Market Outlook: Dealer's Diary

Market Outlook: Dealer's Diary

You might also like

- Stock Market Technique No.1Document120 pagesStock Market Technique No.1sandipgarg100% (12)

- Fiscal Aspects Aviation ManagementDocument298 pagesFiscal Aspects Aviation Managementgcarl_8420909560% (1)

- Final Project On PMSDocument34 pagesFinal Project On PMSNiteesh Singh Rajput0% (1)

- Hilton Hotels Case StudyDocument16 pagesHilton Hotels Case StudyRebecca PaceNo ratings yet

- Bolsen PharmaceuticalsDocument7 pagesBolsen PharmaceuticalswhitewitchNo ratings yet

- Coca Cola CompanyDocument36 pagesCoca Cola CompanyDennis Edwin KasooNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument9 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 25th January 2013Document16 pagesMarket Outlook, 25th January 2013Angel BrokingNo ratings yet

- Market Outlook, 5th February, 2013Document15 pagesMarket Outlook, 5th February, 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument10 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 11th February, 2013Document21 pagesMarket Outlook, 11th February, 2013Angel BrokingNo ratings yet

- Market Outlook Report, 21st JanuaryDocument9 pagesMarket Outlook Report, 21st JanuaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 3rd May 2012Document13 pagesMarket Outlook 3rd May 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 21st February, 2013Document14 pagesMarket Outlook, 21st February, 2013Angel BrokingNo ratings yet

- Market Outlook, 7th February, 2013Document19 pagesMarket Outlook, 7th February, 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 30th April 2012Document16 pagesMarket Outlook 30th April 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryArun ShekharNo ratings yet

- Market Outlook 19th January 2012Document8 pagesMarket Outlook 19th January 2012Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument4 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryangelbrokingNo ratings yet

- Market Outlook, 20-05-13Document15 pagesMarket Outlook, 20-05-13Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument11 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook Market Outlook: Dealer's DiaryangelbrokingNo ratings yet

- Exide Industries, 1Q FY 2014Document12 pagesExide Industries, 1Q FY 2014Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Hitachi Home & Life Solutions: Performance HighlightsDocument13 pagesHitachi Home & Life Solutions: Performance HighlightsAngel BrokingNo ratings yet

- Market Outlook 8th February 2012Document9 pagesMarket Outlook 8th February 2012Angel BrokingNo ratings yet

- Market Outlook 9th August 2011Document6 pagesMarket Outlook 9th August 2011Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- United Spirits 4Q FY 2013Document10 pagesUnited Spirits 4Q FY 2013Angel BrokingNo ratings yet

- Market Outlook Report, 22nd JanuaryDocument16 pagesMarket Outlook Report, 22nd JanuaryAngel BrokingNo ratings yet

- Market Outlook 27th April 2012Document7 pagesMarket Outlook 27th April 2012Angel BrokingNo ratings yet

- FAG Bearings Result UpdatedDocument10 pagesFAG Bearings Result UpdatedAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Dishman, 12th February, 2013Document10 pagesDishman, 12th February, 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument24 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Dishman 2QFY2013RUDocument10 pagesDishman 2QFY2013RUAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Performance Highlights: Company Update - AutomobileDocument13 pagesPerformance Highlights: Company Update - AutomobileZacharia VincentNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Investigation, Guard & Armored Car Service Revenues World Summary: Market Values & Financials by CountryFrom EverandInvestigation, Guard & Armored Car Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Medical Equipment Rental & Leasing Revenues World Summary: Market Values & Financials by CountryFrom EverandMedical Equipment Rental & Leasing Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Oilseeds and Edible Oil UpdateDocument9 pagesOilseeds and Edible Oil UpdateAngel BrokingNo ratings yet

- WPIInflation August2013Document5 pagesWPIInflation August2013Angel BrokingNo ratings yet

- Ranbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertDocument4 pagesRanbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertAngel BrokingNo ratings yet

