Download as doc, pdf, or txt

You might also like

- Case 03 - The Lazy Mower - SolutionDocument7 pagesCase 03 - The Lazy Mower - SolutionDũngPham67% (3)

- Financial Plan TemplateDocument23 pagesFinancial Plan TemplateKosong ZerozirizarazoroNo ratings yet

- Software DISC TestDocument8 pagesSoftware DISC TestIsnin Nadjama Fitri0% (1)

- 11 - Substantive Tests of Property, Plant and EquipmentDocument27 pages11 - Substantive Tests of Property, Plant and EquipmentArleneCastroNo ratings yet

- CXC Principles of Accounts Past Papers May 2012Document9 pagesCXC Principles of Accounts Past Papers May 2012ArcherAcs86% (7)

- Tcode Favorites Sap AaDocument10 pagesTcode Favorites Sap AaKrali MarkoNo ratings yet

- Acc 501 Midterm Solved Papers Long Questions SolvedDocument34 pagesAcc 501 Midterm Solved Papers Long Questions SolvedAbbas Jafri33% (3)

- Gonzaga - Sec1 - Exercises On QaipDocument3 pagesGonzaga - Sec1 - Exercises On QaipSteph Gonzaga100% (1)

- Development of The Institutional Structure of Financial AccountingDocument5 pagesDevelopment of The Institutional Structure of Financial Accountingtiyas100% (1)

- Materials Management 4.6 Exercises MM355 - Day 2 Invoice VerificationDocument10 pagesMaterials Management 4.6 Exercises MM355 - Day 2 Invoice VerificationarunvasamNo ratings yet

- BP LOSC Valuated Vendor ConsignmentDocument18 pagesBP LOSC Valuated Vendor ConsignmentdatbolNo ratings yet

- Solution Financial Reporting May 2013 Solution 1Document10 pagesSolution Financial Reporting May 2013 Solution 1John Bates BlanksonNo ratings yet

- Practicalweek48 0809answersDocument8 pagesPracticalweek48 0809answersLaura BasalicNo ratings yet

- Accounting For Merchandising BusinessesDocument106 pagesAccounting For Merchandising BusinessesKel TranNo ratings yet

- Contents:: Introduction To Invoice VerificationDocument13 pagesContents:: Introduction To Invoice VerificationpravanthbabuNo ratings yet

- Guidance Manual FinalDocument27 pagesGuidance Manual FinalrosdobNo ratings yet

- The Cpa Licensure Examination Syllabus Management ServicesDocument8 pagesThe Cpa Licensure Examination Syllabus Management ServicesCaraigMichaelNo ratings yet

- Chapter 2 Analysis of Solvency, Liquidity, and Financial FlexibilityDocument19 pagesChapter 2 Analysis of Solvency, Liquidity, and Financial FlexibilityYusuf Abdurrachman100% (1)

- Chapter 16Document17 pagesChapter 16Kad SaadNo ratings yet

- Completing Acctg Cycle Four Exercises 06mar21Document12 pagesCompleting Acctg Cycle Four Exercises 06mar21Jasmine ActaNo ratings yet

- O o o o o O: Amortisation, Acquisition, Restructure Charges, In-Process R&D, Pension CurtailmentDocument18 pagesO o o o o O: Amortisation, Acquisition, Restructure Charges, In-Process R&D, Pension CurtailmentmkNo ratings yet

- MBA Strategic Finance AssignmentDocument14 pagesMBA Strategic Finance AssignmentStephanie StephensNo ratings yet

- Assets Liabilities & Shareholders' Equity: Solutions To Chapter 3 Accounting and FinanceDocument12 pagesAssets Liabilities & Shareholders' Equity: Solutions To Chapter 3 Accounting and FinanceTea WonNo ratings yet

- Revision Pack 2009-10Document9 pagesRevision Pack 2009-10Tosin YusufNo ratings yet

- Chart of AccountsDocument17 pagesChart of AccountsRocky Cadiz100% (1)

- Chapter 07, 08, 09 Non Current AssetsDocument8 pagesChapter 07, 08, 09 Non Current Assetsali_sattar15No ratings yet

- R - F-51 - Internal Transfer Posting With ClearingDocument8 pagesR - F-51 - Internal Transfer Posting With Clearingmadhub_17No ratings yet

- Spoilage and BreakageDocument2 pagesSpoilage and Breakagedamianuskrowin0% (1)

- f8 TocDocument41 pagesf8 TocANASNo ratings yet

- Chapter 3 Suggested Solutions: Input Output + - + - + ProcessDocument11 pagesChapter 3 Suggested Solutions: Input Output + - + - + Processapi-3824657No ratings yet

- Legal Change Service AbatementDocument16 pagesLegal Change Service Abatementraj01072007No ratings yet

- Gen Ledger AccountsDocument15 pagesGen Ledger AccountsMoises CalastravoNo ratings yet

- 126 Resource MAFA May 1996 May 2001Document267 pages126 Resource MAFA May 1996 May 2001Erwin Labayog MedinaNo ratings yet

