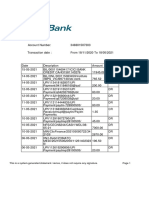

Settlement

Settlement

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Statement: Stefan Fegerl Stefan FegerlDocument2 pagesStatement: Stefan Fegerl Stefan Fegerlpaiment flechetteNo ratings yet

- India Fintech Report 2021Document29 pagesIndia Fintech Report 2021devang bohraNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 156114-124731 20190930 PDFDocument7 pages156114-124731 20190930 PDFAmru OmarNo ratings yet

- Singapore Financial SystemDocument21 pagesSingapore Financial SystemSaikat SahaNo ratings yet

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument15 pagesThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureASHISH PANDEYNo ratings yet

- Soa 102021Document2 pagesSoa 102021Jethro VillahermosaNo ratings yet

- The Bank of The Future PDFDocument124 pagesThe Bank of The Future PDFsubas khanal100% (1)

- Report - 2023 11 16 - 23 56 11Document2 pagesReport - 2023 11 16 - 23 56 11jennyscol4realNo ratings yet

- The Impact of Blockchain Technology in Banking: Roshan KhadkaDocument37 pagesThe Impact of Blockchain Technology in Banking: Roshan KhadkamonuNo ratings yet

- DBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002Document3 pagesDBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002sudheermca068345No ratings yet

- S2-The Ultimate Guide To Buying CryptocurrenciesDocument12 pagesS2-The Ultimate Guide To Buying CryptocurrenciesShoaib MohammadNo ratings yet

- R20AMR ReleaseHighlights ClientDocument176 pagesR20AMR ReleaseHighlights ClientZakaria AlmamariNo ratings yet

- Receipt 2Document2 pagesReceipt 2avsmaju management100% (1)

- NTVAXBPr 6 R 8 H FHU4Document9 pagesNTVAXBPr 6 R 8 H FHU4Ranjit BeheraNo ratings yet

- XboxDocument6 pagesXboxvenipaz63No ratings yet

- Debit CardDocument16 pagesDebit CardAvinash Sahu100% (2)

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiNo ratings yet

- 1.04.22 - 21.08.22 CanaraDocument7 pages1.04.22 - 21.08.22 CanaraMADHUBALA SAHAYNo ratings yet

- Moldcell PromoDocument4 pagesMoldcell PromounifunNo ratings yet

- Famous Debit and Credit Fraud CasesDocument7 pagesFamous Debit and Credit Fraud CasesAmy Jones100% (1)

- Cespt Tijuana Online Payment TranslationDocument2 pagesCespt Tijuana Online Payment TranslationJessica DonahueNo ratings yet

- Freelance Independent Contractor Invoice TemplateDocument2 pagesFreelance Independent Contractor Invoice TemplateBrendan DickinsonNo ratings yet

- Annoucement and Guideline - Eng VDocument1 pageAnnoucement and Guideline - Eng VMohammad Syafiq Mohd YalanNo ratings yet

- Chargeback Process FlowDocument11 pagesChargeback Process FlowguyNo ratings yet

- JNNJDocument48 pagesJNNJBirdmanZxNo ratings yet

- Product Overview IMPSDocument3 pagesProduct Overview IMPSKuriya HardikNo ratings yet

- New BankDocument13 pagesNew BankVelayudhan SunkaraNo ratings yet

- IDFC FASTag Summary1672234138849Document2 pagesIDFC FASTag Summary1672234138849MAHESH MOTORSNo ratings yet

- آليات رقمنة الخدمات المالية والمصرفية لإرساء الشمول المالي الرقمي - اعتماد ابتكارات التكنولوجيا المالية كسبيلDocument16 pagesآليات رقمنة الخدمات المالية والمصرفية لإرساء الشمول المالي الرقمي - اعتماد ابتكارات التكنولوجيا المالية كسبيلsofiane.meamicheNo ratings yet

