Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Week 2 Quiz Answers - Explanations PDFDocument6 pagesWeek 2 Quiz Answers - Explanations PDFanar82% (11)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- FABM 2 - Comprehensive TaskDocument3 pagesFABM 2 - Comprehensive TaskJOHN PAUL LAGAO100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Tugas ALK Chapter 7Document8 pagesTugas ALK Chapter 7Alief AmbyaNo ratings yet

- CFA Level II Cheat Sheet: Equity Fixed IncomeDocument1 pageCFA Level II Cheat Sheet: Equity Fixed Incomeapi-19918095No ratings yet

- The Basics of Capital Budgeting: Evaluating Cash FlowsDocument3 pagesThe Basics of Capital Budgeting: Evaluating Cash Flowstan lee huiNo ratings yet

- Unit 5 Mcqs QPDocument7 pagesUnit 5 Mcqs QPAdrian D'souzaNo ratings yet

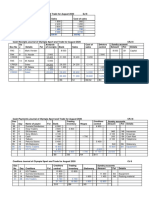

- Debtors Journal of Olympia Sport and Trade For August 2020DJ 8Document7 pagesDebtors Journal of Olympia Sport and Trade For August 2020DJ 8thokoanebokang00No ratings yet

- Levi Strauss & Co Fs 2023Document6 pagesLevi Strauss & Co Fs 2023Info Riskma SolutionsNo ratings yet

- Financial Aid Apllication (Coursera)Document2 pagesFinancial Aid Apllication (Coursera)Arsh AgarwalNo ratings yet

- DMCC Company Regulations - Jan 2022 - V2Document79 pagesDMCC Company Regulations - Jan 2022 - V2Laila NadifNo ratings yet

- Direct Tax Ca FinalDocument10 pagesDirect Tax Ca FinalGaurav GaurNo ratings yet

- Financial StatementsDocument27 pagesFinancial StatementsIrish Castillo100% (2)

- Fundamental Concepts of Managerial AccountingDocument45 pagesFundamental Concepts of Managerial AccountingCarlo CanlasNo ratings yet

- FY2022 Annual ReportEN Rev2Document436 pagesFY2022 Annual ReportEN Rev2Sjdnxbjzjs SbsbsjsjsNo ratings yet

- Priority PackDocument1 pagePriority PackYogesh BantanurNo ratings yet

- 4 Retiremnet and Death of A Partner QNDocument4 pages4 Retiremnet and Death of A Partner QNHridya SNo ratings yet

- Merger ModelDocument8 pagesMerger ModelStuti BansalNo ratings yet

- Book BuildingDocument19 pagesBook Buildingmonilsonaiya_91No ratings yet

- Capital BudgetingDocument48 pagesCapital Budgetingkingword84% (19)

- Chapter 25. Tool Kit For Mergers, Lbos, Divestitures, and Holding CompaniesDocument22 pagesChapter 25. Tool Kit For Mergers, Lbos, Divestitures, and Holding CompaniesPrashantKNo ratings yet

- Comparison of Ifrs, Ind As AsDocument7 pagesComparison of Ifrs, Ind As AsRudrin DasNo ratings yet

- Valuation MultiplesDocument33 pagesValuation MultiplesGuilherme PortoNo ratings yet

- Theoretical Failure of IAS 41Document5 pagesTheoretical Failure of IAS 41Tosin YusufNo ratings yet

- Audited Financial Result 2019 2020Document22 pagesAudited Financial Result 2019 2020Avrajit SarkarNo ratings yet

- Chapter 6 For CUP Financial AccountingDocument15 pagesChapter 6 For CUP Financial Accountingratanak_kong1-9No ratings yet

- Rashmi Class Rough WorkDocument10 pagesRashmi Class Rough WorkTejas Suhas MuleyNo ratings yet

- Dwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFDocument36 pagesDwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFjayden77evans100% (18)

- PIMCO ETFs ISS - Smart PassiveDocument4 pagesPIMCO ETFs ISS - Smart Passivefreebanker777741No ratings yet

- Midterm 1+ 2 (T NG H P)Document13 pagesMidterm 1+ 2 (T NG H P)Shen NPTDNo ratings yet

- North American Equity Research: Recent Mutual Conversion and M&A Trends Northeast SMID BanksDocument23 pagesNorth American Equity Research: Recent Mutual Conversion and M&A Trends Northeast SMID BanksJohn GrundNo ratings yet