Download as pdf

You might also like

- Inspector General's LetterDocument18 pagesInspector General's LetterKatie AnthonyNo ratings yet

- Homework #3 TemplateDocument18 pagesHomework #3 TemplateAnthony ButlerNo ratings yet

- Healthcare Report Q1 2021Document75 pagesHealthcare Report Q1 2021Venkatraman KrishnamoorthyNo ratings yet

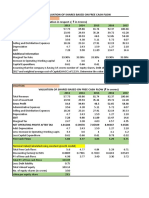

- 72 11 NAV Part 4 Share Prices AfterDocument75 pages72 11 NAV Part 4 Share Prices Aftercfang_2005No ratings yet

- 2014-7 Equity Yield Curve FinalDocument16 pages2014-7 Equity Yield Curve FinalLuke ConstableNo ratings yet

- Pershing Square 1Q17 Shareholder Letter May 11 2017 PSHDocument11 pagesPershing Square 1Q17 Shareholder Letter May 11 2017 PSHmarketfolly.comNo ratings yet

- Category Assumptions Name Category Price - Min. Price - Max. Volume Year 1Document6 pagesCategory Assumptions Name Category Price - Min. Price - Max. Volume Year 1Evert TrochNo ratings yet

- Map - by Counrty PercentDocument11 pagesMap - by Counrty PercentRupee Rudolf Lucy HaNo ratings yet

- Dossier Ossa Mineria EngDocument44 pagesDossier Ossa Mineria Engtoasterzapper100% (1)

- Mphasis: Performance HighlightsDocument13 pagesMphasis: Performance HighlightsAngel BrokingNo ratings yet

- DeNovo Quarterly Q2 2016Document48 pagesDeNovo Quarterly Q2 2016CrowdfundInsiderNo ratings yet

- BP Stats Review 2020 All DataDocument204 pagesBP Stats Review 2020 All DataAdriana FrancoNo ratings yet

- Jordan Telecom 04jan11Document26 pagesJordan Telecom 04jan11papuNo ratings yet

- European World-Class Results Are Close To Overall Results, But Fewer Top Performers On CostDocument35 pagesEuropean World-Class Results Are Close To Overall Results, But Fewer Top Performers On Costkapnau007No ratings yet

- The Iron Ore, Coal and Gas Sectors: Virginia Christie, Brad Mitchell, David Orsmond and Marileze Van ZylDocument8 pagesThe Iron Ore, Coal and Gas Sectors: Virginia Christie, Brad Mitchell, David Orsmond and Marileze Van ZylBatush MongoliaNo ratings yet

- 1-8-19 DoubleLine Just Markets WebcastDocument78 pages1-8-19 DoubleLine Just Markets WebcastZerohedge100% (5)

- Credit RatingDocument3 pagesCredit RatingAshish PoddarNo ratings yet

- BoozCo The Digital Future of Creative EuropeDocument48 pagesBoozCo The Digital Future of Creative EuropeIdomeneeNo ratings yet

- Wildcat 9 CHENDocument18 pagesWildcat 9 CHENitccpvfzkNo ratings yet

- 9-17-19 TR Presentation (9!16!19 Market Update) - UnlockedDocument58 pages9-17-19 TR Presentation (9!16!19 Market Update) - UnlockedZerohedge100% (3)

- Complete Financial ModelDocument47 pagesComplete Financial ModelArrush AhujaNo ratings yet

- TRIAL Palm Oil Financial Model v.1.0Document82 pagesTRIAL Palm Oil Financial Model v.1.0Maksa CuanNo ratings yet

- Bond Calculator TemplateDocument2 pagesBond Calculator Templatechintandesai20083112No ratings yet

- Reality Sinking in - Path To Recovery: GreeceDocument40 pagesReality Sinking in - Path To Recovery: GreeceRusMartinNo ratings yet

- Kruze Fin Model v8 11 SharedDocument69 pagesKruze Fin Model v8 11 SharedsergexNo ratings yet

- BOLT DCF ValuationDocument1 pageBOLT DCF ValuationOld School ValueNo ratings yet

- Alibaba IPO Financial Model WallstreetMojoDocument52 pagesAlibaba IPO Financial Model WallstreetMojoJulian HutabaratNo ratings yet

- Mekko Graphics Sample ChartsDocument47 pagesMekko Graphics Sample ChartsluizacoditaNo ratings yet

- Barclays-Infosys Ltd. - The Next Three Years PDFDocument17 pagesBarclays-Infosys Ltd. - The Next Three Years PDFProfitbytesNo ratings yet

