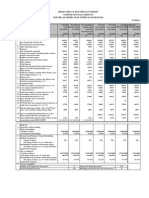

Singer Bangladesh

Singer Bangladesh

You might also like

- Sol. Man. - Chapter 1 Current LiabilitiesDocument10 pagesSol. Man. - Chapter 1 Current LiabilitiesChristine Mae Fernandez Mata100% (4)

- Chart of AccountDocument6 pagesChart of AccountSophath Sky100% (1)

- Convenience Store Business Plan ExampleDocument37 pagesConvenience Store Business Plan ExampleThreeGee JoseNo ratings yet

- Financial Aspect - Feasibility StudyDocument33 pagesFinancial Aspect - Feasibility StudyAgayatak Sa Manen55% (20)

- Financial Analysis of Samsung PLCDocument17 pagesFinancial Analysis of Samsung PLCROHIT SETHI90% (10)

- 02 ChapDocument41 pages02 ChapTanner Womble100% (1)

- A Study of Working Capital Management of Taj Mahal Palace With Oberoi HotelDocument37 pagesA Study of Working Capital Management of Taj Mahal Palace With Oberoi HotelIrshad Khan50% (2)

- Capital Reduction & Reconstruction: Liability AssetsDocument10 pagesCapital Reduction & Reconstruction: Liability AssetsOnaderu Oluwagbenga EnochNo ratings yet

- Consolidated Profit and Loss Account For The Year Ended December 31, 2008Document16 pagesConsolidated Profit and Loss Account For The Year Ended December 31, 2008madihaijazNo ratings yet

- FMDocument233 pagesFMparika khannaNo ratings yet

- Financial Analysis of Ashok Leyland LimitedDocument15 pagesFinancial Analysis of Ashok Leyland LimitedYamini NegiNo ratings yet

- Preeti 149Document16 pagesPreeti 149Preeti NeelamNo ratings yet

- Afs Assignment Profitability RatiosDocument9 pagesAfs Assignment Profitability RatiosMohsin AzizNo ratings yet

- Searle Company Ratio Analysis 2010 2011 2012Document63 pagesSearle Company Ratio Analysis 2010 2011 2012Kaleb VargasNo ratings yet

- RATIOS AnalysisDocument61 pagesRATIOS AnalysisSamuel Dwumfour100% (1)

- Asyad Financial AnalysisDocument9 pagesAsyad Financial AnalysisshawktNo ratings yet

- Ratio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDDocument10 pagesRatio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDShubham DikshitNo ratings yet

- RatiosDocument12 pagesRatiosstuck00123No ratings yet

- Acct330 - Ayush Raj GiriDocument19 pagesAcct330 - Ayush Raj GiriAyush GiriNo ratings yet

- Accounting KFC Holdings Financial Ratio Analysis of Year 2009Document16 pagesAccounting KFC Holdings Financial Ratio Analysis of Year 2009Malathi Sundrasaigaran100% (6)

- 18 Financial StatementsDocument35 pages18 Financial Statementswsahmed28No ratings yet

- ITC Consolidated FinancialsDocument49 pagesITC Consolidated FinancialsVishal JaiswalNo ratings yet

- Fin3320 Proj sp15 ChagutkalngDocument8 pagesFin3320 Proj sp15 Chagutkalngapi-283250650No ratings yet

- Accounts Financial Ratios of KFCDocument20 pagesAccounts Financial Ratios of KFCMalathi Sundrasaigaran91% (11)

- Consolidated Financial StatementsDocument40 pagesConsolidated Financial StatementsSandeep GunjanNo ratings yet

- Financial Statement Analysis: Ratio Analysis of Nokia and LGDocument35 pagesFinancial Statement Analysis: Ratio Analysis of Nokia and LGeimalmalikNo ratings yet

- Profit and Loss Account For The Year Ended March 31, 2010: Column1 Column2Document11 pagesProfit and Loss Account For The Year Ended March 31, 2010: Column1 Column2Karishma JaisinghaniNo ratings yet

- Hero Motocorp: Previous YearsDocument11 pagesHero Motocorp: Previous YearssalimsidNo ratings yet

