Download as pdf or txt

You might also like

- Corporate FinanceDocument310 pagesCorporate Financeaditya.c122No ratings yet

- Case Study 1 - FaircentDocument4 pagesCase Study 1 - FaircentSneha Banerjee100% (1)

- Project Financing... NotesDocument21 pagesProject Financing... NotesRoney Raju Philip75% (4)

- Case Project FinanceDocument9 pagesCase Project FinanceaamritaaNo ratings yet

- Assignment 1Document2 pagesAssignment 1meray8100% (2)

- AFME Guide To Infrastructure FinancingDocument99 pagesAFME Guide To Infrastructure Financingfunction_analysisNo ratings yet

- What's Holding Back European Securitization Issuance?: Structured FinanceDocument9 pagesWhat's Holding Back European Securitization Issuance?: Structured Financeapi-228714775No ratings yet

- Financial Modelling For A ProjectDocument8 pagesFinancial Modelling For A ProjectKingsley Chika NwangwuNo ratings yet

- Prudential Regulation Authority: Bank of EnglandDocument2 pagesPrudential Regulation Authority: Bank of EnglandCrowdfundInsiderNo ratings yet

- Investing in Infrastructure: Are Insurers Ready To Fill The Funding Gap?Document16 pagesInvesting in Infrastructure: Are Insurers Ready To Fill The Funding Gap?api-228714775No ratings yet

- Credit Availability For SMEs in The Crisis: Which Role For The European Investment Bank Group?Document21 pagesCredit Availability For SMEs in The Crisis: Which Role For The European Investment Bank Group?Francesco LiucciNo ratings yet

- Pfi Credit CrisisDocument37 pagesPfi Credit CrisisgammaslideNo ratings yet

- Underwriting The Recovery: Growth in European Shadow Banking Is Unlikely To Offset Bank DeleveragingDocument14 pagesUnderwriting The Recovery: Growth in European Shadow Banking Is Unlikely To Offset Bank Deleveragingapi-228714775No ratings yet

- European Covered Bonds Face Favorable Regulatory Treatment in 2014, But Underlying Risks RemainDocument10 pagesEuropean Covered Bonds Face Favorable Regulatory Treatment in 2014, But Underlying Risks Remainapi-231665846No ratings yet

- Project FinafmnceDocument13 pagesProject FinafmnceMahantesh BalekundriNo ratings yet

- Crowdfunding Industry To EU Open Letter-2012.12.14Document2 pagesCrowdfunding Industry To EU Open Letter-2012.12.14Eric_IngargiolaNo ratings yet

- EY Commercial Real Estate DebtDocument16 pagesEY Commercial Real Estate DebtPaul BalbinNo ratings yet

- Investment BankingDocument3 pagesInvestment BankingEdho TenseiNo ratings yet

- EC Regulation For Money Market Funds May Have Unintended ConsequencesDocument22 pagesEC Regulation For Money Market Funds May Have Unintended Consequencesapi-231665846No ratings yet

- The Business Models and Economics of Peer-to-Peer LendingDocument36 pagesThe Business Models and Economics of Peer-to-Peer LendingkhuongNo ratings yet

- Private Finance Initiative (Pfi) For Road Projects in Uk: Current Practice With A Case StudyDocument9 pagesPrivate Finance Initiative (Pfi) For Road Projects in Uk: Current Practice With A Case StudySky walkingNo ratings yet

- Accredited by NAAC With B Grade Permanently Affiliated To University 0f Mumbai An ISO 9001:2008 Certified CollegeDocument64 pagesAccredited by NAAC With B Grade Permanently Affiliated To University 0f Mumbai An ISO 9001:2008 Certified CollegeAashika ShahNo ratings yet

- Australian Infrastructure Funding: Making StridesDocument5 pagesAustralian Infrastructure Funding: Making Stridesapi-239404108No ratings yet

- Project Financing-Lenders PerspectiveDocument26 pagesProject Financing-Lenders PerspectiveUsman Aziz Khan100% (1)

- Written Evidence Submitted by Pension Insurance Corporation PLC and New Financial LLPDocument8 pagesWritten Evidence Submitted by Pension Insurance Corporation PLC and New Financial LLPjohn.s.ajagbeNo ratings yet

- Do Lenders Cross Subsidise Loans by Selling Payment Protection InsuranceDocument19 pagesDo Lenders Cross Subsidise Loans by Selling Payment Protection InsuranceSubhadip GhoshNo ratings yet