- International Commodities Evening Update September 16 2013Document3 pagesInternational Commodities Evening Update September 16 2013Angel BrokingNo ratings yet

- Daily Agri Tech Report September 14 2013Document2 pagesDaily Agri Tech Report September 14 2013Angel BrokingNo ratings yet

- Currency Daily Report September 16 2013Document4 pagesCurrency Daily Report September 16 2013Angel BrokingNo ratings yet

- Daily Metals and Energy Report September 16 2013Document6 pagesDaily Metals and Energy Report September 16 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5913)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5913)Angel Broking100% (1)

- Daily Agri Tech Report September 16 2013Document2 pagesDaily Agri Tech Report September 16 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Daily Agri Report September 16 2013Document9 pagesDaily Agri Report September 16 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19733) / NIFTY (5851)Document4 pagesDaily Technical Report: Sensex (19733) / NIFTY (5851)Angel BrokingNo ratings yet

- Tata Motors: Jaguar Land Rover - Monthly Sales UpdateDocument6 pagesTata Motors: Jaguar Land Rover - Monthly Sales UpdateAngel BrokingNo ratings yet

- Derivatives Report 8th JanDocument3 pagesDerivatives Report 8th JanAngel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 13Document2 pagesMetal and Energy Tech Report Sept 13Angel BrokingNo ratings yet

- Press Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressDocument1 pagePress Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressAngel BrokingNo ratings yet

- Jaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechDocument4 pagesJaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechAngel BrokingNo ratings yet

- Currency Daily Report September 13 2013Document4 pagesCurrency Daily Report September 13 2013Angel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 12Document2 pagesMetal and Energy Tech Report Sept 12Angel BrokingNo ratings yet

- Currency Daily Report September 12 2013Document4 pagesCurrency Daily Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Daily Agri Report September 12 2013Document9 pagesDaily Agri Report September 12 2013Angel BrokingNo ratings yet

- Daily Metals and Energy Report September 12 2013Document6 pagesDaily Metals and Energy Report September 12 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5897)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5897)Angel BrokingNo ratings yet

- Daily Agri Tech Report September 12 2013Document2 pagesDaily Agri Tech Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- A Study On Customer Preference and Satisfaction Towards Bajaj BikesDocument110 pagesA Study On Customer Preference and Satisfaction Towards Bajaj BikesAjay Savaliya83% (18)

- Domestic Bank Swift CodesDocument12 pagesDomestic Bank Swift CodesSHAKEEL IQBALNo ratings yet

- FRTB Ey ReviewDocument8 pagesFRTB Ey Review4GetM100% (1)

- 10000027359Document38 pages10000027359Chapter 11 DocketsNo ratings yet

- Risk Management: Best PracticeDocument19 pagesRisk Management: Best PracticeTrai SwatdikunNo ratings yet

- Full Art. 1800 - 1842Document10 pagesFull Art. 1800 - 1842Tia LiNo ratings yet

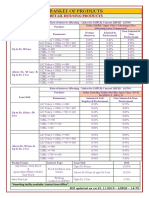

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaNo ratings yet

- Pagadian Commercial PDFDocument20 pagesPagadian Commercial PDFAsher TeogangcoNo ratings yet

- Mortgage Deed SavarkundlaDocument8 pagesMortgage Deed Savarkundladkumar471No ratings yet

- Eclectica Agriculture Fund Feb 2015Document2 pagesEclectica Agriculture Fund Feb 2015CanadianValueNo ratings yet

- Chapter - 8: Sub-Division of Joural:CashbookDocument11 pagesChapter - 8: Sub-Division of Joural:CashbookFaraz AliNo ratings yet

- Coco Life Audited Financial Statement 2014Document95 pagesCoco Life Audited Financial Statement 2014Angel PortosaNo ratings yet

- Pricing: Summary of Questions by Objectives and Bloom'S TaxonomyDocument43 pagesPricing: Summary of Questions by Objectives and Bloom'S TaxonomyJelly AnneNo ratings yet