- Sebi MillionsDocument3 pagesSebi MillionsShubham TrivediNo ratings yet

- Income Statement OldDocument9 pagesIncome Statement OldjhanzabNo ratings yet

- Fin3320 Proj Fa14 HersaltreDocument9 pagesFin3320 Proj Fa14 Hersaltreapi-290544848No ratings yet

- Ratio AnalysisDocument17 pagesRatio AnalysisXain SyedNo ratings yet

- Accounts AssignmentDocument7 pagesAccounts AssignmentHari PrasaadhNo ratings yet

- Bajaj Auto LTD: Presented By: Hitesh RameshDocument15 pagesBajaj Auto LTD: Presented By: Hitesh RameshnancyagarwalNo ratings yet

- Ratio Analysis of BMWDocument16 pagesRatio Analysis of BMWRashidsarwar01No ratings yet

- DB Corp: Key Management TakeawaysDocument6 pagesDB Corp: Key Management TakeawaysAngel BrokingNo ratings yet

- Itc LTD Financial Analysis: Group 4Document20 pagesItc LTD Financial Analysis: Group 4Kanav ChaudharyNo ratings yet

- Assignments Semester IDocument13 pagesAssignments Semester Idriger43No ratings yet

- Term 1 ProjectDocument9 pagesTerm 1 ProjectNiraj ThakurNo ratings yet

- What Are Quantitative FactorsDocument5 pagesWhat Are Quantitative FactorsJunaid CheemaNo ratings yet

- Fundamental Analysis For AIRASIA BERHAD: 1 - History of Consistently Increasing Earnings, Sales & Cash FlowDocument13 pagesFundamental Analysis For AIRASIA BERHAD: 1 - History of Consistently Increasing Earnings, Sales & Cash FlowPraman ChelseaNo ratings yet

- Din Textile Limited ProjDocument34 pagesDin Textile Limited ProjTaiba Akhlaq0% (1)

- Anamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaDocument24 pagesAnamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaAnamika ChakrabartyNo ratings yet

- Half Yearly Dec09-10 PDFDocument15 pagesHalf Yearly Dec09-10 PDFSalman S. ZiaNo ratings yet

- Siyaram Silk Mills Result UpdatedDocument9 pagesSiyaram Silk Mills Result UpdatedAngel BrokingNo ratings yet

- Directors' Report: Dabur Nepal Private LimitedDocument5 pagesDirectors' Report: Dabur Nepal Private LimitedKrishna Kumar ShresthaNo ratings yet

- Lecture 7 - Ratio AnalysisDocument39 pagesLecture 7 - Ratio AnalysisMihai Stoica100% (1)

- Bajaj Auto Financial Analysis: Presented byDocument20 pagesBajaj Auto Financial Analysis: Presented byMayank_Gupta_1995No ratings yet

- Projet PGPM RatioDocument16 pagesProjet PGPM RatioViren PatelNo ratings yet

- Assignment of Financial AccountingDocument15 pagesAssignment of Financial AccountingBhushan WadherNo ratings yet

- Avon Powerpoint PresentationDocument22 pagesAvon Powerpoint PresentationOana TrutaNo ratings yet

- Session 1 Financial Accounting Infor Manju JaiswallDocument41 pagesSession 1 Financial Accounting Infor Manju JaiswallpremoshinNo ratings yet

- Name: Bilal Ahmed ID: Mc090200863 Degree: MBA Specialization: FinanceDocument46 pagesName: Bilal Ahmed ID: Mc090200863 Degree: MBA Specialization: FinanceEngr MahaNo ratings yet

- NTB - 1H2013 Earnings Note - BUY - 27 August 2013Document4 pagesNTB - 1H2013 Earnings Note - BUY - 27 August 2013Randora LkNo ratings yet

- Ma Term Paper 20192mba0328Document8 pagesMa Term Paper 20192mba0328Dileepkumar K DiliNo ratings yet

- PPTDocument35 pagesPPTShivam ChauhanNo ratings yet

- Ratio Analysis of Shinepukur Ceremics Ltd.Document0 pagesRatio Analysis of Shinepukur Ceremics Ltd.Saddam HossainNo ratings yet

