Download as docx, pdf, or txt

You might also like

- Mont Gras CaseDocument10 pagesMont Gras CaseFernando HealyNo ratings yet

- Case 2 - Global Wine WarDocument2 pagesCase 2 - Global Wine Warneha nairNo ratings yet

- Assignment #3 - MRP Calculation: Part A 1 2 3 4 5 6Document2 pagesAssignment #3 - MRP Calculation: Part A 1 2 3 4 5 6jigar kanjani0% (1)

- Case 2-The Beer IndustryDocument13 pagesCase 2-The Beer IndustrypatiseNo ratings yet

- MCDonald's Multi-Domestic StrategyDocument23 pagesMCDonald's Multi-Domestic StrategyHảii Ngọcc50% (2)

- ITC Sales and DistributionDocument16 pagesITC Sales and Distributionmohit rajput100% (1)

- Denmark Wine Landscapes: Wine Intelligence Wine IntelligenceDocument8 pagesDenmark Wine Landscapes: Wine Intelligence Wine IntelligenceСтефани ЛазароваNo ratings yet

- Viden Io Delamere Vineyard Strategy Group 02 Delamere VineyardDocument19 pagesViden Io Delamere Vineyard Strategy Group 02 Delamere VineyardtanNo ratings yet

- BUS 400 Mondavi Case FinalDocument6 pagesBUS 400 Mondavi Case Finalfamewang0% (1)

- SCM G01 - A01 Chalice WinesDocument11 pagesSCM G01 - A01 Chalice WinesPankaj GoyalNo ratings yet

- Chalice WinesDocument42 pagesChalice Winesdk.asal6361No ratings yet

- Case 19 NotesDocument5 pagesCase 19 NotesFLODOHANo ratings yet

- Kodak Funtime MarginsDocument1 pageKodak Funtime Marginsan052091No ratings yet

- Porter's Five ForcesDocument9 pagesPorter's Five Forcesmark alcantaraNo ratings yet

- Global Wine War 2009 New World Versus Old Case Analysis - 1Document5 pagesGlobal Wine War 2009 New World Versus Old Case Analysis - 1feridun01100% (3)

- Global Final - Wine WarsDocument4 pagesGlobal Final - Wine Warsjen18612No ratings yet

- Global Wine War 2009 FixDocument39 pagesGlobal Wine War 2009 FixImam Mashari100% (8)

- The Global Alcohol Industry: Daniel O'Leary - 1469525Document16 pagesThe Global Alcohol Industry: Daniel O'Leary - 1469525doleary1109No ratings yet

- Assessment 1 Evaluate International Marketing Opportunities: Bonatelli Wines Pty LTDDocument10 pagesAssessment 1 Evaluate International Marketing Opportunities: Bonatelli Wines Pty LTDMark Allen ChavezNo ratings yet

- Wine Industry Market PlanDocument14 pagesWine Industry Market PlanWashif AnwarNo ratings yet

- Group 10 Section 3: Case Summary The Australian Wine IndustryDocument19 pagesGroup 10 Section 3: Case Summary The Australian Wine IndustryNick JNo ratings yet

- Florida International University Professional MBA Downtown Program - Spring 2018 - Cohort 14Document23 pagesFlorida International University Professional MBA Downtown Program - Spring 2018 - Cohort 14Michelle LindsayNo ratings yet

- Identifying The Main Challenges and Opportunities Facing The Wine IndustryDocument3 pagesIdentifying The Main Challenges and Opportunities Facing The Wine IndustryFaculty of the ProfessionsNo ratings yet

- TR 08 08 Whatshotaroundtheglobe-BeveragesDocument25 pagesTR 08 08 Whatshotaroundtheglobe-Beveragesapi-248965729No ratings yet

- FAO Agbiz Handbook Grapes 0Document39 pagesFAO Agbiz Handbook Grapes 0furtunattaNo ratings yet

- Top 50 Wine Brands 2011Document14 pagesTop 50 Wine Brands 2011Luiz ColaNo ratings yet

- Chile and The Chilean Wine IndustryDocument39 pagesChile and The Chilean Wine IndustryRiad-us SalehinNo ratings yet

