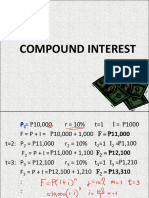

3.5 Continuous Growth Rate and The Number e

3.5 Continuous Growth Rate and The Number e

You might also like

- My Pay PDFDocument1 pageMy Pay PDFbuckwheat122507No ratings yet

- Log Interpretation Principles Applications PDFDocument241 pagesLog Interpretation Principles Applications PDFأحمد عطيه طلبه100% (6)

- Log Interpretation Principles Applications PDFDocument241 pagesLog Interpretation Principles Applications PDFأحمد عطيه طلبه100% (6)

- Abhishek Summer Training Report RecentDocument60 pagesAbhishek Summer Training Report Recentabhishekvijay2150% (2)

- Grapes Raisin (Kishmish)Document8 pagesGrapes Raisin (Kishmish)Paneendra KumarNo ratings yet

- Grameen Bank (Bangladesh)Document19 pagesGrameen Bank (Bangladesh)Haqiqat AliNo ratings yet

- FM Management NotesDocument96 pagesFM Management NotesGovindh200178% (9)

- Lecture 1: Compound Interests: Chapter 1: Mathematics of FinanceDocument34 pagesLecture 1: Compound Interests: Chapter 1: Mathematics of FinanceSa NguyenNo ratings yet

- Simple Interest Compounded Interest Population Growth Half LifeDocument32 pagesSimple Interest Compounded Interest Population Growth Half LifeCarmen GoguNo ratings yet

- Mathematics of FinanceDocument81 pagesMathematics of FinanceyonesNo ratings yet

- Ge 114 Module 7Document7 pagesGe 114 Module 7frederick liponNo ratings yet

- Lesson 4Document76 pagesLesson 4Syuhaidah Binti Aziz ZudinNo ratings yet

- First Reporter Compound Interest .2Document29 pagesFirst Reporter Compound Interest .2Golden Gate Colleges Main LibraryNo ratings yet

- Reading3 3BDocument5 pagesReading3 3BSphamandla MakalimaNo ratings yet

- Mathematics of Finance: 3. Annuity 4Document10 pagesMathematics of Finance: 3. Annuity 4Eduardo Tello del PinoNo ratings yet

- Safari - 22 Nov 2022 at 06 - 37Document1 pageSafari - 22 Nov 2022 at 06 - 37Tonie NascentNo ratings yet

- First-Reporter-Compound-Interest .2Document25 pagesFirst-Reporter-Compound-Interest .2Mherie Joy Cantos GutierrezNo ratings yet

- Mathematics of InvestmentsDocument8 pagesMathematics of InvestmentsMathew EsparragoNo ratings yet

- Interest Money-Time Relationship Part 2Document9 pagesInterest Money-Time Relationship Part 2Carlnagum 123456789No ratings yet

- Examples: Simple and Compound InterestDocument3 pagesExamples: Simple and Compound InterestnonononowayNo ratings yet

- Chapter 4 StudentDocument21 pagesChapter 4 Studentgerearegawi721No ratings yet

- General Mathematics: I.2 Learning ActivitiesDocument6 pagesGeneral Mathematics: I.2 Learning ActivitiesAndrea InocNo ratings yet

- Gen - Math 11Document15 pagesGen - Math 11Chrry MrcdNo ratings yet

- BUSANA1 Chapter 2 (2) : Compound InterestDocument22 pagesBUSANA1 Chapter 2 (2) : Compound Interest7 bitNo ratings yet

- # 4. Money-Time Relationships: Capital Returns and InterestsDocument38 pages# 4. Money-Time Relationships: Capital Returns and InterestsJean Claire LlemitNo ratings yet

- Senior High School ReportDocument14 pagesSenior High School ReportKOUJI N. MARQUEZ0% (1)

- Maple: Objective: After Reading This Chapter, You Will Solve Mathematical Problems Using MapleDocument5 pagesMaple: Objective: After Reading This Chapter, You Will Solve Mathematical Problems Using MaplerockydarkNo ratings yet

