Download as xls, pdf, or txt

You might also like

- Final Exam - KW - Simulation - Tamal 2239890Document7 pagesFinal Exam - KW - Simulation - Tamal 2239890Tamal Sarkar100% (2)

- Seagate LBO AnalysisDocument58 pagesSeagate LBO Analysisthetesterofthings100% (2)

- Natureview Farm - Case AnalysisDocument11 pagesNatureview Farm - Case AnalysisSubhrata MishraNo ratings yet

- Merger Analysis COMPUTER CONCEPTS/COMPUTECHDocument24 pagesMerger Analysis COMPUTER CONCEPTS/COMPUTECHJerry K Floater0% (2)

- Broad Shifts in MarketingDocument3 pagesBroad Shifts in MarketingNIHAR RANJAN MishraNo ratings yet

- LEK ValuationDocument10 pagesLEK Valuationmmitre2100% (1)

- FT MBA Exam Spreadsheet Clean Edge RazorDocument1 pageFT MBA Exam Spreadsheet Clean Edge RazorDoshi VaibhavNo ratings yet

- Segment Wise Details of Markstrat at The End of Period 4Document17 pagesSegment Wise Details of Markstrat at The End of Period 4sazk070% (1)

- Fin439 Final Luv Aal UpdatedDocument91 pagesFin439 Final Luv Aal Updatedapi-323273427No ratings yet

- Bankinter Customer ProfitabilityDocument1 pageBankinter Customer Profitabilitylifeee100% (1)

- Limestone ModelDocument28 pagesLimestone ModellifeeeNo ratings yet

- Clean Edge ExcelDocument19 pagesClean Edge ExcelPriyanka BindumadhavanNo ratings yet

- Monmouth Group4Document18 pagesMonmouth Group4Jake Rolly0% (1)

- Debt Policy at Ust IncDocument18 pagesDebt Policy at Ust InctutenkhamenNo ratings yet

- MonmouthDocument25 pagesMonmouthPerci LunarejoNo ratings yet

- Annual Earnings Per Share Growth Rate Price/Earnings Ratio Market/Book RatioDocument5 pagesAnnual Earnings Per Share Growth Rate Price/Earnings Ratio Market/Book RatiossslucysssNo ratings yet

- Lessons From Capital Market History: Return & RiskDocument46 pagesLessons From Capital Market History: Return & RiskBlue DemonNo ratings yet

- MA819 Business Economics: Products, Marketing and PricingDocument26 pagesMA819 Business Economics: Products, Marketing and PricingAhmad FikriNo ratings yet

- Analyst Rating: About Apple IncDocument8 pagesAnalyst Rating: About Apple Incqwe200No ratings yet

- Sales Force Leadership: Sales Person Performance EvaluationDocument31 pagesSales Force Leadership: Sales Person Performance EvaluationSabu VincentNo ratings yet

- Revenue Variance ExampleDocument1 pageRevenue Variance ExampleImperoCo LLCNo ratings yet

- Revenue Variance ExampleDocument1 pageRevenue Variance ExampleNakkolopNo ratings yet

- Fin Model Practice 1Document17 pagesFin Model Practice 1elangelang99No ratings yet

- HW20Document18 pagesHW20kayteeminiNo ratings yet

- Wet Seal - VLDocument1 pageWet Seal - VLJohn Aldridge ChewNo ratings yet

- TiO2 FinancialDocument15 pagesTiO2 Financialbhagvandodiya88% (8)

- Confectionery MarketDocument96 pagesConfectionery Marketargyr@ath.forthnet.grNo ratings yet

- MonmouthDocument16 pagesMonmouthjamn1979100% (1)

- Images of MC DonaldsDocument12 pagesImages of MC Donaldsakash786rathiNo ratings yet

- Financial Ratio Calculator: (Complete The Yellow Cells Only, The Spreadsheet Does The Rest)Document4 pagesFinancial Ratio Calculator: (Complete The Yellow Cells Only, The Spreadsheet Does The Rest)tasleemshahzadNo ratings yet

- Case2 Team4 v4Document7 pagesCase2 Team4 v4whatifknowNo ratings yet

- Terminal MultipleDocument39 pagesTerminal MultiplegyanelexNo ratings yet

- Ch03 17Document3 pagesCh03 17Md Emamul HassanNo ratings yet

- Eportfolio MicroeconomicsDocument16 pagesEportfolio Microeconomicsapi-241510748No ratings yet

- DMA Case DataDocument1 pageDMA Case Datathrust_xoneNo ratings yet

- Corporate Finance - Situation No. 03Document4 pagesCorporate Finance - Situation No. 03Muhammad TalhaNo ratings yet

