Download as pdf or txt

You might also like

- Bookkeeping & Accounting For Small Business, 7th Ed PDFDocument190 pagesBookkeeping & Accounting For Small Business, 7th Ed PDFAhrian Bena100% (2)

- Lundolm & Sloan. Equity Valuation and Analysis With Eval. 3rd Edition CHP 01Document5 pagesLundolm & Sloan. Equity Valuation and Analysis With Eval. 3rd Edition CHP 01Peter Pa N0% (1)

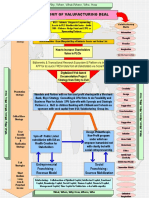

- ANATOMY OF Valufacturing Deal .Document26 pagesANATOMY OF Valufacturing Deal .BabarNo ratings yet

- Week 4 Activity Identify The Element of Financial StatementDocument2 pagesWeek 4 Activity Identify The Element of Financial StatementMarlyn Lotivio100% (1)

- Market Outlook: Dealer's DiaryDocument24 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 24th January 2012Document12 pagesMarket Outlook 24th January 2012Angel BrokingNo ratings yet

- Market Outlook 15th JanDocument17 pagesMarket Outlook 15th JanAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 16th March 2012Document4 pagesMarket Outlook 16th March 2012Angel BrokingNo ratings yet

- Market Outlook Report, 22nd JanuaryDocument16 pagesMarket Outlook Report, 22nd JanuaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 16th September 2011Document6 pagesMarket Outlook 16th September 2011Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 12th March 2012Document4 pagesMarket Outlook 12th March 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 5th October 2011Document4 pagesMarket Outlook 5th October 2011Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument21 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 28th January 2013Document17 pagesMarket Outlook, 28th January 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 15th February 2013Document19 pagesMarket Outlook, 15th February 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 1st February 2013Document20 pagesMarket Outlook, 1st February 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Week Ended September 21, 2012: Icici Amc Idfc Amc Icici BankDocument4 pagesWeek Ended September 21, 2012: Icici Amc Idfc Amc Icici BankBonthala BadrNo ratings yet

- Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 21st February, 2013Document14 pagesMarket Outlook, 21st February, 2013Angel BrokingNo ratings yet

- Market Outlook 1st March 2012Document4 pagesMarket Outlook 1st March 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 21st February 2012Document4 pagesMarket Outlook 21st February 2012Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 26th December 2011Document4 pagesMarket Outlook 26th December 2011Angel BrokingNo ratings yet

- Market Outlook 20th March 2012Document3 pagesMarket Outlook 20th March 2012Angel BrokingNo ratings yet

- Market Outlook 23rd February 2012Document4 pagesMarket Outlook 23rd February 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 30th Decmber 2011Document3 pagesMarket Outlook 30th Decmber 2011Angel BrokingNo ratings yet

- Market Outlook 31st January 2012Document10 pagesMarket Outlook 31st January 2012Angel BrokingNo ratings yet

- Fag 3qcy2012ruDocument6 pagesFag 3qcy2012ruAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryangelbrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Report, 21st JanuaryDocument9 pagesMarket Outlook Report, 21st JanuaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Reliance Single PremiumDocument80 pagesReliance Single Premiumsumitkumarnawadia22No ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 13th February 2012Document9 pagesMarket Outlook 13th February 2012Angel BrokingNo ratings yet

- Market Outlook 3rd May 2012Document13 pagesMarket Outlook 3rd May 2012Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 20th January 2012Document11 pagesMarket Outlook 20th January 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument11 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- India Equity Analytics Today: Hold Rating On Prestige Estates StockDocument25 pagesIndia Equity Analytics Today: Hold Rating On Prestige Estates StockNarnolia Securities LimitedNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument4 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 6th February 2012Document7 pagesMarket Outlook 6th February 2012Angel BrokingNo ratings yet

- Ranbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertDocument4 pagesRanbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertAngel BrokingNo ratings yet

- Daily Agri Tech Report September 16 2013Document2 pagesDaily Agri Tech Report September 16 2013Angel BrokingNo ratings yet

- Daily Agri Tech Report September 14 2013Document2 pagesDaily Agri Tech Report September 14 2013Angel BrokingNo ratings yet

- Currency Daily Report September 13 2013Document4 pagesCurrency Daily Report September 13 2013Angel BrokingNo ratings yet

- WPIInflation August2013Document5 pagesWPIInflation August2013Angel BrokingNo ratings yet

- Daily Metals and Energy Report September 16 2013Document6 pagesDaily Metals and Energy Report September 16 2013Angel BrokingNo ratings yet

- Oilseeds and Edible Oil UpdateDocument9 pagesOilseeds and Edible Oil UpdateAngel BrokingNo ratings yet

- International Commodities Evening Update September 16 2013Document3 pagesInternational Commodities Evening Update September 16 2013Angel BrokingNo ratings yet

- Derivatives Report 8th JanDocument3 pagesDerivatives Report 8th JanAngel BrokingNo ratings yet

- Daily Agri Report September 16 2013Document9 pagesDaily Agri Report September 16 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Daily Metals and Energy Report September 12 2013Document6 pagesDaily Metals and Energy Report September 12 2013Angel BrokingNo ratings yet

