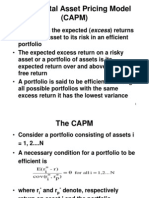

Equilibrium Pricing

Equilibrium Pricing

You might also like

- Answer Key Inter Acctg 2Document66 pagesAnswer Key Inter Acctg 2URBANO CREATIONS PRINTING & GRAPHICS100% (2)

- CAPM Approach Beta Is Dead or AliveDocument23 pagesCAPM Approach Beta Is Dead or AliveKazim KhanNo ratings yet

- Commodity Volatility SurfaceDocument4 pagesCommodity Volatility SurfaceMarco Avello IbarraNo ratings yet

- OIS Discounting PiterbargDocument6 pagesOIS Discounting PiterbargharsjusNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Asset Pricing ModelDocument62 pagesAsset Pricing ModelA. LatifNo ratings yet

- Textbook: Readings:: Cubs MSC Finance 1999-2000 Asset Management: Lecture 3Document13 pagesTextbook: Readings:: Cubs MSC Finance 1999-2000 Asset Management: Lecture 3Atif SaeedNo ratings yet

- The Capital Asset Pricing Model (CAPM)Document31 pagesThe Capital Asset Pricing Model (CAPM)Tanmay AbhijeetNo ratings yet

- Chapter 7: The CAPM: Investment ScienceDocument22 pagesChapter 7: The CAPM: Investment Scienceouji62No ratings yet

- Capital Market LineDocument8 pagesCapital Market Linecjpadin09No ratings yet

- Topic 4Document6 pagesTopic 4arp140102No ratings yet

- Do Taxes Matter in The CAPM?: 1 Presentation of The ProblemDocument8 pagesDo Taxes Matter in The CAPM?: 1 Presentation of The Problemapi-158666950No ratings yet

- CAPM Academic PieceDocument29 pagesCAPM Academic PiecespelicansNo ratings yet

- CAPM and The RisklessDocument28 pagesCAPM and The RisklessAdamNo ratings yet

- Capm 2004 ADocument35 pagesCapm 2004 Aobaidsimon123No ratings yet

- 7 AptDocument19 pages7 AptBikram MaharjanNo ratings yet

- Module 2 CAPMDocument11 pagesModule 2 CAPMTanvi DevadigaNo ratings yet

- Notes On DerivativesDocument7 pagesNotes On DerivativesLiliana AguirreNo ratings yet

- I.4.3 The Capital Asset Pricing Model: Investors' PreferencesDocument19 pagesI.4.3 The Capital Asset Pricing Model: Investors' Preferencesjohnsm2010No ratings yet

- Capital Market TheoryDocument5 pagesCapital Market TheoryZakia ElhamNo ratings yet

- Mefa 2 MarksDocument12 pagesMefa 2 MarksSaidinesh SurineniNo ratings yet

- Web Additional ExercisesDocument14 pagesWeb Additional ExercisesLeticia RoccaNo ratings yet

- The Liquidity Premium in Average Interest Rates : Wilbur John Coleman IIDocument17 pagesThe Liquidity Premium in Average Interest Rates : Wilbur John Coleman IIererereretrterNo ratings yet

- 04 Forward and Future Exchange RateDocument12 pages04 Forward and Future Exchange RateAdnan KamalNo ratings yet

- Port MNGT tRiskandReturn4Document105 pagesPort MNGT tRiskandReturn4guhandossNo ratings yet

- The Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchDocument22 pagesThe Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchThakur Raj AnandNo ratings yet

- Fama French 2004Document50 pagesFama French 2004William RamosNo ratings yet

- The Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchDocument27 pagesThe Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchAndus ManurungNo ratings yet

- Fama & French (CAPM)Document55 pagesFama & French (CAPM)NICOLE PATRICIA MUNOZ MERINONo ratings yet

- An Introduction To Portfolio Theory: Paul J. AtzbergerDocument16 pagesAn Introduction To Portfolio Theory: Paul J. AtzbergerSamNo ratings yet

