Download as pdf or txt

You might also like

- 10000006242Document31 pages10000006242Chapter 11 DocketsNo ratings yet

- Defence - RedactedDocument15 pagesDefence - RedactedAdam Ha100% (1)

- Amadora V CADocument3 pagesAmadora V CAEmir MendozaNo ratings yet

- Exhibit 11BDocument25 pagesExhibit 11BOSDocs2012No ratings yet

- Exhibit 19GDocument3 pagesExhibit 19GOSDocs2012No ratings yet

- BP Gulf Oil Spill Settlement - IntroductionDocument46 pagesBP Gulf Oil Spill Settlement - IntroductionGeorge ConkNo ratings yet

- 8963 37Document30 pages8963 37OSDocs2012No ratings yet

- HĐ Cif, Purchase - IccDocument12 pagesHĐ Cif, Purchase - IccLiên TháiNo ratings yet

- Exhibit 18JDocument23 pagesExhibit 18JOSDocs2012No ratings yet

- Exhibit 19HDocument7 pagesExhibit 19HOSDocs2012No ratings yet

- #119914 V2 - Mti NotcredappempcorporaterecoveryDocument6 pages#119914 V2 - Mti NotcredappempcorporaterecoveryChapter 11 DocketsNo ratings yet

- Exhibit 07BDocument14 pagesExhibit 07BOSDocs2012No ratings yet

- Motion For Preliminary InjunctionDocument14 pagesMotion For Preliminary InjunctionOSDocs2012No ratings yet

- Compromise Settlements and Technical Write-OffsDocument5 pagesCompromise Settlements and Technical Write-OffsSaurabh MalooNo ratings yet

- Financial Rehabilitation & Insolvent Act of 2010 or FRIA (RA 10142), Sec. 2 Id., Sec. 3Document55 pagesFinancial Rehabilitation & Insolvent Act of 2010 or FRIA (RA 10142), Sec. 2 Id., Sec. 3Amvigatun to MacottorNo ratings yet

- Et Af.,iDocument22 pagesEt Af.,iChapter 11 DocketsNo ratings yet

- 3424 Carson Street, Suite 350: " Central District of CaliforniaDocument76 pages3424 Carson Street, Suite 350: " Central District of CaliforniaChapter 11 DocketsNo ratings yet

- Week 3Document23 pagesWeek 3Brian Dean100% (2)

- Attorneys For Midland Loan Services, Inc.: Limited Objection To Motion To Approve Fee Procedures Page 1 of 6 F-283676Document6 pagesAttorneys For Midland Loan Services, Inc.: Limited Objection To Motion To Approve Fee Procedures Page 1 of 6 F-283676Chapter 11 DocketsNo ratings yet

- 2019 Supreme Court Cases Involving The COMMISSION On AUDITDocument376 pages2019 Supreme Court Cases Involving The COMMISSION On AUDITLiane V.No ratings yet

- 15b. Appendix 2 - Brent Council Debt Write-Off ProcedureDocument8 pages15b. Appendix 2 - Brent Council Debt Write-Off ProcedureGere TassewNo ratings yet

- Claim Form - Marine Inland Policy-ICICIDocument15 pagesClaim Form - Marine Inland Policy-ICICImib_santoshNo ratings yet

- 8963 36Document37 pages8963 36OSDocs2012No ratings yet

- Gulf Coast Claims Facility: November 30, 2011Document8 pagesGulf Coast Claims Facility: November 30, 2011Michael AllenNo ratings yet

- 2019 Supreme Court Cases Involving The COMMISSION On AUDITDocument376 pages2019 Supreme Court Cases Involving The COMMISSION On AUDITLiane V.No ratings yet

- Home DepotDocument74 pagesHome Depotjeff_roberts881100% (2)

- Insolvency and Bankruptcy Code 2016Document4 pagesInsolvency and Bankruptcy Code 2016Tanima SoodNo ratings yet

- Philex Mining Vs CIR G.R. No. 148187Document26 pagesPhilex Mining Vs CIR G.R. No. 148187crizaldedNo ratings yet