- Currency Daily Report September 16 2013Document4 pagesCurrency Daily Report September 16 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19733) / NIFTY (5851)Document4 pagesDaily Technical Report: Sensex (19733) / NIFTY (5851)Angel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 13Document2 pagesMetal and Energy Tech Report Sept 13Angel BrokingNo ratings yet

- Jaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechDocument4 pagesJaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechAngel BrokingNo ratings yet

- Press Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressDocument1 pagePress Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressAngel BrokingNo ratings yet

- Tata Motors: Jaguar Land Rover - Monthly Sales UpdateDocument6 pagesTata Motors: Jaguar Land Rover - Monthly Sales UpdateAngel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 12Document2 pagesMetal and Energy Tech Report Sept 12Angel BrokingNo ratings yet

- Daily Agri Report September 12 2013Document9 pagesDaily Agri Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5913)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5913)Angel Broking100% (1)

- Daily Technical Report: Sensex (19997) / NIFTY (5897)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5897)Angel BrokingNo ratings yet

- Daily Agri Tech Report September 12 2013Document2 pagesDaily Agri Tech Report September 12 2013Angel BrokingNo ratings yet

- Currency Daily Report September 12 2013Document4 pagesCurrency Daily Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Final Summer Internship Project NBFC Sector.Document78 pagesFinal Summer Internship Project NBFC Sector.avinash singhNo ratings yet

- Pre-Feasibility Study: Social Media Marketing AgencyDocument21 pagesPre-Feasibility Study: Social Media Marketing AgencyNauman QureshiNo ratings yet

- ZackDocument1 pageZackrajj96101No ratings yet

- Q2 FY22 Financial TablesDocument13 pagesQ2 FY22 Financial TablesDennis AngNo ratings yet

- Lease Purchase AgreementDocument2 pagesLease Purchase AgreementmuparutsaNo ratings yet

- Amway Business OpportunityDocument18 pagesAmway Business OpportunityDinabandhu PatraNo ratings yet

- Itr-1 Sahaj Individual Income Tax Return: Part A General InformationDocument5 pagesItr-1 Sahaj Individual Income Tax Return: Part A General Informationrajesh kumar sharmaNo ratings yet

- Chapter 4 - 150822Document31 pagesChapter 4 - 150822ndiem1402No ratings yet

- Every StepDocument9 pagesEvery StepNatalie MudavanhuNo ratings yet

- Swot Analysis of Pension Schemes Administration in Selected African CountriesDocument5 pagesSwot Analysis of Pension Schemes Administration in Selected African CountriesrushidNo ratings yet

- Kusum Gupta v. ITO (Delhi HC)Document6 pagesKusum Gupta v. ITO (Delhi HC)Avar LambaNo ratings yet

- CIBC International Student Banking Offer: Payment InstructionsDocument1 pageCIBC International Student Banking Offer: Payment InstructionsCL-A-11 KUNAL BHOSALENo ratings yet

- Cross-Border Insurance in Nigeria - A Legal Impossibility?Document4 pagesCross-Border Insurance in Nigeria - A Legal Impossibility?odoemenam chidiNo ratings yet

- General Banking Law of 2000 OutlineDocument3 pagesGeneral Banking Law of 2000 OutlineDence Cris RondonNo ratings yet

- Mitsubishi Electric Annual ReportDocument21 pagesMitsubishi Electric Annual ReportAbhinavHarshalNo ratings yet

- IAS 16 PPE NotesDocument3 pagesIAS 16 PPE NotesKatreena Mae Constantino100% (2)

- Chapter - 1: LancoDocument97 pagesChapter - 1: LancotysontrivNo ratings yet

- Aud Prob ReceivablesDocument13 pagesAud Prob ReceivablesMary Joanne Tapia0% (1)

- Abstract: The Aim of The Research Is To Shed Light On The Accounting System in Iraq and ToDocument23 pagesAbstract: The Aim of The Research Is To Shed Light On The Accounting System in Iraq and Toفاطمه عبدالسلام عبودNo ratings yet

- Khadi & Village Industries Commission Project Profile For Gramodyog Rozgar Yojana PlumbingDocument2 pagesKhadi & Village Industries Commission Project Profile For Gramodyog Rozgar Yojana PlumbingMohammed Mohsin YedavalliNo ratings yet

- Key Highlights of Simplified Form GSTR 9 and Form GSTR 9c PDFDocument2 pagesKey Highlights of Simplified Form GSTR 9 and Form GSTR 9c PDFPriyanka BahiratNo ratings yet

- The Indian Capital Market - An Overview: Chapter-1 Gagandeep SinghDocument45 pagesThe Indian Capital Market - An Overview: Chapter-1 Gagandeep SinghgaganNo ratings yet

- Republic vs. MeralcoDocument11 pagesRepublic vs. MeralcoIvy ZaldarriagaNo ratings yet

- Post Graduate Diploma in Business Administration Programme CurriculumDocument33 pagesPost Graduate Diploma in Business Administration Programme CurriculumMicky StarNo ratings yet

- 21.doctrine of Ultra ViresDocument4 pages21.doctrine of Ultra ViresAgam GoelNo ratings yet

- Entrepreneurship (Module 6)Document17 pagesEntrepreneurship (Module 6)prasenjit00750% (4)