Poster Appam

Poster Appam

You might also like

- Case 6 - University Day Care CentreDocument3 pagesCase 6 - University Day Care CentreAnirudh Gulur100% (3)

- Kipp Houston Public Schools: Case Study 9Document16 pagesKipp Houston Public Schools: Case Study 9Hafiz DabeerNo ratings yet

- Piedmont University Group 4Document24 pagesPiedmont University Group 4Sangita Dhamdhere100% (4)

- D O No. 2, S. 2013-Revised Implementing Guidelines and Regulations of RA No. 8525 Otherwise Known As The Adopt-A-School Program ActDocument15 pagesD O No. 2, S. 2013-Revised Implementing Guidelines and Regulations of RA No. 8525 Otherwise Known As The Adopt-A-School Program ActAllan Jr Pancho0% (1)

- Establishing Fiscal Strength in Higher Education; Management Strategies for Transformative Revenue GenerationFrom EverandEstablishing Fiscal Strength in Higher Education; Management Strategies for Transformative Revenue GenerationNo ratings yet

- 1 Swings and Roundabouts: Margaret BrownDocument24 pages1 Swings and Roundabouts: Margaret BrownSridhar SathyaNo ratings yet

- Chapter 4-5 RemedialDocument19 pagesChapter 4-5 RemedialTata Duero Lachica100% (4)

- Fiscal State of The University Spring 2013Document20 pagesFiscal State of The University Spring 2013dailytitanNo ratings yet

- Paradise Community Collegefy2014budgetDocument11 pagesParadise Community Collegefy2014budgetapi-222496408No ratings yet

- 2011-12 Financial State of The District - FinalDocument19 pages2011-12 Financial State of The District - FinalBrendan WalshNo ratings yet

- Employee Health Clinic 2017 BOS Work Session 09.14.17Document25 pagesEmployee Health Clinic 2017 BOS Work Session 09.14.17Fauquier NowNo ratings yet

- North Syracuse Central School District: Proposed BudgetDocument30 pagesNorth Syracuse Central School District: Proposed BudgetTime Warner Cable NewsNo ratings yet

- Performance Based BudgetingDocument19 pagesPerformance Based BudgetingAmit ToshniwalNo ratings yet

- Superintendent's Recommendation WebsiteDocument21 pagesSuperintendent's Recommendation WebsitedaggerpressNo ratings yet

- Financial InformationDocument80 pagesFinancial InformationStarLink1No ratings yet

- Harrisburg School District FY2012-13 FC 10-14-13 - 1Document9 pagesHarrisburg School District FY2012-13 FC 10-14-13 - 1Emily PrevitiNo ratings yet

- DeKalb County Schools Fiscal Year 2014 Proposed Budget Executive SummaryDocument9 pagesDeKalb County Schools Fiscal Year 2014 Proposed Budget Executive SummaryThe Brookhaven PostNo ratings yet

- Benchmark - Budget DefenseDocument15 pagesBenchmark - Budget Defenseapi-623626988No ratings yet

- The University of Iowa General Education Fund FY 2019 BudgetDocument33 pagesThe University of Iowa General Education Fund FY 2019 BudgetHimanshu SethNo ratings yet

- James McKenna's 2013-14 Proposed Budget Presentation, March 14, 2013.Document33 pagesJames McKenna's 2013-14 Proposed Budget Presentation, March 14, 2013.Suffolk TimesNo ratings yet

- Importance of Annual BudgetDocument10 pagesImportance of Annual BudgetNwigwe Promise ChukwuebukaNo ratings yet

- GPPSS 2012-13 Financial State of The District - FINALDocument18 pagesGPPSS 2012-13 Financial State of The District - FINALBrendan WalshNo ratings yet

- 2013 Evaluation For UND President Robert KelleyDocument3 pages2013 Evaluation For UND President Robert KelleyRob PortNo ratings yet