- Customer Invoicing2Document14 pagesCustomer Invoicing2Octavian GenunchiNo ratings yet

- Financial Statements, Taxes, and Cash Flow: Chapter Web SitesDocument5 pagesFinancial Statements, Taxes, and Cash Flow: Chapter Web SitesTonyWalterNo ratings yet

- Class Exercise: Cash Flow StatementDocument2 pagesClass Exercise: Cash Flow StatementshaunaryaNo ratings yet

- Total Assets 524,600 ? ? 220,111Document2 pagesTotal Assets 524,600 ? ? 220,111Saranya VillaNo ratings yet

- Ch24 Full Disclosure in Financial ReportingDocument31 pagesCh24 Full Disclosure in Financial ReportingAries BautistaNo ratings yet

- Curriculum Vitae: Personal ProfileDocument9 pagesCurriculum Vitae: Personal ProfilerahulhaldankarNo ratings yet

- Chapter 10 Quiz 1: 100% (22 Out of 22 Correct)Document10 pagesChapter 10 Quiz 1: 100% (22 Out of 22 Correct)im_donnavierojoNo ratings yet

- EduInsight - Accounting 2014 Support Seminar Answer PaperDocument18 pagesEduInsight - Accounting 2014 Support Seminar Answer PaperSanduni WijewardaneNo ratings yet

- Attempt All Questions Part One-Short Answer Questions (Chapters 1,3,6,8,11,12,18)Document6 pagesAttempt All Questions Part One-Short Answer Questions (Chapters 1,3,6,8,11,12,18)nirmaldevalNo ratings yet

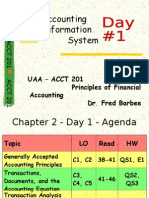

- Accounting Information System: Uaa - Acct 201 Principles of Financial Accounting Dr. Fred BarbeeDocument55 pagesAccounting Information System: Uaa - Acct 201 Principles of Financial Accounting Dr. Fred BarbeeyenzelNo ratings yet

- Ajara Urban Co-Op Bank LTD., Ajara Dist - Kolhapur: N.M. Joshi MargDocument32 pagesAjara Urban Co-Op Bank LTD., Ajara Dist - Kolhapur: N.M. Joshi Margpramesh1010No ratings yet

- Management Accounting - CentumDocument100 pagesManagement Accounting - CentumShyam SundarNo ratings yet

- Time Interest Earned RatioDocument40 pagesTime Interest Earned RatioFarihaFardeenNo ratings yet

- A2 Book Without Space For June 2021Document259 pagesA2 Book Without Space For June 2021Abdul MoizNo ratings yet

- Chap 003Document11 pagesChap 003Sercan DemirNo ratings yet

- Solutions Guide: Please Reword The Answers To Essay Type Parts So As To Guarantee That Your Answer Is An Original. Do Not Submit As Your OwnDocument9 pagesSolutions Guide: Please Reword The Answers To Essay Type Parts So As To Guarantee That Your Answer Is An Original. Do Not Submit As Your Ownkswb12No ratings yet

- Week 4 Balance OffDocument16 pagesWeek 4 Balance OffNor LailyNo ratings yet

- Solution To Case 01: Growing PainsDocument7 pagesSolution To Case 01: Growing PainsBel LOENo ratings yet

- Impact of Audit Evidence On Auditor'S Report PDFDocument9 pagesImpact of Audit Evidence On Auditor'S Report PDFAlexander Decker100% (1)

- Ch13 RevAnsDocument16 pagesCh13 RevAnssamuel_dwumfourNo ratings yet

- Job Description AccountsDocument16 pagesJob Description AccountsnayanghimireNo ratings yet

- Cuyahoga County Issue 7: What Is The Sin TaxDocument8 pagesCuyahoga County Issue 7: What Is The Sin TaxBrian CumminsNo ratings yet

- Ryan International SchoolDocument1 pageRyan International SchoolSidhantNo ratings yet

- Accounting for Real Estate Transactions: A Guide For Public Accountants and Corporate Financial ProfessionalsFrom EverandAccounting for Real Estate Transactions: A Guide For Public Accountants and Corporate Financial ProfessionalsNo ratings yet

- Life-Cycle Costing: Using Activity-Based Costing and Monte Carlo Methods to Manage Future Costs and RisksFrom EverandLife-Cycle Costing: Using Activity-Based Costing and Monte Carlo Methods to Manage Future Costs and RisksNo ratings yet

- Water Well Drilling Contractors World Summary: Market Values & Financials by CountryFrom EverandWater Well Drilling Contractors World Summary: Market Values & Financials by CountryNo ratings yet

- Operational Profitability: Systematic Approaches for Continuous ImprovementFrom EverandOperational Profitability: Systematic Approaches for Continuous ImprovementNo ratings yet

- Water, Sewer & Pipeline Construction World Summary: Market Values & Financials by CountryFrom EverandWater, Sewer & Pipeline Construction World Summary: Market Values & Financials by CountryNo ratings yet