- DbmsDocument29 pagesDbmsCarla Marielle CruzNo ratings yet

- 1 12 Integrated Marketing Communications Evaluation Case Study Colgate Cibaca The Road Ahead... (Courtesy FCB Ulka Comstrat 2006) Case OutlineDocument12 pages1 12 Integrated Marketing Communications Evaluation Case Study Colgate Cibaca The Road Ahead... (Courtesy FCB Ulka Comstrat 2006) Case OutlineNeha NaliniNo ratings yet

- Sfar 88 Airbus-Modification List Jan 08Document16 pagesSfar 88 Airbus-Modification List Jan 08Poshak Prasad GnawaliNo ratings yet

- Accounts Made EasyDocument9 pagesAccounts Made EasyPrashant KunduNo ratings yet

- What Is Company? Adminstration of Company LawDocument10 pagesWhat Is Company? Adminstration of Company Lawradhika77799100% (1)

- Fund Factsheets - IndividualDocument57 pagesFund Factsheets - IndividualRam KumarNo ratings yet

- What Is Global StrategyDocument7 pagesWhat Is Global StrategySonika MishraNo ratings yet

- Audi Nachhaltigkeitsbericht EN 2017 PDFDocument87 pagesAudi Nachhaltigkeitsbericht EN 2017 PDF꧁ Diego Breeze Martínez꧂No ratings yet

- How Traditional Firms Must Compete in The Sharing EconomyDocument4 pagesHow Traditional Firms Must Compete in The Sharing EconomyJorgeNo ratings yet

- 2015 Saln Form-From CSCDocument3 pages2015 Saln Form-From CSCRowel Magsino GonzalesNo ratings yet

- Reviewer ParcorpDocument2 pagesReviewer ParcorpLyka TejadaNo ratings yet

Download as pdf or txt

You might also like

- Stock Market Technique No.1Document120 pagesStock Market Technique No.1sandipgarg100% (12)

- Fiscal Aspects Aviation ManagementDocument298 pagesFiscal Aspects Aviation Managementgcarl_8420909560% (1)

- Final Project On PMSDocument34 pagesFinal Project On PMSNiteesh Singh Rajput0% (1)

- Hilton Hotels Case StudyDocument16 pagesHilton Hotels Case StudyRebecca PaceNo ratings yet

- Bolsen PharmaceuticalsDocument7 pagesBolsen PharmaceuticalswhitewitchNo ratings yet

- Coca Cola CompanyDocument36 pagesCoca Cola CompanyDennis Edwin KasooNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument9 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 25th January 2013Document16 pagesMarket Outlook, 25th January 2013Angel BrokingNo ratings yet

- Market Outlook, 5th February, 2013Document15 pagesMarket Outlook, 5th February, 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument10 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 11th February, 2013Document21 pagesMarket Outlook, 11th February, 2013Angel BrokingNo ratings yet

- Market Outlook Report, 21st JanuaryDocument9 pagesMarket Outlook Report, 21st JanuaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 3rd May 2012Document13 pagesMarket Outlook 3rd May 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook, 21st February, 2013Document14 pagesMarket Outlook, 21st February, 2013Angel BrokingNo ratings yet

- Market Outlook, 7th February, 2013Document19 pagesMarket Outlook, 7th February, 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook 30th April 2012Document16 pagesMarket Outlook 30th April 2012Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryArun ShekharNo ratings yet

- Market Outlook 19th January 2012Document8 pagesMarket Outlook 19th January 2012Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument4 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryangelbrokingNo ratings yet

- Market Outlook, 20-05-13Document15 pagesMarket Outlook, 20-05-13Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument16 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument11 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument14 pagesMarket Outlook Market Outlook: Dealer's DiaryangelbrokingNo ratings yet