- F1attach3 PDFDocument220 pagesF1attach3 PDFriskyplayerNo ratings yet

- Shenendehowa School District Budget PresentationDocument21 pagesShenendehowa School District Budget PresentationDavid LombardoNo ratings yet

- New Public Fiscal Admin Module 1 Lesson 1Document30 pagesNew Public Fiscal Admin Module 1 Lesson 1Jöhn LöydNo ratings yet

- Shanayes Budget Defense BenchmarkDocument15 pagesShanayes Budget Defense Benchmarkapi-529462240100% (1)

- 2012 2013ProposedBudgetVersion2 6Document136 pages2012 2013ProposedBudgetVersion2 6Robert WilonskyNo ratings yet

- Performance Audit Report: Tuition Waivers and Student StipendsDocument87 pagesPerformance Audit Report: Tuition Waivers and Student StipendsRob PortNo ratings yet

- Salem-Keizer Schools Budget Message 2011-12Document32 pagesSalem-Keizer Schools Budget Message 2011-12Statesman JournalNo ratings yet

- TEKEVDocument26 pagesTEKEVYosafat KurniawanNo ratings yet

- Ead 510 Benchmark Budget Defense Keisha ThompsonDocument18 pagesEad 510 Benchmark Budget Defense Keisha Thompsonapi-671417127100% (1)

- Annual Budget: A Presentation To The Board of Governors February 2013Document20 pagesAnnual Budget: A Presentation To The Board of Governors February 2013jeanyoperNo ratings yet

- The Cooper Union Working Group ReportDocument54 pagesThe Cooper Union Working Group ReportarchitectmagNo ratings yet

- Description: Tags: 06reportsuppDocument3 pagesDescription: Tags: 06reportsuppanon-783284No ratings yet

- FY14 Superintendents Proposed BudgetDocument170 pagesFY14 Superintendents Proposed BudgetFauquier NowNo ratings yet

- Appendix 6 2008Document4 pagesAppendix 6 2008Sadaf InamNo ratings yet

- 2010-11 Budget Draft #2 - Final - UnabridgedDocument38 pages2010-11 Budget Draft #2 - Final - UnabridgedBrendan WalshNo ratings yet

- Module 5 SummaryDocument3 pagesModule 5 SummaryJoan Jambalos TuertoNo ratings yet

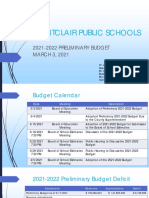

- Montclair's 2021-22 Preliminary School BudgetDocument18 pagesMontclair's 2021-22 Preliminary School BudgetLouis C. HochmanNo ratings yet

- Budget2012 13 - v4 1Document669 pagesBudget2012 13 - v4 1tawnellNo ratings yet

- Mcvey Mary - Ead - 510 - Clincial Field Experience B - Schoolwide Budgetary NeedsDocument8 pagesMcvey Mary - Ead - 510 - Clincial Field Experience B - Schoolwide Budgetary Needsapi-529486237No ratings yet

- Analysis of The Financial Situation of Kutztown University, by Howard BunsisDocument54 pagesAnalysis of The Financial Situation of Kutztown University, by Howard BunsisRCPressNo ratings yet

- Review of Chignecto-Central Regional School Board 2012-13 BudgetDocument26 pagesReview of Chignecto-Central Regional School Board 2012-13 Budgetnick_logan9361No ratings yet

- U of L Final Exec Comp Report v1Document55 pagesU of L Final Exec Comp Report v1petersoe0No ratings yet

- Abhi Project 1Document85 pagesAbhi Project 1sanketkumarrathiNo ratings yet

- Salem-Keizer Public Schools 2012-13 Budget Message (Draft)Document23 pagesSalem-Keizer Public Schools 2012-13 Budget Message (Draft)Statesman JournalNo ratings yet

- BudgetdefenseDocument15 pagesBudgetdefenseapi-559694769No ratings yet

- Group Assignment-Money PlantDocument13 pagesGroup Assignment-Money PlantnitiyahsegarNo ratings yet

