Download as pdf or txt

You might also like

- Proposed Changes To Marijuana LawDocument165 pagesProposed Changes To Marijuana LawJessie BalmertNo ratings yet

- Dry Bulk Full Report SMOO Q1 2024Document8 pagesDry Bulk Full Report SMOO Q1 2024bill duan100% (1)

- Oilfield Seamanship Series - Complete SetDocument2 pagesOilfield Seamanship Series - Complete SetWisnu Kertaningnagoro0% (1)

- The Hollywood Film Music Reader PDFDocument393 pagesThe Hollywood Film Music Reader PDFMarc100% (1)

- IKEA Case StudyDocument12 pagesIKEA Case StudyAmrit Prasad0% (1)

- Argus: Tanker FreightDocument25 pagesArgus: Tanker FreightIvan OsipovNo ratings yet

- European Spot Gas Markets-11-Jan-2021Document20 pagesEuropean Spot Gas Markets-11-Jan-2021Tihomir RoščićNo ratings yet

- Volume Chain Locker GL ClassDocument1 pageVolume Chain Locker GL ClassWisnu KertaningnagoroNo ratings yet

- Fearnley Market Report December 2018Document20 pagesFearnley Market Report December 2018Charles GohNo ratings yet

- RS Platou Global Support Vessel Monthly February 2012Document15 pagesRS Platou Global Support Vessel Monthly February 2012kelvin_chong_38No ratings yet

- RDocument34 pagesRJhoel HuanacoNo ratings yet

- Urea Weekly Market Report 6 Sept17Document18 pagesUrea Weekly Market Report 6 Sept17Victor VazquezNo ratings yet

- Questionnaire Exercise: Deals Desk Analyst Please Answer Below Questions and Email Your Responses Before First Technical Round of InterviewDocument2 pagesQuestionnaire Exercise: Deals Desk Analyst Please Answer Below Questions and Email Your Responses Before First Technical Round of InterviewAbhinav SahaniNo ratings yet

- Shipboard High Voltage Application and Safeties - Hanif Dewan's BlogDocument26 pagesShipboard High Voltage Application and Safeties - Hanif Dewan's BlogWisnu KertaningnagoroNo ratings yet

- Enclosed Space Drill ScenarioDocument1 pageEnclosed Space Drill ScenarioWisnu Kertaningnagoro100% (1)

- Vegetable Oils and Fats On Chemical Tankers - Capt Ajit VadakayilDocument29 pagesVegetable Oils and Fats On Chemical Tankers - Capt Ajit VadakayilWisnu KertaningnagoroNo ratings yet

- Example COSHH Risk Assessment - Workshop - COSHHDocument2 pagesExample COSHH Risk Assessment - Workshop - COSHHWisnu KertaningnagoroNo ratings yet

- Tankers Dry Bulk: Published by Fearnresearch 18. September 2013Document3 pagesTankers Dry Bulk: Published by Fearnresearch 18. September 2013SimmarineNo ratings yet

- Intermodal Weekly Market Report 3rd February 2015, Week 5Document9 pagesIntermodal Weekly Market Report 3rd February 2015, Week 5Budi PrayitnoNo ratings yet

- Shipping OutlookDocument27 pagesShipping OutlookmervynteoNo ratings yet

- Week 34Document18 pagesWeek 34notaristisNo ratings yet

- SeaIntel Sunday Spotlight Issue 100Document31 pagesSeaIntel Sunday Spotlight Issue 100Alan Roos MurphyNo ratings yet

- Container Market PDFDocument3 pagesContainer Market PDFDhruv AgarwalNo ratings yet

- Worldyards May 2007 NewsletterDocument20 pagesWorldyards May 2007 Newsletternestor mospanNo ratings yet

- CRSL Presentation 2nd October 2013 FinalDocument41 pagesCRSL Presentation 2nd October 2013 FinalWilliam FergusonNo ratings yet

- Daily Market Report: Poten & PartnersDocument1 pageDaily Market Report: Poten & PartnersalgeriacandaNo ratings yet