- L&T 4Q Fy 2013Document15 pagesL&T 4Q Fy 2013Angel BrokingNo ratings yet

- Intrinsic and FCF ValuationDocument3 pagesIntrinsic and FCF ValuationSHISHIR RANANo ratings yet

- Eusprig 2015 CoralityDocument20 pagesEusprig 2015 CoralityserpepeNo ratings yet

- Bitcoin As A Monetary System: Examining Attention and AttendanceDocument115 pagesBitcoin As A Monetary System: Examining Attention and AttendanceJuan Paulo Moreno CrisostomoNo ratings yet

- Financial - Plan - KSK GlobalDocument13 pagesFinancial - Plan - KSK GlobalEvert TrochNo ratings yet

- Exercises LBODocument2 pagesExercises LBORafael Lizana ZúñigaNo ratings yet

- ChristophJanz SaaSCohortAnalysis21Document13 pagesChristophJanz SaaSCohortAnalysis21Diego SinayNo ratings yet

- Analysys Mason Due Diligence ExpertiseDocument9 pagesAnalysys Mason Due Diligence ExpertiseJessievanNo ratings yet

- Excel Financial SampelDocument123 pagesExcel Financial SampelaryNo ratings yet

- Q3 2017 - Investor LetterDocument5 pagesQ3 2017 - Investor Letterbillroberts981No ratings yet

- Resource-4a-BCG-The-Rise-of-the AI-Powered-Company-in-the-Postcrisis-World-Apr-2020 - tcm9-243435Document7 pagesResource-4a-BCG-The-Rise-of-the AI-Powered-Company-in-the-Postcrisis-World-Apr-2020 - tcm9-243435Koushali BanerjeeNo ratings yet

- LBO Valuation - Working File CV2Document5 pagesLBO Valuation - Working File CV2Ayushi GuptaNo ratings yet

- UKUnquote 448Document44 pagesUKUnquote 448Ithaka KafeneionNo ratings yet

- Funding Proposal Fp005 Acumen Kenya and RwandaDocument47 pagesFunding Proposal Fp005 Acumen Kenya and RwandaBreath WiltonNo ratings yet

- Investment Project Financial AnalysisDocument31 pagesInvestment Project Financial AnalysisBinus JoseNo ratings yet

- Mini Case Chapter 3 Final VersionDocument14 pagesMini Case Chapter 3 Final VersionAlberto MariñoNo ratings yet

- Synopsis of Many LandsDocument6 pagesSynopsis of Many Landsraj shekarNo ratings yet

- Invesco India Caterpillar Portfolio March 2018Document28 pagesInvesco India Caterpillar Portfolio March 2018Gokul SudhakaranNo ratings yet

- BM410-16 Equity Valuation 2 - Intrinsic Value 19oct05Document35 pagesBM410-16 Equity Valuation 2 - Intrinsic Value 19oct05muhammadanasmustafaNo ratings yet

- HP Analyst ReportDocument11 pagesHP Analyst Reportjoycechan879827No ratings yet

- Ame Research Thesis 11-13-2014Document890 pagesAme Research Thesis 11-13-2014ValueWalkNo ratings yet

- Afe Investor Presentation For The Quarter Ended 31 March 2019Document30 pagesAfe Investor Presentation For The Quarter Ended 31 March 2019Tarek DomiatyNo ratings yet

- Dabur Financial Modeling-Live Project.Document47 pagesDabur Financial Modeling-Live Project.rahul1094No ratings yet

- Project Secure Investment Summary September 2022Document1 pageProject Secure Investment Summary September 2022Satria MarthaniNo ratings yet

- TVS Motor DCF ModelDocument35 pagesTVS Motor DCF ModelPrabhdeep DadyalNo ratings yet

- Euro Themes - SpainDocument22 pagesEuro Themes - SpainGuy DviriNo ratings yet

- Accenture Gas Grows UpDocument32 pagesAccenture Gas Grows Upadibella77No ratings yet

- Cours 2 Essec 2018 Lbo PDFDocument81 pagesCours 2 Essec 2018 Lbo PDFmerag76668No ratings yet

- Crude Oil Report April 2011Document74 pagesCrude Oil Report April 2011Crude Oil TradeNo ratings yet

- May 2011Document82 pagesMay 2011MauriceNo ratings yet

- Short Term Energy Outlook: HighlightsDocument39 pagesShort Term Energy Outlook: HighlightswillywNo ratings yet

- Manila Bulletin, June 4, 2019, Pay Hike For Teachers Still A Promise PDFDocument2 pagesManila Bulletin, June 4, 2019, Pay Hike For Teachers Still A Promise PDFpribhor2No ratings yet