- 1 19Document8 pages1 19Yilei RenNo ratings yet

- Security Analysis and Portfolio Management Selected Solutions To Problem Set #3: Section I: Portfolio Management 3) Portfolio Expected ReturnDocument7 pagesSecurity Analysis and Portfolio Management Selected Solutions To Problem Set #3: Section I: Portfolio Management 3) Portfolio Expected ReturnPradeep GuptaNo ratings yet

- Teaching Note 96-01: Default Risk As An Option: Version Date: November 3, 2003 C:/Classbackup/Teaching Notes/Tn96-01.WpdDocument5 pagesTeaching Note 96-01: Default Risk As An Option: Version Date: November 3, 2003 C:/Classbackup/Teaching Notes/Tn96-01.WpdVeeken ChaglassianNo ratings yet

- Valuation2 Oct6014Document7 pagesValuation2 Oct6014hoalongkiemNo ratings yet

- The Capital Asset Pricing Model (CAPM) : AssumptionsDocument4 pagesThe Capital Asset Pricing Model (CAPM) : AssumptionsRomazh Sifuentes RamirezNo ratings yet

- Chapter-10 Return & RiskDocument19 pagesChapter-10 Return & Riskaparajita promaNo ratings yet

- Exercises: Capital Asset Pricing Model (SOLUTIONS) : Department of Finance University of Basel Fall 2009Document4 pagesExercises: Capital Asset Pricing Model (SOLUTIONS) : Department of Finance University of Basel Fall 2009aftab20No ratings yet

- Chapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnDocument9 pagesChapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnBiloni KadakiaNo ratings yet

- Indifference Curve, Which Reflects That Investor's Preferences Regarding Risk and Return, IsDocument5 pagesIndifference Curve, Which Reflects That Investor's Preferences Regarding Risk and Return, Ismd mehedi hasanNo ratings yet

- Black 1976 Debt CovenantsDocument17 pagesBlack 1976 Debt Covenantsk60.2112343080No ratings yet

- The Mathematics of Ponzi SchemesDocument26 pagesThe Mathematics of Ponzi SchemesSPaul7No ratings yet

- WACC and APV RevisitedDocument11 pagesWACC and APV Revisitedrogelio rojasNo ratings yet

- CAPMDocument43 pagesCAPMProf.V.Vanaja sureshNo ratings yet

- Problem Set 2: 1 Insurance With Adverse SelectionDocument5 pagesProblem Set 2: 1 Insurance With Adverse SelectionAmine El AzdiNo ratings yet

- Portfolio Management 1Document28 pagesPortfolio Management 1Sattar Md AbdusNo ratings yet

- Pricing Swaps Including Funding CostsDocument19 pagesPricing Swaps Including Funding CostsobrefoNo ratings yet

- An Introduction To Modern Portfolio TheoryDocument38 pagesAn Introduction To Modern Portfolio Theoryhmme21No ratings yet

- MFPMDocument25 pagesMFPMMadhusmita MishraNo ratings yet

- Optimal Risky PortfolioDocument25 pagesOptimal Risky PortfolioAlexandra HsiajsnaksNo ratings yet

- Module - 4b - CAL, CMT, CAPM, SIM and APTDocument49 pagesModule - 4b - CAL, CMT, CAPM, SIM and APTGourav ParidaNo ratings yet

- Analysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelDocument8 pagesAnalysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelAmal AsseyrNo ratings yet

- A Laymans Approach To Black-Litterman ModelDocument7 pagesA Laymans Approach To Black-Litterman Modelswinki3No ratings yet

- The Transactions Demand For Cash: An Inventory Theoretic Approac FDocument15 pagesThe Transactions Demand For Cash: An Inventory Theoretic Approac FCanela DavidNo ratings yet