- Shipping Market Report 17082011Document18 pagesShipping Market Report 17082011bleuwinzNo ratings yet

- SRJ Aug Sep 2009Document76 pagesSRJ Aug Sep 2009majdirossrossNo ratings yet

- Po 20140910Document30 pagesPo 20140910mcontrerjNo ratings yet

- Willis Energy Market Review 2013 PDFDocument92 pagesWillis Energy Market Review 2013 PDFsushilk28No ratings yet

- Insights Reg PlantationsDocument69 pagesInsights Reg PlantationsNasya YenitaNo ratings yet

- Daily Market ReportDocument1 pageDaily Market ReportSmitha MohanNo ratings yet

- Polymerscan: Americas Polymer Spot Price AssessmentsDocument29 pagesPolymerscan: Americas Polymer Spot Price AssessmentsmcontrerjNo ratings yet

- Euro Gas DailyDocument8 pagesEuro Gas DailyJose DenizNo ratings yet

- Drimcgrawhill - Platts - Oilgram Price Report Nov 96Document12 pagesDrimcgrawhill - Platts - Oilgram Price Report Nov 96Cristhian AymaNo ratings yet

- AMR SummaryDocument37 pagesAMR SummaryChatkamol KaewbuddeeNo ratings yet

- SSY Chemical WeeklyDocument3 pagesSSY Chemical WeeklyBeytullah KokoçNo ratings yet

- Ihs Markit Is SectorsDocument2 pagesIhs Markit Is SectorsKapilanNavaratnamNo ratings yet

- Opr 20181205Document32 pagesOpr 20181205rojovies24No ratings yet

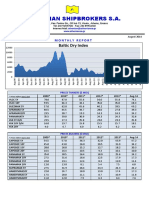

- Athenian Shipbrokers - Monthy Report - 14.08.15Document17 pagesAthenian Shipbrokers - Monthy Report - 14.08.15georgevarsasNo ratings yet

- Monthly Oil Market Report - Feb 2023Document24 pagesMonthly Oil Market Report - Feb 2023asaNo ratings yet

- LPGDocument15 pagesLPGMilkiss SweetNo ratings yet

- DynaLiners Weekly 49-2015Document12 pagesDynaLiners Weekly 49-2015Somayajula SuryaramNo ratings yet

- Platts 2020 Outlook Report PDFDocument21 pagesPlatts 2020 Outlook Report PDFKamal ShayedNo ratings yet

- Platts LPG Gaswire 23082013Document6 pagesPlatts LPG Gaswire 23082013udelmarkNo ratings yet

- Market ScanDocument23 pagesMarket ScanGhasem2010No ratings yet

- Oil Gram Price ReportDocument15 pagesOil Gram Price ReportIppo MakunouchiNo ratings yet

- LW 20180731Document10 pagesLW 20180731Victor FernandezNo ratings yet

- LNG 20150116Document11 pagesLNG 20150116Rajeshkumar ElangoNo ratings yet

- Chemical Forecaster Exec Summary TOCDocument12 pagesChemical Forecaster Exec Summary TOCalgeriacandaNo ratings yet

- QA Monthly Report 2022-09 SeptemberDocument32 pagesQA Monthly Report 2022-09 SeptemberMark Mirosevic-SorgoNo ratings yet

- Argus Freight PDFDocument11 pagesArgus Freight PDFdonidinattaNo ratings yet

- Shell Trading (US) Company v. Lion Oil Trading & Transportation, Inc.Document11 pagesShell Trading (US) Company v. Lion Oil Trading & Transportation, Inc.Alyssa Marie MartinezNo ratings yet

- Shipping Intelligence 26.novDocument20 pagesShipping Intelligence 26.novleejingsongNo ratings yet

- Vam PricesDocument28 pagesVam PricesMandar J DeshpandeNo ratings yet

- Dry Bulk Research 9sep16Document13 pagesDry Bulk Research 9sep16Takis RappasNo ratings yet