- Chapter1 - Return CalculationsDocument37 pagesChapter1 - Return CalculationsChris CheungNo ratings yet

- Measures of Interests-1Document36 pagesMeasures of Interests-1francel floresNo ratings yet

- TVM ProblemsDocument7 pagesTVM ProblemsBala SudhakarNo ratings yet

- Simple and Compound InterestDocument83 pagesSimple and Compound InterestアンジェロドンNo ratings yet

- FM I Chapter 3Document12 pagesFM I Chapter 3mearghaile4No ratings yet

- Lec1-Time Value of MoneyDocument27 pagesLec1-Time Value of Moneyhassan baradaNo ratings yet

- 8 Compound-InterestDocument16 pages8 Compound-InterestVj McNo ratings yet

- Module 2Document22 pagesModule 2margieNo ratings yet

- Gen Math Mod67Document15 pagesGen Math Mod67Jun ChavezNo ratings yet

- Business Mathematics CH-4Document35 pagesBusiness Mathematics CH-4AYNETU TEREFENo ratings yet

- LAS 9 GenMath 11Document9 pagesLAS 9 GenMath 11Chantal AltheaNo ratings yet

- Winter Semester 2023-24 - MGT2006 - TH - AP2023246000029 - 2024-01-20 - Reference-Material-IDocument24 pagesWinter Semester 2023-24 - MGT2006 - TH - AP2023246000029 - 2024-01-20 - Reference-Material-Isujithsai2004No ratings yet

- Compound Interest Formula and Examples - MathBootCampsDocument8 pagesCompound Interest Formula and Examples - MathBootCampsFederation NORSU AlumniNo ratings yet

- Notes On Engineering Economic Analysis: College of Engineering and Computer Science Mechanical Engineering DepartmentDocument15 pagesNotes On Engineering Economic Analysis: College of Engineering and Computer Science Mechanical Engineering Departmentkishorereddy_btechNo ratings yet

- Chapter Four Lecture Notes On Business MathematicsDocument24 pagesChapter Four Lecture Notes On Business MathematicsErmias Guragaw100% (3)

- WEEK3. Simple AnnuityDocument31 pagesWEEK3. Simple AnnuityMarquez FrancisNo ratings yet

- ABMBRC 3 LESSON 4 Compound InterestDocument4 pagesABMBRC 3 LESSON 4 Compound InterestZOEZEL ANNLEIH LAYONGNo ratings yet

- Module 3Document52 pagesModule 3Jozel ValenzuelaNo ratings yet

- Annual CompoundingDocument6 pagesAnnual CompoundingSreekar ParimiNo ratings yet

- Simple and Compound InterestDocument46 pagesSimple and Compound InterestAndres MabiniNo ratings yet

- PPT02 - Nominal and Effective Interest RatesDocument33 pagesPPT02 - Nominal and Effective Interest RatesImam Al GhazaliNo ratings yet

- General Mathematics: LAS, Week 3 - Quarter 2Document18 pagesGeneral Mathematics: LAS, Week 3 - Quarter 2Prince Joshua SumagitNo ratings yet

- Introduction To Financial MathematicsDocument81 pagesIntroduction To Financial MathematicsBayu DokuuNo ratings yet

- 10.6 Compound Interest PDFDocument7 pages10.6 Compound Interest PDFMarijoy MarquezNo ratings yet

- Module 3Document5 pagesModule 3RyuddaenNo ratings yet

- Chapter 2-Part 2Document13 pagesChapter 2-Part 2Puji dyukeNo ratings yet

- Mathematics of Finance: Md. Aktar Kamal Lecturer Department of Management Bangladesh University of Professionals (BUPDocument14 pagesMathematics of Finance: Md. Aktar Kamal Lecturer Department of Management Bangladesh University of Professionals (BUPZubaer RiadNo ratings yet