- Book An Introduction To The Math of Financial Derivatives Neftci S.N. SOLUTIONDocument90 pagesBook An Introduction To The Math of Financial Derivatives Neftci S.N. SOLUTIONAtiqur KhanNo ratings yet

- Arbitrage Pricing TheoryDocument15 pagesArbitrage Pricing TheoryYixing ZhangNo ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- The Volatility Surface: A Practitioner's GuideFrom EverandThe Volatility Surface: A Practitioner's GuideRating: 4 out of 5 stars4/5 (4)

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioFrom EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioRating: 4.5 out of 5 stars4.5/5 (3)

- Time: 3 Hours Maximum Marks: 100 Note: Attempt Questions From Each Section As Per Instructions GivenDocument4 pagesTime: 3 Hours Maximum Marks: 100 Note: Attempt Questions From Each Section As Per Instructions GivenAshwin R JohnNo ratings yet

- Mec-003 QT 2014Document7 pagesMec-003 QT 2014Ashwin R John100% (1)

- Master of Arts (Economics) : Time: 3 Hours Maximum Marks: 100 Note: Answer Questions From Each Section As DirectedDocument4 pagesMaster of Arts (Economics) : Time: 3 Hours Maximum Marks: 100 Note: Answer Questions From Each Section As DirectedAshwin R JohnNo ratings yet

- MEC-001 - Micronomic Analysis 2015Document12 pagesMEC-001 - Micronomic Analysis 2015Ashwin R JohnNo ratings yet

- Swap Rate PaperDocument50 pagesSwap Rate PaperAshwin R JohnNo ratings yet

- Did Fair-Value Accounting Contribute To The Financial Crisis?Document48 pagesDid Fair-Value Accounting Contribute To The Financial Crisis?Ashwin R JohnNo ratings yet

- Fabm Module 10 Quarter 1Document8 pagesFabm Module 10 Quarter 1Rhea Alipio SadorraNo ratings yet

- Activity 13 May 2023 Key To CorrectionDocument1 pageActivity 13 May 2023 Key To CorrectionJohn Paul MagbitangNo ratings yet

- Downturn Upturn Expectations Consumption: Vocabulary 1: THE BUSINESS CYCLEDocument9 pagesDownturn Upturn Expectations Consumption: Vocabulary 1: THE BUSINESS CYCLEANH LƯƠNG NGUYỄN VÂNNo ratings yet

- SLBS Opportunities - 24 Jan 2024Document4 pagesSLBS Opportunities - 24 Jan 2024Pravin SinghNo ratings yet

- Muthoot Fincorp CalrificationsDocument6 pagesMuthoot Fincorp CalrificationslulughoshNo ratings yet

- Risk 2840202 Jan 2021Document3 pagesRisk 2840202 Jan 2021PILLO PATELNo ratings yet

- Renaissance University, Indore Proforma of First Page of PresentationsDocument7 pagesRenaissance University, Indore Proforma of First Page of PresentationsMudit MaheshwariNo ratings yet

- Exchange Rate Determination 1Document5 pagesExchange Rate Determination 1Tayyab Hassan ButtNo ratings yet

- EBIT - EPS QuestionsDocument6 pagesEBIT - EPS QuestionsTaliya ShaikhNo ratings yet

- Securities (Overweight - Initiate)Document41 pagesSecurities (Overweight - Initiate)Danh Phạm ThànhNo ratings yet

- The Liquidity Time Bomb by Nouriel Roubini - Project SyndicateDocument3 pagesThe Liquidity Time Bomb by Nouriel Roubini - Project SyndicateNickmann Ba'alNo ratings yet

- Fin Act - PUP-Manila - July 2009Document8 pagesFin Act - PUP-Manila - July 2009Lara Lewis AchillesNo ratings yet

- Presentation HDFC Mutual Fund - Product Suite - Oct 18Document57 pagesPresentation HDFC Mutual Fund - Product Suite - Oct 18ritik bumbakNo ratings yet