- Alcohol Marketing Paper Sept 30Document20 pagesAlcohol Marketing Paper Sept 30puja157No ratings yet

- Harvard Business School CaseDocument51 pagesHarvard Business School Casemuhammad fadliNo ratings yet

- Canadian Wine IndustryDocument21 pagesCanadian Wine IndustryconnectindiaNo ratings yet

- CLV Calculation With No Changes To Brand Strategy: NPV of Expected Cash Flow From Customer (CLV) $378.49Document4 pagesCLV Calculation With No Changes To Brand Strategy: NPV of Expected Cash Flow From Customer (CLV) $378.49killerboyeNo ratings yet

- High End WineDocument24 pagesHigh End WinelakhanNo ratings yet

- The Changing Nature of Fine Wine BuyingDocument23 pagesThe Changing Nature of Fine Wine Buyingfcs uhhgfNo ratings yet

- Chataux Margaux Business CaseDocument37 pagesChataux Margaux Business Caserohit goswamiNo ratings yet

- Ricasoli Case StudyDocument21 pagesRicasoli Case StudyRodianneNo ratings yet

- Alcohol Promotion and The Marketing Industry Trends, Tactics, and Public HealthDocument21 pagesAlcohol Promotion and The Marketing Industry Trends, Tactics, and Public HealthDipanjan DasNo ratings yet

- Consumer Behaviour and Sensory Preference Differences: Implications For Wine Product MarketingDocument14 pagesConsumer Behaviour and Sensory Preference Differences: Implications For Wine Product MarketingsagittareNo ratings yet

- Analyst ViewDocument9 pagesAnalyst ViewSreejit NairNo ratings yet

- Natureview Farm - ExcelDocument35 pagesNatureview Farm - ExcelGaurav Suresh YadavNo ratings yet

- Etaly Vancouver Business Plan V3Document28 pagesEtaly Vancouver Business Plan V3Gurinder ParmarNo ratings yet

- Wine Industry Report April2011Document26 pagesWine Industry Report April2011dragandragoonNo ratings yet

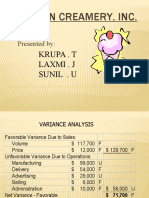

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Nike AnalysisDocument27 pagesNike Analysisriz4winNo ratings yet

- Macroeconomic Analysis Wine IndustryDocument8 pagesMacroeconomic Analysis Wine IndustryAntony Varghese Palamuttam100% (1)

- Blue Ocean Strategy in The Wine IndustryDocument25 pagesBlue Ocean Strategy in The Wine IndustryTMRW EngineNo ratings yet

- KFC JapanDocument10 pagesKFC JapanAnonymous 5GHZXlNo ratings yet

- ZomatoDocument56 pagesZomatopreethishNo ratings yet

- C1214 Wine Production in Australia Industry ReportDocument60 pagesC1214 Wine Production in Australia Industry ReportAndrea CayetanoNo ratings yet

- Midwest Office Products - AHMDocument4 pagesMidwest Office Products - AHMMSINS SDEDNo ratings yet

- Practice Questions 2012-13Document2 pagesPractice Questions 2012-13anant_jain88114No ratings yet

- VarianceDocument3 pagesVarianceWan Noor AsmuniNo ratings yet

- MondaviDocument3 pagesMondaviritu_wadhwa0079769No ratings yet

- Robert Mondavi & The Wine IndustryDocument6 pagesRobert Mondavi & The Wine Industryআবদুল্লাহ আল মাহমুদ100% (2)

- Robert Mondavi & Wine IndustryDocument10 pagesRobert Mondavi & Wine Industrypaco_burg100% (1)

- Group Activity: Competitive Analysis and Opportunities in The Marketplace of CoconutDocument3 pagesGroup Activity: Competitive Analysis and Opportunities in The Marketplace of CoconutVance UrsulumNo ratings yet

- Mi Ill BrookDocument19 pagesMi Ill Brookbdosch99No ratings yet

- 1Document6 pages1khansiNo ratings yet

- Case SM1 Updated v1Document15 pagesCase SM1 Updated v1Divya ChaudharyNo ratings yet

- To The CustomersDocument31 pagesTo The CustomersSaranyaelangovan MargaretNo ratings yet