- Despite Relatively Calmer Markets, Systemic and Specific Funding Risks For Banks Have Not Gone AwayDocument17 pagesDespite Relatively Calmer Markets, Systemic and Specific Funding Risks For Banks Have Not Gone Awayapi-227433089No ratings yet

- S&P Etude Bâle III Et Solva IIDocument14 pagesS&P Etude Bâle III Et Solva IIclechantreNo ratings yet

- Standard and Poor Document Need To Read For IPFDocument17 pagesStandard and Poor Document Need To Read For IPFza1891No ratings yet

- Master Thesis TopicsDocument58 pagesMaster Thesis TopicsNauman Shafiq100% (2)

- Financing and Investing in Infrastructure Week 1 SlidesDocument39 pagesFinancing and Investing in Infrastructure Week 1 SlidesNeindow Hassan YakubuNo ratings yet

- 2014 Safe Report - en PDFDocument170 pages2014 Safe Report - en PDFionutzz_ianisNo ratings yet

- Fsug Opinions 190408 Responsible Consumer Credit Lending enDocument24 pagesFsug Opinions 190408 Responsible Consumer Credit Lending enjmalemanyNo ratings yet

- Synopsis Summer Internship ProjectDocument7 pagesSynopsis Summer Internship ProjectVedanth ChoudharyNo ratings yet

- Project Finance Risk ManagementDocument10 pagesProject Finance Risk ManagementAfrid ArafNo ratings yet

- Bvpi-Abip-green Paper Lti - ResponsepdfDocument5 pagesBvpi-Abip-green Paper Lti - ResponsepdfpensiontalkNo ratings yet

- Private Equity: A Discussion of Risk and Regulatory EngagementDocument30 pagesPrivate Equity: A Discussion of Risk and Regulatory EngagementYun MaNo ratings yet

- Irish Spvs Emir and DerivativesDocument31 pagesIrish Spvs Emir and Derivativesjohn pynchonNo ratings yet

- Epec State Guarantees in Ppps PublicDocument40 pagesEpec State Guarantees in Ppps PublicAluscia76No ratings yet

- Unlocking SME Finance Through Market Based DebtDocument103 pagesUnlocking SME Finance Through Market Based DebtFif SmithNo ratings yet

- Sharing Deal Insight: European Financial Services M&A News and Views From PWCDocument5 pagesSharing Deal Insight: European Financial Services M&A News and Views From PWCvm7489No ratings yet

- 1 Pre Read For Introductions To Project FinancingDocument4 pages1 Pre Read For Introductions To Project FinancingChanchal MisraNo ratings yet

- Project Finance Summary Debt Rating Criteria-S&P PDFDocument17 pagesProject Finance Summary Debt Rating Criteria-S&P PDFReisha Ananda PutriNo ratings yet

- Mongolia Development Module FSADocument17 pagesMongolia Development Module FSAAltansukhDamdinsurenNo ratings yet

- TET 407 - Energy Financing & TradingDocument31 pagesTET 407 - Energy Financing & TradingMonterez SalvanoNo ratings yet

- European Systemic Risk Board, Report On Commercial Real Estate and Financial Stability in The EU, December 2015Document77 pagesEuropean Systemic Risk Board, Report On Commercial Real Estate and Financial Stability in The EU, December 2015hulei1114No ratings yet

- Investment barriers in the European Union 2023: A report by the European Investment BankFrom EverandInvestment barriers in the European Union 2023: A report by the European Investment BankNo ratings yet

- Vol - 14 2 4Document20 pagesVol - 14 2 4Abdiman HabiboNo ratings yet

- FM Assignment AnswersDocument4 pagesFM Assignment Answerskarteekay negiNo ratings yet

- Eca and Project FinanceDocument6 pagesEca and Project FinancedanielparkNo ratings yet

- Financial Risk and Its Mitigation PDFDocument19 pagesFinancial Risk and Its Mitigation PDFDEBALINA SENNo ratings yet

- European Capital Markets UnionDocument14 pagesEuropean Capital Markets UnionSurendranNo ratings yet

- Project Report of Financial Institution - 2019 PDFDocument91 pagesProject Report of Financial Institution - 2019 PDFBhakti GoswamiNo ratings yet

- Corporate Bonds Market in Pakistan - Business FinanceDocument19 pagesCorporate Bonds Market in Pakistan - Business FinanceAfzal Hanif100% (1)

