82% (11)

- Pops Plan Workbook 18oct 2016Document44 pagesPops Plan Workbook 18oct 2016Cherry Bepitel100% (1)

- Prescribed Barangay FormsDocument54 pagesPrescribed Barangay FormsnelggkramNo ratings yet

- Ateneo Central Bar Operations 2007 Civil Law Summer ReviewerDocument24 pagesAteneo Central Bar Operations 2007 Civil Law Summer ReviewerMiGay Tan-Pelaez89% (9)

- Ateneo Central Bar Operations 2007 Civil Law Summer ReviewerDocument24 pagesAteneo Central Bar Operations 2007 Civil Law Summer ReviewerMiGay Tan-Pelaez89% (9)

- 56a - 21P Indemnity Bond Form (Taxpayer) (Final 08-08-20)Document1 page56a - 21P Indemnity Bond Form (Taxpayer) (Final 08-08-20)Alberto MartinezNo ratings yet

- Volume I (Operating Procedures)Document70 pagesVolume I (Operating Procedures)Warren JaraboNo ratings yet

- Volume I (Operating Procedures)Document73 pagesVolume I (Operating Procedures)Jay PabloNo ratings yet

- FY 2020 Budget Forum-LBM78Document85 pagesFY 2020 Budget Forum-LBM78Arman Bentain100% (1)

- Bgy Appropriations & Commitments Revised .5.8.07Document48 pagesBgy Appropriations & Commitments Revised .5.8.07AnnamaAnnama100% (1)

- Dardarat Budget NewDocument37 pagesDardarat Budget NewApril Joy Sumagit Hidalgo100% (1)

- Accounting For Barangay TransactionsDocument26 pagesAccounting For Barangay TransactionsDalrymple CasballedoNo ratings yet

- Brgy BudgetingDocument71 pagesBrgy BudgetingJing GraceNo ratings yet

- Republic of The Philippines Province of Camarines Sur Municipality of Ocampo Barangay Gatbo - O0oDocument26 pagesRepublic of The Philippines Province of Camarines Sur Municipality of Ocampo Barangay Gatbo - O0oCristina MelloriaNo ratings yet

- Republic Act No 10742Document19 pagesRepublic Act No 10742Rhuel MalquistoNo ratings yet

- Advisory Calendar of Barangay Mandatory DeliverablesDocument9 pagesAdvisory Calendar of Barangay Mandatory DeliverablesJo ReyesNo ratings yet

- SK Resolution Aprroving ABYIPDocument3 pagesSK Resolution Aprroving ABYIPBarangay JovellarNo ratings yet

- Barangay Budget Preparation 06-07-17Document132 pagesBarangay Budget Preparation 06-07-17Robert Tayam, Jr.0% (1)

- Sectoral StudiesDocument108 pagesSectoral StudiesIan Yoselle Narciso100% (1)

- AIP Blank Form 2020Document1 pageAIP Blank Form 2020Johara Soriano0% (1)

- DTP Narrative Template SampleDocument8 pagesDTP Narrative Template SampleBarangay Mabayo Morong Bataan100% (1)

- Annex C - Document Checklist DC1Document2 pagesAnnex C - Document Checklist DC1Christy Ledesma-Navarro100% (2)

- Cashbook: Deposit 2021Document5 pagesCashbook: Deposit 2021Yham Muleta AbordoNo ratings yet

- Bid Documents 2022Document17 pagesBid Documents 2022Arlene VillarosaNo ratings yet

- BDC Audit SGLGBDocument77 pagesBDC Audit SGLGBDILG LUPONNo ratings yet

- Office of The Sangguniang KabataanDocument4 pagesOffice of The Sangguniang KabataanParis DNNo ratings yet

- Annex A. LCPC WFP Form 001 CDocument1 pageAnnex A. LCPC WFP Form 001 CRhapNo ratings yet

- Laying The Foundation 1st 100 DaysDocument13 pagesLaying The Foundation 1st 100 DaysElias PolistoNo ratings yet

- Resolution No. 14 Realigned From Reading CenterDocument2 pagesResolution No. 14 Realigned From Reading CenterEileen Gerty ArceoNo ratings yet

- Barangay Development Council (BDC)Document2 pagesBarangay Development Council (BDC)sadzNo ratings yet

- Katarungang Pambarangay: By: Angelo S. Mahinay Enhanced By: Mlgoo Fidel M. NarismaDocument138 pagesKatarungang Pambarangay: By: Angelo S. Mahinay Enhanced By: Mlgoo Fidel M. NarismaMelvs NavarraNo ratings yet

- Dilg Memocircular 2019718 E4cdf5e7b2Document46 pagesDilg Memocircular 2019718 E4cdf5e7b2Elmalyn Olavera CarilloNo ratings yet

- Rbi Purok Luyan Registry of Barangay InhabitantsDocument38 pagesRbi Purok Luyan Registry of Barangay InhabitantsAldrin Dela CruzNo ratings yet