- Fa ProjectDocument16 pagesFa Projecttapas_kbNo ratings yet

- Prepared By: Umair Mazher (3371) Submitted To: Iqbal LalaniDocument22 pagesPrepared By: Umair Mazher (3371) Submitted To: Iqbal Lalaniumair_mazherNo ratings yet

- Financial Analysis: P & L Statement of GE ShippingDocument4 pagesFinancial Analysis: P & L Statement of GE ShippingShashank ShrivastavaNo ratings yet

- Financial Statement Analysis of Lucky CementDocument27 pagesFinancial Statement Analysis of Lucky CementRaja UmairNo ratings yet

- TSL Audited Results For FY Ended 31 Oct 13Document2 pagesTSL Audited Results For FY Ended 31 Oct 13Business Daily ZimbabweNo ratings yet

- Series 1: 1. Profit Margin RatioDocument10 pagesSeries 1: 1. Profit Margin RatioPooja WadhwaniNo ratings yet

- Financial Reporting and Analysis ProjectDocument15 pagesFinancial Reporting and Analysis Projectsonar_neel100% (1)

- Business Credit Institutions Miscellaneous Revenues World Summary: Market Values & Financials by CountryFrom EverandBusiness Credit Institutions Miscellaneous Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Bangladesh Withholding Tax Return FormDocument15 pagesBangladesh Withholding Tax Return FormMahbubur RahmanNo ratings yet

- Janata Bank ProcessDocument5 pagesJanata Bank ProcessMahbubur RahmanNo ratings yet

- Excuse LaterDocument1 pageExcuse LaterMahbubur RahmanNo ratings yet

- Technical Analysis N Cost of CapitalDocument29 pagesTechnical Analysis N Cost of CapitalMahbubur RahmanNo ratings yet

- Cement Industry in BDDocument26 pagesCement Industry in BDMahbubur Rahman75% (4)

- Project:: Project Management Is The Discipline of Planning, Organizing and ManagingDocument14 pagesProject:: Project Management Is The Discipline of Planning, Organizing and ManagingMahbubur RahmanNo ratings yet

- Elements of Business PlanDocument10 pagesElements of Business PlanMahbubur RahmanNo ratings yet

- Bextex LTD Report (Ratio Analysis)Document17 pagesBextex LTD Report (Ratio Analysis)Mahbubur Rahman100% (3)

- Press ReleaseDocument2 pagesPress ReleaseMahbubur RahmanNo ratings yet

- Proposal Latter For Dance Program at TVDocument2 pagesProposal Latter For Dance Program at TVMahbubur RahmanNo ratings yet

- Financial Statement Analysis of GlaxosmithklineDocument19 pagesFinancial Statement Analysis of GlaxosmithklineRaquibul HassanNo ratings yet

- Estados Financieros NESTLEDocument2 pagesEstados Financieros NESTLEdsgasdgaNo ratings yet

- a056e97a33e0bf6fa4710a27d010a65dDocument101 pagesa056e97a33e0bf6fa4710a27d010a65dLinda KurniawanNo ratings yet

- Balance Sheet TutorialDocument68 pagesBalance Sheet TutorialavadcsNo ratings yet

- Hand Out 1 Practice SetDocument6 pagesHand Out 1 Practice SetLayka ResorezNo ratings yet

- Kamat Hotels India LTDDocument44 pagesKamat Hotels India LTDpsy mediaNo ratings yet

- Cigar Manufacturing Business PlanDocument24 pagesCigar Manufacturing Business PlanVivek DodaNo ratings yet

- Chapter 2 Analysis of Financial StatementDocument18 pagesChapter 2 Analysis of Financial StatementSuman ChaudharyNo ratings yet

- Pure Gold Financial StatementsDocument90 pagesPure Gold Financial StatementsHanz SoNo ratings yet

- Fs 2018 NardaDocument13 pagesFs 2018 NardaMelanie GaledoNo ratings yet

- Quiz - Chapter 1 - Current Liabilities - 2021Document3 pagesQuiz - Chapter 1 - Current Liabilities - 2021Jennifer RelosoNo ratings yet