- Company Analysis - Electricite de France SA - FR0010242511 - EDF FP EquityDocument8 pagesCompany Analysis - Electricite de France SA - FR0010242511 - EDF FP EquityQ.M.S Advisors LLCNo ratings yet

- Calculation of DataDocument3 pagesCalculation of Datafahad fareedNo ratings yet

- CbloDocument6 pagesCbloPojigiNo ratings yet

- JP Morgan Jargon BusterDocument24 pagesJP Morgan Jargon BusterzowpowNo ratings yet

- Money-Wise E-BookDocument122 pagesMoney-Wise E-BookSuds NariNo ratings yet

- D14Document12 pagesD14YaniNo ratings yet

- TelephoneBill 8253069363Document3 pagesTelephoneBill 8253069363sourajpatelNo ratings yet

- A Study On Credit Risk Management at Canara Bank: Project Report Submitted in Partial Fulfilment of The Requirement ofDocument10 pagesA Study On Credit Risk Management at Canara Bank: Project Report Submitted in Partial Fulfilment of The Requirement ofbabuluckyNo ratings yet

- Quizesfm 2Document2 pagesQuizesfm 2Prince MalabaNo ratings yet

- Bonds and DepreciationDocument12 pagesBonds and DepreciationJayson Cuadra PagalaNo ratings yet

- Keys To Trading Gold US PDFDocument15 pagesKeys To Trading Gold US PDFfxindia19100% (2)

- Chapter 3 Case PartnershipDocument19 pagesChapter 3 Case PartnershipZPadsNo ratings yet

- BenefitIllustrationDocument4 pagesBenefitIllustrationshikha742642No ratings yet

- Currency ETFDocument1 pageCurrency ETFstrongasNo ratings yet

- MJ Channel Finance ProgramDocument3 pagesMJ Channel Finance ProgramSatyavir SinghNo ratings yet

- Lembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Document11 pagesLembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Putri AgustinaNo ratings yet

Download as pdf or txt

You might also like

- Answer Key Inter Acctg 2Document66 pagesAnswer Key Inter Acctg 2URBANO CREATIONS PRINTING & GRAPHICS100% (2)

- CAPM Approach Beta Is Dead or AliveDocument23 pagesCAPM Approach Beta Is Dead or AliveKazim KhanNo ratings yet

- Commodity Volatility SurfaceDocument4 pagesCommodity Volatility SurfaceMarco Avello IbarraNo ratings yet

- OIS Discounting PiterbargDocument6 pagesOIS Discounting PiterbargharsjusNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Asset Pricing ModelDocument62 pagesAsset Pricing ModelA. LatifNo ratings yet

- Textbook: Readings:: Cubs MSC Finance 1999-2000 Asset Management: Lecture 3Document13 pagesTextbook: Readings:: Cubs MSC Finance 1999-2000 Asset Management: Lecture 3Atif SaeedNo ratings yet

- The Capital Asset Pricing Model (CAPM)Document31 pagesThe Capital Asset Pricing Model (CAPM)Tanmay AbhijeetNo ratings yet

- Chapter 7: The CAPM: Investment ScienceDocument22 pagesChapter 7: The CAPM: Investment Scienceouji62No ratings yet

- Capital Market LineDocument8 pagesCapital Market Linecjpadin09No ratings yet

- Topic 4Document6 pagesTopic 4arp140102No ratings yet

- Do Taxes Matter in The CAPM?: 1 Presentation of The ProblemDocument8 pagesDo Taxes Matter in The CAPM?: 1 Presentation of The Problemapi-158666950No ratings yet

- CAPM Academic PieceDocument29 pagesCAPM Academic PiecespelicansNo ratings yet

- CAPM and The RisklessDocument28 pagesCAPM and The RisklessAdamNo ratings yet

- Capm 2004 ADocument35 pagesCapm 2004 Aobaidsimon123No ratings yet

- 7 AptDocument19 pages7 AptBikram MaharjanNo ratings yet

- Module 2 CAPMDocument11 pagesModule 2 CAPMTanvi DevadigaNo ratings yet

- Notes On DerivativesDocument7 pagesNotes On DerivativesLiliana AguirreNo ratings yet

