Download as pdf or txt

You might also like

- World Oil SupplyDocument3 pagesWorld Oil SupplyAnu ReetNo ratings yet

- Hydro Skimming Margins Vs Cracking MarginsDocument4 pagesHydro Skimming Margins Vs Cracking MarginsHassan RazaNo ratings yet

- Oil PricesDocument19 pagesOil PricesAjay KumarNo ratings yet

- Peak Oil Review Vol. 3 No. 47 November 24Document6 pagesPeak Oil Review Vol. 3 No. 47 November 24api-26190745No ratings yet

- Global Crude Oil and Liquid Fuels U.S. Crude Oil and Liquid Fuels Natural Gas Electricity Coal Carbon Dioxide EmissionsDocument38 pagesGlobal Crude Oil and Liquid Fuels U.S. Crude Oil and Liquid Fuels Natural Gas Electricity Coal Carbon Dioxide EmissionsMeenal Prabal BhadoriaNo ratings yet

- Task 2 - ImplementationDocument6 pagesTask 2 - ImplementationIndianagrofarmsNo ratings yet

- OPEC - Monthly Oil Market ReportDocument75 pagesOPEC - Monthly Oil Market Reportrryan123123No ratings yet

- Fundamental Analysis of Crude OilDocument15 pagesFundamental Analysis of Crude Oilmoxit shahNo ratings yet

- 2010 CNPC Industry Report 20110124Document29 pages2010 CNPC Industry Report 20110124Amanpreet SinghNo ratings yet

- Oil Prices Core GeorgetownDocument196 pagesOil Prices Core GeorgetownMichael LiNo ratings yet

- World Oil Market report-IEA-2010Document71 pagesWorld Oil Market report-IEA-2010Fnu JoefrizalNo ratings yet

- Short Term Energy Outlook: HighlightsDocument39 pagesShort Term Energy Outlook: HighlightswillywNo ratings yet

- 14DEC2022 OilMarketReportDocument74 pages14DEC2022 OilMarketReportCheng KellynNo ratings yet

- CS - OPEC CartelDocument4 pagesCS - OPEC Cartelroshansv23No ratings yet

- Energy Data Highlights: China, Kazakhstan Sign Agreement To Expand Natural-Gas Pipeline NetworkDocument8 pagesEnergy Data Highlights: China, Kazakhstan Sign Agreement To Expand Natural-Gas Pipeline NetworkchoiceenergyNo ratings yet

- Gasoline Prices PrimerDocument17 pagesGasoline Prices PrimerEnergy Tomorrow50% (2)

- Energy Report - 7th March 2011Document5 pagesEnergy Report - 7th March 2011sandeep duranNo ratings yet

- How Are Oil Prices DeterminedDocument8 pagesHow Are Oil Prices DeterminedSumit SachdevaNo ratings yet

- 01 Changes Supply Demand Crude OilDocument14 pages01 Changes Supply Demand Crude Oilkaustubh_dec17No ratings yet

- Oil Price Shocks and The Nigeria Economy: A Variance Autoregressive (VAR) ModelDocument11 pagesOil Price Shocks and The Nigeria Economy: A Variance Autoregressive (VAR) ModelDiamante GomezNo ratings yet

- Koyama Ken (2005)Document18 pagesKoyama Ken (2005)zati azizNo ratings yet

- OPEC's Oil Production QuotasDocument7 pagesOPEC's Oil Production QuotasYash BhayaniNo ratings yet

- Input For Possible ArticleDocument3 pagesInput For Possible ArticleRG MoPNGNo ratings yet

- Astenbeck Capital Letter July2015Document9 pagesAstenbeck Capital Letter July2015ZerohedgeNo ratings yet

- R.Lakshmi Anvitha (1226213102) : Green TechnologiesDocument8 pagesR.Lakshmi Anvitha (1226213102) : Green TechnologiesTejeesh Chandra PonnagantiNo ratings yet

- Reuters Analysis 2014 Oil CrashDocument19 pagesReuters Analysis 2014 Oil Crashjohn smith100% (1)

- Presentazione Riyadh 25janDocument16 pagesPresentazione Riyadh 25janLfshriyadh100% (1)

- Industry Analysts Expect That Hundreds More Rigs WillDocument6 pagesIndustry Analysts Expect That Hundreds More Rigs Willapi-26190745No ratings yet

- Yousif Al Ateeqi - 207116632: Petrolium Assignment 3/11/2010Document4 pagesYousif Al Ateeqi - 207116632: Petrolium Assignment 3/11/2010Yousif Al AteeqiNo ratings yet