- The Worlds Top Ship Broking FirmsDocument2 pagesThe Worlds Top Ship Broking Firmsjikkuabraham2No ratings yet

- Coal Outlook ReportDocument51 pagesCoal Outlook ReportSterios SouyoutzoglouNo ratings yet

- Argus: Coal Daily InternationalDocument15 pagesArgus: Coal Daily InternationalUmang KadivarNo ratings yet

- Polymerscan: Americas Polymer Spot Price AssessmentsDocument28 pagesPolymerscan: Americas Polymer Spot Price AssessmentsmcontrerjNo ratings yet

- Aldorf Presentation 5th World LNG August 31Document29 pagesAldorf Presentation 5th World LNG August 31stavros7No ratings yet

- Indonesia Palm Oil: Sector BriefingDocument40 pagesIndonesia Palm Oil: Sector BriefingatanmasriNo ratings yet

- Report 1Document50 pagesReport 1qwerty1991srNo ratings yet

- Shipping Market Fearnleys Week 52Document1 pageShipping Market Fearnleys Week 52VizziniNo ratings yet

- Crude PricingDocument15 pagesCrude PricingGirish1412No ratings yet

- Chemf 2007 2Document120 pagesChemf 2007 2Anupam AsthanaNo ratings yet

- International Thermodynamic Tables of the Fluid State: Propylene (Propene)From EverandInternational Thermodynamic Tables of the Fluid State: Propylene (Propene)No ratings yet

- Intermodal Weekly 16-2013Document8 pagesIntermodal Weekly 16-2013Wisnu KertaningnagoroNo ratings yet

- IMP Market Outlook SRODocument22 pagesIMP Market Outlook SRObhavin183No ratings yet

- MLC 2006 - Onboard Complaint PDFDocument2 pagesMLC 2006 - Onboard Complaint PDFWisnu KertaningnagoroNo ratings yet

- Teardrops in The Rain (Chords) by CNBlueDocument2 pagesTeardrops in The Rain (Chords) by CNBlueWisnu KertaningnagoroNo ratings yet

- 5.3.3 HIRADC For Lifting and Installation of Container and Chiller (04!06!14)Document3 pages5.3.3 HIRADC For Lifting and Installation of Container and Chiller (04!06!14)Wisnu KertaningnagoroNo ratings yet

- 5.3.2 MOC-Installing Portable Container and ChillerDocument1 page5.3.2 MOC-Installing Portable Container and ChillerWisnu KertaningnagoroNo ratings yet

- Winposh Rampart Towing - Vertical & Horizontal Transvere Force Stated On Stability ...Document1 pageWinposh Rampart Towing - Vertical & Horizontal Transvere Force Stated On Stability ...Wisnu KertaningnagoroNo ratings yet

- Coshh Basics - CoshhDocument2 pagesCoshh Basics - CoshhWisnu Kertaningnagoro100% (1)

- Methodology For Calculating The Energy Performance of Buildings - Riigi TeatajaDocument3 pagesMethodology For Calculating The Energy Performance of Buildings - Riigi TeatajaWisnu Kertaningnagoro100% (1)

- Environmental Ship Index 1Document2 pagesEnvironmental Ship Index 1Wisnu KertaningnagoroNo ratings yet

- Example COSHH Risk Assessment - Warehouse - COSHHDocument2 pagesExample COSHH Risk Assessment - Warehouse - COSHHWisnu KertaningnagoroNo ratings yet

- Example COSHH Risk Assessment - Office - COSHHDocument2 pagesExample COSHH Risk Assessment - Office - COSHHWisnu Kertaningnagoro100% (1)

- Home Products Minerals & Metallurgy Steel Steel SheetsDocument13 pagesHome Products Minerals & Metallurgy Steel Steel SheetsWisnu KertaningnagoroNo ratings yet

- PSV Charter Rate 2Document2 pagesPSV Charter Rate 2Wisnu KertaningnagoroNo ratings yet

- Electrical SystemDocument283 pagesElectrical Systemzed shop73100% (1)