- 10000000736Document94 pages10000000736Chapter 11 DocketsNo ratings yet

- BIMCO Circular On Chater Party Guarantee PDFDocument4 pagesBIMCO Circular On Chater Party Guarantee PDFmohammadbadrifarNo ratings yet

- Week - 1 FRIA EditedDocument106 pagesWeek - 1 FRIA EditedjemalynjoshlynNo ratings yet

- Premium Finance Agreement An GratingDocument18 pagesPremium Finance Agreement An GratingChapter 11 DocketsNo ratings yet

- Provisions, Contingent Liabilities and Contingent Assets: By:-Yohannes NegatuDocument52 pagesProvisions, Contingent Liabilities and Contingent Assets: By:-Yohannes NegatuEshetie Mekonene AmareNo ratings yet

- Sale Procedures Hearing Date: October 23, 2008 at 1:30 P.M. Sale Procedures Objection Deadline: October 22, 2008 at 4:00 P.M. Related Docket Nos. 620, 621Document20 pagesSale Procedures Hearing Date: October 23, 2008 at 1:30 P.M. Sale Procedures Objection Deadline: October 22, 2008 at 4:00 P.M. Related Docket Nos. 620, 621Chapter 11 DocketsNo ratings yet

- Loss ExpenseDocument10 pagesLoss ExpensefuzahjamilNo ratings yet

- Central Bank of Bahrain Volume 3-Insurance PART BDocument26 pagesCentral Bank of Bahrain Volume 3-Insurance PART BZaheer AhmadNo ratings yet

- Fria OutlineDocument17 pagesFria OutlineIvy PazNo ratings yet

- Financial Rehabilitation and Insolvency Act: Review Notes (Following 2020 Bar Syllabus)Document13 pagesFinancial Rehabilitation and Insolvency Act: Review Notes (Following 2020 Bar Syllabus)Vanessa VelascoNo ratings yet

- Adani Draft Claim No. 7 - 11.01.2024 - JDVDocument24 pagesAdani Draft Claim No. 7 - 11.01.2024 - JDVtanyaNo ratings yet

- Bañas vs. Asia Pacific Corp., 343 SCRA 527 October 18, 2000 TEODORO BAÑASDocument39 pagesBañas vs. Asia Pacific Corp., 343 SCRA 527 October 18, 2000 TEODORO BAÑASRizza Mae EudNo ratings yet

- Declaration of Daniell. Fitchett in Support of Chapter 11Document21 pagesDeclaration of Daniell. Fitchett in Support of Chapter 11Chapter 11 DocketsNo ratings yet

- 10.digested Philippine Asset Growth Two Inc. vs. Fastech Synergy Philippines Inc. GR. No. 206528 June 28 2016Document4 pages10.digested Philippine Asset Growth Two Inc. vs. Fastech Synergy Philippines Inc. GR. No. 206528 June 28 2016Arrianne Obias0% (1)

- IAS 37 Provisions, Contingent Liabilities and Contingent AssetsDocument33 pagesIAS 37 Provisions, Contingent Liabilities and Contingent AssetsTsegay ArayaNo ratings yet

- Transcribed Notes With Supplements: AnswerDocument18 pagesTranscribed Notes With Supplements: AnswerEricha Joy GonadanNo ratings yet

- Merchants Industrial Bank, A Corporation Organized and Existing Under The Laws of The State of Colorado v. Commissioner of Internal Revenue, 475 F.2d 1063, 10th Cir. (1973)Document5 pagesMerchants Industrial Bank, A Corporation Organized and Existing Under The Laws of The State of Colorado v. Commissioner of Internal Revenue, 475 F.2d 1063, 10th Cir. (1973)Scribd Government DocsNo ratings yet

- Ch04 Provisions, Contingent Assets & LiabDocument6 pagesCh04 Provisions, Contingent Assets & LiabralphalonzoNo ratings yet

- M.C 2020 18 Regulatory Relief For Coops - Staggered Booking of Allowance For Loan LossesDocument10 pagesM.C 2020 18 Regulatory Relief For Coops - Staggered Booking of Allowance For Loan Lossesasdfjkl asddfNo ratings yet