- 2014 EY European Insurance Outlook: Unlock New Opportunities, Simplify Existing OperationsDocument12 pages2014 EY European Insurance Outlook: Unlock New Opportunities, Simplify Existing Operationsapi-247693317No ratings yet

- Onthee Credit Quality of Project Financing: Ffect of Green Bonds On The Profitability andDocument23 pagesOnthee Credit Quality of Project Financing: Ffect of Green Bonds On The Profitability andhzulqadadarNo ratings yet

- Private Credit White Paper 2021 (8.23.21)Document10 pagesPrivate Credit White Paper 2021 (8.23.21)gm9sfwdmfdNo ratings yet

- Week 1 Practice Questions Solution-2Document5 pagesWeek 1 Practice Questions Solution-2Caroline FrisciliaNo ratings yet

- Inderst and Ottaviani 2012 Regulating Financial AdviceDocument11 pagesInderst and Ottaviani 2012 Regulating Financial Adviceian.robertsNo ratings yet

- Unlocking Capital: How to Structure Bankable and Bondable ProjectsFrom EverandUnlocking Capital: How to Structure Bankable and Bondable ProjectsNo ratings yet

- Latvia Long-Term Rating Raised To 'A-' On Strong Growth and Fiscal Performance Outlook StableDocument8 pagesLatvia Long-Term Rating Raised To 'A-' On Strong Growth and Fiscal Performance Outlook Stableapi-228714775No ratings yet

- Investing in Infrastructure: Are Insurers Ready To Fill The Funding Gap?Document16 pagesInvesting in Infrastructure: Are Insurers Ready To Fill The Funding Gap?api-228714775No ratings yet

- Ireland Upgraded To 'A-' On Improved Domestic Prospects Outlook PositiveDocument9 pagesIreland Upgraded To 'A-' On Improved Domestic Prospects Outlook Positiveapi-228714775No ratings yet

- Romania Upgraded To 'BBB-/A-3' On Pace of External Adjustments Outlook StableDocument7 pagesRomania Upgraded To 'BBB-/A-3' On Pace of External Adjustments Outlook Stableapi-228714775No ratings yet

- A Strong Shekel and A Weak Construction Sector Are Holding Back Israel's EconomyDocument10 pagesA Strong Shekel and A Weak Construction Sector Are Holding Back Israel's Economyapi-228714775No ratings yet

- What's Holding Back European Securitization Issuance?: Structured FinanceDocument9 pagesWhat's Holding Back European Securitization Issuance?: Structured Financeapi-228714775No ratings yet

- Securitization Regulation in Focus: Proposed Liquidity Rules Have Softened, But May Still Deter European Bank InvestorsDocument8 pagesSecuritization Regulation in Focus: Proposed Liquidity Rules Have Softened, But May Still Deter European Bank Investorsapi-228714775No ratings yet

- UntitledDocument53 pagesUntitledapi-228714775No ratings yet

- Infrastructure Development Holds The Key To Two African Sovereigns' Resource-Led FuturesDocument8 pagesInfrastructure Development Holds The Key To Two African Sovereigns' Resource-Led Futuresapi-228714775No ratings yet

- Outlook On Portugal Revised To Stable From Negative On Economic and Fiscal Stabilization 'BB/B' Ratings AffirmedDocument9 pagesOutlook On Portugal Revised To Stable From Negative On Economic and Fiscal Stabilization 'BB/B' Ratings Affirmedapi-228714775No ratings yet

- UntitledDocument14 pagesUntitledapi-228714775No ratings yet

- European Corporate Credit Outlook: Warming UpDocument60 pagesEuropean Corporate Credit Outlook: Warming Upapi-228714775No ratings yet

- European Structured Finance 12-Month Rolling Default Level Drops To Its Lowest Since Mid-2010Document14 pagesEuropean Structured Finance 12-Month Rolling Default Level Drops To Its Lowest Since Mid-2010api-228714775No ratings yet

- S&P Forum To Explore Opportunities and Challenges in Saudi Debt Capital MarketsDocument2 pagesS&P Forum To Explore Opportunities and Challenges in Saudi Debt Capital Marketsapi-228714775No ratings yet

- Russia Foreign Currency Ratings Lowered To 'BBB-/A-3' On Risk of Marked Deterioration in External Financing Outlook NegDocument9 pagesRussia Foreign Currency Ratings Lowered To 'BBB-/A-3' On Risk of Marked Deterioration in External Financing Outlook Negapi-228714775No ratings yet

