Download as rtf, pdf, or txt

You might also like

- Mabel Wong's Professional PracticeDocument7 pagesMabel Wong's Professional PracticeClene Doconte44% (9)

- Practice MCQs - Set 02Document16 pagesPractice MCQs - Set 02Minh HoàngNo ratings yet

- Blueprint To A BillionDocument20 pagesBlueprint To A Billionolumakin100% (1)

- Angel Broking Internship ReportDocument48 pagesAngel Broking Internship ReportUstaado KE Ustaad100% (1)

- The StartUp Kit: Everything you need to start a small businessFrom EverandThe StartUp Kit: Everything you need to start a small businessRating: 4 out of 5 stars4/5 (8)

- Hemant Kandpal Internship ReportDocument30 pagesHemant Kandpal Internship Reporthemant kandpalNo ratings yet

- Project On Demat Account FinalDocument74 pagesProject On Demat Account Finalgoyalraju073% (48)

- Marketing Strategies of Mahindra TractorsDocument62 pagesMarketing Strategies of Mahindra TractorsAnil Puniya90% (10)

- Mahindra Project-Report NewDocument77 pagesMahindra Project-Report NewManjunath@11689% (9)

- The Entrepreneurial EmergencyDocument60 pagesThe Entrepreneurial Emergencyletmeinwillya100% (3)

- Blackbook Project On Export Import Bank of IndiaDocument75 pagesBlackbook Project On Export Import Bank of IndiaDhiraj Chaurasiya100% (1)

- Sip EdelweissDocument54 pagesSip Edelweissindra340% (2)

- A PROJECT REPORT On Equity Analysis IT SectorDocument75 pagesA PROJECT REPORT On Equity Analysis IT SectorRobin Awathare57% (7)

- 2016 FRM Part I Practice ExamDocument129 pages2016 FRM Part I Practice Examguliguru100% (3)

- Report On Ing-VysyaDocument112 pagesReport On Ing-VysyaBinit AgarwallaNo ratings yet

- ING-Vysya Summer Training ReportDocument112 pagesING-Vysya Summer Training Reportmukhargoel9096No ratings yet

- A Project Report On "Create Awareness of Bank'S Product Offered BY ING-Vysya Bank "Document40 pagesA Project Report On "Create Awareness of Bank'S Product Offered BY ING-Vysya Bank "Vikram SharmaNo ratings yet

- Pallavi ProjectDocument44 pagesPallavi ProjectPallavi GargNo ratings yet

- Amar ReportDocument76 pagesAmar ReportnishantchopraNo ratings yet

- New Project 3Document50 pagesNew Project 3Sagar BhargavNo ratings yet

- Comparative Analysis Between Unicon Investment and Its Competitors-2010Document102 pagesComparative Analysis Between Unicon Investment and Its Competitors-2010Vasudev GuptaNo ratings yet

- Project On Demat AccountDocument62 pagesProject On Demat Accountsmruti bansod100% (1)

- Mohammed Meraj Ul Haq TaquiDocument60 pagesMohammed Meraj Ul Haq TaquiAmit KapoorNo ratings yet

- A Study of Small and Medium Enterprises Loans Ing Vsaya BankDocument95 pagesA Study of Small and Medium Enterprises Loans Ing Vsaya BankSilvi KhuranaNo ratings yet

- A Summer Internship Project Report OnDocument21 pagesA Summer Internship Project Report Onpappu_k75% (4)

- Project Report ON: "Comparision of Ing Vysya Bank With Icici and HDFC Bank"Document17 pagesProject Report ON: "Comparision of Ing Vysya Bank With Icici and HDFC Bank"sudhanshuaswalNo ratings yet

- "Need of Financial Advisors For Mutual Fund Investment'': A Project Report ONDocument41 pages"Need of Financial Advisors For Mutual Fund Investment'': A Project Report ONRavi ShuklaNo ratings yet

- Study of Portfolio Management System: With Special Reference To Bajaj CapitalDocument119 pagesStudy of Portfolio Management System: With Special Reference To Bajaj CapitalhemubnnaNo ratings yet