- 2012-13 Proposed Budget DocumentDocument397 pages2012-13 Proposed Budget DocumentStatesman JournalNo ratings yet

- 2010-11 GPPSS Staffing and Budgeting ProcessDocument15 pages2010-11 GPPSS Staffing and Budgeting ProcessBrendan WalshNo ratings yet

- 2012 FiscalPlanning MOEDocument45 pages2012 FiscalPlanning MOEParents' Coalition of Montgomery County, MarylandNo ratings yet

- Return On Investment in Education: A "System-Strategy" ApproachDocument14 pagesReturn On Investment in Education: A "System-Strategy" ApproachAfzal LodhiNo ratings yet

- Outlaw 14-15 BudgetDocument5 pagesOutlaw 14-15 Budgetapi-282985696No ratings yet

- PRMEDocument4 pagesPRMEkatykat101001No ratings yet

- Presentation 1Document28 pagesPresentation 1api-207421477No ratings yet

- 2024 - 0213 TST BOCES Budget PresentationDocument11 pages2024 - 0213 TST BOCES Budget PresentationShadeNo ratings yet

- School Board Work Session Jan 17 2012Document23 pagesSchool Board Work Session Jan 17 2012SaveWekivaElementaryNo ratings yet

- School Budget Planning Guide Rev Oct 13Document11 pagesSchool Budget Planning Guide Rev Oct 13violeta soriano100% (1)

- 002 Apfs 01Document116 pages002 Apfs 01Kevin Chrysler MarcoNo ratings yet

- Financial Strategy for Higher Education: A Field Guide for Presidents, C F Os, and Boards of TrusteesFrom EverandFinancial Strategy for Higher Education: A Field Guide for Presidents, C F Os, and Boards of TrusteesNo ratings yet

- Full Text Skripsi Irma HidayahDocument129 pagesFull Text Skripsi Irma HidayahCindi SartonoNo ratings yet

- Em Tech Quarter 2 LAS Week 56Document24 pagesEm Tech Quarter 2 LAS Week 56gabby ilaganNo ratings yet

- Ten SquareDocument53 pagesTen SquareYork Daily Record/Sunday NewsNo ratings yet

- SCSD News ReleaseDocument1 pageSCSD News ReleaseAmanda GonzalesNo ratings yet

- Revised Group 11 PresentationDocument40 pagesRevised Group 11 PresentationJanet Floreno VillasanaNo ratings yet

- Action Plan in Esp & SportsDocument13 pagesAction Plan in Esp & SportsMay-ann Ramos Galliguez ValdezNo ratings yet

- Results-Based Performance Management System (RPMS) For TeachersDocument6 pagesResults-Based Performance Management System (RPMS) For TeachersMelanie AplacaNo ratings yet

- Handbook of Eduaction Policy Research PDFDocument6 pagesHandbook of Eduaction Policy Research PDFIlham NurhidayatNo ratings yet

- Hiep, Nguyen Tat, Non English-Major Students' Attitudes Towards E-Learning, 2021Document16 pagesHiep, Nguyen Tat, Non English-Major Students' Attitudes Towards E-Learning, 2021HrvojeNo ratings yet

- Borgo Free Jazz in The ClassroomDocument29 pagesBorgo Free Jazz in The ClassroomJohn PetrucelliNo ratings yet

- Innateness Theory PresentationDocument9 pagesInnateness Theory PresentationMarisol LealNo ratings yet

- Cebu Technological University: Republic of The PhilippinesDocument1 pageCebu Technological University: Republic of The PhilippinesCleo TokongNo ratings yet

- ManiDocument5 pagesManiOn Point management serviceNo ratings yet

- Syllabus Math1215 s22Document6 pagesSyllabus Math1215 s22Jordane WayNo ratings yet

- Dissertation Proposal University of LeedsDocument7 pagesDissertation Proposal University of LeedsPaperWritingServicesBestSingapore100% (1)