- Slide in Oil PricesDocument7 pagesSlide in Oil PricesRituparna SamantarayNo ratings yet

- Energy Data Highlights: Power Outage May Have Caused More Than $100M in Losses To AreaDocument8 pagesEnergy Data Highlights: Power Outage May Have Caused More Than $100M in Losses To AreachoiceenergyNo ratings yet

- Team - Mud Men: Past Events Regarding ConflictDocument2 pagesTeam - Mud Men: Past Events Regarding ConflictsourravNo ratings yet

- Oil Monitor As of 27 September 2022Document2 pagesOil Monitor As of 27 September 2022Reighn Kirsten DimacaleNo ratings yet

- OPEC Oil Outlook 2030Document22 pagesOPEC Oil Outlook 2030Bruno Dias da CostaNo ratings yet

- Understanding Shocks of Oil Prices: IJASCSE Vol 1 Issue 1 2012Document7 pagesUnderstanding Shocks of Oil Prices: IJASCSE Vol 1 Issue 1 2012IJASCSENo ratings yet

- Crude Oil CommodityDocument19 pagesCrude Oil CommodityAbhishek NagNo ratings yet

- Energy Data Highlights: Japan Utilities' LNG Imports, Consumption Climb To RecordDocument7 pagesEnergy Data Highlights: Japan Utilities' LNG Imports, Consumption Climb To RecordchoiceenergyNo ratings yet

- Oil DemandDocument64 pagesOil Demandkaustubh_dec17No ratings yet

- EPIC Shale Oil Presentation FINAL 4.13.151Document24 pagesEPIC Shale Oil Presentation FINAL 4.13.151Anonymous NmOXutCKNo ratings yet

- Using Technology To Increase Middle Distillate Production-EnglishDocument6 pagesUsing Technology To Increase Middle Distillate Production-Englishsaleh4060No ratings yet

- Natural Gas/ Power NewsDocument10 pagesNatural Gas/ Power NewschoiceenergyNo ratings yet

- Because When The Price of Crude Oil Fell in 2014, The Land Rose SignificantlyDocument3 pagesBecause When The Price of Crude Oil Fell in 2014, The Land Rose SignificantlyJulianaNo ratings yet

- Presentation On Oil PricesDocument41 pagesPresentation On Oil PricesVaibhav Garg0% (1)

- Marketing 2Document12 pagesMarketing 2Saul Martinez MolinaNo ratings yet

- Business Environment Presentation By: Tejas SinghDocument15 pagesBusiness Environment Presentation By: Tejas SinghParas SharmaNo ratings yet

- Short-Term Energy Outlook (STEO) : Forecast HighlightsDocument50 pagesShort-Term Energy Outlook (STEO) : Forecast HighlightsRudi DarussalamNo ratings yet

- Oil CrisisDocument26 pagesOil CrisisSagar MojidraNo ratings yet

- Effects of Oil Prices ON Economy: Muhammad Junaid Mughal ASC 2625 CMS 281144 SEC C 91Document20 pagesEffects of Oil Prices ON Economy: Muhammad Junaid Mughal ASC 2625 CMS 281144 SEC C 91Junaid MughalNo ratings yet

- Oil Market Report (июнь 2023) IEADocument47 pagesOil Market Report (июнь 2023) IEAmaryli121212No ratings yet

- Oil Prices2Document40 pagesOil Prices2ediwskiNo ratings yet

- Energy Data Highlights: Frosty Air Heating Up Gas FuturesDocument8 pagesEnergy Data Highlights: Frosty Air Heating Up Gas FutureschoiceenergyNo ratings yet

- Middle East Energy May 2013Document23 pagesMiddle East Energy May 2013Naseem AhmadNo ratings yet

- Demand of Petrolium ProductDocument18 pagesDemand of Petrolium ProductSwapnil MurudkarNo ratings yet

- Commodities Letter December 2014Document5 pagesCommodities Letter December 2014Swedbank AB (publ)No ratings yet

- Oil Price FluctuationDocument28 pagesOil Price FluctuationmksscribdNo ratings yet

- Using Technology To Increase Middle Distillate Production-EnglishDocument6 pagesUsing Technology To Increase Middle Distillate Production-Englishtapanpatni100% (1)

- 2012 - Oil and The Global EconomyDocument6 pages2012 - Oil and The Global EconomyLogan JulienNo ratings yet

