Download as docx, pdf, or txt

You might also like

- Homework 1 LABREVDocument6 pagesHomework 1 LABREVBrigette DomingoNo ratings yet

- A Khutbah On Warning of DesiresDocument16 pagesA Khutbah On Warning of DesiresMountainofknowledge100% (1)

- Supplemental Notes - Being Faithful in A Faithless World - 00 - Chuck MisslerDocument13 pagesSupplemental Notes - Being Faithful in A Faithless World - 00 - Chuck Misslerapi-3735674100% (1)

- Biong Making Sense of The PastDocument9 pagesBiong Making Sense of The PastCarlo Biong100% (5)

- GM KPSC QCDocument40 pagesGM KPSC QCMahendra M100% (1)

- Social Economic ZoneDocument3 pagesSocial Economic ZoneRakesh Raj SinghaniayaNo ratings yet

- Special Economic ZoneDocument1 pageSpecial Economic ZoneJananee RajagopalanNo ratings yet

- Monday, October 19, 2009Document12 pagesMonday, October 19, 2009Vaibhav 761No ratings yet

- SEZDocument22 pagesSEZSonali SharmaNo ratings yet

- SEZ PolicyDocument30 pagesSEZ PolicyKushal UpadhyayaNo ratings yet

- SEZ PresentationDocument18 pagesSEZ Presentationvinunair79No ratings yet

- Special Economic ZoneDocument16 pagesSpecial Economic ZoneEsheeta KainthlaNo ratings yet

- Seminars On General Topics: Sez and Its Effect On The EconomyDocument21 pagesSeminars On General Topics: Sez and Its Effect On The EconomyLubna ShaikhNo ratings yet

- Understanding SEZ and Its Implications: The Inception of The Special Economic Zones (SEZ) in India Was Done byDocument8 pagesUnderstanding SEZ and Its Implications: The Inception of The Special Economic Zones (SEZ) in India Was Done byDeepika PrakashNo ratings yet

- There Are 13 Functional Sezs and About 61 Sezs, Which Have Been Approved and Are Under The Process of Establishment in IndiaDocument6 pagesThere Are 13 Functional Sezs and About 61 Sezs, Which Have Been Approved and Are Under The Process of Establishment in IndiaShifa Kunal GuptaNo ratings yet

- Performance and Policies Vishal Sarin LHSBDocument20 pagesPerformance and Policies Vishal Sarin LHSBAnoop KularNo ratings yet

- Special Economic ZonesDocument3 pagesSpecial Economic ZonesSarath Kumar ReddyNo ratings yet

- Development With Special Emphasis On SEZ: Need, Performance and Government Strategy For InfrastructuralDocument5 pagesDevelopment With Special Emphasis On SEZ: Need, Performance and Government Strategy For InfrastructuralSimran SimieNo ratings yet

- Special Economic Zone (SEZ)Document27 pagesSpecial Economic Zone (SEZ)ChunnuriNo ratings yet

- Special Economic Zone - DefinitionDocument4 pagesSpecial Economic Zone - Definitionaastha vermaNo ratings yet

- Sez ActDocument5 pagesSez ActTapasya KabraNo ratings yet

- A Special Economic ZoneDocument8 pagesA Special Economic ZonetukunadhalNo ratings yet

- Sezs Indirect Tax Implicationsof Special Economic ZonesiDocument6 pagesSezs Indirect Tax Implicationsof Special Economic ZonesiVijay Srinivas KukkalaNo ratings yet

- Introduction and HistoryDocument9 pagesIntroduction and Historyvidit1789No ratings yet

- SEZ Notes - ManagementParadise - Com - Your MBA Online Degree Program and Management Students Forum For MBA, BMS, MMS, BMM, BBA, Students & AspirantsDocument5 pagesSEZ Notes - ManagementParadise - Com - Your MBA Online Degree Program and Management Students Forum For MBA, BMS, MMS, BMM, BBA, Students & AspirantsVinod WaghelaNo ratings yet

- Indian Sez ModelsDocument24 pagesIndian Sez ModelsAnuja BakareNo ratings yet

- Introduction - Facilities and Incentives - Export Performances - Operational Sezs in India - Approved Sezs in IndiaDocument10 pagesIntroduction - Facilities and Incentives - Export Performances - Operational Sezs in India - Approved Sezs in IndiaArti SharmaNo ratings yet

- Special Economic ZoneDocument9 pagesSpecial Economic ZoneGïŘï Yadav RasthaNo ratings yet

- GST Implication On Special Economic Zones With Focus On IT SectorDocument4 pagesGST Implication On Special Economic Zones With Focus On IT Sectoryogeshshukla.ys14No ratings yet

- Special Economic Zone: An Overview of The Sez ACT, 2005Document10 pagesSpecial Economic Zone: An Overview of The Sez ACT, 2005sreedevi sureshNo ratings yet

- The Main Objectives of The SEZ Act AreDocument4 pagesThe Main Objectives of The SEZ Act AreParag YadavNo ratings yet