- MMO Sample Papers For Class 1Document19 pagesMMO Sample Papers For Class 1Linh DiệpNo ratings yet

- Catch Up Friday Feb 2Document7 pagesCatch Up Friday Feb 2Mark Laurenze Manga100% (2)

- Workplace Skills Assignment 2023Document6 pagesWorkplace Skills Assignment 2023c2qbrxcwqqNo ratings yet

- Homeroom PTA AgendaDocument5 pagesHomeroom PTA AgendaALPHA RACHEL TULINGNo ratings yet

- Course Syllabus - Food Service SystemDocument10 pagesCourse Syllabus - Food Service SystemDerick MacedaNo ratings yet

- History 4C - Paper #1: Pere GoriotDocument2 pagesHistory 4C - Paper #1: Pere GoriotSteven MackeyNo ratings yet

- Term 1 Week 6 Ey MinutesDocument2 pagesTerm 1 Week 6 Ey Minutesapi-459118418No ratings yet

- Sdact0m - 01 - Mark077 MarkedDocument6 pagesSdact0m - 01 - Mark077 MarkedEdmoreMucheka100% (1)

- Ielts Answer SheetDocument2 pagesIelts Answer SheetTharra JungNo ratings yet

- RPP BHS Inggris MilaDocument2 pagesRPP BHS Inggris MilaBio17 ArifNo ratings yet

- Omnibus Sworn CertificationDocument3 pagesOmnibus Sworn CertificationMarck Vyn LopezNo ratings yet

- Enclosure No 4 INSET SESSION GUIDE TEMPLATE SCHOOL LEVELDocument2 pagesEnclosure No 4 INSET SESSION GUIDE TEMPLATE SCHOOL LEVELHiyasmine Altona GarciaNo ratings yet

- Pharmacology Quiz Question & Answers (Question Bank) - 3Document1 pagePharmacology Quiz Question & Answers (Question Bank) - 3Owusuasare ChrispakNo ratings yet

Download as pdf or txt

You might also like

- Case 6 - University Day Care CentreDocument3 pagesCase 6 - University Day Care CentreAnirudh Gulur100% (3)

- Kipp Houston Public Schools: Case Study 9Document16 pagesKipp Houston Public Schools: Case Study 9Hafiz DabeerNo ratings yet

- Piedmont University Group 4Document24 pagesPiedmont University Group 4Sangita Dhamdhere100% (4)

- D O No. 2, S. 2013-Revised Implementing Guidelines and Regulations of RA No. 8525 Otherwise Known As The Adopt-A-School Program ActDocument15 pagesD O No. 2, S. 2013-Revised Implementing Guidelines and Regulations of RA No. 8525 Otherwise Known As The Adopt-A-School Program ActAllan Jr Pancho0% (1)

- Establishing Fiscal Strength in Higher Education; Management Strategies for Transformative Revenue GenerationFrom EverandEstablishing Fiscal Strength in Higher Education; Management Strategies for Transformative Revenue GenerationNo ratings yet

- 1 Swings and Roundabouts: Margaret BrownDocument24 pages1 Swings and Roundabouts: Margaret BrownSridhar SathyaNo ratings yet

- Chapter 4-5 RemedialDocument19 pagesChapter 4-5 RemedialTata Duero Lachica100% (4)

- Fiscal State of The University Spring 2013Document20 pagesFiscal State of The University Spring 2013dailytitanNo ratings yet

- Paradise Community Collegefy2014budgetDocument11 pagesParadise Community Collegefy2014budgetapi-222496408No ratings yet

- 2011-12 Financial State of The District - FinalDocument19 pages2011-12 Financial State of The District - FinalBrendan WalshNo ratings yet

- Employee Health Clinic 2017 BOS Work Session 09.14.17Document25 pagesEmployee Health Clinic 2017 BOS Work Session 09.14.17Fauquier NowNo ratings yet