- Exide Industries, 1Q FY 2014Document12 pagesExide Industries, 1Q FY 2014Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument18 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Hitachi Home & Life Solutions: Performance HighlightsDocument13 pagesHitachi Home & Life Solutions: Performance HighlightsAngel BrokingNo ratings yet

- Market Outlook 8th February 2012Document9 pagesMarket Outlook 8th February 2012Angel BrokingNo ratings yet

- Market Outlook 9th August 2011Document6 pagesMarket Outlook 9th August 2011Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument19 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- United Spirits 4Q FY 2013Document10 pagesUnited Spirits 4Q FY 2013Angel BrokingNo ratings yet

- Market Outlook Report, 22nd JanuaryDocument16 pagesMarket Outlook Report, 22nd JanuaryAngel BrokingNo ratings yet

- Market Outlook 27th April 2012Document7 pagesMarket Outlook 27th April 2012Angel BrokingNo ratings yet

- FAG Bearings Result UpdatedDocument10 pagesFAG Bearings Result UpdatedAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument17 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Dishman, 12th February, 2013Document10 pagesDishman, 12th February, 2013Angel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument24 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Dishman 2QFY2013RUDocument10 pagesDishman 2QFY2013RUAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument15 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Performance Highlights: Company Update - AutomobileDocument13 pagesPerformance Highlights: Company Update - AutomobileZacharia VincentNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument20 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Investigation, Guard & Armored Car Service Revenues World Summary: Market Values & Financials by CountryFrom EverandInvestigation, Guard & Armored Car Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Medical Equipment Rental & Leasing Revenues World Summary: Market Values & Financials by CountryFrom EverandMedical Equipment Rental & Leasing Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Oilseeds and Edible Oil UpdateDocument9 pagesOilseeds and Edible Oil UpdateAngel BrokingNo ratings yet

- WPIInflation August2013Document5 pagesWPIInflation August2013Angel BrokingNo ratings yet

- Ranbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertDocument4 pagesRanbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertAngel BrokingNo ratings yet

- International Commodities Evening Update September 16 2013Document3 pagesInternational Commodities Evening Update September 16 2013Angel BrokingNo ratings yet

- Daily Agri Tech Report September 14 2013Document2 pagesDaily Agri Tech Report September 14 2013Angel BrokingNo ratings yet

- Currency Daily Report September 16 2013Document4 pagesCurrency Daily Report September 16 2013Angel BrokingNo ratings yet

- Daily Metals and Energy Report September 16 2013Document6 pagesDaily Metals and Energy Report September 16 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5913)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5913)Angel Broking100% (1)

- Daily Agri Tech Report September 16 2013Document2 pagesDaily Agri Tech Report September 16 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Daily Agri Report September 16 2013Document9 pagesDaily Agri Report September 16 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19733) / NIFTY (5851)Document4 pagesDaily Technical Report: Sensex (19733) / NIFTY (5851)Angel BrokingNo ratings yet

- Tata Motors: Jaguar Land Rover - Monthly Sales UpdateDocument6 pagesTata Motors: Jaguar Land Rover - Monthly Sales UpdateAngel BrokingNo ratings yet

- Derivatives Report 8th JanDocument3 pagesDerivatives Report 8th JanAngel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 13Document2 pagesMetal and Energy Tech Report Sept 13Angel BrokingNo ratings yet

- Press Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressDocument1 pagePress Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressAngel BrokingNo ratings yet

- Jaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechDocument4 pagesJaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechAngel BrokingNo ratings yet

- Currency Daily Report September 13 2013Document4 pagesCurrency Daily Report September 13 2013Angel BrokingNo ratings yet

- Metal and Energy Tech Report Sept 12Document2 pagesMetal and Energy Tech Report Sept 12Angel BrokingNo ratings yet

- Currency Daily Report September 12 2013Document4 pagesCurrency Daily Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument12 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- Daily Agri Report September 12 2013Document9 pagesDaily Agri Report September 12 2013Angel BrokingNo ratings yet