- Financial Services Provided by Anand RathiDocument35 pagesFinancial Services Provided by Anand RathisokajiNo ratings yet

- Export Import Bank of India PDFDocument83 pagesExport Import Bank of India PDFPranav ViraNo ratings yet

- COMPANY ANALYSIS BAJAJ FINANCE NIKUNJ GohilDocument44 pagesCOMPANY ANALYSIS BAJAJ FINANCE NIKUNJ GohilURVISH GAJJAR100% (1)

- Demat AccountDocument67 pagesDemat AccountAvijit MitraNo ratings yet

- Angel Broking Project ReportDocument51 pagesAngel Broking Project ReportKomica Garg100% (3)

- The Origin of ING Group: ProfileDocument36 pagesThe Origin of ING Group: ProfilefunnycreationsNo ratings yet

- Blackbook Project On Export Import Bank of IndiaDocument75 pagesBlackbook Project On Export Import Bank of IndiaLaxman bhosaleNo ratings yet

- 360 Degree Financial Planning (Bajaj Capital LTD)Document47 pages360 Degree Financial Planning (Bajaj Capital LTD)Asin Ganguly100% (1)

- Project On Reliance MoneyDocument74 pagesProject On Reliance MoneyMrudul JoshiNo ratings yet

- Submission Type - FINAL REPORT Project Group - MWH 012 NMU 28.06.2020Document15 pagesSubmission Type - FINAL REPORT Project Group - MWH 012 NMU 28.06.2020Tejaswini SolankiNo ratings yet

- Pioneer Institute of ManagementV2Document58 pagesPioneer Institute of ManagementV2ashwinijindal10No ratings yet

- Sales Promotion Techniques Used by Outlook: A Report ONDocument41 pagesSales Promotion Techniques Used by Outlook: A Report ONRisi JayaswalNo ratings yet

- Kotak Mahindra BankDocument13 pagesKotak Mahindra BankKunal Singh100% (1)

- Axis Bank ProjectDocument19 pagesAxis Bank ProjectNikky NamdeoNo ratings yet

- Investment Services and Investment Process of Unicon Investment SolutionsDocument15 pagesInvestment Services and Investment Process of Unicon Investment SolutionsArif KhanNo ratings yet

- Project Canara Bank-123Document28 pagesProject Canara Bank-123Yaadrahulkumar MoharanaNo ratings yet

- Marketing Mix of Idbi Bank Insurance CompanyDocument16 pagesMarketing Mix of Idbi Bank Insurance CompanydimanshuNo ratings yet

- Customer Relationship Management On Retail Banking. On ING BANKDocument63 pagesCustomer Relationship Management On Retail Banking. On ING BANKNilesh SahuNo ratings yet

- Sutithi Das (20192356) - SIP ReportDocument41 pagesSutithi Das (20192356) - SIP ReportNIKHIL KUMAR AGRAWALNo ratings yet

- IndusInd Bank LTD.Document72 pagesIndusInd Bank LTD.Prateek Logani100% (2)

- Project Report On ING Vysya BankDocument48 pagesProject Report On ING Vysya BankRahul SawantNo ratings yet

- Summer Training Report On Mas FinanceDocument73 pagesSummer Training Report On Mas FinanceHimanshu Singh TanwarNo ratings yet

- Alankit Assignments LTD.: Project Report ONDocument84 pagesAlankit Assignments LTD.: Project Report ONmannuNo ratings yet

- DR A.P.J. Abdul Kalam Technical University Lucknow: Uttam Group of InstitutionsDocument31 pagesDR A.P.J. Abdul Kalam Technical University Lucknow: Uttam Group of InstitutionsMayank jainNo ratings yet

- Study On Consumer Durable Loans and GoodsDocument73 pagesStudy On Consumer Durable Loans and GoodsRoshan Ghatge RG100% (1)

- A Project Report On HDFC Bank Submiited by Ankita SinghDocument30 pagesA Project Report On HDFC Bank Submiited by Ankita SinghShalu KumariNo ratings yet