- Inside Credit: Leveraged Credit Conditions in Europe Become Increasingly Stretched As Investor Demand Outstrips SupplyDocument10 pagesInside Credit: Leveraged Credit Conditions in Europe Become Increasingly Stretched As Investor Demand Outstrips Supplyapi-228714775No ratings yet

- Assess Macroeconomic Policies Which Might Be Used To Respond To Rising Commodity Prices During A Period of Slow Economic GrowthDocument2 pagesAssess Macroeconomic Policies Which Might Be Used To Respond To Rising Commodity Prices During A Period of Slow Economic GrowthJamie HaywoodNo ratings yet

- Mena Full Deck 20161109Document106 pagesMena Full Deck 20161109rezaNo ratings yet

- AR CL 2018 4 10 VF PDFDocument436 pagesAR CL 2018 4 10 VF PDFWike WidyanitaNo ratings yet

- Preparation of Detailed Area Plan (DAP) For DMDPDocument132 pagesPreparation of Detailed Area Plan (DAP) For DMDPMasud Rana60% (5)

- S L Kapur CommitteeDocument92 pagesS L Kapur CommitteeAjit RunwalNo ratings yet

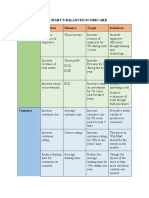

- Wal-Mart's Balanced ScorecardDocument3 pagesWal-Mart's Balanced ScorecardCấn Thu HuyềnNo ratings yet

- Westernacher Consulting Global Roll Out Presentation enDocument18 pagesWesternacher Consulting Global Roll Out Presentation enStelioEduardoMucaveleNo ratings yet

- Treasury Management Fasa SF A F 1rf1f Qs Q F A A Qu Qu SF QF Uqwf Qu Qu Quqw F C Q1wag DFB BDocument21 pagesTreasury Management Fasa SF A F 1rf1f Qs Q F A A Qu Qu SF QF Uqwf Qu Qu Quqw F C Q1wag DFB BhoangthingoclinhNo ratings yet

- Market Economy: Private PropertyDocument2 pagesMarket Economy: Private PropertyThe Grizzled VetNo ratings yet

- 17 GDR FCCB and Qip Procedures Legal PerspectivesDocument5 pages17 GDR FCCB and Qip Procedures Legal Perspectivesdg270872No ratings yet

- Kec Internatinal Ltd.Document14 pagesKec Internatinal Ltd.Rahul RathoreNo ratings yet

- Module 1 - Handout 5eDocument90 pagesModule 1 - Handout 5epi_31415No ratings yet

- Moneyball Movie Assignment MGT427Document4 pagesMoneyball Movie Assignment MGT427Fahim SheikhNo ratings yet

- Module-3 IFSS-NoteDocument29 pagesModule-3 IFSS-NoteAbhisekNo ratings yet

- Greeks (Finance)Document6 pagesGreeks (Finance)lalasnoopyNo ratings yet

- Colombia and Free Trade Agreements: Between Mobilisation and ConflictDocument9 pagesColombia and Free Trade Agreements: Between Mobilisation and ConflictLaauu KaasteellaanosNo ratings yet

- Closing Operations: Foreign Currency ValuationDocument17 pagesClosing Operations: Foreign Currency Valuationsamirkumar s4sahooNo ratings yet

- The Home DepotDocument30 pagesThe Home DepotParveen BariNo ratings yet

- 2820 MT Ephraim Avenue, LLCDocument14 pages2820 MT Ephraim Avenue, LLCPro Business PlansNo ratings yet

- Unit 2Document15 pagesUnit 2Maithra DNo ratings yet

- Investments 3Document5 pagesInvestments 3Marinel AbrilNo ratings yet

- Birla Institute of Technology: Master of Business AdministrationDocument16 pagesBirla Institute of Technology: Master of Business Administrationdixit_abhishek_neoNo ratings yet

- Zilveren Kruis Application FormDocument2 pagesZilveren Kruis Application FormwangchanghuiNo ratings yet

- ENT 300 PresentationDocument51 pagesENT 300 PresentationSuraya IbrahimNo ratings yet

- FELDADocument93 pagesFELDACj Lee100% (2)

- Market Correlation Market Returns and Po PDFDocument868 pagesMarket Correlation Market Returns and Po PDFAlina MoiseNo ratings yet

- Hospitality Industry Oman AsDocument7 pagesHospitality Industry Oman AsArshad ShahzadNo ratings yet

- The Company That You Manage Has InvestedDocument2 pagesThe Company That You Manage Has InvestedtahmeemNo ratings yet