- DCCK TrendsDocument4 pagesDCCK TrendsSamanthaNo ratings yet

- Fusiontomo Inc.: Sales Rep Q1 Q2 Q3 Q4 TotalDocument8 pagesFusiontomo Inc.: Sales Rep Q1 Q2 Q3 Q4 TotalBillyNo ratings yet

- Worksheet Rule TypeDocument35 pagesWorksheet Rule Typerayna6633100% (1)

- Fischer Price ToysDocument11 pagesFischer Price ToysAvijit BanerjeeNo ratings yet

- Conn's - Follow-Up Report (Click Here To View in Scribd Format)Document10 pagesConn's - Follow-Up Report (Click Here To View in Scribd Format)interactivebuysideNo ratings yet

- Financial RatiosDocument78 pagesFinancial Ratiospun33tNo ratings yet

- Quantitative Methods Case Study: Mattel's Global Expansion: Analysing Growth Trends Name: Taksh Dhami Enrolment No: 20BSP2609 Division: GDocument7 pagesQuantitative Methods Case Study: Mattel's Global Expansion: Analysing Growth Trends Name: Taksh Dhami Enrolment No: 20BSP2609 Division: GJyot DhamiNo ratings yet

- UST SpreadsheetDocument21 pagesUST SpreadsheetTUNo ratings yet

- Number Cell of MAX ValueDocument21 pagesNumber Cell of MAX Valuepvenky_kkdNo ratings yet

- Star Sales DistributionDocument2 pagesStar Sales DistributionEmmanuelle MiuNo ratings yet

- Comparable Companies AnalysisDocument13 pagesComparable Companies AnalysisRehaan_Khan_RangerNo ratings yet

- A Review of IPO Activity Pricing and AllocationsDocument34 pagesA Review of IPO Activity Pricing and AllocationssharetopreetNo ratings yet

- Copycooperative Financial Ratio Calculator 2011Document10 pagesCopycooperative Financial Ratio Calculator 2011Selly SeftiantiNo ratings yet

- EportfoliomircoDocument3 pagesEportfoliomircoapi-248403849No ratings yet

- Determinants of IPO ValuationDocument21 pagesDeterminants of IPO ValuationSiiPoetryKeongNo ratings yet

- Lansdale Reporter Rate CardDocument7 pagesLansdale Reporter Rate CardjrcNo ratings yet

- Gums - Final Academy PresentationDocument26 pagesGums - Final Academy Presentationshru294100% (1)

- Case 21 Aurora Textile Company 0Document17 pagesCase 21 Aurora Textile Company 0nguyen_tridung250% (2)

- JPM Guide To The Markets - Q1 2014Document71 pagesJPM Guide To The Markets - Q1 2014adamsro9No ratings yet

- Turtle Beach ValuationDocument46 pagesTurtle Beach Valuationcale2kitNo ratings yet

- Debt Policy at UST Inc.Document47 pagesDebt Policy at UST Inc.karthikk1990100% (2)

- The Asian Financial Crisis: Hung-Gay Fung University of Missouri-St. LouisDocument32 pagesThe Asian Financial Crisis: Hung-Gay Fung University of Missouri-St. LouisPrateek BatraNo ratings yet

- SimVoi 306 ExampleDocument19 pagesSimVoi 306 ExampleSiddharth Shankar BebartaNo ratings yet

- Beyond Smart Beta: Index Investment Strategies for Active Portfolio ManagementFrom EverandBeyond Smart Beta: Index Investment Strategies for Active Portfolio ManagementNo ratings yet

- Macro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsFrom EverandMacro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsNo ratings yet

- Electroplating, Plating, Polishing, Anodizing & Coloring World Summary: Market Values & Financials by CountryFrom EverandElectroplating, Plating, Polishing, Anodizing & Coloring World Summary: Market Values & Financials by CountryNo ratings yet

- Commodity Market Trading and Investment: A Practitioners Guide to the MarketsFrom EverandCommodity Market Trading and Investment: A Practitioners Guide to the MarketsNo ratings yet

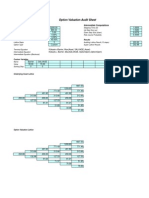

- Option Valuation Audit Sheet: Assumptions Intermediate ComputationsDocument1 pageOption Valuation Audit Sheet: Assumptions Intermediate ComputationslifeeeNo ratings yet

- Option Valuation Audit Sheet: Assumptions Intermediate ComputationsDocument1 pageOption Valuation Audit Sheet: Assumptions Intermediate ComputationslifeeeNo ratings yet