- Customer Satisfactn in Tata Aig LicDocument47 pagesCustomer Satisfactn in Tata Aig Lichimanshusharma007100% (2)

- Riddhi JoshiDocument40 pagesRiddhi JoshiRiddhi JoshiNo ratings yet

- The Innovation Toolkit: Insights to help executives stay ahead of the curveFrom EverandThe Innovation Toolkit: Insights to help executives stay ahead of the curveNo ratings yet

- Incubating Indonesia’s Young Entrepreneurs:: Recommendations for Improving Development ProgramsFrom EverandIncubating Indonesia’s Young Entrepreneurs:: Recommendations for Improving Development ProgramsNo ratings yet

- Customer at the Heart: How B2B leaders build successful Customer-Centric OrganisationsFrom EverandCustomer at the Heart: How B2B leaders build successful Customer-Centric OrganisationsNo ratings yet

- Summary of Josh Anon & Carlos González de Villaumbrosia's The Product BookFrom EverandSummary of Josh Anon & Carlos González de Villaumbrosia's The Product BookNo ratings yet

- The Lean Startup (Review and Analysis of Ries' Book)From EverandThe Lean Startup (Review and Analysis of Ries' Book)Rating: 4.5 out of 5 stars4.5/5 (4)

- Non Code Businesses: A Comprehensive Guide on How to Start and SucceedFrom EverandNon Code Businesses: A Comprehensive Guide on How to Start and SucceedNo ratings yet

- Project Report On Bajaj Allianzlife Insurance Co LTDDocument99 pagesProject Report On Bajaj Allianzlife Insurance Co LTDManjunath@116No ratings yet

- Aipmt 2010 ScreeningDocument55 pagesAipmt 2010 ScreeningManjunath@116No ratings yet

- Canon IR400 BrochureDocument7 pagesCanon IR400 BrochureManjunath@116No ratings yet

- Mba MarketingDocument35 pagesMba MarketingRitupan KalitaNo ratings yet

- Health and Safety HandbookDocument126 pagesHealth and Safety HandbookManjunath@116100% (1)

- A Project Report On Labour Welfare and SafetyDocument82 pagesA Project Report On Labour Welfare and SafetyManjunath@116100% (1)

- Study The Consumer Awareness About Nandini Milk and Milk Products and Impact of Promotional Activities On Creating AwarenessDocument75 pagesStudy The Consumer Awareness About Nandini Milk and Milk Products and Impact of Promotional Activities On Creating AwarenessManjunath@116No ratings yet

- "Training and Development at Airtel": A Summer Training Report INDocument62 pages"Training and Development at Airtel": A Summer Training Report INdjboyashish0% (1)

- Union Bank Credit Appraisal Project ReportDocument43 pagesUnion Bank Credit Appraisal Project Reportkamdica42% (12)

- Summer Project On SBIDocument63 pagesSummer Project On SBIchinmaya.parija73% (52)

- A Project Report On Labour Welfare and SafetyDocument82 pagesA Project Report On Labour Welfare and SafetyManjunath@116100% (1)

- HR ProjectsDocument6 pagesHR ProjectsManjunath@116No ratings yet

- Organisation Structure of Air Tel: Sri. - BBM Degree College, GulbargaDocument49 pagesOrganisation Structure of Air Tel: Sri. - BBM Degree College, GulbargaManjunath@1160% (1)

- Canon IR400 BrochureDocument7 pagesCanon IR400 BrochureManjunath@116No ratings yet

- Ultratech CementDocument53 pagesUltratech CementManjunath@116100% (2)

- State Bank of India: Department of Commerce & Management Government Degree College, GulbargaDocument33 pagesState Bank of India: Department of Commerce & Management Government Degree College, GulbargaManjunath@116No ratings yet

- Chapter - 1: Study of Recruitment Policies and Procedure Adopted in Icici Prudential Life Insurance LTD."Document60 pagesChapter - 1: Study of Recruitment Policies and Procedure Adopted in Icici Prudential Life Insurance LTD."Manjunath@116No ratings yet