- Unit 4 MMDocument21 pagesUnit 4 MMChalachew EyobNo ratings yet

- MOI Midterm LessonDocument82 pagesMOI Midterm LessonPie CanapiNo ratings yet

- MODULE 1 Math 08 - f2fDocument19 pagesMODULE 1 Math 08 - f2fShiena mae IndacNo ratings yet

- Annuities and Perpetuities: Present Value: William L. SilberDocument3 pagesAnnuities and Perpetuities: Present Value: William L. SilberdrakowamNo ratings yet

- Engineering Economy Module 2Document33 pagesEngineering Economy Module 2James ClarkNo ratings yet

- 2 Effective and Nominal RateDocument19 pages2 Effective and Nominal RateKelvin BarceLonNo ratings yet

- Ch.4 Math of Finance-1Document19 pagesCh.4 Math of Finance-1hildamezmur9No ratings yet

- Compound Interest: P21,073.92 Is The Compound Amount of P15,000 Compounded Annually For 3 Years at 12%Document4 pagesCompound Interest: P21,073.92 Is The Compound Amount of P15,000 Compounded Annually For 3 Years at 12%Bloodmier GabrielNo ratings yet

- Topic 4 Interest RatesDocument12 pagesTopic 4 Interest RatesAtish JainNo ratings yet

- Time Value of Money ConceptsDocument9 pagesTime Value of Money ConceptskishorerocxNo ratings yet

- Lecture 4A - PDM CPM and Barchart - Part 1Document19 pagesLecture 4A - PDM CPM and Barchart - Part 1MmNo ratings yet

- The Number Concept, True its Definition and The Division by ZeroFrom EverandThe Number Concept, True its Definition and The Division by ZeroNo ratings yet

- التحصيل في اصول الدين - أ. سعيد فودةDocument12 pagesالتحصيل في اصول الدين - أ. سعيد فودةMusersameNo ratings yet

- التحصيل في اصول الدين - أ. سعيد فودةDocument12 pagesالتحصيل في اصول الدين - أ. سعيد فودةMusersameNo ratings yet

- SPE 77386 Analysis of Black Oil PVT Reports Revisited: B B B at P PDocument5 pagesSPE 77386 Analysis of Black Oil PVT Reports Revisited: B B B at P PJuan MartinezNo ratings yet

- IPR AnalysisDocument12 pagesIPR Analysisأحمد عطيه طلبهNo ratings yet

- Capillarity and Mechanics of The SurfaceDocument33 pagesCapillarity and Mechanics of The SurfaceSubhasish MitraNo ratings yet

- Almeda vs. CADocument7 pagesAlmeda vs. CAAnonymous oDPxEkdNo ratings yet

- Om Sai Ent GGN DLFDocument5 pagesOm Sai Ent GGN DLFVinod RahejaNo ratings yet

- Account StatementDocument12 pagesAccount Statementharish rajNo ratings yet

- International Financial Management Abridged 10 Edition: by Jeff MaduraDocument9 pagesInternational Financial Management Abridged 10 Edition: by Jeff MaduraHiếu Nhi TrịnhNo ratings yet

- Tenancy ContractDocument4 pagesTenancy ContractАндрей МатюшинNo ratings yet

- Forensic Review: Prepared For Howard County Public School System ("HCPSS")Document13 pagesForensic Review: Prepared For Howard County Public School System ("HCPSS")Pooja FuliaNo ratings yet

- 2-Oma STD Local Commercial Terms (SCT)Document6 pages2-Oma STD Local Commercial Terms (SCT)navisNo ratings yet

- Chaojing Fu: ProfileDocument2 pagesChaojing Fu: Profilec_fu1No ratings yet

- Budget Sheet - EmptyDocument329 pagesBudget Sheet - EmptyAyush PalawatNo ratings yet

- InflationDocument38 pagesInflationleen2006waelNo ratings yet

- Banking NotesDocument28 pagesBanking NotesnitiNo ratings yet

- Resume - Rajan PalanDocument3 pagesResume - Rajan PalanShrikant RamNo ratings yet