- North Syracuse Central School District: Proposed BudgetDocument30 pagesNorth Syracuse Central School District: Proposed BudgetTime Warner Cable NewsNo ratings yet

- Performance Based BudgetingDocument19 pagesPerformance Based BudgetingAmit ToshniwalNo ratings yet

- Superintendent's Recommendation WebsiteDocument21 pagesSuperintendent's Recommendation WebsitedaggerpressNo ratings yet

- Financial InformationDocument80 pagesFinancial InformationStarLink1No ratings yet

- Harrisburg School District FY2012-13 FC 10-14-13 - 1Document9 pagesHarrisburg School District FY2012-13 FC 10-14-13 - 1Emily PrevitiNo ratings yet

- DeKalb County Schools Fiscal Year 2014 Proposed Budget Executive SummaryDocument9 pagesDeKalb County Schools Fiscal Year 2014 Proposed Budget Executive SummaryThe Brookhaven PostNo ratings yet

- Benchmark - Budget DefenseDocument15 pagesBenchmark - Budget Defenseapi-623626988No ratings yet

- The University of Iowa General Education Fund FY 2019 BudgetDocument33 pagesThe University of Iowa General Education Fund FY 2019 BudgetHimanshu SethNo ratings yet

- James McKenna's 2013-14 Proposed Budget Presentation, March 14, 2013.Document33 pagesJames McKenna's 2013-14 Proposed Budget Presentation, March 14, 2013.Suffolk TimesNo ratings yet

- Importance of Annual BudgetDocument10 pagesImportance of Annual BudgetNwigwe Promise ChukwuebukaNo ratings yet

- GPPSS 2012-13 Financial State of The District - FINALDocument18 pagesGPPSS 2012-13 Financial State of The District - FINALBrendan WalshNo ratings yet

- 2013 Evaluation For UND President Robert KelleyDocument3 pages2013 Evaluation For UND President Robert KelleyRob PortNo ratings yet

- F1attach3 PDFDocument220 pagesF1attach3 PDFriskyplayerNo ratings yet

- Shenendehowa School District Budget PresentationDocument21 pagesShenendehowa School District Budget PresentationDavid LombardoNo ratings yet

- New Public Fiscal Admin Module 1 Lesson 1Document30 pagesNew Public Fiscal Admin Module 1 Lesson 1Jöhn LöydNo ratings yet

- Shanayes Budget Defense BenchmarkDocument15 pagesShanayes Budget Defense Benchmarkapi-529462240100% (1)

- 2012 2013ProposedBudgetVersion2 6Document136 pages2012 2013ProposedBudgetVersion2 6Robert WilonskyNo ratings yet

- Performance Audit Report: Tuition Waivers and Student StipendsDocument87 pagesPerformance Audit Report: Tuition Waivers and Student StipendsRob PortNo ratings yet

- Salem-Keizer Schools Budget Message 2011-12Document32 pagesSalem-Keizer Schools Budget Message 2011-12Statesman JournalNo ratings yet

- TEKEVDocument26 pagesTEKEVYosafat KurniawanNo ratings yet

- Ead 510 Benchmark Budget Defense Keisha ThompsonDocument18 pagesEad 510 Benchmark Budget Defense Keisha Thompsonapi-671417127100% (1)

- Annual Budget: A Presentation To The Board of Governors February 2013Document20 pagesAnnual Budget: A Presentation To The Board of Governors February 2013jeanyoperNo ratings yet

- The Cooper Union Working Group ReportDocument54 pagesThe Cooper Union Working Group ReportarchitectmagNo ratings yet

- Description: Tags: 06reportsuppDocument3 pagesDescription: Tags: 06reportsuppanon-783284No ratings yet

- FY14 Superintendents Proposed BudgetDocument170 pagesFY14 Superintendents Proposed BudgetFauquier NowNo ratings yet