- Actg 431 Quiz Week 4 Theory of Accounts (Part IV) Liabilities QuizDocument4 pagesActg 431 Quiz Week 4 Theory of Accounts (Part IV) Liabilities QuizMarilou Arcillas PanisalesNo ratings yet

- Working Capital Managmnet - Pune University - MBA Project Report - Set2Document48 pagesWorking Capital Managmnet - Pune University - MBA Project Report - Set2amol.naleNo ratings yet

- Dr. Mohammed Anam Akhtar Lecturer Accounting & FinanceDocument55 pagesDr. Mohammed Anam Akhtar Lecturer Accounting & FinanceAfra ShaikhNo ratings yet

- Spreadsheet - FinancialsDocument97 pagesSpreadsheet - FinancialstevalNo ratings yet

- FINM 7044 Group Assignment 终Document4 pagesFINM 7044 Group Assignment 终jimmmmNo ratings yet

- AFM - Module 3Document61 pagesAFM - Module 3Abhishek JainNo ratings yet

- Population Reference Bureau Annual-Report-2019Document10 pagesPopulation Reference Bureau Annual-Report-2019eyaoNo ratings yet

- Liquid CultureDocument16 pagesLiquid CultureDolly BadlaniNo ratings yet

- Nov2021 CPE Assessment of KSU FinancesDocument52 pagesNov2021 CPE Assessment of KSU FinancesWKYTNo ratings yet

- Chapter18 - Answer PDFDocument25 pagesChapter18 - Answer PDFJONAS VINCENT SamsonNo ratings yet

- Report On Financial Structure of Maruti Suzuki India LimitedDocument6 pagesReport On Financial Structure of Maruti Suzuki India LimitedSabab ZamanNo ratings yet

- Summer Training Project ReportDocument63 pagesSummer Training Project ReportrathodmauleshNo ratings yet

- Azgard Nine Limited-Internship ReportDocument102 pagesAzgard Nine Limited-Internship ReportM.Faisal100% (1)

Download as doc, pdf, or txt

You might also like

- Sol. Man. - Chapter 1 Current LiabilitiesDocument10 pagesSol. Man. - Chapter 1 Current LiabilitiesChristine Mae Fernandez Mata100% (4)

- Chart of AccountDocument6 pagesChart of AccountSophath Sky100% (1)

- Convenience Store Business Plan ExampleDocument37 pagesConvenience Store Business Plan ExampleThreeGee JoseNo ratings yet

- Financial Aspect - Feasibility StudyDocument33 pagesFinancial Aspect - Feasibility StudyAgayatak Sa Manen55% (20)

- Financial Analysis of Samsung PLCDocument17 pagesFinancial Analysis of Samsung PLCROHIT SETHI90% (10)

- 02 ChapDocument41 pages02 ChapTanner Womble100% (1)

- A Study of Working Capital Management of Taj Mahal Palace With Oberoi HotelDocument37 pagesA Study of Working Capital Management of Taj Mahal Palace With Oberoi HotelIrshad Khan50% (2)

- Capital Reduction & Reconstruction: Liability AssetsDocument10 pagesCapital Reduction & Reconstruction: Liability AssetsOnaderu Oluwagbenga EnochNo ratings yet

- Consolidated Profit and Loss Account For The Year Ended December 31, 2008Document16 pagesConsolidated Profit and Loss Account For The Year Ended December 31, 2008madihaijazNo ratings yet

- FMDocument233 pagesFMparika khannaNo ratings yet

- Financial Analysis of Ashok Leyland LimitedDocument15 pagesFinancial Analysis of Ashok Leyland LimitedYamini NegiNo ratings yet

- Preeti 149Document16 pagesPreeti 149Preeti NeelamNo ratings yet

- Afs Assignment Profitability RatiosDocument9 pagesAfs Assignment Profitability RatiosMohsin AzizNo ratings yet

- Searle Company Ratio Analysis 2010 2011 2012Document63 pagesSearle Company Ratio Analysis 2010 2011 2012Kaleb VargasNo ratings yet