- Attorneys For Midland Loan Services, IncDocument36 pagesAttorneys For Midland Loan Services, IncChapter 11 DocketsNo ratings yet

- 10000001776Document16 pages10000001776Chapter 11 DocketsNo ratings yet

- In Re:) Chapter 11) Collins & Aikman Corporation, Et Al.) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors.) ) (Tax Identification #13-3489233) ) ) Honorable Steven W. RhodesDocument9 pagesIn Re:) Chapter 11) Collins & Aikman Corporation, Et Al.) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors.) ) (Tax Identification #13-3489233) ) ) Honorable Steven W. RhodesChapter 11 DocketsNo ratings yet

- Banking LawsDocument33 pagesBanking LawsliboaninoNo ratings yet

- Ig MLC Faqs External 1 April 2019 Clean FinalDocument8 pagesIg MLC Faqs External 1 April 2019 Clean FinalAbhi ChaudhuriNo ratings yet

- 2011+ +FRIA+Outline+ +ALS+Commercial+Law+ReviewDocument19 pages2011+ +FRIA+Outline+ +ALS+Commercial+Law+ReviewmanzzzzzNo ratings yet

- Advanced Accounting 4th Edition Jeter Solutions Manual Full Chapter PDFDocument50 pagesAdvanced Accounting 4th Edition Jeter Solutions Manual Full Chapter PDFanwalteru32x100% (19)

- Motion of The Chapter 11 Trustee For Entry of Interim and Final Orders Authorizing Use of Cash Collateral and Request For Expedited DeterminationDocument26 pagesMotion of The Chapter 11 Trustee For Entry of Interim and Final Orders Authorizing Use of Cash Collateral and Request For Expedited DeterminationJPNo ratings yet

- Et Al./: (LL) (Ill)Document32 pagesEt Al./: (LL) (Ill)Chapter 11 DocketsNo ratings yet

- Issue: Whether The Rehabilitation Plan Is FeasibleDocument3 pagesIssue: Whether The Rehabilitation Plan Is FeasibleHomer Cervantes0% (1)

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- BP's Proposed Findings - Combined FileDocument1,303 pagesBP's Proposed Findings - Combined FileOSDocs2012No ratings yet

- To's Proposed FOF and COLDocument326 pagesTo's Proposed FOF and COLOSDocs2012No ratings yet

- DOJ Pre-Trial Statement On QuantificationDocument14 pagesDOJ Pre-Trial Statement On QuantificationwhitremerNo ratings yet

- USAs Proposed Findings Phase I (Doc. 10460 - 6.21.2013)Document121 pagesUSAs Proposed Findings Phase I (Doc. 10460 - 6.21.2013)OSDocs2012No ratings yet

- BP's Post-Trial BriefDocument72 pagesBP's Post-Trial BriefOSDocs2012No ratings yet

- HESI's Proposed FOF and COLDocument335 pagesHESI's Proposed FOF and COLOSDocs2012No ratings yet

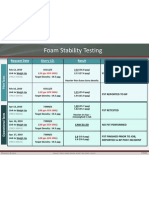

- Foam Stability Testing: Request Date Slurry I.D. Result CommentsDocument1 pageFoam Stability Testing: Request Date Slurry I.D. Result CommentsOSDocs2012No ratings yet

- Macondo Bod (Basis of Design)Document23 pagesMacondo Bod (Basis of Design)OSDocs2012No ratings yet

- PSC Post-Trial Brief (Phase One) (Doc 10458) 6-21-2013Document72 pagesPSC Post-Trial Brief (Phase One) (Doc 10458) 6-21-2013OSDocs2012100% (1)

- Plaintiffs Proposed Findings and Conclusions (Phase One) (Doc 10459) 6-21-2013Document199 pagesPlaintiffs Proposed Findings and Conclusions (Phase One) (Doc 10459) 6-21-2013OSDocs2012No ratings yet

- Arnaud Bobillier Email: June 17, 2010: "I See Some Similarities With What Happened On The Horizon"Document5 pagesArnaud Bobillier Email: June 17, 2010: "I See Some Similarities With What Happened On The Horizon"OSDocs2012No ratings yet