- Appendix 6 2008Document4 pagesAppendix 6 2008Sadaf InamNo ratings yet

- 2010-11 Budget Draft #2 - Final - UnabridgedDocument38 pages2010-11 Budget Draft #2 - Final - UnabridgedBrendan WalshNo ratings yet

- Module 5 SummaryDocument3 pagesModule 5 SummaryJoan Jambalos TuertoNo ratings yet

- Montclair's 2021-22 Preliminary School BudgetDocument18 pagesMontclair's 2021-22 Preliminary School BudgetLouis C. HochmanNo ratings yet

- Budget2012 13 - v4 1Document669 pagesBudget2012 13 - v4 1tawnellNo ratings yet

- Mcvey Mary - Ead - 510 - Clincial Field Experience B - Schoolwide Budgetary NeedsDocument8 pagesMcvey Mary - Ead - 510 - Clincial Field Experience B - Schoolwide Budgetary Needsapi-529486237No ratings yet

- Analysis of The Financial Situation of Kutztown University, by Howard BunsisDocument54 pagesAnalysis of The Financial Situation of Kutztown University, by Howard BunsisRCPressNo ratings yet

- Review of Chignecto-Central Regional School Board 2012-13 BudgetDocument26 pagesReview of Chignecto-Central Regional School Board 2012-13 Budgetnick_logan9361No ratings yet

- U of L Final Exec Comp Report v1Document55 pagesU of L Final Exec Comp Report v1petersoe0No ratings yet

- Abhi Project 1Document85 pagesAbhi Project 1sanketkumarrathiNo ratings yet

- Salem-Keizer Public Schools 2012-13 Budget Message (Draft)Document23 pagesSalem-Keizer Public Schools 2012-13 Budget Message (Draft)Statesman JournalNo ratings yet

- BudgetdefenseDocument15 pagesBudgetdefenseapi-559694769No ratings yet

- Group Assignment-Money PlantDocument13 pagesGroup Assignment-Money PlantnitiyahsegarNo ratings yet

- 2012-13 Proposed Budget DocumentDocument397 pages2012-13 Proposed Budget DocumentStatesman JournalNo ratings yet

- 2010-11 GPPSS Staffing and Budgeting ProcessDocument15 pages2010-11 GPPSS Staffing and Budgeting ProcessBrendan WalshNo ratings yet

- 2012 FiscalPlanning MOEDocument45 pages2012 FiscalPlanning MOEParents' Coalition of Montgomery County, MarylandNo ratings yet

- Return On Investment in Education: A "System-Strategy" ApproachDocument14 pagesReturn On Investment in Education: A "System-Strategy" ApproachAfzal LodhiNo ratings yet

- Outlaw 14-15 BudgetDocument5 pagesOutlaw 14-15 Budgetapi-282985696No ratings yet

- PRMEDocument4 pagesPRMEkatykat101001No ratings yet

- Presentation 1Document28 pagesPresentation 1api-207421477No ratings yet

- 2024 - 0213 TST BOCES Budget PresentationDocument11 pages2024 - 0213 TST BOCES Budget PresentationShadeNo ratings yet

- School Board Work Session Jan 17 2012Document23 pagesSchool Board Work Session Jan 17 2012SaveWekivaElementaryNo ratings yet

- School Budget Planning Guide Rev Oct 13Document11 pagesSchool Budget Planning Guide Rev Oct 13violeta soriano100% (1)

- 002 Apfs 01Document116 pages002 Apfs 01Kevin Chrysler MarcoNo ratings yet

- Financial Strategy for Higher Education: A Field Guide for Presidents, C F Os, and Boards of TrusteesFrom EverandFinancial Strategy for Higher Education: A Field Guide for Presidents, C F Os, and Boards of TrusteesNo ratings yet

- Full Text Skripsi Irma HidayahDocument129 pagesFull Text Skripsi Irma HidayahCindi SartonoNo ratings yet