- I.4.3 The Capital Asset Pricing Model: Investors' PreferencesDocument19 pagesI.4.3 The Capital Asset Pricing Model: Investors' Preferencesjohnsm2010No ratings yet

- Capital Market TheoryDocument5 pagesCapital Market TheoryZakia ElhamNo ratings yet

- Mefa 2 MarksDocument12 pagesMefa 2 MarksSaidinesh SurineniNo ratings yet

- Web Additional ExercisesDocument14 pagesWeb Additional ExercisesLeticia RoccaNo ratings yet

- The Liquidity Premium in Average Interest Rates : Wilbur John Coleman IIDocument17 pagesThe Liquidity Premium in Average Interest Rates : Wilbur John Coleman IIererereretrterNo ratings yet

- 04 Forward and Future Exchange RateDocument12 pages04 Forward and Future Exchange RateAdnan KamalNo ratings yet

- Port MNGT tRiskandReturn4Document105 pagesPort MNGT tRiskandReturn4guhandossNo ratings yet

- The Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchDocument22 pagesThe Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchThakur Raj AnandNo ratings yet

- Fama French 2004Document50 pagesFama French 2004William RamosNo ratings yet

- The Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchDocument27 pagesThe Capital Asset Pricing Model: Theory and Evidence: Eugene F. Fama and Kenneth R. FrenchAndus ManurungNo ratings yet

- Fama & French (CAPM)Document55 pagesFama & French (CAPM)NICOLE PATRICIA MUNOZ MERINONo ratings yet

- An Introduction To Portfolio Theory: Paul J. AtzbergerDocument16 pagesAn Introduction To Portfolio Theory: Paul J. AtzbergerSamNo ratings yet

- 1 19Document8 pages1 19Yilei RenNo ratings yet

- Security Analysis and Portfolio Management Selected Solutions To Problem Set #3: Section I: Portfolio Management 3) Portfolio Expected ReturnDocument7 pagesSecurity Analysis and Portfolio Management Selected Solutions To Problem Set #3: Section I: Portfolio Management 3) Portfolio Expected ReturnPradeep GuptaNo ratings yet

- Teaching Note 96-01: Default Risk As An Option: Version Date: November 3, 2003 C:/Classbackup/Teaching Notes/Tn96-01.WpdDocument5 pagesTeaching Note 96-01: Default Risk As An Option: Version Date: November 3, 2003 C:/Classbackup/Teaching Notes/Tn96-01.WpdVeeken ChaglassianNo ratings yet

- Valuation2 Oct6014Document7 pagesValuation2 Oct6014hoalongkiemNo ratings yet

- The Capital Asset Pricing Model (CAPM) : AssumptionsDocument4 pagesThe Capital Asset Pricing Model (CAPM) : AssumptionsRomazh Sifuentes RamirezNo ratings yet

- Chapter-10 Return & RiskDocument19 pagesChapter-10 Return & Riskaparajita promaNo ratings yet

- Exercises: Capital Asset Pricing Model (SOLUTIONS) : Department of Finance University of Basel Fall 2009Document4 pagesExercises: Capital Asset Pricing Model (SOLUTIONS) : Department of Finance University of Basel Fall 2009aftab20No ratings yet

- Chapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnDocument9 pagesChapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnBiloni KadakiaNo ratings yet

- Indifference Curve, Which Reflects That Investor's Preferences Regarding Risk and Return, IsDocument5 pagesIndifference Curve, Which Reflects That Investor's Preferences Regarding Risk and Return, Ismd mehedi hasanNo ratings yet

- Black 1976 Debt CovenantsDocument17 pagesBlack 1976 Debt Covenantsk60.2112343080No ratings yet

