Download as txt, pdf, or txt

You might also like

- Hospital Supply Inc. - SolutionsDocument5 pagesHospital Supply Inc. - SolutionsMEERA JOSHY 192743650% (4)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 12Document34 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 12jasperkennedy078% (27)

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 11Document44 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 11jasperkennedy089% (28)

- Quiz 16Document7 pagesQuiz 16suranumiNo ratings yet

- Solution Manual - Chapter 3Document10 pagesSolution Manual - Chapter 3psrikanthmbaNo ratings yet

- Answers To Questions: Reflection Paper ON Hospital Supply SummaryDocument2 pagesAnswers To Questions: Reflection Paper ON Hospital Supply SummaryambrosiaeffectNo ratings yet

- Business School - Docx FinalDocument11 pagesBusiness School - Docx FinalMeletios LioulisNo ratings yet

- Hospital SupplyDocument3 pagesHospital SupplyJeanne Madrona100% (1)

- Marginal CostingDocument30 pagesMarginal Costinganon_3722476140% (1)

- Hospital Supply, IncDocument3 pagesHospital Supply, Incmade3875% (4)

- Man Acc 1Document6 pagesMan Acc 1Ange Buenaventura SalazarNo ratings yet

- Geronimo e - Assignment 2Document1 pageGeronimo e - Assignment 2Geronimo EnguitoNo ratings yet

- Case Study MANACODocument39 pagesCase Study MANACOAmorNo ratings yet

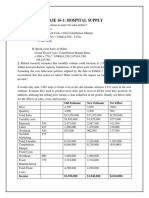

- Case 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Document6 pagesCase 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Lalit SapkaleNo ratings yet

- Cost - Direct Costing, CVP AnalysisDocument7 pagesCost - Direct Costing, CVP AnalysisAriMurdiyantoNo ratings yet

- Bill French - Write Up1Document10 pagesBill French - Write Up1Nina EllyanaNo ratings yet

- BEP AnalysisDocument7 pagesBEP Analysissumaya tasnimNo ratings yet

- Case Study 16-3 Bill FrenchDocument28 pagesCase Study 16-3 Bill FrenchShah 6020% (2)

- CVP, Variable Costing and Absorption CostingDocument7 pagesCVP, Variable Costing and Absorption CostingHannah Vaniza NapolesNo ratings yet

- Day 3Document33 pagesDay 3Leo ApilanNo ratings yet

- Case 16-1 (Alfi & Yessy)Document4 pagesCase 16-1 (Alfi & Yessy)Ana KristianaNo ratings yet

- Agenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingDocument33 pagesAgenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingApoorvNo ratings yet

- Hock CMA P1 2019 (Sections D & E) AnswersDocument9 pagesHock CMA P1 2019 (Sections D & E) AnswersNathan DrakeNo ratings yet

- Answers To QuestionsDocument8 pagesAnswers To QuestionsElie YabroudiNo ratings yet

- Chapter 2: Markets and Instruments: BD BD Ask BidDocument5 pagesChapter 2: Markets and Instruments: BD BD Ask BidSilviu Trebuian100% (1)

- Geronimoe - Assignment 1 & Assignment 2Document1 pageGeronimoe - Assignment 1 & Assignment 2Geronimo EnguitoNo ratings yet

- Seal 6 Esolutions CH 15Document56 pagesSeal 6 Esolutions CH 15Katlego MasibiNo ratings yet

- ESCOPETE Assignment CVPDocument6 pagesESCOPETE Assignment CVPmiljane perdizoNo ratings yet

- Institute of Certified General Accountants of Bangladesh (ICGAB) Performance Management (P13) LC-3: CVP AnalysisDocument5 pagesInstitute of Certified General Accountants of Bangladesh (ICGAB) Performance Management (P13) LC-3: CVP AnalysisMozid RahmanNo ratings yet

- Decsion Analysis Printing Hock ExamsuccessDocument92 pagesDecsion Analysis Printing Hock ExamsuccessJane Michelle EmanNo ratings yet

- Solution Manual Managerial Accounting Hansen Mowen 8th Editions CH 11Document44 pagesSolution Manual Managerial Accounting Hansen Mowen 8th Editions CH 11kkamjonginnNo ratings yet

- 2-Contribution Margin:: - WithDocument6 pages2-Contribution Margin:: - WithAlyn AlconeraNo ratings yet

- Chapter On CVP 2015 - Acc 2Document16 pagesChapter On CVP 2015 - Acc 2nur aqilah ridzuanNo ratings yet

- Sample Quiz On CVP - SolutionDocument2 pagesSample Quiz On CVP - Solutionmamasita25No ratings yet

- CVP CH One MDocument42 pagesCVP CH One MYonasNo ratings yet

- Absorption CostingDocument33 pagesAbsorption CostingMohit PaswanNo ratings yet

- Latihan UAS Manacc TUTORKU (Answered)Document10 pagesLatihan UAS Manacc TUTORKU (Answered)Della BianchiNo ratings yet

- Q1 AND Q4 (MCQS)Document3 pagesQ1 AND Q4 (MCQS)Maarij KhanNo ratings yet

- CH 03 SolDocument45 pagesCH 03 SolrocketamberNo ratings yet

- Chapter 17Document8 pagesChapter 17rahmiamelianazarNo ratings yet

- Cost BehaviorDocument17 pagesCost BehaviorRona Mae Ocampo ResareNo ratings yet

- COMA Mid Term - 2022-23 V1 - SolutionsDocument6 pagesCOMA Mid Term - 2022-23 V1 - SolutionssurajNo ratings yet

- CMA AK 1 AnswersDocument3 pagesCMA AK 1 Answersshahid yarNo ratings yet

- 2016 GMA711S Exam 2 MemoDocument8 pages2016 GMA711S Exam 2 MemoNolan TitusNo ratings yet

- CH 05Document28 pagesCH 05Rommel CruzNo ratings yet

- RCA Solutions Mod5Document5 pagesRCA Solutions Mod5Danica Austria DimalibotNo ratings yet

- MBA 504 Ch4 SolutionsDocument25 pagesMBA 504 Ch4 SolutionsPiyush JainNo ratings yet

- Implementation / Plan of Action:: Break-Even PointDocument1 pageImplementation / Plan of Action:: Break-Even PointMandeepkaur SandhuNo ratings yet

- Notes CVP 2009, 2017Document13 pagesNotes CVP 2009, 2017Aaron ForbesNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Summary of Austin Frakt & Mike Piper's Microeconomics Made SimpleFrom EverandSummary of Austin Frakt & Mike Piper's Microeconomics Made SimpleNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)