- How Artificial Intelligence Can Help The Sector of Accounting and Audit Deal Wtih Covid-19Document9 pagesHow Artificial Intelligence Can Help The Sector of Accounting and Audit Deal Wtih Covid-19Hoàng Hải QuyênNo ratings yet

- Summer Internship ReportDocument22 pagesSummer Internship ReportBeljohn AlappatNo ratings yet

- Debt Funding in IndiaDocument54 pagesDebt Funding in IndiaAbhinay KumarNo ratings yet

- Form - DIME Calclator (Life Insurance)Document2 pagesForm - DIME Calclator (Life Insurance)Corbin Lindsey100% (1)

- 4&5 AssignmentDocument18 pages4&5 AssignmentQaulan Tsaqila100% (2)

- Akuntansi Perusahaan Dagang Panorama HijauDocument27 pagesAkuntansi Perusahaan Dagang Panorama Hijausintya saputri100% (1)

- HDMF Citizens CharterDocument24 pagesHDMF Citizens CharterEarl Russell S PaulicanNo ratings yet

- Dire Proposal PDFDocument26 pagesDire Proposal PDFshiferaw kumbiNo ratings yet

- Entrepreneurship and Business Ownership: COMM 1010: Business in A Global ContextDocument15 pagesEntrepreneurship and Business Ownership: COMM 1010: Business in A Global ContextAbeer ArifNo ratings yet

- #1prepare Trail Balance: (1) NAME Under Name DR CR Total 22010 0 22010 0Document3 pages#1prepare Trail Balance: (1) NAME Under Name DR CR Total 22010 0 22010 0kingmib1No ratings yet

- Analysis of Indian EconomyDocument41 pagesAnalysis of Indian EconomySaurav GhoshNo ratings yet

- Super Very FinalDocument5 pagesSuper Very FinalLeanne YumangNo ratings yet

- Consolidation IIIDocument36 pagesConsolidation IIIMuhammad Asad100% (1)

Download as pdf or txt

You might also like

- My Pay PDFDocument1 pageMy Pay PDFbuckwheat122507No ratings yet

- Log Interpretation Principles Applications PDFDocument241 pagesLog Interpretation Principles Applications PDFأحمد عطيه طلبه100% (6)

- Log Interpretation Principles Applications PDFDocument241 pagesLog Interpretation Principles Applications PDFأحمد عطيه طلبه100% (6)

- Abhishek Summer Training Report RecentDocument60 pagesAbhishek Summer Training Report Recentabhishekvijay2150% (2)

- Grapes Raisin (Kishmish)Document8 pagesGrapes Raisin (Kishmish)Paneendra KumarNo ratings yet

- Grameen Bank (Bangladesh)Document19 pagesGrameen Bank (Bangladesh)Haqiqat AliNo ratings yet

- FM Management NotesDocument96 pagesFM Management NotesGovindh200178% (9)

- Lecture 1: Compound Interests: Chapter 1: Mathematics of FinanceDocument34 pagesLecture 1: Compound Interests: Chapter 1: Mathematics of FinanceSa NguyenNo ratings yet

- Simple Interest Compounded Interest Population Growth Half LifeDocument32 pagesSimple Interest Compounded Interest Population Growth Half LifeCarmen GoguNo ratings yet

- Mathematics of FinanceDocument81 pagesMathematics of FinanceyonesNo ratings yet

- Ge 114 Module 7Document7 pagesGe 114 Module 7frederick liponNo ratings yet

- Lesson 4Document76 pagesLesson 4Syuhaidah Binti Aziz ZudinNo ratings yet

- First Reporter Compound Interest .2Document29 pagesFirst Reporter Compound Interest .2Golden Gate Colleges Main LibraryNo ratings yet