- RATIOS AnalysisDocument61 pagesRATIOS AnalysisSamuel Dwumfour100% (1)

- Asyad Financial AnalysisDocument9 pagesAsyad Financial AnalysisshawktNo ratings yet

- Ratio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDDocument10 pagesRatio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDShubham DikshitNo ratings yet

- RatiosDocument12 pagesRatiosstuck00123No ratings yet

- Acct330 - Ayush Raj GiriDocument19 pagesAcct330 - Ayush Raj GiriAyush GiriNo ratings yet

- Accounting KFC Holdings Financial Ratio Analysis of Year 2009Document16 pagesAccounting KFC Holdings Financial Ratio Analysis of Year 2009Malathi Sundrasaigaran100% (6)

- 18 Financial StatementsDocument35 pages18 Financial Statementswsahmed28No ratings yet

- ITC Consolidated FinancialsDocument49 pagesITC Consolidated FinancialsVishal JaiswalNo ratings yet

- Fin3320 Proj sp15 ChagutkalngDocument8 pagesFin3320 Proj sp15 Chagutkalngapi-283250650No ratings yet

- Accounts Financial Ratios of KFCDocument20 pagesAccounts Financial Ratios of KFCMalathi Sundrasaigaran91% (11)

- Consolidated Financial StatementsDocument40 pagesConsolidated Financial StatementsSandeep GunjanNo ratings yet

- Financial Statement Analysis: Ratio Analysis of Nokia and LGDocument35 pagesFinancial Statement Analysis: Ratio Analysis of Nokia and LGeimalmalikNo ratings yet

- Profit and Loss Account For The Year Ended March 31, 2010: Column1 Column2Document11 pagesProfit and Loss Account For The Year Ended March 31, 2010: Column1 Column2Karishma JaisinghaniNo ratings yet

- Hero Motocorp: Previous YearsDocument11 pagesHero Motocorp: Previous YearssalimsidNo ratings yet

- Sebi MillionsDocument3 pagesSebi MillionsShubham TrivediNo ratings yet

- Income Statement OldDocument9 pagesIncome Statement OldjhanzabNo ratings yet

- Fin3320 Proj Fa14 HersaltreDocument9 pagesFin3320 Proj Fa14 Hersaltreapi-290544848No ratings yet

- Ratio AnalysisDocument17 pagesRatio AnalysisXain SyedNo ratings yet

- Accounts AssignmentDocument7 pagesAccounts AssignmentHari PrasaadhNo ratings yet

- Bajaj Auto LTD: Presented By: Hitesh RameshDocument15 pagesBajaj Auto LTD: Presented By: Hitesh RameshnancyagarwalNo ratings yet

- Ratio Analysis of BMWDocument16 pagesRatio Analysis of BMWRashidsarwar01No ratings yet

- DB Corp: Key Management TakeawaysDocument6 pagesDB Corp: Key Management TakeawaysAngel BrokingNo ratings yet

- Itc LTD Financial Analysis: Group 4Document20 pagesItc LTD Financial Analysis: Group 4Kanav ChaudharyNo ratings yet

- Assignments Semester IDocument13 pagesAssignments Semester Idriger43No ratings yet

- Term 1 ProjectDocument9 pagesTerm 1 ProjectNiraj ThakurNo ratings yet

- What Are Quantitative FactorsDocument5 pagesWhat Are Quantitative FactorsJunaid CheemaNo ratings yet

- Fundamental Analysis For AIRASIA BERHAD: 1 - History of Consistently Increasing Earnings, Sales & Cash FlowDocument13 pagesFundamental Analysis For AIRASIA BERHAD: 1 - History of Consistently Increasing Earnings, Sales & Cash FlowPraman ChelseaNo ratings yet

- Din Textile Limited ProjDocument34 pagesDin Textile Limited ProjTaiba Akhlaq0% (1)

- Anamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaDocument24 pagesAnamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaAnamika ChakrabartyNo ratings yet

