Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5824)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chap 02Document25 pagesChap 02Tim JamesNo ratings yet

- Formulating Company PoliciesDocument8 pagesFormulating Company PoliciesKyambadde FranciscoNo ratings yet

- Tip Reporting - Tips vs. Service ChargesDocument2 pagesTip Reporting - Tips vs. Service ChargesOConnor DaviesNo ratings yet

- Organizational IT SecurityDocument2 pagesOrganizational IT SecurityOConnor DaviesNo ratings yet

- Audit and Accounting UpdateDocument4 pagesAudit and Accounting UpdateOConnor DaviesNo ratings yet

- Increased Scrutiny Over HIPAA Compliance AheadDocument3 pagesIncreased Scrutiny Over HIPAA Compliance AheadOConnor DaviesNo ratings yet

- Chat, BTC AdvantageDocument2 pagesChat, BTC Advantagesu baiNo ratings yet

- Asos Com Edition 14 PDFDocument4 pagesAsos Com Edition 14 PDFShakeel JanhangeerNo ratings yet

- Ecss M ST 40c Rev.1 (6march2009)Document103 pagesEcss M ST 40c Rev.1 (6march2009)jsadachiNo ratings yet

- Review 1Document24 pagesReview 1Michael LoenardiNo ratings yet

- Advertisement Vs Sales PromotionDocument29 pagesAdvertisement Vs Sales PromotionPoorna VenkatNo ratings yet

- Summary of Your Banking Relationship: Savings & InvestmentsDocument3 pagesSummary of Your Banking Relationship: Savings & InvestmentsJeffreyNo ratings yet

- ExxonDocument5 pagesExxonyozoranoNo ratings yet

- Argument Essay ExampleDocument3 pagesArgument Essay ExampleParth KapilNo ratings yet

- Workflow Performance TuningDocument74 pagesWorkflow Performance TuningSumit PawarNo ratings yet

- Milling and Grain - April 2015 - FULL EDITIONDocument100 pagesMilling and Grain - April 2015 - FULL EDITIONMilling and Grain magazineNo ratings yet

- Comparison of Selected Equity Capital and Mutual Fund Schemes in Respect Their RiskDocument7 pagesComparison of Selected Equity Capital and Mutual Fund Schemes in Respect Their RiskSuman V RaichurNo ratings yet

- Service Marketing: Service Failures - Recovery StrategiesDocument25 pagesService Marketing: Service Failures - Recovery StrategiesReyad100% (1)

- Pradhan Mantri Jan Dhan YojnaDocument55 pagesPradhan Mantri Jan Dhan YojnaKuanlNo ratings yet

- Transportation Law Course Outline PDFDocument9 pagesTransportation Law Course Outline PDFjsmecayerNo ratings yet

- City Gas Distribution Projects: 8 Petro IndiaDocument22 pagesCity Gas Distribution Projects: 8 Petro Indiavijay240483No ratings yet

- Sazon V Vasquez and Petron V Joven & ErmaDocument18 pagesSazon V Vasquez and Petron V Joven & ErmaAngelo Lajarca100% (1)

- Invoice: Yiwu Miaofu Home Decor CompanyDocument8 pagesInvoice: Yiwu Miaofu Home Decor CompanyAldair CarazasNo ratings yet

- Terex Genie Rl4000 Parts ManualDocument5 pagesTerex Genie Rl4000 Parts Manualwesley100% (36)

- DoP - ARCWELD - AS2 - LEA - 617 - 0Document1 pageDoP - ARCWELD - AS2 - LEA - 617 - 0Felicia Cioaba100% (1)

- An20231002 1430Document4 pagesAn20231002 1430Jozel DogelioNo ratings yet

- Nci Presentation 14Document261 pagesNci Presentation 14drmohamed120No ratings yet

- Business Plan QuestionnaireDocument3 pagesBusiness Plan QuestionnaireZain KhalidNo ratings yet

- Weekly Inside Bar (WIB), Technical Analysis ScannerDocument4 pagesWeekly Inside Bar (WIB), Technical Analysis ScannerDeepak KansalNo ratings yet

- SI52 BP Monitoring BookDocument34 pagesSI52 BP Monitoring BookmalakondareddyNo ratings yet

- Accounting 9th Edition Hoggett Solutions ManualDocument35 pagesAccounting 9th Edition Hoggett Solutions Manualmellow.duncical.v9vuq100% (27)

- (1)Document8 pages(1)Minh ThiNo ratings yet

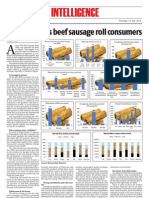

- Meet Nigeria's Beef Sausage Roll ConsumersDocument1 pageMeet Nigeria's Beef Sausage Roll ConsumersObodo EjiroNo ratings yet

- Datebase 2Document11 pagesDatebase 2jm syNo ratings yet