- Reading3 3BDocument5 pagesReading3 3BSphamandla MakalimaNo ratings yet

- Mathematics of Finance: 3. Annuity 4Document10 pagesMathematics of Finance: 3. Annuity 4Eduardo Tello del PinoNo ratings yet

- Safari - 22 Nov 2022 at 06 - 37Document1 pageSafari - 22 Nov 2022 at 06 - 37Tonie NascentNo ratings yet

- First-Reporter-Compound-Interest .2Document25 pagesFirst-Reporter-Compound-Interest .2Mherie Joy Cantos GutierrezNo ratings yet

- Mathematics of InvestmentsDocument8 pagesMathematics of InvestmentsMathew EsparragoNo ratings yet

- Interest Money-Time Relationship Part 2Document9 pagesInterest Money-Time Relationship Part 2Carlnagum 123456789No ratings yet

- Examples: Simple and Compound InterestDocument3 pagesExamples: Simple and Compound InterestnonononowayNo ratings yet

- Chapter 4 StudentDocument21 pagesChapter 4 Studentgerearegawi721No ratings yet

- General Mathematics: I.2 Learning ActivitiesDocument6 pagesGeneral Mathematics: I.2 Learning ActivitiesAndrea InocNo ratings yet

- Gen - Math 11Document15 pagesGen - Math 11Chrry MrcdNo ratings yet

- BUSANA1 Chapter 2 (2) : Compound InterestDocument22 pagesBUSANA1 Chapter 2 (2) : Compound Interest7 bitNo ratings yet

- # 4. Money-Time Relationships: Capital Returns and InterestsDocument38 pages# 4. Money-Time Relationships: Capital Returns and InterestsJean Claire LlemitNo ratings yet

- Senior High School ReportDocument14 pagesSenior High School ReportKOUJI N. MARQUEZ0% (1)

- Maple: Objective: After Reading This Chapter, You Will Solve Mathematical Problems Using MapleDocument5 pagesMaple: Objective: After Reading This Chapter, You Will Solve Mathematical Problems Using MaplerockydarkNo ratings yet

- Chapter1 - Return CalculationsDocument37 pagesChapter1 - Return CalculationsChris CheungNo ratings yet

- Measures of Interests-1Document36 pagesMeasures of Interests-1francel floresNo ratings yet

- TVM ProblemsDocument7 pagesTVM ProblemsBala SudhakarNo ratings yet

- Simple and Compound InterestDocument83 pagesSimple and Compound InterestアンジェロドンNo ratings yet

- FM I Chapter 3Document12 pagesFM I Chapter 3mearghaile4No ratings yet

- Lec1-Time Value of MoneyDocument27 pagesLec1-Time Value of Moneyhassan baradaNo ratings yet

- 8 Compound-InterestDocument16 pages8 Compound-InterestVj McNo ratings yet

- Module 2Document22 pagesModule 2margieNo ratings yet

- Gen Math Mod67Document15 pagesGen Math Mod67Jun ChavezNo ratings yet

- Business Mathematics CH-4Document35 pagesBusiness Mathematics CH-4AYNETU TEREFENo ratings yet

- LAS 9 GenMath 11Document9 pagesLAS 9 GenMath 11Chantal AltheaNo ratings yet

- Winter Semester 2023-24 - MGT2006 - TH - AP2023246000029 - 2024-01-20 - Reference-Material-IDocument24 pagesWinter Semester 2023-24 - MGT2006 - TH - AP2023246000029 - 2024-01-20 - Reference-Material-Isujithsai2004No ratings yet

- Compound Interest Formula and Examples - MathBootCampsDocument8 pagesCompound Interest Formula and Examples - MathBootCampsFederation NORSU AlumniNo ratings yet

- Notes On Engineering Economic Analysis: College of Engineering and Computer Science Mechanical Engineering DepartmentDocument15 pagesNotes On Engineering Economic Analysis: College of Engineering and Computer Science Mechanical Engineering Departmentkishorereddy_btechNo ratings yet