- Buy Bitcoin Cash With A Credit Card Trust WalletDocument1 pageBuy Bitcoin Cash With A Credit Card Trust WalletMichelle GoorisNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Statement: Stefan Fegerl Stefan FegerlDocument2 pagesStatement: Stefan Fegerl Stefan Fegerlpaiment flechetteNo ratings yet

- India Fintech Report 2021Document29 pagesIndia Fintech Report 2021devang bohraNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 156114-124731 20190930 PDFDocument7 pages156114-124731 20190930 PDFAmru OmarNo ratings yet

- Singapore Financial SystemDocument21 pagesSingapore Financial SystemSaikat SahaNo ratings yet

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument15 pagesThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureASHISH PANDEYNo ratings yet

- Soa 102021Document2 pagesSoa 102021Jethro VillahermosaNo ratings yet

- The Bank of The Future PDFDocument124 pagesThe Bank of The Future PDFsubas khanal100% (1)

- Report - 2023 11 16 - 23 56 11Document2 pagesReport - 2023 11 16 - 23 56 11jennyscol4realNo ratings yet

- The Impact of Blockchain Technology in Banking: Roshan KhadkaDocument37 pagesThe Impact of Blockchain Technology in Banking: Roshan KhadkamonuNo ratings yet

- DBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002Document3 pagesDBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002sudheermca068345No ratings yet

- S2-The Ultimate Guide To Buying CryptocurrenciesDocument12 pagesS2-The Ultimate Guide To Buying CryptocurrenciesShoaib MohammadNo ratings yet

- R20AMR ReleaseHighlights ClientDocument176 pagesR20AMR ReleaseHighlights ClientZakaria AlmamariNo ratings yet

- Receipt 2Document2 pagesReceipt 2avsmaju management100% (1)

- NTVAXBPr 6 R 8 H FHU4Document9 pagesNTVAXBPr 6 R 8 H FHU4Ranjit BeheraNo ratings yet

- XboxDocument6 pagesXboxvenipaz63No ratings yet

- Debit CardDocument16 pagesDebit CardAvinash Sahu100% (2)

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiNo ratings yet

- 1.04.22 - 21.08.22 CanaraDocument7 pages1.04.22 - 21.08.22 CanaraMADHUBALA SAHAYNo ratings yet

- Moldcell PromoDocument4 pagesMoldcell PromounifunNo ratings yet

- Famous Debit and Credit Fraud CasesDocument7 pagesFamous Debit and Credit Fraud CasesAmy Jones100% (1)

- Cespt Tijuana Online Payment TranslationDocument2 pagesCespt Tijuana Online Payment TranslationJessica DonahueNo ratings yet

- Freelance Independent Contractor Invoice TemplateDocument2 pagesFreelance Independent Contractor Invoice TemplateBrendan DickinsonNo ratings yet

- Annoucement and Guideline - Eng VDocument1 pageAnnoucement and Guideline - Eng VMohammad Syafiq Mohd YalanNo ratings yet

- Chargeback Process FlowDocument11 pagesChargeback Process FlowguyNo ratings yet

- JNNJDocument48 pagesJNNJBirdmanZxNo ratings yet

- Product Overview IMPSDocument3 pagesProduct Overview IMPSKuriya HardikNo ratings yet

- New BankDocument13 pagesNew BankVelayudhan SunkaraNo ratings yet

- IDFC FASTag Summary1672234138849Document2 pagesIDFC FASTag Summary1672234138849MAHESH MOTORSNo ratings yet

- آليات رقمنة الخدمات المالية والمصرفية لإرساء الشمول المالي الرقمي - اعتماد ابتكارات التكنولوجيا المالية كسبيلDocument16 pagesآليات رقمنة الخدمات المالية والمصرفية لإرساء الشمول المالي الرقمي - اعتماد ابتكارات التكنولوجيا المالية كسبيلsofiane.meamicheNo ratings yet

- Buy Bitcoin Cash With A Credit Card Trust WalletDocument1 pageBuy Bitcoin Cash With A Credit Card Trust WalletMichelle GoorisNo ratings yet