- Porter 5Document4 pagesPorter 5'Sånjîdå KåBîr'No ratings yet

- Boston Beer PresentationDocument9 pagesBoston Beer PresentationShahriar RawshonNo ratings yet

- Report Description: Chapter 1 IntroductionDocument28 pagesReport Description: Chapter 1 Introductionsidhujassi91No ratings yet

- Wine Research Paper TopicsDocument6 pagesWine Research Paper Topicslqinlccnd100% (3)

- Week 4 & 5 DDG (Designing Channel Networks)Document32 pagesWeek 4 & 5 DDG (Designing Channel Networks)Aqib LatifNo ratings yet

- Ifad Group AssignmentDocument8 pagesIfad Group AssignmentIsmail DxNo ratings yet

- Internatinal MKT Worksheet (1) 4Document9 pagesInternatinal MKT Worksheet (1) 4dagnawNo ratings yet

- E Business Assignment 2Document7 pagesE Business Assignment 2Shikha MishraNo ratings yet

- Unit 5 DIGITALMARKETING AND E COMMERCEDocument16 pagesUnit 5 DIGITALMARKETING AND E COMMERCESUFIYAN KHANNo ratings yet

- Definition and Scope of RetailingDocument12 pagesDefinition and Scope of RetailingRamesh PalNo ratings yet

- JharkhandDocument57 pagesJharkhandDigitalsolar NoidaNo ratings yet

- Analisis Dampak Perkembangan Revolusi Industri 4.0 Dan Society 5.0 Pada Perilaku Masyarakat Ekonomi (E-Commerce)Document7 pagesAnalisis Dampak Perkembangan Revolusi Industri 4.0 Dan Society 5.0 Pada Perilaku Masyarakat Ekonomi (E-Commerce)Rangga ReboxNo ratings yet

- Final RequirementDocument2 pagesFinal RequirementHi Alkaid MagdadaroNo ratings yet

- Case Study SMDocument100 pagesCase Study SMMeet DalalNo ratings yet

- Travel Agency and Tour Operations Business (PDFDrive)Document102 pagesTravel Agency and Tour Operations Business (PDFDrive)Sachin Thakur100% (1)

- SCMchapter 4Document39 pagesSCMchapter 4KgnasNo ratings yet

- Wonder Cake ProjectDocument14 pagesWonder Cake ProjectKing Krish50% (2)

- SDRM FinalDocument26 pagesSDRM Finalsiddhant hingoraniNo ratings yet

- 872 Idbi StatementDocument17 pages872 Idbi StatementDavesh JadonNo ratings yet

- Basics of Supply Chain Management Business ConceptsDocument7 pagesBasics of Supply Chain Management Business ConceptsrsdeshmukhNo ratings yet

- Introduction To Retail ManagementDocument30 pagesIntroduction To Retail Managementakriti bawaNo ratings yet

- Angelito Alvarez Sales Account Executive LagunaDocument5 pagesAngelito Alvarez Sales Account Executive LagunaRonie CerinoNo ratings yet

- Chapyer 3Document10 pagesChapyer 3Taif AlbassriNo ratings yet

- Report On Colgate Max Fresh: Global Brand Roll-OutDocument20 pagesReport On Colgate Max Fresh: Global Brand Roll-OuttrijtkaNo ratings yet

- 1 Retail Turnaround VFDocument8 pages1 Retail Turnaround VFTakudzwa S MupfurutsaNo ratings yet

- FDNMARK - Notes For Quiz 2Document8 pagesFDNMARK - Notes For Quiz 2Ma. Kelly Cassandra RiveraNo ratings yet

- Part I Chapter 1 Marketing Channel NOTESDocument25 pagesPart I Chapter 1 Marketing Channel NOTESEriberto100% (1)

- Bank Data InstallationDocument91 pagesBank Data InstallationManoj bhostekarNo ratings yet

- Distribution Channel and Promotional ToolsDocument7 pagesDistribution Channel and Promotional ToolsMonique MalateNo ratings yet

- BigCommerce Build An Ecommerce WebsiteDocument21 pagesBigCommerce Build An Ecommerce Websitedevartli09No ratings yet

- Marketing GraduationDocument52 pagesMarketing GraduationManik GargNo ratings yet