- FOCUS REPORT: U.S. Shale Gale under Threat from Oil Price PlungeFrom EverandFOCUS REPORT: U.S. Shale Gale under Threat from Oil Price PlungeRating: 2 out of 5 stars2/5 (1)

- An Introduction to Petroleum Technology, Economics, and PoliticsFrom EverandAn Introduction to Petroleum Technology, Economics, and PoliticsNo ratings yet

- Energy Myths and Realities: Bringing Science to the Energy Policy DebateFrom EverandEnergy Myths and Realities: Bringing Science to the Energy Policy DebateRating: 4 out of 5 stars4/5 (4)

- Advance Monthly Sales For Retail and Food Services September 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services September 2010qtipxNo ratings yet

- Speech 456Document11 pagesSpeech 456qtipxNo ratings yet

- Euro Area Annual Inflation Up To 1.9%Document4 pagesEuro Area Annual Inflation Up To 1.9%qtipxNo ratings yet

- Tots ADocument2 pagesTots AqtipxNo ratings yet

- Mtis CurrentDocument3 pagesMtis CurrentqtipxNo ratings yet

- Euro Area and EU27 GDP Up by 1.0%Document6 pagesEuro Area and EU27 GDP Up by 1.0%qtipxNo ratings yet

- NewresconstDocument6 pagesNewresconstqtipxNo ratings yet

- Final Cat Inc ReleaseDocument34 pagesFinal Cat Inc ReleaseqtipxNo ratings yet

- Money and Asset Prices: Indicators of Market UncertaintyDocument9 pagesMoney and Asset Prices: Indicators of Market UncertaintyqtipxNo ratings yet

- PR201007Document1 pagePR201007qtipxNo ratings yet

- Obama Administration Introduces Monthly Housing ScorecardDocument11 pagesObama Administration Introduces Monthly Housing ScorecardqtipxNo ratings yet

- 2010 First Quarter Business Review: (Unaudited)Document19 pages2010 First Quarter Business Review: (Unaudited)qtipxNo ratings yet

- Advance Monthly Sales For Retail and Food Services APRIL 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services APRIL 2010qtipxNo ratings yet

- Advance Monthly Sales For Retail and Food Services JUNE 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services JUNE 2010qtipxNo ratings yet

- Q1 ProdDocument15 pagesQ1 ProdqtipxNo ratings yet

- U.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau NewsDocument4 pagesU.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau News U.S. Census Bureau NewsqtipxNo ratings yet

- CHN Jun 10 RevDocument3 pagesCHN Jun 10 RevqtipxNo ratings yet

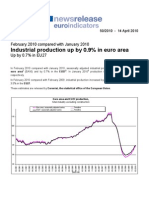

- Industrial Production Up by 0.9% in Euro AreaDocument6 pagesIndustrial Production Up by 0.9% in Euro AreaqtipxNo ratings yet

- gdp1q10 2ndDocument15 pagesgdp1q10 2ndqtipxNo ratings yet

- International Monetary Fund: How Did Emerging Markets Cope in The Crisis?Document47 pagesInternational Monetary Fund: How Did Emerging Markets Cope in The Crisis?qtipxNo ratings yet

- PPI March 2010Document22 pagesPPI March 2010qtipxNo ratings yet

- Cpi MayDocument19 pagesCpi MayqtipxNo ratings yet

- Joint Release U.S. Department of Housing and Urban DevelopmentDocument6 pagesJoint Release U.S. Department of Housing and Urban DevelopmentqtipxNo ratings yet

- Small Businesses Add 66,000 New Jobs in AprilDocument5 pagesSmall Businesses Add 66,000 New Jobs in AprilqtipxNo ratings yet

- The Coca-Cola Company Reports 2010 First Quarter Financial ResultsDocument15 pagesThe Coca-Cola Company Reports 2010 First Quarter Financial ResultsqtipxNo ratings yet

- Advance Monthly Sales For Retail and Food Services MARCH 2010Document4 pagesAdvance Monthly Sales For Retail and Food Services MARCH 2010qtipxNo ratings yet

- Cpimar 10Document19 pagesCpimar 10qtipxNo ratings yet

- CMA Global Sovereign Credit Risk Report Q1 2010Document17 pagesCMA Global Sovereign Credit Risk Report Q1 2010qtipxNo ratings yet

- Eap April2010 ChinaDocument3 pagesEap April2010 ChinaqtipxNo ratings yet

- Euro Area GDP Stable and EU27 GDP Up by 0.1%Document10 pagesEuro Area GDP Stable and EU27 GDP Up by 0.1%qtipxNo ratings yet