- Half Yearly Dec09-10 PDFDocument15 pagesHalf Yearly Dec09-10 PDFSalman S. ZiaNo ratings yet

- Siyaram Silk Mills Result UpdatedDocument9 pagesSiyaram Silk Mills Result UpdatedAngel BrokingNo ratings yet

- Directors' Report: Dabur Nepal Private LimitedDocument5 pagesDirectors' Report: Dabur Nepal Private LimitedKrishna Kumar ShresthaNo ratings yet

- Lecture 7 - Ratio AnalysisDocument39 pagesLecture 7 - Ratio AnalysisMihai Stoica100% (1)

- Bajaj Auto Financial Analysis: Presented byDocument20 pagesBajaj Auto Financial Analysis: Presented byMayank_Gupta_1995No ratings yet

- Projet PGPM RatioDocument16 pagesProjet PGPM RatioViren PatelNo ratings yet

- Assignment of Financial AccountingDocument15 pagesAssignment of Financial AccountingBhushan WadherNo ratings yet

- Avon Powerpoint PresentationDocument22 pagesAvon Powerpoint PresentationOana TrutaNo ratings yet

- Session 1 Financial Accounting Infor Manju JaiswallDocument41 pagesSession 1 Financial Accounting Infor Manju JaiswallpremoshinNo ratings yet

- Name: Bilal Ahmed ID: Mc090200863 Degree: MBA Specialization: FinanceDocument46 pagesName: Bilal Ahmed ID: Mc090200863 Degree: MBA Specialization: FinanceEngr MahaNo ratings yet

- NTB - 1H2013 Earnings Note - BUY - 27 August 2013Document4 pagesNTB - 1H2013 Earnings Note - BUY - 27 August 2013Randora LkNo ratings yet

- Ma Term Paper 20192mba0328Document8 pagesMa Term Paper 20192mba0328Dileepkumar K DiliNo ratings yet

- PPTDocument35 pagesPPTShivam ChauhanNo ratings yet

- Ratio Analysis of Shinepukur Ceremics Ltd.Document0 pagesRatio Analysis of Shinepukur Ceremics Ltd.Saddam HossainNo ratings yet

- Fa ProjectDocument16 pagesFa Projecttapas_kbNo ratings yet

- Prepared By: Umair Mazher (3371) Submitted To: Iqbal LalaniDocument22 pagesPrepared By: Umair Mazher (3371) Submitted To: Iqbal Lalaniumair_mazherNo ratings yet

- Financial Analysis: P & L Statement of GE ShippingDocument4 pagesFinancial Analysis: P & L Statement of GE ShippingShashank ShrivastavaNo ratings yet

- Financial Statement Analysis of Lucky CementDocument27 pagesFinancial Statement Analysis of Lucky CementRaja UmairNo ratings yet

- TSL Audited Results For FY Ended 31 Oct 13Document2 pagesTSL Audited Results For FY Ended 31 Oct 13Business Daily ZimbabweNo ratings yet

- Series 1: 1. Profit Margin RatioDocument10 pagesSeries 1: 1. Profit Margin RatioPooja WadhwaniNo ratings yet

- Financial Reporting and Analysis ProjectDocument15 pagesFinancial Reporting and Analysis Projectsonar_neel100% (1)

- Business Credit Institutions Miscellaneous Revenues World Summary: Market Values & Financials by CountryFrom EverandBusiness Credit Institutions Miscellaneous Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Bangladesh Withholding Tax Return FormDocument15 pagesBangladesh Withholding Tax Return FormMahbubur RahmanNo ratings yet

- Janata Bank ProcessDocument5 pagesJanata Bank ProcessMahbubur RahmanNo ratings yet

- Excuse LaterDocument1 pageExcuse LaterMahbubur RahmanNo ratings yet

- Technical Analysis N Cost of CapitalDocument29 pagesTechnical Analysis N Cost of CapitalMahbubur RahmanNo ratings yet

- Cement Industry in BDDocument26 pagesCement Industry in BDMahbubur Rahman75% (4)

- Project:: Project Management Is The Discipline of Planning, Organizing and ManagingDocument14 pagesProject:: Project Management Is The Discipline of Planning, Organizing and ManagingMahbubur RahmanNo ratings yet