- Daily Metals and Energy Report September 12 2013Document6 pagesDaily Metals and Energy Report September 12 2013Angel BrokingNo ratings yet

- Daily Technical Report: Sensex (19997) / NIFTY (5897)Document4 pagesDaily Technical Report: Sensex (19997) / NIFTY (5897)Angel BrokingNo ratings yet

- Daily Agri Tech Report September 12 2013Document2 pagesDaily Agri Tech Report September 12 2013Angel BrokingNo ratings yet

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingNo ratings yet

- A Study On Customer Preference and Satisfaction Towards Bajaj BikesDocument110 pagesA Study On Customer Preference and Satisfaction Towards Bajaj BikesAjay Savaliya83% (18)

- Domestic Bank Swift CodesDocument12 pagesDomestic Bank Swift CodesSHAKEEL IQBALNo ratings yet

- FRTB Ey ReviewDocument8 pagesFRTB Ey Review4GetM100% (1)

- 10000027359Document38 pages10000027359Chapter 11 DocketsNo ratings yet

- Risk Management: Best PracticeDocument19 pagesRisk Management: Best PracticeTrai SwatdikunNo ratings yet

- Full Art. 1800 - 1842Document10 pagesFull Art. 1800 - 1842Tia LiNo ratings yet

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaNo ratings yet

- Pagadian Commercial PDFDocument20 pagesPagadian Commercial PDFAsher TeogangcoNo ratings yet

- Mortgage Deed SavarkundlaDocument8 pagesMortgage Deed Savarkundladkumar471No ratings yet

- Eclectica Agriculture Fund Feb 2015Document2 pagesEclectica Agriculture Fund Feb 2015CanadianValueNo ratings yet

- Chapter - 8: Sub-Division of Joural:CashbookDocument11 pagesChapter - 8: Sub-Division of Joural:CashbookFaraz AliNo ratings yet

- Coco Life Audited Financial Statement 2014Document95 pagesCoco Life Audited Financial Statement 2014Angel PortosaNo ratings yet

- Pricing: Summary of Questions by Objectives and Bloom'S TaxonomyDocument43 pagesPricing: Summary of Questions by Objectives and Bloom'S TaxonomyJelly AnneNo ratings yet

- DbmsDocument29 pagesDbmsCarla Marielle CruzNo ratings yet

- 1 12 Integrated Marketing Communications Evaluation Case Study Colgate Cibaca The Road Ahead... (Courtesy FCB Ulka Comstrat 2006) Case OutlineDocument12 pages1 12 Integrated Marketing Communications Evaluation Case Study Colgate Cibaca The Road Ahead... (Courtesy FCB Ulka Comstrat 2006) Case OutlineNeha NaliniNo ratings yet

- Sfar 88 Airbus-Modification List Jan 08Document16 pagesSfar 88 Airbus-Modification List Jan 08Poshak Prasad GnawaliNo ratings yet

- Accounts Made EasyDocument9 pagesAccounts Made EasyPrashant KunduNo ratings yet

- What Is Company? Adminstration of Company LawDocument10 pagesWhat Is Company? Adminstration of Company Lawradhika77799100% (1)

- Fund Factsheets - IndividualDocument57 pagesFund Factsheets - IndividualRam KumarNo ratings yet

- What Is Global StrategyDocument7 pagesWhat Is Global StrategySonika MishraNo ratings yet

- Audi Nachhaltigkeitsbericht EN 2017 PDFDocument87 pagesAudi Nachhaltigkeitsbericht EN 2017 PDF꧁ Diego Breeze Martínez꧂No ratings yet

- How Traditional Firms Must Compete in The Sharing EconomyDocument4 pagesHow Traditional Firms Must Compete in The Sharing EconomyJorgeNo ratings yet

- 2015 Saln Form-From CSCDocument3 pages2015 Saln Form-From CSCRowel Magsino GonzalesNo ratings yet

- Reviewer ParcorpDocument2 pagesReviewer ParcorpLyka TejadaNo ratings yet