- Project Report On Market Share of AirtelDocument84 pagesProject Report On Market Share of AirtelSimran Dhanjal75% (12)

- Birla Sun Life Mutual FundDocument75 pagesBirla Sun Life Mutual FundManjunath@116No ratings yet

- Comfort LetterDocument5 pagesComfort LetterAfrizar PaneNo ratings yet

- Time Value of Money Solutions PDFDocument12 pagesTime Value of Money Solutions PDFIoana Dragne100% (1)

- Presentation - On - Companies - Act2013 - K C MehtaDocument116 pagesPresentation - On - Companies - Act2013 - K C MehtasarashviNo ratings yet

- Ornamental Fish Industry in Sri LankaDocument49 pagesOrnamental Fish Industry in Sri LankaSupun Abayawardana100% (4)

- Titan AR 2002-03Document10 pagesTitan AR 2002-03bondamiNo ratings yet

- Liabilities ReviewerDocument4 pagesLiabilities ReviewerTessie GonzalesNo ratings yet

- Pas 20 Government Grant: Conceptual Framework and Accounting StantardsDocument6 pagesPas 20 Government Grant: Conceptual Framework and Accounting StantardsMeg sharkNo ratings yet

- Intercompany Profit Transactions - 02.20.18Document36 pagesIntercompany Profit Transactions - 02.20.18Venz LacreNo ratings yet

- G.R. No. L-69344 April 26, 1991 Pg. 191Document3 pagesG.R. No. L-69344 April 26, 1991 Pg. 191Allysa Lei Delos ReyesNo ratings yet

- Republic Vs GonzalesDocument2 pagesRepublic Vs GonzalesCarl MontemayorNo ratings yet

- Lecture Note On Project AppraisalDocument36 pagesLecture Note On Project Appraisalmatiwos samuel100% (3)

- Super Ethereum White Paper v.1.2018Document31 pagesSuper Ethereum White Paper v.1.2018Anonymous cRJ33LNNkNo ratings yet

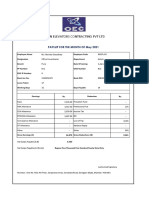

- Orion Elevators Contracting PVT LTD: Payslip For The Month of May 2021Document1 pageOrion Elevators Contracting PVT LTD: Payslip For The Month of May 2021Monika ChoudhariNo ratings yet

- Merged Na para Minsanan Sa CTRL FDocument139 pagesMerged Na para Minsanan Sa CTRL FAngelica PostreNo ratings yet

- Tax ReviewerDocument10 pagesTax ReviewerClaire ZafraNo ratings yet

- Paystub Golden Limousine, Inc 20210906 20210919Document2 pagesPaystub Golden Limousine, Inc 20210906 20210919Alexander Weir-WitmerNo ratings yet

- Option StrategiesDocument24 pagesOption Strategiesarvi2020100% (1)

- (Drewry) Ports & Terminals Insight - 2017Document34 pages(Drewry) Ports & Terminals Insight - 2017Ngo Tung100% (1)

- Chapter 21 Business Cycle, Changes in The General Price Level and UnemploymentDocument58 pagesChapter 21 Business Cycle, Changes in The General Price Level and UnemploymentJason ChungNo ratings yet

- 15 ABS CBN vs. CTA 108 SCRA 142Document6 pages15 ABS CBN vs. CTA 108 SCRA 142Rogelio CartinNo ratings yet

- Pension RulesDocument70 pagesPension RulesSehrish MemonNo ratings yet

- Principles of TaxationDocument25 pagesPrinciples of TaxationceejayeNo ratings yet

- Chapter IIIDocument54 pagesChapter IIINesri YayaNo ratings yet

- Time Value FinalDocument3 pagesTime Value FinalRamiro Magbanua Feliciano100% (1)

- Example of Prior Period ErrorDocument2 pagesExample of Prior Period ErrorMjhayeNo ratings yet