Download as pdf or txt

You might also like

- Aberrant d20 PDFDocument234 pagesAberrant d20 PDFlolcityNo ratings yet

- Daily Agri Report, March 12Document8 pagesDaily Agri Report, March 12Angel BrokingNo ratings yet

- Daily Agri Report, March 13Document8 pagesDaily Agri Report, March 13Angel BrokingNo ratings yet

- Daily Agri Report Oct 22Document8 pagesDaily Agri Report Oct 22Angel BrokingNo ratings yet

- Daily Agri Report Oct 11Document8 pagesDaily Agri Report Oct 11Angel BrokingNo ratings yet

- Daily Agri Report, March 25Document8 pagesDaily Agri Report, March 25Angel BrokingNo ratings yet

- Daily Agri Report, March 28Document8 pagesDaily Agri Report, March 28Angel BrokingNo ratings yet

- Daily Agri Report, August 16 2013Document9 pagesDaily Agri Report, August 16 2013Angel BrokingNo ratings yet

- Daily Agri Report, February 20Document8 pagesDaily Agri Report, February 20Angel BrokingNo ratings yet

- Daily Agri Report, May 17Document7 pagesDaily Agri Report, May 17Angel BrokingNo ratings yet

- Daily Agri Report 3rd JanDocument8 pagesDaily Agri Report 3rd JanAngel BrokingNo ratings yet

- Daily Agri Report, February 22Document8 pagesDaily Agri Report, February 22Angel BrokingNo ratings yet

- Daily Agri Report, May 07Document7 pagesDaily Agri Report, May 07Angel BrokingNo ratings yet

- Daily Agri Report Oct 23Document8 pagesDaily Agri Report Oct 23Angel BrokingNo ratings yet

- Daily Agri Report Nov 12Document8 pagesDaily Agri Report Nov 12Angel BrokingNo ratings yet

- Daily Agri Report, June 06Document7 pagesDaily Agri Report, June 06Angel BrokingNo ratings yet

- Daily Agri Report, March 18Document8 pagesDaily Agri Report, March 18Angel BrokingNo ratings yet

- Daily Agri Report, March 22Document8 pagesDaily Agri Report, March 22Angel BrokingNo ratings yet

- Daily Agri Report Aug 17Document8 pagesDaily Agri Report Aug 17Angel BrokingNo ratings yet

- Daily Agri Report, February 13Document8 pagesDaily Agri Report, February 13Angel BrokingNo ratings yet

- Daily Agri Report Nov 2Document8 pagesDaily Agri Report Nov 2Angel BrokingNo ratings yet

- Daily Agri Report, April 26Document8 pagesDaily Agri Report, April 26Angel BrokingNo ratings yet

- Daily Agri Report, February 18Document8 pagesDaily Agri Report, February 18Angel BrokingNo ratings yet

- Daily Agri Report, April 03Document8 pagesDaily Agri Report, April 03Angel BrokingNo ratings yet

- Daily Agri Report, May 30Document7 pagesDaily Agri Report, May 30Angel BrokingNo ratings yet

- Daily Agri Report 07 March 2013Document8 pagesDaily Agri Report 07 March 2013Angel BrokingNo ratings yet

- Daily Agri Report Nov 10Document8 pagesDaily Agri Report Nov 10Angel BrokingNo ratings yet

- Daily Agri Report, March 21Document8 pagesDaily Agri Report, March 21Angel BrokingNo ratings yet

- Daily Agri Report, May 09Document7 pagesDaily Agri Report, May 09Angel BrokingNo ratings yet

- Daily Agri Report Nov 21Document8 pagesDaily Agri Report Nov 21Angel BrokingNo ratings yet

- Daily Agri Report Nov 9Document8 pagesDaily Agri Report Nov 9Angel BrokingNo ratings yet

- Daily Agri Report Oct 29Document8 pagesDaily Agri Report Oct 29Angel BrokingNo ratings yet

- Daily Agri Report, March 04Document8 pagesDaily Agri Report, March 04Angel BrokingNo ratings yet

- Daily Agri Report, June 05Document7 pagesDaily Agri Report, June 05Angel BrokingNo ratings yet

- Daily Agri Report Nov 3Document8 pagesDaily Agri Report Nov 3Angel BrokingNo ratings yet

- Daily Agri Report, February 27Document8 pagesDaily Agri Report, February 27Angel BrokingNo ratings yet

- Daily Agri Report, March 14Document8 pagesDaily Agri Report, March 14Angel BrokingNo ratings yet

- Daily Agri Report, May 10Document7 pagesDaily Agri Report, May 10Angel BrokingNo ratings yet

- Daily Agri Report, February 23Document8 pagesDaily Agri Report, February 23Angel BrokingNo ratings yet

- Daily Agri Report, April 02Document8 pagesDaily Agri Report, April 02Angel BrokingNo ratings yet