- Chapter Four Lecture Notes On Business MathematicsDocument24 pagesChapter Four Lecture Notes On Business MathematicsErmias Guragaw100% (3)

- WEEK3. Simple AnnuityDocument31 pagesWEEK3. Simple AnnuityMarquez FrancisNo ratings yet

- ABMBRC 3 LESSON 4 Compound InterestDocument4 pagesABMBRC 3 LESSON 4 Compound InterestZOEZEL ANNLEIH LAYONGNo ratings yet

- Module 3Document52 pagesModule 3Jozel ValenzuelaNo ratings yet

- Annual CompoundingDocument6 pagesAnnual CompoundingSreekar ParimiNo ratings yet

- Simple and Compound InterestDocument46 pagesSimple and Compound InterestAndres MabiniNo ratings yet

- PPT02 - Nominal and Effective Interest RatesDocument33 pagesPPT02 - Nominal and Effective Interest RatesImam Al GhazaliNo ratings yet

- General Mathematics: LAS, Week 3 - Quarter 2Document18 pagesGeneral Mathematics: LAS, Week 3 - Quarter 2Prince Joshua SumagitNo ratings yet

- Introduction To Financial MathematicsDocument81 pagesIntroduction To Financial MathematicsBayu DokuuNo ratings yet

- 10.6 Compound Interest PDFDocument7 pages10.6 Compound Interest PDFMarijoy MarquezNo ratings yet

- Module 3Document5 pagesModule 3RyuddaenNo ratings yet

- Chapter 2-Part 2Document13 pagesChapter 2-Part 2Puji dyukeNo ratings yet

- Mathematics of Finance: Md. Aktar Kamal Lecturer Department of Management Bangladesh University of Professionals (BUPDocument14 pagesMathematics of Finance: Md. Aktar Kamal Lecturer Department of Management Bangladesh University of Professionals (BUPZubaer RiadNo ratings yet

- Unit 4 MMDocument21 pagesUnit 4 MMChalachew EyobNo ratings yet

- MOI Midterm LessonDocument82 pagesMOI Midterm LessonPie CanapiNo ratings yet

- MODULE 1 Math 08 - f2fDocument19 pagesMODULE 1 Math 08 - f2fShiena mae IndacNo ratings yet

- Annuities and Perpetuities: Present Value: William L. SilberDocument3 pagesAnnuities and Perpetuities: Present Value: William L. SilberdrakowamNo ratings yet

- Engineering Economy Module 2Document33 pagesEngineering Economy Module 2James ClarkNo ratings yet

- 2 Effective and Nominal RateDocument19 pages2 Effective and Nominal RateKelvin BarceLonNo ratings yet

- Ch.4 Math of Finance-1Document19 pagesCh.4 Math of Finance-1hildamezmur9No ratings yet

- Compound Interest: P21,073.92 Is The Compound Amount of P15,000 Compounded Annually For 3 Years at 12%Document4 pagesCompound Interest: P21,073.92 Is The Compound Amount of P15,000 Compounded Annually For 3 Years at 12%Bloodmier GabrielNo ratings yet

- Topic 4 Interest RatesDocument12 pagesTopic 4 Interest RatesAtish JainNo ratings yet

- Time Value of Money ConceptsDocument9 pagesTime Value of Money ConceptskishorerocxNo ratings yet

- Lecture 4A - PDM CPM and Barchart - Part 1Document19 pagesLecture 4A - PDM CPM and Barchart - Part 1MmNo ratings yet

- The Number Concept, True its Definition and The Division by ZeroFrom EverandThe Number Concept, True its Definition and The Division by ZeroNo ratings yet

- التحصيل في اصول الدين - أ. سعيد فودةDocument12 pagesالتحصيل في اصول الدين - أ. سعيد فودةMusersameNo ratings yet

- التحصيل في اصول الدين - أ. سعيد فودةDocument12 pagesالتحصيل في اصول الدين - أ. سعيد فودةMusersameNo ratings yet