- The Mathematics of Ponzi SchemesDocument26 pagesThe Mathematics of Ponzi SchemesSPaul7No ratings yet

- WACC and APV RevisitedDocument11 pagesWACC and APV Revisitedrogelio rojasNo ratings yet

- CAPMDocument43 pagesCAPMProf.V.Vanaja sureshNo ratings yet

- Problem Set 2: 1 Insurance With Adverse SelectionDocument5 pagesProblem Set 2: 1 Insurance With Adverse SelectionAmine El AzdiNo ratings yet

- Portfolio Management 1Document28 pagesPortfolio Management 1Sattar Md AbdusNo ratings yet

- Pricing Swaps Including Funding CostsDocument19 pagesPricing Swaps Including Funding CostsobrefoNo ratings yet

- An Introduction To Modern Portfolio TheoryDocument38 pagesAn Introduction To Modern Portfolio Theoryhmme21No ratings yet

- MFPMDocument25 pagesMFPMMadhusmita MishraNo ratings yet

- Optimal Risky PortfolioDocument25 pagesOptimal Risky PortfolioAlexandra HsiajsnaksNo ratings yet

- Module - 4b - CAL, CMT, CAPM, SIM and APTDocument49 pagesModule - 4b - CAL, CMT, CAPM, SIM and APTGourav ParidaNo ratings yet

- Analysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelDocument8 pagesAnalysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelAmal AsseyrNo ratings yet

- A Laymans Approach To Black-Litterman ModelDocument7 pagesA Laymans Approach To Black-Litterman Modelswinki3No ratings yet

- The Transactions Demand For Cash: An Inventory Theoretic Approac FDocument15 pagesThe Transactions Demand For Cash: An Inventory Theoretic Approac FCanela DavidNo ratings yet

- Book An Introduction To The Math of Financial Derivatives Neftci S.N. SOLUTIONDocument90 pagesBook An Introduction To The Math of Financial Derivatives Neftci S.N. SOLUTIONAtiqur KhanNo ratings yet

- Arbitrage Pricing TheoryDocument15 pagesArbitrage Pricing TheoryYixing ZhangNo ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- The Volatility Surface: A Practitioner's GuideFrom EverandThe Volatility Surface: A Practitioner's GuideRating: 4 out of 5 stars4/5 (4)

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioFrom EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioRating: 4.5 out of 5 stars4.5/5 (3)

- Time: 3 Hours Maximum Marks: 100 Note: Attempt Questions From Each Section As Per Instructions GivenDocument4 pagesTime: 3 Hours Maximum Marks: 100 Note: Attempt Questions From Each Section As Per Instructions GivenAshwin R JohnNo ratings yet

- Mec-003 QT 2014Document7 pagesMec-003 QT 2014Ashwin R John100% (1)

- Master of Arts (Economics) : Time: 3 Hours Maximum Marks: 100 Note: Answer Questions From Each Section As DirectedDocument4 pagesMaster of Arts (Economics) : Time: 3 Hours Maximum Marks: 100 Note: Answer Questions From Each Section As DirectedAshwin R JohnNo ratings yet

- MEC-001 - Micronomic Analysis 2015Document12 pagesMEC-001 - Micronomic Analysis 2015Ashwin R JohnNo ratings yet

- Swap Rate PaperDocument50 pagesSwap Rate PaperAshwin R JohnNo ratings yet

- Did Fair-Value Accounting Contribute To The Financial Crisis?Document48 pagesDid Fair-Value Accounting Contribute To The Financial Crisis?Ashwin R JohnNo ratings yet

- Fabm Module 10 Quarter 1Document8 pagesFabm Module 10 Quarter 1Rhea Alipio SadorraNo ratings yet

- Activity 13 May 2023 Key To CorrectionDocument1 pageActivity 13 May 2023 Key To CorrectionJohn Paul MagbitangNo ratings yet