- Daily Agri Report, March 23Document8 pagesDaily Agri Report, March 23Angel BrokingNo ratings yet

- Daily Agri Report, August 12 2013Document9 pagesDaily Agri Report, August 12 2013Angel BrokingNo ratings yet

- Daily Agri Report, May 16Document7 pagesDaily Agri Report, May 16Angel BrokingNo ratings yet

- Daily Agri Report Oct 27Document8 pagesDaily Agri Report Oct 27Angel BrokingNo ratings yet

- Daily Agri Report, June 12Document7 pagesDaily Agri Report, June 12Angel BrokingNo ratings yet

- Daily Agri Report, April 05Document8 pagesDaily Agri Report, April 05Angel BrokingNo ratings yet

- Daily Agri Report Nov 7Document8 pagesDaily Agri Report Nov 7Angel BrokingNo ratings yet

- Daily Agri Report, February 15Document8 pagesDaily Agri Report, February 15Angel BrokingNo ratings yet

- Daily Agri Report, May 08Document7 pagesDaily Agri Report, May 08Angel BrokingNo ratings yet

- Daily Agri Report, May 02Document8 pagesDaily Agri Report, May 02Angel BrokingNo ratings yet

- Daily Agri Report Nov 1Document8 pagesDaily Agri Report Nov 1Angel BrokingNo ratings yet

- Daily Agri Report, April 13Document8 pagesDaily Agri Report, April 13Angel BrokingNo ratings yet

- Daily Agri Report Nov 15Document8 pagesDaily Agri Report Nov 15Angel BrokingNo ratings yet

- Daily Agri Report, May 18Document7 pagesDaily Agri Report, May 18Angel BrokingNo ratings yet

- Daily Agri Report, February 19Document8 pagesDaily Agri Report, February 19Angel BrokingNo ratings yet

- Daily Agri Report Aug 24Document8 pagesDaily Agri Report Aug 24Angel BrokingNo ratings yet

- Daily Agri Report Sep 25Document8 pagesDaily Agri Report Sep 25Angel BrokingNo ratings yet

- Commodity Report September 2311 88240911Document8 pagesCommodity Report September 2311 88240911Abhinav JainNo ratings yet

- Daily Agri Report Oct 8Document8 pagesDaily Agri Report Oct 8Angel BrokingNo ratings yet

- Daily Agri Report Sep 6Document8 pagesDaily Agri Report Sep 6Angel BrokingNo ratings yet

- Pesticide & Agricultural Chemicals World Summary: Market Values & Financials by CountryFrom EverandPesticide & Agricultural Chemicals World Summary: Market Values & Financials by CountryNo ratings yet

- International Commodities Evening Update September 16 2013Document3 pagesInternational Commodities Evening Update September 16 2013Angel BrokingNo ratings yet

- Ranbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertDocument4 pagesRanbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertAngel BrokingNo ratings yet

- WPIInflation August2013Document5 pagesWPIInflation August2013Angel BrokingNo ratings yet

- Oilseeds and Edible Oil UpdateDocument9 pagesOilseeds and Edible Oil UpdateAngel BrokingNo ratings yet

- Daily Technical Report: Sensex (19733) / NIFTY (5851)Document4 pagesDaily Technical Report: Sensex (19733) / NIFTY (5851)Angel BrokingNo ratings yet

- Daily Agri Tech Report September 14 2013Document2 pagesDaily Agri Tech Report September 14 2013Angel BrokingNo ratings yet

- Daily Metals and Energy Report September 16 2013Document6 pagesDaily Metals and Energy Report September 16 2013Angel BrokingNo ratings yet

- Daily Agri Tech Report September 16 2013Document2 pagesDaily Agri Tech Report September 16 2013Angel BrokingNo ratings yet

- Daily Agri Report September 16 2013Document9 pagesDaily Agri Report September 16 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Currency Daily Report September 16 2013Document4 pagesCurrency Daily Report September 16 2013Angel BrokingNo ratings yet

- Tata Motors: Jaguar Land Rover - Monthly Sales UpdateDocument6 pagesTata Motors: Jaguar Land Rover - Monthly Sales UpdateAngel BrokingNo ratings yet

- Press Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressDocument1 pagePress Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressAngel BrokingNo ratings yet

- Derivatives Report 8th JanDocument3 pagesDerivatives Report 8th JanAngel BrokingNo ratings yet

- Daily Metals and Energy Report September 12 2013Document6 pagesDaily Metals and Energy Report September 12 2013Angel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 13Document2 pagesMetal and Energy Tech Report Sept 13Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Currency Daily Report September 13 2013Document4 pagesCurrency Daily Report September 13 2013Angel BrokingNo ratings yet

- Jaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechDocument4 pagesJaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechAngel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 12Document2 pagesMetal and Energy Tech Report Sept 12Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5913)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5913)Angel Broking100% (1)