- Assignment #3 Hypothesis TestingDocument10 pagesAssignment #3 Hypothesis TestingJihen SmariNo ratings yet

- Criminal Complaint: United States v. Jack Eugene Carpenter IIIDocument7 pagesCriminal Complaint: United States v. Jack Eugene Carpenter IIIBen OrnerNo ratings yet

- La Carlota Sugar Central v. Jimenez GR L-12436, 31 May 1961 (2 SCRA 295) FactsDocument1 pageLa Carlota Sugar Central v. Jimenez GR L-12436, 31 May 1961 (2 SCRA 295) FactsAlyssa GuevarraNo ratings yet

- Environmental Problem in Urban LandscapeDocument22 pagesEnvironmental Problem in Urban LandscapekatherinewingettNo ratings yet

- Smart Meter Refusal LetterDocument1 pageSmart Meter Refusal Lettereditor9357No ratings yet

- Gradation ListDocument77 pagesGradation Listabhijeet0% (1)

- الإسلام المعاصر في فكر محمد إقبالDocument17 pagesالإسلام المعاصر في فكر محمد إقبالعطية الويشيNo ratings yet

- The Significance of Improving Intercultural Communicative Competence in Educational ProcessDocument3 pagesThe Significance of Improving Intercultural Communicative Competence in Educational ProcessEditor IJTSRDNo ratings yet

- Payment Card-Skimming Device InvestigationDocument21 pagesPayment Card-Skimming Device InvestigationernieNo ratings yet

- Creation of FacebookDocument39 pagesCreation of FacebookSwadesh BhattacharyaNo ratings yet

- Pakistan Studies Complete XIIDocument87 pagesPakistan Studies Complete XIIAbdan Khan100% (1)

- National Security-1Document4 pagesNational Security-1Gerly SayajonNo ratings yet

- Units: Muhammad AhsanDocument2 pagesUnits: Muhammad AhsanAreeb WaseemNo ratings yet

- BANAJIDocument1 pageBANAJISayati DasNo ratings yet

- Proc - 479 - 1994 Filipino Values MonthDocument1 pageProc - 479 - 1994 Filipino Values MonthAngel Mae PontilloNo ratings yet

- Untouchability and Mensuration PeriodDocument21 pagesUntouchability and Mensuration PeriodRadhika BudhaNo ratings yet

- Extemp Attention JokesDocument18 pagesExtemp Attention JokesElmer YangNo ratings yet

- Explanation RestrospectiveDocument9 pagesExplanation RestrospectiveHariharan SundaramNo ratings yet

- America Episode9 Guide FinDocument3 pagesAmerica Episode9 Guide FinEmilyNo ratings yet

- Wps Vs ScsDocument5 pagesWps Vs ScsRoselle LagamayoNo ratings yet

- Fu S-.FF Ift Q ('R T"-T (" K (S Q-A DTQ (Fu, Fi) Ffir'qr .Q. # Ffia Ftor Fi LTR Frffi'ft "" "FT"Document3 pagesFu S-.FF Ift Q ('R T"-T (" K (S Q-A DTQ (Fu, Fi) Ffir'qr .Q. # Ffia Ftor Fi LTR Frffi'ft "" "FT"tester mahesh25No ratings yet

- ICE Custody Classification GuidelinesDocument17 pagesICE Custody Classification GuidelinesGreg SaulmonNo ratings yet

- Florence Gallez, "A Proposal For A Code of Ethics For Collaborative Journalism in The Digital Age: The Open Park Code"Document300 pagesFlorence Gallez, "A Proposal For A Code of Ethics For Collaborative Journalism in The Digital Age: The Open Park Code"MIT Comparative Media Studies/WritingNo ratings yet

- Administrative Rules and RegulationsDocument3 pagesAdministrative Rules and RegulationsDonaldDeLeonNo ratings yet

- Macariola v. AsuncionDocument2 pagesMacariola v. AsuncionVanityHughNo ratings yet

- Lesson 2 Week 2 The Philippines in The 19th Century As Rizals Context by CSDDocument11 pagesLesson 2 Week 2 The Philippines in The 19th Century As Rizals Context by CSDMariel C. SegadorNo ratings yet

- 2NDQ Second Summative Test UcspDocument2 pages2NDQ Second Summative Test UcspJarven SaguinNo ratings yet

- Advance 7 Alp ProjectDocument11 pagesAdvance 7 Alp ProjectSharon Laurente RamónNo ratings yet