- Webster:: Trial Transcript at 4136:17-18Document1 pageWebster:: Trial Transcript at 4136:17-18OSDocs2012No ratings yet

- Production Interval: 14.1-14.2 PPG M57B Gas Brine GasDocument1 pageProduction Interval: 14.1-14.2 PPG M57B Gas Brine GasOSDocs2012No ratings yet

- Exterior: Circa 2003Document1 pageExterior: Circa 2003OSDocs2012No ratings yet

- End of Transmission: Transocean Drill Crew Turned The Pumps Off To InvestigateDocument1 pageEnd of Transmission: Transocean Drill Crew Turned The Pumps Off To InvestigateOSDocs2012No ratings yet

- Circa 2003Document1 pageCirca 2003OSDocs2012No ratings yet

- Driller HITEC Display CCTV Camera System: Source: TREX 4248 8153Document1 pageDriller HITEC Display CCTV Camera System: Source: TREX 4248 8153OSDocs2012No ratings yet

- Major DWH Maintenance Timeline: April 20, 2010 Rig in ServiceDocument7 pagesMajor DWH Maintenance Timeline: April 20, 2010 Rig in ServiceOSDocs2012No ratings yet

- Laboratory Results Cement Program Material Transfer TicketDocument13 pagesLaboratory Results Cement Program Material Transfer TicketOSDocs2012No ratings yet

- DR Gene: CloggedDocument1 pageDR Gene: CloggedOSDocs2012No ratings yet

- Webster:: Trial Transcript at 4015:14-16Document1 pageWebster:: Trial Transcript at 4015:14-16OSDocs2012No ratings yet

- April 20, BLOWOUT: BP Misreads Logs Does Not IdentifyDocument22 pagesApril 20, BLOWOUT: BP Misreads Logs Does Not IdentifyOSDocs2012No ratings yet

- Engines: Electrical Power Generation (ELPG) Emergency Shutdown System (ESD)Document1 pageEngines: Electrical Power Generation (ELPG) Emergency Shutdown System (ESD)OSDocs2012No ratings yet

- Webster:: Trial Transcript at 3975:2-4Document1 pageWebster:: Trial Transcript at 3975:2-4OSDocs2012No ratings yet

- Thrusters: Propulsion (PROP)Document1 pageThrusters: Propulsion (PROP)OSDocs2012No ratings yet

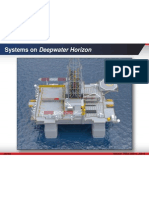

- Systems On Deepwater Horizon: Source: TREX-30014, 30015 D6753Document1 pageSystems On Deepwater Horizon: Source: TREX-30014, 30015 D6753OSDocs2012No ratings yet

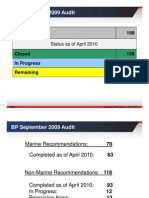

- BP September 2009 Audit: Total Items 188Document3 pagesBP September 2009 Audit: Total Items 188OSDocs2012No ratings yet

- BP Is The OperatorDocument1 pageBP Is The OperatorOSDocs2012No ratings yet

- Lloyd's Report - Appendix C: Deepwater Horizon Summary ReportDocument1 pageLloyd's Report - Appendix C: Deepwater Horizon Summary ReportOSDocs2012No ratings yet

- Transocean 2009 Annual Report: D6732 Source: TREX-5649Document3 pagesTransocean 2009 Annual Report: D6732 Source: TREX-5649OSDocs2012No ratings yet

- The General Contracting & Trading Co., LLC v. Interpole, Inc. v. Transamerican Steamship Corporation, Third-Party, 899 F.2d 109, 1st Cir. (1990)Document11 pagesThe General Contracting & Trading Co., LLC v. Interpole, Inc. v. Transamerican Steamship Corporation, Third-Party, 899 F.2d 109, 1st Cir. (1990)Scribd Government DocsNo ratings yet

- Panay Railways v. HEVA Management, GR No. 154061Document5 pagesPanay Railways v. HEVA Management, GR No. 154061MarvinNo ratings yet