- Daily Agri Report September 12 2013Document9 pagesDaily Agri Report September 12 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5897)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5897)Angel BrokingNo ratings yet

- Daily Agri Tech Report September 12 2013Document2 pagesDaily Agri Tech Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Currency Daily Report September 12 2013Document4 pagesCurrency Daily Report September 12 2013Angel BrokingNo ratings yet

- ANIMAL FREE Statement - Flowchart - Grotanol 3025Document2 pagesANIMAL FREE Statement - Flowchart - Grotanol 3025erwinyamashitaNo ratings yet

- Labor Variance: By: Group 2Document24 pagesLabor Variance: By: Group 2Kris BayronNo ratings yet

- Egyption Exchange InDexs PDFDocument3 pagesEgyption Exchange InDexs PDFMahmoudElbehairyNo ratings yet

- FALL 2020 INB 372 MID-Sec-4Document2 pagesFALL 2020 INB 372 MID-Sec-4ashraful islam shawonNo ratings yet

- The Sleeping Giant Wakes Up - Thirty Years After Reunification, Germany Is Shouldering More Responsibility - Leaders - The EconomistDocument6 pagesThe Sleeping Giant Wakes Up - Thirty Years After Reunification, Germany Is Shouldering More Responsibility - Leaders - The EconomistviniciusltNo ratings yet

- Bajaj Cae Study Mba KottayamDocument2 pagesBajaj Cae Study Mba KottayamRaginNo ratings yet

- Chapter 1-Introduction To Accounting and Business: True/FalseDocument3 pagesChapter 1-Introduction To Accounting and Business: True/FalseChloe Gabriel Evangeline ChaseNo ratings yet

- Premier Cement PDFDocument183 pagesPremier Cement PDFSor O RityNo ratings yet

- Five Forces AnalysisDocument5 pagesFive Forces Analysiswonderland123No ratings yet

- Unit 2 Writing About Graphs and TablesDocument70 pagesUnit 2 Writing About Graphs and TableshuytnNo ratings yet

- Notice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsDocument2 pagesNotice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsJustia.comNo ratings yet

- Schroder Dana Prestasi Gebyar Indonesia II MF IDENDocument1 pageSchroder Dana Prestasi Gebyar Indonesia II MF IDENJohanes SetiawanNo ratings yet

- The Role of Time Element in The DeterminationDocument9 pagesThe Role of Time Element in The DeterminationniranjanaNo ratings yet

- Bat Bep 2Document107 pagesBat Bep 2Imelda ElisabethNo ratings yet

- Schneider F DegrowthDocument8 pagesSchneider F DegrowthNatalia DueñasNo ratings yet

- Question 5Document2 pagesQuestion 5Sumit GoyalNo ratings yet

- Fertilizer TechnologyDocument6 pagesFertilizer TechnologySehjad khan BalochNo ratings yet

- Circular 23 2017Document2 pagesCircular 23 2017Singh SranNo ratings yet

- Rapid Reporting System (RRS) : Introduction To RRS For Lady Supervisors (LS)Document35 pagesRapid Reporting System (RRS) : Introduction To RRS For Lady Supervisors (LS)Vishnu VermaNo ratings yet

- Desk Review & Planning-SSDADocument5 pagesDesk Review & Planning-SSDARiya RoyNo ratings yet

- Indonesiacoalconcessionareaa31 140121094533 Phpapp02Document2 pagesIndonesiacoalconcessionareaa31 140121094533 Phpapp02Sean ChoiNo ratings yet

- Sujet 02-Isstn - 18051373Document4 pagesSujet 02-Isstn - 18051373Fadel AlimNo ratings yet

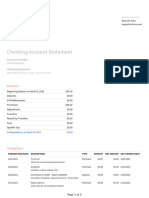

- Checking Account StatementDocument3 pagesChecking Account Statementandyspeers0No ratings yet

- Lumang Pera NG PilipinasDocument2 pagesLumang Pera NG PilipinasYeng100% (1)

- Tourism at The Crossroads Challenges To Developing Countries by The New World Trade OrderDocument69 pagesTourism at The Crossroads Challenges To Developing Countries by The New World Trade OrderEquitable Tourism Options (EQUATIONS)No ratings yet

- Annex 1B Child Mapping-TAGAS EditedDocument10 pagesAnnex 1B Child Mapping-TAGAS Editedalma agnasNo ratings yet

- Levy of Penal Charges On Non-Maintenance of Minimum Balances in Savings Bank AccountsDocument3 pagesLevy of Penal Charges On Non-Maintenance of Minimum Balances in Savings Bank AccountsVMKanetkarNo ratings yet

- 111Document7 pages111haerudinsaniNo ratings yet

- LimeRoad's-Suchi Mukherjee Talks About Building Brand Stickiness-Business Standard News PDFDocument8 pagesLimeRoad's-Suchi Mukherjee Talks About Building Brand Stickiness-Business Standard News PDFKanika SharmaNo ratings yet