- SEZ Notes - February 18th, 2009: DegreeDocument5 pagesSEZ Notes - February 18th, 2009: DegreeZofail HassanNo ratings yet

- Imm Work Final 2013Document67 pagesImm Work Final 2013Keyur BhojakNo ratings yet

- Who Can Set Up Sezs? Can Foreign Companies Set Up Sezs?: Basic Difference Between Epzs and SezsDocument7 pagesWho Can Set Up Sezs? Can Foreign Companies Set Up Sezs?: Basic Difference Between Epzs and SezsMohan SubramanianNo ratings yet

- Research Paper On SEZDocument6 pagesResearch Paper On SEZyogeshshukla.ys14No ratings yet

- Naaannnsssiii IiiibbbbDocument3 pagesNaaannnsssiii IiiibbbbMahalakshmi RavikumarNo ratings yet

- Revised SEZ PolicyDocument11 pagesRevised SEZ PolicyM R GUHANNo ratings yet

- Special Economic ZonesDocument4 pagesSpecial Economic ZonesLalithya Sannitha MeesalaNo ratings yet

- The Current Status of SEZ, India: S. Chandrachud, Dr. N. GajalakshmiDocument3 pagesThe Current Status of SEZ, India: S. Chandrachud, Dr. N. GajalakshmiManisha TiwariNo ratings yet

- Taxation Customs Labour Regulations Tax HolidaysDocument2 pagesTaxation Customs Labour Regulations Tax HolidaysAashita mittalNo ratings yet

- Meaning and Definition of Special Economic ZoneDocument12 pagesMeaning and Definition of Special Economic ZoneMubina shaikhNo ratings yet

- Export Promotion Zone/Special Economic Zone (Epz/Sez) & Export Oriented Units (EOU)Document17 pagesExport Promotion Zone/Special Economic Zone (Epz/Sez) & Export Oriented Units (EOU)sakshiNo ratings yet

- The Current Status of SEZ, India: S. Chandrachud, Dr. N. GajalakshmiDocument10 pagesThe Current Status of SEZ, India: S. Chandrachud, Dr. N. GajalakshmiInternational Organization of Scientific Research (IOSR)No ratings yet

- Project Report - BepDocument11 pagesProject Report - Bepstudyy bossNo ratings yet

- Normative Analyses of Investment Incentive in EthiopiaDocument6 pagesNormative Analyses of Investment Incentive in EthiopiaBelay MekuanintNo ratings yet

- SEZ ActDocument2 pagesSEZ ActD Attitude KidNo ratings yet

- Special Economic Zones (Sez)Document3 pagesSpecial Economic Zones (Sez)kunalagrey.milsNo ratings yet

- Presentation On SEZ Concept in IndiaDocument12 pagesPresentation On SEZ Concept in IndiaVishal TrivediNo ratings yet

- Special Economic Zones in IndiaDocument23 pagesSpecial Economic Zones in IndiaJey AnandNo ratings yet

- Special Economic Zones (SEZ)Document12 pagesSpecial Economic Zones (SEZ)Ajay K PandianNo ratings yet

- Special Economic Zones (SEZ) - IntroductionDocument23 pagesSpecial Economic Zones (SEZ) - IntroductionR. SainiNo ratings yet

- Project Report On SEZDocument24 pagesProject Report On SEZanandsabbani92% (12)

- Special Economic ZoneDocument13 pagesSpecial Economic Zonejoe80% (5)

- Taxx Special Economic ZonesDocument4 pagesTaxx Special Economic ZonesAlina RizviNo ratings yet

- Special Economic ZonesDocument10 pagesSpecial Economic ZonesPranay Manikanta JainiNo ratings yet

- Special Economic ZoneDocument27 pagesSpecial Economic ZonehaphuNo ratings yet

- Sez Act 2005Document20 pagesSez Act 2005ravie2009No ratings yet

- Special Economic Zones: A Brief Study OFDocument23 pagesSpecial Economic Zones: A Brief Study OFShailesh BansalNo ratings yet

- SEZFacilities IncentivesDocument1 pageSEZFacilities IncentivesNitin JadavNo ratings yet

- Sez PDFDocument6 pagesSez PDFdilip5685No ratings yet

- A Special Economic ZoneDocument12 pagesA Special Economic ZoneVlad SemenovNo ratings yet

- Role of Special Economic Zone in Strategic Plannnig For Business Unit EstablishmentDocument25 pagesRole of Special Economic Zone in Strategic Plannnig For Business Unit EstablishmentShiv RajNo ratings yet

- Special Economic Zone Special Economic Zone Special Economic Zone Special Economic ZoneDocument13 pagesSpecial Economic Zone Special Economic Zone Special Economic Zone Special Economic ZoneXMBA 24 ITM VashiNo ratings yet

- Acccounting Concepts and ConvetionsDocument4 pagesAcccounting Concepts and ConvetionsShIva Leela ChoUdaryNo ratings yet