- Downturn Upturn Expectations Consumption: Vocabulary 1: THE BUSINESS CYCLEDocument9 pagesDownturn Upturn Expectations Consumption: Vocabulary 1: THE BUSINESS CYCLEANH LƯƠNG NGUYỄN VÂNNo ratings yet

- SLBS Opportunities - 24 Jan 2024Document4 pagesSLBS Opportunities - 24 Jan 2024Pravin SinghNo ratings yet

- Muthoot Fincorp CalrificationsDocument6 pagesMuthoot Fincorp CalrificationslulughoshNo ratings yet

- Risk 2840202 Jan 2021Document3 pagesRisk 2840202 Jan 2021PILLO PATELNo ratings yet

- Renaissance University, Indore Proforma of First Page of PresentationsDocument7 pagesRenaissance University, Indore Proforma of First Page of PresentationsMudit MaheshwariNo ratings yet

- Exchange Rate Determination 1Document5 pagesExchange Rate Determination 1Tayyab Hassan ButtNo ratings yet

- EBIT - EPS QuestionsDocument6 pagesEBIT - EPS QuestionsTaliya ShaikhNo ratings yet

- Securities (Overweight - Initiate)Document41 pagesSecurities (Overweight - Initiate)Danh Phạm ThànhNo ratings yet

- The Liquidity Time Bomb by Nouriel Roubini - Project SyndicateDocument3 pagesThe Liquidity Time Bomb by Nouriel Roubini - Project SyndicateNickmann Ba'alNo ratings yet

- Fin Act - PUP-Manila - July 2009Document8 pagesFin Act - PUP-Manila - July 2009Lara Lewis AchillesNo ratings yet

- Presentation HDFC Mutual Fund - Product Suite - Oct 18Document57 pagesPresentation HDFC Mutual Fund - Product Suite - Oct 18ritik bumbakNo ratings yet

- Company Analysis - Electricite de France SA - FR0010242511 - EDF FP EquityDocument8 pagesCompany Analysis - Electricite de France SA - FR0010242511 - EDF FP EquityQ.M.S Advisors LLCNo ratings yet

- Calculation of DataDocument3 pagesCalculation of Datafahad fareedNo ratings yet

- CbloDocument6 pagesCbloPojigiNo ratings yet

- JP Morgan Jargon BusterDocument24 pagesJP Morgan Jargon BusterzowpowNo ratings yet

- Money-Wise E-BookDocument122 pagesMoney-Wise E-BookSuds NariNo ratings yet

- D14Document12 pagesD14YaniNo ratings yet

- TelephoneBill 8253069363Document3 pagesTelephoneBill 8253069363sourajpatelNo ratings yet

- A Study On Credit Risk Management at Canara Bank: Project Report Submitted in Partial Fulfilment of The Requirement ofDocument10 pagesA Study On Credit Risk Management at Canara Bank: Project Report Submitted in Partial Fulfilment of The Requirement ofbabuluckyNo ratings yet

- Quizesfm 2Document2 pagesQuizesfm 2Prince MalabaNo ratings yet

- Bonds and DepreciationDocument12 pagesBonds and DepreciationJayson Cuadra PagalaNo ratings yet

- Keys To Trading Gold US PDFDocument15 pagesKeys To Trading Gold US PDFfxindia19100% (2)

- Chapter 3 Case PartnershipDocument19 pagesChapter 3 Case PartnershipZPadsNo ratings yet

- BenefitIllustrationDocument4 pagesBenefitIllustrationshikha742642No ratings yet

- Currency ETFDocument1 pageCurrency ETFstrongasNo ratings yet

- MJ Channel Finance ProgramDocument3 pagesMJ Channel Finance ProgramSatyavir SinghNo ratings yet

- Lembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Document11 pagesLembar Kerja Mengelola Buku Jurnal: Praktek Akuntansi Keuangan (Manual)Putri AgustinaNo ratings yet