- The Municipal Budget ObservationDocument9 pagesThe Municipal Budget ObservationLoyd At AppleNo ratings yet

- Guidelines On The Appropriation, Release, PlanningDocument20 pagesGuidelines On The Appropriation, Release, PlanningCamila Anne GambanNo ratings yet

- Relevant Laws, Rules and Regulations For The Operations of SK'sDocument19 pagesRelevant Laws, Rules and Regulations For The Operations of SK'sLyndon G TimpugNo ratings yet

- Barangay Development CouncilDocument5 pagesBarangay Development CouncilJohny VillanuevaNo ratings yet

- Barangay FDPDocument17 pagesBarangay FDPCarlo Torres100% (1)

- SGLGDocument3 pagesSGLGNatacia100% (1)

- We Envision Barangay Cabraran Pequeño As A Unified and Peaceful Community. Promoting The Moral and Social Values of The Constituents and Responsive Barangay OfficialsDocument22 pagesWe Envision Barangay Cabraran Pequeño As A Unified and Peaceful Community. Promoting The Moral and Social Values of The Constituents and Responsive Barangay OfficialsGing F. Lumauig100% (1)

- Barangay Landican Annual Budget 2022Document25 pagesBarangay Landican Annual Budget 2022Maya AdovoNo ratings yet

- 2024 ADAC Audit AnnexesDocument57 pages2024 ADAC Audit Annexesdriezer23No ratings yet

- Office of The Punong Barangay Training DesignDocument5 pagesOffice of The Punong Barangay Training DesignLyka Abdullah TayuanNo ratings yet

- BUDGET AUTHORIZATION LECTURE-BARANGAYS-2020 - DesDocument66 pagesBUDGET AUTHORIZATION LECTURE-BARANGAYS-2020 - DesFernando ComedoyNo ratings yet

- Office of The Municipal Planning and Development CoordinatorDocument3 pagesOffice of The Municipal Planning and Development CoordinatorMark MagalonaNo ratings yet

- Utilization of 2018 SK FundsDocument2 pagesUtilization of 2018 SK FundsDavid Mikael Nava TaclinoNo ratings yet

- Internal Rules of Procedure SKDocument5 pagesInternal Rules of Procedure SKmanila dilgncr100% (2)

- The New Barangay Accounting SystemDocument10 pagesThe New Barangay Accounting SystemShekeinah Calingasan100% (1)

- Barangay Sto. Tomas: Office of The Punong Barangay Executive Order No. 23Document4 pagesBarangay Sto. Tomas: Office of The Punong Barangay Executive Order No. 23Jorge DanielleNo ratings yet

- Monitoring The Functionality of Barangay Nutrition CouncilDocument1 pageMonitoring The Functionality of Barangay Nutrition CouncilJoseph VillafuerteNo ratings yet

- Office of The Sangguniang Barangay: Autonomous Region in Muslim Mindanao Municipality of Binidayan Barangay PicotaaanDocument7 pagesOffice of The Sangguniang Barangay: Autonomous Region in Muslim Mindanao Municipality of Binidayan Barangay PicotaaanAlianimamsampornaNo ratings yet

- GAD Accomplishment Report 2021Document16 pagesGAD Accomplishment Report 2021Edgar Sanchez EndozoNo ratings yet

- Irp New 2Document8 pagesIrp New 2Barangay CalliatNo ratings yet

- Annual Investment Program CY 2016Document125 pagesAnnual Investment Program CY 2016Carl100% (2)

- Barangay Budget PreparationDocument72 pagesBarangay Budget PreparationRjay's EscapadeNo ratings yet

- Steps in Crafting The SK Annual Budget 2020Document2 pagesSteps in Crafting The SK Annual Budget 2020Jaypee BucatcatNo ratings yet

- 2018 BDC Orientation Seminar Executive SummaryDocument8 pages2018 BDC Orientation Seminar Executive SummaryJerry CruzNo ratings yet

- Record of Estimated and Actual IncomeDocument14 pagesRecord of Estimated and Actual IncomeEdna Salvador LadieroNo ratings yet

- CSO SelectionDocument38 pagesCSO SelectionLindsey MarieNo ratings yet

- Barangay BudgetingDocument25 pagesBarangay BudgetingEarthAngel OrganicsNo ratings yet

- Citizens Charter PDFDocument343 pagesCitizens Charter PDFJunnieson BonielNo ratings yet

- Accounting Reports PreparationDocument23 pagesAccounting Reports Preparationcao.lilydawnfNo ratings yet

- Barangay Financial ManagementDocument40 pagesBarangay Financial ManagementAgnes FernandezNo ratings yet

- MEMO - AnnoucementDocument1 pageMEMO - AnnoucementMarliezel SardaNo ratings yet

- Public Policy Formulation SlidesDocument29 pagesPublic Policy Formulation SlidesMarliezel Sarda100% (1)

- Department of Budget and ManagementDocument2 pagesDepartment of Budget and ManagementMarliezel SardaNo ratings yet