- Fin RPT ViewerDocument22 pagesFin RPT ViewerShIva Leela ChoUdaryNo ratings yet

- Nuclear Catastrophes: International Nuclear Event ScaleDocument2 pagesNuclear Catastrophes: International Nuclear Event ScaleShIva Leela ChoUdaryNo ratings yet

- Merger:: BusinessDocument4 pagesMerger:: BusinessShIva Leela ChoUdaryNo ratings yet

- Finalsied Practicum of 3Document56 pagesFinalsied Practicum of 3ShIva Leela ChoUdaryNo ratings yet

- Climate Change: TH TH THDocument9 pagesClimate Change: TH TH THShIva Leela ChoUdaryNo ratings yet

- Project of Surya FoodsDocument56 pagesProject of Surya FoodsShIva Leela ChoUdary50% (2)

- Institutional Setups For Export Promotions: Agricultural and Processed Food Products Export Development Authority (APEDA)Document26 pagesInstitutional Setups For Export Promotions: Agricultural and Processed Food Products Export Development Authority (APEDA)ShIva Leela ChoUdaryNo ratings yet

- A Report: Ndia Urkey ElationsDocument16 pagesA Report: Ndia Urkey ElationsShIva Leela ChoUdaryNo ratings yet

- Trump Trial Date SetDocument6 pagesTrump Trial Date SetPeter BurkeNo ratings yet

- Commissioner of Internal Revenue Vs CoaDocument4 pagesCommissioner of Internal Revenue Vs CoaAb Castil100% (1)

- Quarterly Percentage Tax Rates Table: Taxable Base Tax RateDocument4 pagesQuarterly Percentage Tax Rates Table: Taxable Base Tax RateKathrine CruzNo ratings yet

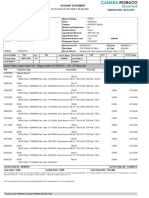

- Canara Robeco Equity Hybrid Fund - Regular Monthly IDCW (GBDP) - ISIN: INF760K01068Document2 pagesCanara Robeco Equity Hybrid Fund - Regular Monthly IDCW (GBDP) - ISIN: INF760K01068brotoNo ratings yet

- Account Opening Agreement FormDocument7 pagesAccount Opening Agreement FormSajad AhmadNo ratings yet

- In Re BalumaDocument1 pageIn Re BalumaCaitlin KintanarNo ratings yet

- 12.6% P.A. Quarterly Conditional Coupon With Memory Effect - European Barrier at 60% - 1 Year and 3 Months - EURDocument1 page12.6% P.A. Quarterly Conditional Coupon With Memory Effect - European Barrier at 60% - 1 Year and 3 Months - EURapi-25889552No ratings yet

- Ecclesiastes Study GuideDocument13 pagesEcclesiastes Study GuideJosh McKibbenNo ratings yet

- P38 - Calculation of Damages For Loss - TortDocument12 pagesP38 - Calculation of Damages For Loss - TortNBT OONo ratings yet

- Articles of Incorporation of Stock CorporationDocument4 pagesArticles of Incorporation of Stock CorporationInnoKalNo ratings yet

- Employement AgreementDocument4 pagesEmployement AgreementVipin202020No ratings yet

- Narrative Report On NCST CultureDocument8 pagesNarrative Report On NCST CultureVarenLagartoNo ratings yet

- Mmodule 5 Segment 1 Dispute ResolutionDocument3 pagesMmodule 5 Segment 1 Dispute ResolutionBALANGAT, Mc RhannelNo ratings yet

- UNETHICALDocument12 pagesUNETHICALalyssa babylaiNo ratings yet

- UA5000 Hardware Description Manual PDFDocument377 pagesUA5000 Hardware Description Manual PDFYunes Hasan Ahmed Ali100% (2)

- Regolamento Delegato (UE) 574 - 2014Document6 pagesRegolamento Delegato (UE) 574 - 2014c_passerino6572No ratings yet

- People V JalosjosDocument4 pagesPeople V JalosjosChad Osorio100% (2)

- Law of Obligations and ContractsDocument31 pagesLaw of Obligations and Contractscolleenyu100% (1)

- CM-S-004 I01 Composite Materials Shared Databases - KopieDocument9 pagesCM-S-004 I01 Composite Materials Shared Databases - KopieriversgardenNo ratings yet

- Application ModificationDocument7 pagesApplication Modificationnarender707463No ratings yet

- De Jesus Vs COADocument1 pageDe Jesus Vs COAMac100% (1)

- MANACCOGUIDEDocument4 pagesMANACCOGUIDEhcimtdNo ratings yet

- Soft Token Application FormDocument1 pageSoft Token Application FormAnnamalai TNo ratings yet

- South Sudan Overview of Corruption and Anti-Corruption EffortsDocument24 pagesSouth Sudan Overview of Corruption and Anti-Corruption Effortsjonnybilek2112No ratings yet

- Madison College Extenuating CircumstanceDocument3 pagesMadison College Extenuating CircumstanceMindy ThomasNo ratings yet