- Commissioner of Internal Revenue vs. ReyesDocument19 pagesCommissioner of Internal Revenue vs. Reyesangelsu04No ratings yet

- PDB Blanks & Glitter v. DeFries - AnswerDocument22 pagesPDB Blanks & Glitter v. DeFries - AnswerSarah BursteinNo ratings yet

- Dayag vs. CanizaresDocument7 pagesDayag vs. CanizaresPollyana TanaleonNo ratings yet

- Contract of LeaseDocument7 pagesContract of LeaseJhoey Castillo BuenoNo ratings yet

- Transpo Case 12 Pantranco North Express Vs Baesa and Ico Et - Al.Document5 pagesTranspo Case 12 Pantranco North Express Vs Baesa and Ico Et - Al.Ma. Cielito Carmela Gabrielle G. MateoNo ratings yet

- 3d Crystal Engraving System PDFDocument24 pages3d Crystal Engraving System PDFGangana RaNo ratings yet

- Amco Republic of Resubmitted Decision: Indonesia: Case On JurisdictionDocument13 pagesAmco Republic of Resubmitted Decision: Indonesia: Case On JurisdictionKylie Kaur Manalon DadoNo ratings yet

- False Testimony V PerjuryDocument10 pagesFalse Testimony V PerjuryV100% (1)

- Federal Whistleblower and Targeted Individual of U.S Sponsored Mind Control Executive Summary June 29, 2015Document16 pagesFederal Whistleblower and Targeted Individual of U.S Sponsored Mind Control Executive Summary June 29, 2015Stan J. CaterboneNo ratings yet

- Case Digest No. 23Document3 pagesCase Digest No. 23Nikki P. GabianeNo ratings yet

- Professional Ethics and Accounting System ProjectDocument6 pagesProfessional Ethics and Accounting System ProjectPayal YadavNo ratings yet

- Stat Con ReviewerDocument4 pagesStat Con ReviewerjoaneriqNo ratings yet

- San Gabriel vs. Atty. SempioDocument2 pagesSan Gabriel vs. Atty. SempioRob0% (1)

- Land Titles MADocument27 pagesLand Titles MASuiNo ratings yet

- Heirs of Ypon v. PonterasDocument2 pagesHeirs of Ypon v. PonterasCzarina CidNo ratings yet

- Ang Tibay Vs CADocument2 pagesAng Tibay Vs CAEarl LarroderNo ratings yet

- Fulache V ABSCBNDocument4 pagesFulache V ABSCBNpurplebasketNo ratings yet

- B'M S Bhagwati Prasad Pawan Kumar Vs Union of IndiaDocument7 pagesB'M S Bhagwati Prasad Pawan Kumar Vs Union of IndiaAnay MehrotraNo ratings yet

- Affiliation and Disaffiliation CaseDocument57 pagesAffiliation and Disaffiliation Casedave_88op100% (1)

- What Is An Alternative Dispute Resolution?Document8 pagesWhat Is An Alternative Dispute Resolution?Rajveer Singh SekhonNo ratings yet

- Deutsche Bank Natl. Trust Co. v. QuinonesDocument4 pagesDeutsche Bank Natl. Trust Co. v. QuinonesForeclosure FraudNo ratings yet

- Chapter 12 Lecture 1 Organizational StructureDocument27 pagesChapter 12 Lecture 1 Organizational Structurealy_alsayedNo ratings yet

- Adiarte Vs Tumaneng 88 Phil 333Document2 pagesAdiarte Vs Tumaneng 88 Phil 333Joshua VivarNo ratings yet

- Lorenzana Vs AustriaDocument9 pagesLorenzana Vs AustriaMary ChrisNo ratings yet

- Law and PovertyDocument15 pagesLaw and PovertyAnonymous mpgedaEft100% (1)

- Uson vs. Del Rosario, 92 Phil 530, Jan. 29, 1953Document2 pagesUson vs. Del Rosario, 92 Phil 530, Jan. 29, 1953Krisha Marie Carlos50% (2)