- The ASEAN Economic CommunityDocument3 pagesThe ASEAN Economic CommunityMarliezel SardaNo ratings yet

- Corruption Affects Us AllDocument2 pagesCorruption Affects Us AllMarliezel SardaNo ratings yet

- Reaction Paper NO 1 - Martial Law (Final)Document7 pagesReaction Paper NO 1 - Martial Law (Final)Marliezel Sarda40% (5)

- Federalism Refers To The Mixed or Compound Mode of GovernmentDocument3 pagesFederalism Refers To The Mixed or Compound Mode of GovernmentMarliezel SardaNo ratings yet

- Jardine Davies vs. CaDocument2 pagesJardine Davies vs. CaMarliezel SardaNo ratings yet

- UOB Infinity User Guide (Admin and Services)Document39 pagesUOB Infinity User Guide (Admin and Services)TomNo ratings yet

- Chapter 2, Concept of MoneyDocument18 pagesChapter 2, Concept of Moneymiracle123No ratings yet

- Sugeeta Wifi BillDocument2 pagesSugeeta Wifi Billsachin.dudelaNo ratings yet

- Lesson 1 Cash and Cash EquivalentsDocument10 pagesLesson 1 Cash and Cash EquivalentsRica Lei N. DomingoNo ratings yet

- 187 State of Karnataka V Ecom Gill Coffee Trading PVT LTD 13 Mar 2023 463904Document7 pages187 State of Karnataka V Ecom Gill Coffee Trading PVT LTD 13 Mar 2023 463904Nithyananda N LNo ratings yet

- bANK mANAGEMENTDocument111 pagesbANK mANAGEMENTSwati SharmaNo ratings yet

- Maharashtra State Electricity Distribution Co. LTD.: For Any Queries On This Bill Please Contact MSEDCL CallDocument1 pageMaharashtra State Electricity Distribution Co. LTD.: For Any Queries On This Bill Please Contact MSEDCL Callkishor chandaliyaNo ratings yet

- TheProcure To PayCyclebyChristineDoxeyDocument6 pagesTheProcure To PayCyclebyChristineDoxeyrajus_cisa6423No ratings yet

- Total Statement SummaryDocument4 pagesTotal Statement SummaryIia AdvertisementsNo ratings yet

- COMLAW3 Module1 Negotiable Instruments Law A PrimerDocument21 pagesCOMLAW3 Module1 Negotiable Instruments Law A PrimerAccounting 201No ratings yet

- Interview Capsule For Ibps RRB Sbi Po Ibps Po Ibps So 2023Document19 pagesInterview Capsule For Ibps RRB Sbi Po Ibps Po Ibps So 2023z09y68dhptNo ratings yet

- LANDBANK Weaccess Terms and ConditionsDocument4 pagesLANDBANK Weaccess Terms and ConditionsSabang High School (Region IV-B - Oriental Mindoro)No ratings yet

- L Uk Proc Wfa030 JDC 001 Gwi Job Data ChangeDocument32 pagesL Uk Proc Wfa030 JDC 001 Gwi Job Data Changeعادل بشير بٹھNo ratings yet

- The Federal Reserve System: Its Purposes and Functions 1939Document33 pagesThe Federal Reserve System: Its Purposes and Functions 1939Trey Sells100% (1)

- Account Statement PDFDocument12 pagesAccount Statement PDFChetan TNNo ratings yet

- 2 - Important Case Laws Important Case Laws On The Negotiable Instruments Act - Sec.138 CasesDocument30 pages2 - Important Case Laws Important Case Laws On The Negotiable Instruments Act - Sec.138 CasesAshish DavessarNo ratings yet

- Final AccountsDocument12 pagesFinal AccountsXander Tabuzo100% (1)

- Easy Pay Slip PDFDocument1 pageEasy Pay Slip PDFChanchal SharmaNo ratings yet

- Job Profile PWD PDFDocument32 pagesJob Profile PWD PDFJitender KumarNo ratings yet

- 157a PDFDocument24 pages157a PDFmedia boxNo ratings yet

- Commercial BanksDocument7 pagesCommercial BanksMahealaniPerezNo ratings yet

- GST ChallanDocument2 pagesGST ChallanRonak PataniNo ratings yet

- Fargo ND Civil Asset RecordsDocument75 pagesFargo ND Civil Asset RecordsDustin GawrylowNo ratings yet

- Circular Memo On Online RoW Portal 03.09.2022Document39 pagesCircular Memo On Online RoW Portal 03.09.2022Special Cell VMCNo ratings yet

- Lesson 3Document3 pagesLesson 3Adrian MarfilNo ratings yet

- Bcoc 131Document5 pagesBcoc 131Anamika T AnilNo ratings yet

- Mas 12 Working Capital ManagementDocument11 pagesMas 12 Working Capital ManagementDexanne BulanNo ratings yet

- Far Quick Notes and Test Bank PDFDocument72 pagesFar Quick Notes and Test Bank PDFFujikoNo ratings yet