- Class 2Document21 pagesClass 2md sakhwat hossainNo ratings yet

- H B F CDocument22 pagesH B F Capi-3745637100% (1)

- BA 501-Text AnalyticsDocument2 pagesBA 501-Text AnalyticsTanisha AgarwalNo ratings yet

- Case Study On Four WheelerDocument35 pagesCase Study On Four WheelerViŠhål PätělNo ratings yet

- Emi01 2013Document14 pagesEmi01 2013Universal Music CanadaNo ratings yet

- Occupational Health Hazards Due To Mine Dust: Unit-14Document9 pagesOccupational Health Hazards Due To Mine Dust: Unit-14Dinesh dhakarNo ratings yet

- SAFe Foundations (v4.0.6)Document33 pagesSAFe Foundations (v4.0.6)PoltakJeffersonPandianganNo ratings yet

- Setting of CementDocument15 pagesSetting of Cementverma jiNo ratings yet

- Taxpayers' Tax Compliance Behavior - Business Profit Taxpayers' of Addis Ababa City AdministrationDocument126 pagesTaxpayers' Tax Compliance Behavior - Business Profit Taxpayers' of Addis Ababa City AdministrationGELETAW TSEGAW80% (5)

- Differential Amplifier: Mrs.V.Srirenganachiyar, Ap/Ece Ramco Institute of Technology Academic Year:2017-2018 (Odd)Document13 pagesDifferential Amplifier: Mrs.V.Srirenganachiyar, Ap/Ece Ramco Institute of Technology Academic Year:2017-2018 (Odd)Hitlar MamaNo ratings yet

- Sil ReviewDocument19 pagesSil Reviewtrung2i100% (1)

- HMT306 Food Processing and PreservationDocument431 pagesHMT306 Food Processing and Preservationgumnani.rewachandNo ratings yet

- Computer Science #3Document356 pagesComputer Science #3Sean s Chipanga100% (1)

- The Potential and Challenges of Dairy Products in The Malaysian Market 2015Document99 pagesThe Potential and Challenges of Dairy Products in The Malaysian Market 2015Hương ChiêmNo ratings yet

- Automated Packaging Machine Using PLCDocument7 pagesAutomated Packaging Machine Using PLCTimothy FieldsNo ratings yet

- AB-3P BrochureDocument12 pagesAB-3P Brochurealisya.blwsNo ratings yet

- Lecture6 FinalDocument43 pagesLecture6 FinalcmlimNo ratings yet

- Understanding Entrepreneurship: A Case Study On Ms. Namita Sharma "The Queen of NFH"Document3 pagesUnderstanding Entrepreneurship: A Case Study On Ms. Namita Sharma "The Queen of NFH"International Journal of Application or Innovation in Engineering & Management100% (1)

- Catalytic Distillation VersionDocument4 pagesCatalytic Distillation Versionlux0008No ratings yet

- Installation Guide C175-C172 All Models Appendix C 242 Rev BDocument52 pagesInstallation Guide C175-C172 All Models Appendix C 242 Rev BJonathan Miguel Gómez MogollónNo ratings yet

- Christian Eminent College: Department of Computer Science and ElectronicsDocument6 pagesChristian Eminent College: Department of Computer Science and Electronicsfake id1No ratings yet

- Dacasin Vs DacasinDocument1 pageDacasin Vs DacasinJulian DubaNo ratings yet

- General InformationDocument4 pagesGeneral InformationSonthi MooljindaNo ratings yet

- Social Network Theory: March 2017Document13 pagesSocial Network Theory: March 2017mariam ikramNo ratings yet

- Personalised Mobile Health and Fitness Apps: Lessons Learned From Myfitnesscompanion®Document11 pagesPersonalised Mobile Health and Fitness Apps: Lessons Learned From Myfitnesscompanion®sayed shahabuddin AdeebNo ratings yet

- ExcaDrill 45A DF560L DatasheetDocument2 pagesExcaDrill 45A DF560L DatasheetИгорь ИвановNo ratings yet