- Peningkatan Return Saham Dan Kinerja Keuangan Melalui: Corporate Social Responsibility Dan Good Corporate GovernanceDocument10 pagesPeningkatan Return Saham Dan Kinerja Keuangan Melalui: Corporate Social Responsibility Dan Good Corporate GovernanceIsnin Nadjama FitriNo ratings yet

- Slide Chapter 4Document29 pagesSlide Chapter 4Isnin Nadjama FitriNo ratings yet

- Tugass Prak MikrobiologiDocument4 pagesTugass Prak MikrobiologiIsnin Nadjama FitriNo ratings yet

- 4 CH 05 The Cultural EnvironmentDocument35 pages4 CH 05 The Cultural EnvironmentIsnin Nadjama FitriNo ratings yet

- Opini Pendapat Tidak Wajar (Adverse Opinion)Document3 pagesOpini Pendapat Tidak Wajar (Adverse Opinion)Isnin Nadjama FitriNo ratings yet

- Opini Pendapat Tidak Wajar (Adverse Opinion)Document3 pagesOpini Pendapat Tidak Wajar (Adverse Opinion)Isnin Nadjama FitriNo ratings yet

- Leadership Development Program (LDP)Document4 pagesLeadership Development Program (LDP)Ha Huy CuongNo ratings yet

- ACCA AAA (P7) Notes by Sir Owais MirchawalaDocument25 pagesACCA AAA (P7) Notes by Sir Owais MirchawalaMirchawala's100% (2)

- Finec 2Document11 pagesFinec 2nurulnatasha sinclairaquariusNo ratings yet

- COSO GuidanceDocument71 pagesCOSO GuidancemahmudtohaNo ratings yet

- Curriculum Vitae of Abu Naser-1Document3 pagesCurriculum Vitae of Abu Naser-1Naser SumonNo ratings yet

- Book-Keeping: Jayant Sethia C.A.FinalistDocument29 pagesBook-Keeping: Jayant Sethia C.A.FinalistShreekumar100% (1)

- 01 Forensic AuditingDocument30 pages01 Forensic AuditingSRIVISHNU BNo ratings yet

- Cortez, Danica M. - IUEEU AssignmentDocument2 pagesCortez, Danica M. - IUEEU AssignmentDanica CortezNo ratings yet

- Assignment 4Document5 pagesAssignment 4Syeda ToobaNo ratings yet

- Kanix Brochure PDFDocument8 pagesKanix Brochure PDFRajkumar RENo ratings yet

- The Development of Public Sector Accounting and Financial Reporting in Sri LankaDocument20 pagesThe Development of Public Sector Accounting and Financial Reporting in Sri LankaPrabowo HadiNo ratings yet

- HRM 3Document14 pagesHRM 3Engr Nargis HussainNo ratings yet

- All Subj - Board Exam-Picpa EeDocument9 pagesAll Subj - Board Exam-Picpa EeMJ YaconNo ratings yet

- 5000Document54 pages5000kunjapNo ratings yet

- Equity Funding Corporation of AmericaDocument19 pagesEquity Funding Corporation of AmericaCharles100% (1)

- Toshiba - Accounting Fraud - Teaching NoteDocument11 pagesToshiba - Accounting Fraud - Teaching NoteMariam AlraeesiNo ratings yet

- PT Barito Pacific TBK - Final Des 2021Document193 pagesPT Barito Pacific TBK - Final Des 2021Haris MaulanaNo ratings yet

- Doubtful AccountsDocument2 pagesDoubtful AccountsCharles Reginald K. HwangNo ratings yet

- External Users of AccountingDocument3 pagesExternal Users of AccountingMarko Zero Four0% (1)

- Acconts Preliminary Paper 2Document13 pagesAcconts Preliminary Paper 2AMIN BUHARI ABDUL KHADERNo ratings yet

- Abul Hasan Miah: Career ObjectiveDocument5 pagesAbul Hasan Miah: Career ObjectiveAbul Hasan MiahNo ratings yet

- 251 Internal Audit OfficerDocument2 pages251 Internal Audit OfficerYang PhearaNo ratings yet

- Guidance Note On Bank Audit 2023 16.03.2023 PDFDocument812 pagesGuidance Note On Bank Audit 2023 16.03.2023 PDFSrini100% (1)

- Audit Plan Example 9K 14K 45KDocument2 pagesAudit Plan Example 9K 14K 45KDatuakNo ratings yet

- Social AuditDocument9 pagesSocial Auditananthi RNo ratings yet

- Chapter 3 Auditing Payroll and Personnel Cycle-1Document6 pagesChapter 3 Auditing Payroll and Personnel Cycle-1HABTAMU TULUNo ratings yet

- MEGHNATH REGMI CV AccountantDocument5 pagesMEGHNATH REGMI CV AccountantPrakash RegmiNo ratings yet

- Audit 12 - Rizq Aly AfifDocument2 pagesAudit 12 - Rizq Aly AfifRizq Aly AfifNo ratings yet