Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- CFO Job Description DRAFTDocument3 pagesCFO Job Description DRAFTpatrickNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Some of The More Common Accounting Best Practices IncludeDocument6 pagesSome of The More Common Accounting Best Practices IncludeCalvince OumaNo ratings yet

- Annual Accomplishment Report - Jan - Nov 2021Document5 pagesAnnual Accomplishment Report - Jan - Nov 2021Valerie SantiagoNo ratings yet

- Capital MarketsDocument17 pagesCapital MarketsSHEILA LUMAYGAY100% (1)

- Vrio Framework of GilleteDocument2 pagesVrio Framework of GilleteHenry NelsonNo ratings yet

- Kanpur Confectioneries Private Limited - Case StudyDocument2 pagesKanpur Confectioneries Private Limited - Case StudyParveen BhardwajNo ratings yet

- 1 s2.0 S1042443123000690 MainDocument17 pages1 s2.0 S1042443123000690 MainOumema AL AZHARNo ratings yet

- BBA 1st Financial AccountingDocument3 pagesBBA 1st Financial AccountingAbbas Sky50% (4)

- International Relations and Current Affairs: Answer: (D)Document3 pagesInternational Relations and Current Affairs: Answer: (D)Mujahid Ali0% (1)

- Investments Chapter 1 Powerpoint SlideDocument11 pagesInvestments Chapter 1 Powerpoint SlideDénise RafaëlNo ratings yet

- 2014 - Pharmaceuticals and Healthcare Q214 Round Up (BMI)Document33 pages2014 - Pharmaceuticals and Healthcare Q214 Round Up (BMI)SamNo ratings yet

- Revista de AdministraçãoDocument12 pagesRevista de AdministraçãoJoe BotelloNo ratings yet

- Advantages of AdvertisingDocument4 pagesAdvantages of Advertisingali khanNo ratings yet

- Case Study SummaryDocument3 pagesCase Study Summary4 7No ratings yet

- Fin542 Individual AssDocument8 pagesFin542 Individual AssImran AziziNo ratings yet

- Implementation of Tax Regulations On Internet-Based Business Activity Case Study: Google'S Tax Avoidance in IndonesiaDocument11 pagesImplementation of Tax Regulations On Internet-Based Business Activity Case Study: Google'S Tax Avoidance in IndonesiagilangNo ratings yet

- IPR09Document164 pagesIPR09Fred ChenNo ratings yet

- Abans SP November-2020Document18 pagesAbans SP November-2020Ramesh SenjaliyaNo ratings yet

- Demonetization Scenario in IndiaDocument8 pagesDemonetization Scenario in IndiaNiharika YadavNo ratings yet

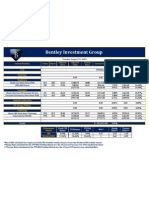

- Bentley Investment Group: Tuesday August 25, 2009Document1 pageBentley Investment Group: Tuesday August 25, 2009bentleyinvestmentgroupNo ratings yet

- A Literature Review On Social Enterprise: Yuting Zhang & Yong LiDocument6 pagesA Literature Review On Social Enterprise: Yuting Zhang & Yong LiJEFFREY WILLIAMS P M 20221013No ratings yet

- Environment: The Functions of EnvironmentDocument2 pagesEnvironment: The Functions of EnvironmentZyaban Dorayakiez CuphuwNo ratings yet

- SPK Akugrosir 2018 (Staff Gudang) in EnglishDocument3 pagesSPK Akugrosir 2018 (Staff Gudang) in EnglishBimo Mahendra PutraNo ratings yet

- Silo - Tips - Acca Paper f5 Performance Management PDFDocument57 pagesSilo - Tips - Acca Paper f5 Performance Management PDFSashauna GrahamNo ratings yet

- Entrepreneurship 31 PDF FreeDocument19 pagesEntrepreneurship 31 PDF FreeLovern Kaye RonquilloNo ratings yet

- EU Food and Drink IndustryDocument9 pagesEU Food and Drink IndustryMuhammad HarisNo ratings yet

- Test Bank For Macroeconomics 13th Edition Michael ParkinDocument36 pagesTest Bank For Macroeconomics 13th Edition Michael Parkingaoleryis.cj8rly100% (53)

- MAN 385 - Opportunity Identification and Analysis - Doggett - 04695Document7 pagesMAN 385 - Opportunity Identification and Analysis - Doggett - 04695ceojiNo ratings yet

- Business Responsibility ReportDocument9 pagesBusiness Responsibility Reportraghunandhan.cvNo ratings yet

- A Presentation OnDocument14 pagesA Presentation OnanishNo ratings yet