- Em Tech Quarter 2 LAS Week 56Document24 pagesEm Tech Quarter 2 LAS Week 56gabby ilaganNo ratings yet

- Ten SquareDocument53 pagesTen SquareYork Daily Record/Sunday NewsNo ratings yet

- SCSD News ReleaseDocument1 pageSCSD News ReleaseAmanda GonzalesNo ratings yet

- Revised Group 11 PresentationDocument40 pagesRevised Group 11 PresentationJanet Floreno VillasanaNo ratings yet

- Action Plan in Esp & SportsDocument13 pagesAction Plan in Esp & SportsMay-ann Ramos Galliguez ValdezNo ratings yet

- Results-Based Performance Management System (RPMS) For TeachersDocument6 pagesResults-Based Performance Management System (RPMS) For TeachersMelanie AplacaNo ratings yet

- Handbook of Eduaction Policy Research PDFDocument6 pagesHandbook of Eduaction Policy Research PDFIlham NurhidayatNo ratings yet

- Hiep, Nguyen Tat, Non English-Major Students' Attitudes Towards E-Learning, 2021Document16 pagesHiep, Nguyen Tat, Non English-Major Students' Attitudes Towards E-Learning, 2021HrvojeNo ratings yet

- Borgo Free Jazz in The ClassroomDocument29 pagesBorgo Free Jazz in The ClassroomJohn PetrucelliNo ratings yet

- Innateness Theory PresentationDocument9 pagesInnateness Theory PresentationMarisol LealNo ratings yet

- Cebu Technological University: Republic of The PhilippinesDocument1 pageCebu Technological University: Republic of The PhilippinesCleo TokongNo ratings yet

- ManiDocument5 pagesManiOn Point management serviceNo ratings yet

- Syllabus Math1215 s22Document6 pagesSyllabus Math1215 s22Jordane WayNo ratings yet

- Dissertation Proposal University of LeedsDocument7 pagesDissertation Proposal University of LeedsPaperWritingServicesBestSingapore100% (1)

- MMO Sample Papers For Class 1Document19 pagesMMO Sample Papers For Class 1Linh DiệpNo ratings yet

- Catch Up Friday Feb 2Document7 pagesCatch Up Friday Feb 2Mark Laurenze Manga100% (2)

- Workplace Skills Assignment 2023Document6 pagesWorkplace Skills Assignment 2023c2qbrxcwqqNo ratings yet

- Homeroom PTA AgendaDocument5 pagesHomeroom PTA AgendaALPHA RACHEL TULINGNo ratings yet

- Course Syllabus - Food Service SystemDocument10 pagesCourse Syllabus - Food Service SystemDerick MacedaNo ratings yet

- History 4C - Paper #1: Pere GoriotDocument2 pagesHistory 4C - Paper #1: Pere GoriotSteven MackeyNo ratings yet

- Term 1 Week 6 Ey MinutesDocument2 pagesTerm 1 Week 6 Ey Minutesapi-459118418No ratings yet

- Sdact0m - 01 - Mark077 MarkedDocument6 pagesSdact0m - 01 - Mark077 MarkedEdmoreMucheka100% (1)

- Ielts Answer SheetDocument2 pagesIelts Answer SheetTharra JungNo ratings yet

- RPP BHS Inggris MilaDocument2 pagesRPP BHS Inggris MilaBio17 ArifNo ratings yet

- Omnibus Sworn CertificationDocument3 pagesOmnibus Sworn CertificationMarck Vyn LopezNo ratings yet

- Enclosure No 4 INSET SESSION GUIDE TEMPLATE SCHOOL LEVELDocument2 pagesEnclosure No 4 INSET SESSION GUIDE TEMPLATE SCHOOL LEVELHiyasmine Altona GarciaNo ratings yet

- Pharmacology Quiz Question & Answers (Question Bank) - 3Document1 pagePharmacology Quiz Question & Answers (Question Bank) - 3Owusuasare ChrispakNo ratings yet