- Finnews Q5Document48 pagesFinnews Q5lifeeeNo ratings yet

- Certifications Overview - CFA, FRM and FLIPDocument7 pagesCertifications Overview - CFA, FRM and FLIPlifeeeNo ratings yet

- NCFM SMBM QuestionsDocument12 pagesNCFM SMBM QuestionslifeeeNo ratings yet

- Results CompiledDocument41 pagesResults CompiledlifeeeNo ratings yet

- Current Affairs - Rupee Plunge and DELL: Overview of The Scenario Followed by DiscussionDocument8 pagesCurrent Affairs - Rupee Plunge and DELL: Overview of The Scenario Followed by DiscussionlifeeeNo ratings yet

- FinGame Assignment 1Document1 pageFinGame Assignment 1lifeeeNo ratings yet

- Determinants of Regional Minimum Wages in The PhilippinesDocument4 pagesDeterminants of Regional Minimum Wages in The PhilippinesHanz Glitzer MosquedaNo ratings yet

- HDFC Life Smart Pension Plan BrochureDocument17 pagesHDFC Life Smart Pension Plan BrochureSatyajeet AnandNo ratings yet

- Chapter Five DSFDocument15 pagesChapter Five DSFtame kibruNo ratings yet

- Premises MOU NewDocument2 pagesPremises MOU NewRehanNo ratings yet

- 2022 10 20 PH S CNVRGDocument7 pages2022 10 20 PH S CNVRGValiente RandzNo ratings yet

- Process Costing TheoryDocument2 pagesProcess Costing TheoryNicoleNo ratings yet

- 7TH Loans PayableDocument4 pages7TH Loans PayableAnthony DyNo ratings yet

- MA - Vertical Statement Question BankDocument18 pagesMA - Vertical Statement Question Bankmanav.vakhariaNo ratings yet

- OM Group 5, National Cranberry CooperativeDocument10 pagesOM Group 5, National Cranberry Cooperativesudip2003No ratings yet

- Ogl 186051683101404946 PDFDocument5 pagesOgl 186051683101404946 PDFRajesh KumarNo ratings yet

- AllergenDocument2 pagesAllergenAgronomist ahmed hassanNo ratings yet

- Mco 04 Business Environment PDFDocument467 pagesMco 04 Business Environment PDFCA PASSNo ratings yet

- Practice Problem Set With Answers-Updated-Module-2 PDFDocument6 pagesPractice Problem Set With Answers-Updated-Module-2 PDFGhoul GamingNo ratings yet

- Contract of LeaseDocument3 pagesContract of LeaseSushiiiNo ratings yet

- Digital To The Core: The Banking Software CompanyDocument212 pagesDigital To The Core: The Banking Software CompanyCarlosMacedoDasNevesNo ratings yet

- PPRA Islamabad Conference Participants ListDocument6 pagesPPRA Islamabad Conference Participants ListAzhar HayatNo ratings yet

- What Is CapitalismDocument5 pagesWhat Is CapitalismAifel Joy Dayao FranciscoNo ratings yet

- Economics GR 12 Exam Guidelines 2014 EngDocument25 pagesEconomics GR 12 Exam Guidelines 2014 EngSphiwenhle MbheleNo ratings yet

- Module 6 EconDocument5 pagesModule 6 EconAstxilNo ratings yet

- Session 1Document31 pagesSession 1KARAN KAPOOR PGP 2021-23 BatchNo ratings yet

- Straddle StrategyDocument11 pagesStraddle StrategyРуслан СалаватовNo ratings yet

- Eulaw PDFDocument475 pagesEulaw PDFMarka LandishNo ratings yet

- Kr-Sel-Gvs: Express WorldwideDocument3 pagesKr-Sel-Gvs: Express WorldwideGraceNo ratings yet

- Report PDFDocument26 pagesReport PDFMayank MishraNo ratings yet

- Managing Strategy Operations and Partnerships 1773803 194477557Document32 pagesManaging Strategy Operations and Partnerships 1773803 194477557Gontla Sai SrijaNo ratings yet

- MCQs - Journal, Ledger & Trial BalanceDocument15 pagesMCQs - Journal, Ledger & Trial BalanceFareed khanNo ratings yet

- Case Study 2 - AccountingDocument5 pagesCase Study 2 - AccountingThrowaway TwoNo ratings yet

- Sri Lanka Sustainable Finance Roadmap FINAL 08.04.19Document29 pagesSri Lanka Sustainable Finance Roadmap FINAL 08.04.19Cr CryptoNo ratings yet

- Fmi Assignment #8: Ind - Ps - Ps - A1 McqsDocument4 pagesFmi Assignment #8: Ind - Ps - Ps - A1 McqsAditi RawatNo ratings yet