- Elements of Business PlanDocument10 pagesElements of Business PlanMahbubur RahmanNo ratings yet

- Bextex LTD Report (Ratio Analysis)Document17 pagesBextex LTD Report (Ratio Analysis)Mahbubur Rahman100% (3)

- Press ReleaseDocument2 pagesPress ReleaseMahbubur RahmanNo ratings yet

- Proposal Latter For Dance Program at TVDocument2 pagesProposal Latter For Dance Program at TVMahbubur RahmanNo ratings yet

- Financial Statement Analysis of GlaxosmithklineDocument19 pagesFinancial Statement Analysis of GlaxosmithklineRaquibul HassanNo ratings yet

- Estados Financieros NESTLEDocument2 pagesEstados Financieros NESTLEdsgasdgaNo ratings yet

- a056e97a33e0bf6fa4710a27d010a65dDocument101 pagesa056e97a33e0bf6fa4710a27d010a65dLinda KurniawanNo ratings yet

- Balance Sheet TutorialDocument68 pagesBalance Sheet TutorialavadcsNo ratings yet

- Hand Out 1 Practice SetDocument6 pagesHand Out 1 Practice SetLayka ResorezNo ratings yet

- Kamat Hotels India LTDDocument44 pagesKamat Hotels India LTDpsy mediaNo ratings yet

- Cigar Manufacturing Business PlanDocument24 pagesCigar Manufacturing Business PlanVivek DodaNo ratings yet

- Chapter 2 Analysis of Financial StatementDocument18 pagesChapter 2 Analysis of Financial StatementSuman ChaudharyNo ratings yet

- Pure Gold Financial StatementsDocument90 pagesPure Gold Financial StatementsHanz SoNo ratings yet

- Fs 2018 NardaDocument13 pagesFs 2018 NardaMelanie GaledoNo ratings yet

- Quiz - Chapter 1 - Current Liabilities - 2021Document3 pagesQuiz - Chapter 1 - Current Liabilities - 2021Jennifer RelosoNo ratings yet

- Actg 431 Quiz Week 4 Theory of Accounts (Part IV) Liabilities QuizDocument4 pagesActg 431 Quiz Week 4 Theory of Accounts (Part IV) Liabilities QuizMarilou Arcillas PanisalesNo ratings yet

- Working Capital Managmnet - Pune University - MBA Project Report - Set2Document48 pagesWorking Capital Managmnet - Pune University - MBA Project Report - Set2amol.naleNo ratings yet

- Dr. Mohammed Anam Akhtar Lecturer Accounting & FinanceDocument55 pagesDr. Mohammed Anam Akhtar Lecturer Accounting & FinanceAfra ShaikhNo ratings yet

- Spreadsheet - FinancialsDocument97 pagesSpreadsheet - FinancialstevalNo ratings yet

- FINM 7044 Group Assignment 终Document4 pagesFINM 7044 Group Assignment 终jimmmmNo ratings yet

- AFM - Module 3Document61 pagesAFM - Module 3Abhishek JainNo ratings yet

- Population Reference Bureau Annual-Report-2019Document10 pagesPopulation Reference Bureau Annual-Report-2019eyaoNo ratings yet

- Liquid CultureDocument16 pagesLiquid CultureDolly BadlaniNo ratings yet

- Nov2021 CPE Assessment of KSU FinancesDocument52 pagesNov2021 CPE Assessment of KSU FinancesWKYTNo ratings yet

- Chapter18 - Answer PDFDocument25 pagesChapter18 - Answer PDFJONAS VINCENT SamsonNo ratings yet

- Report On Financial Structure of Maruti Suzuki India LimitedDocument6 pagesReport On Financial Structure of Maruti Suzuki India LimitedSabab ZamanNo ratings yet

- Summer Training Project ReportDocument63 pagesSummer Training Project ReportrathodmauleshNo ratings yet

- Azgard Nine Limited-Internship ReportDocument102 pagesAzgard Nine Limited-Internship ReportM.Faisal100% (1)