- SPE 77386 Analysis of Black Oil PVT Reports Revisited: B B B at P PDocument5 pagesSPE 77386 Analysis of Black Oil PVT Reports Revisited: B B B at P PJuan MartinezNo ratings yet

- IPR AnalysisDocument12 pagesIPR Analysisأحمد عطيه طلبهNo ratings yet

- Capillarity and Mechanics of The SurfaceDocument33 pagesCapillarity and Mechanics of The SurfaceSubhasish MitraNo ratings yet

- Almeda vs. CADocument7 pagesAlmeda vs. CAAnonymous oDPxEkdNo ratings yet

- Om Sai Ent GGN DLFDocument5 pagesOm Sai Ent GGN DLFVinod RahejaNo ratings yet

- Account StatementDocument12 pagesAccount Statementharish rajNo ratings yet

- International Financial Management Abridged 10 Edition: by Jeff MaduraDocument9 pagesInternational Financial Management Abridged 10 Edition: by Jeff MaduraHiếu Nhi TrịnhNo ratings yet

- Tenancy ContractDocument4 pagesTenancy ContractАндрей МатюшинNo ratings yet

- Forensic Review: Prepared For Howard County Public School System ("HCPSS")Document13 pagesForensic Review: Prepared For Howard County Public School System ("HCPSS")Pooja FuliaNo ratings yet

- 2-Oma STD Local Commercial Terms (SCT)Document6 pages2-Oma STD Local Commercial Terms (SCT)navisNo ratings yet

- Chaojing Fu: ProfileDocument2 pagesChaojing Fu: Profilec_fu1No ratings yet

- Budget Sheet - EmptyDocument329 pagesBudget Sheet - EmptyAyush PalawatNo ratings yet

- InflationDocument38 pagesInflationleen2006waelNo ratings yet

- Banking NotesDocument28 pagesBanking NotesnitiNo ratings yet

- Resume - Rajan PalanDocument3 pagesResume - Rajan PalanShrikant RamNo ratings yet

- How Artificial Intelligence Can Help The Sector of Accounting and Audit Deal Wtih Covid-19Document9 pagesHow Artificial Intelligence Can Help The Sector of Accounting and Audit Deal Wtih Covid-19Hoàng Hải QuyênNo ratings yet

- Summer Internship ReportDocument22 pagesSummer Internship ReportBeljohn AlappatNo ratings yet

- Debt Funding in IndiaDocument54 pagesDebt Funding in IndiaAbhinay KumarNo ratings yet

- Form - DIME Calclator (Life Insurance)Document2 pagesForm - DIME Calclator (Life Insurance)Corbin Lindsey100% (1)

- 4&5 AssignmentDocument18 pages4&5 AssignmentQaulan Tsaqila100% (2)

- Akuntansi Perusahaan Dagang Panorama HijauDocument27 pagesAkuntansi Perusahaan Dagang Panorama Hijausintya saputri100% (1)

- HDMF Citizens CharterDocument24 pagesHDMF Citizens CharterEarl Russell S PaulicanNo ratings yet

- Dire Proposal PDFDocument26 pagesDire Proposal PDFshiferaw kumbiNo ratings yet

- Entrepreneurship and Business Ownership: COMM 1010: Business in A Global ContextDocument15 pagesEntrepreneurship and Business Ownership: COMM 1010: Business in A Global ContextAbeer ArifNo ratings yet

- #1prepare Trail Balance: (1) NAME Under Name DR CR Total 22010 0 22010 0Document3 pages#1prepare Trail Balance: (1) NAME Under Name DR CR Total 22010 0 22010 0kingmib1No ratings yet

- Analysis of Indian EconomyDocument41 pagesAnalysis of Indian EconomySaurav GhoshNo ratings yet

- Super Very FinalDocument5 pagesSuper Very FinalLeanne YumangNo ratings yet

- Consolidation IIIDocument36 pagesConsolidation IIIMuhammad Asad100% (1)