Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Blackbook Project On Consumer Perception About Life Insurance PoliciesDocument80 pagesBlackbook Project On Consumer Perception About Life Insurance PoliciesMohit Kumar89% (28)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Ch12 Harrison 8e GE SMDocument87 pagesCh12 Harrison 8e GE SMMuh BilalNo ratings yet

- Free Trip To Islay - June 1975Document20 pagesFree Trip To Islay - June 1975Kintyre On RecordNo ratings yet

- Worshop Banking and Money VocabularyDocument3 pagesWorshop Banking and Money VocabularyJuan C. LópezNo ratings yet

- Uk PayslipDocument2 pagesUk PayslipraoNo ratings yet

- Sec One 950123 05 2539Document161 pagesSec One 950123 05 2539Minh VănNo ratings yet

- Tutorial Questions Weesadk 5. - Risk UncertainDocument3 pagesTutorial Questions Weesadk 5. - Risk UncertainMinh VănNo ratings yet

- Role of Foraaaaaeign Banks in Emerging Markets BodyDocument40 pagesRole of Foraaaaaeign Banks in Emerging Markets BodyMinh VănNo ratings yet

- Peak-Load Pricing: Charging More When Its Costs More To ProduceDocument7 pagesPeak-Load Pricing: Charging More When Its Costs More To ProduceMinh Văn100% (1)

- Bank Efficiency and Non-Performing Loans: Evidence From Malaysia and SingaporeDocument15 pagesBank Efficiency and Non-Performing Loans: Evidence From Malaysia and SingaporeMinh VănNo ratings yet

- Classens, K. and Van Horen, N. (2012) Foreign Banks: Trends, Impact and Financial Stability', IMF Working Paper, International Monetary FundDocument4 pagesClassens, K. and Van Horen, N. (2012) Foreign Banks: Trends, Impact and Financial Stability', IMF Working Paper, International Monetary FundMinh VănNo ratings yet

- File LoadaDocument1 pageFile LoadaMinh VănNo ratings yet

- Concerts 19jan2012 v2Document28 pagesConcerts 19jan2012 v2Minh VănNo ratings yet

- ECF3120 Class Handout - Lecture 1 Soderlind, Steven Dale, Consumer Economics: A Practical Overview, CH 1&2Document35 pagesECF3120 Class Handout - Lecture 1 Soderlind, Steven Dale, Consumer Economics: A Practical Overview, CH 1&2Minh VănNo ratings yet

- Eo Ar 2008Document184 pagesEo Ar 2008Saleh HashimNo ratings yet

- Consolidation Following Acquisition: Irwin/Mcgraw-HillDocument26 pagesConsolidation Following Acquisition: Irwin/Mcgraw-HillAmir ImraniNo ratings yet

- Innovative Climate and Disaster Risk Finance Solutions Resilience Building and Fiscal StrengtheningDocument26 pagesInnovative Climate and Disaster Risk Finance Solutions Resilience Building and Fiscal StrengtheningcarlosNo ratings yet

- Course Outline-Tax ReviewDocument27 pagesCourse Outline-Tax ReviewMaanNo ratings yet

- Appraisal RightDocument166 pagesAppraisal RightMike E DmNo ratings yet

- Annual Report 2019 2020Document208 pagesAnnual Report 2019 2020bhalaNo ratings yet

- TECHNOWA Invoice 170 - 24.05.2023Document1 pageTECHNOWA Invoice 170 - 24.05.2023Mathewraj Dhanasekaran palanivelNo ratings yet

- Luna v. EncarnacionDocument5 pagesLuna v. EncarnacionEmma Ruby Aguilar-ApradoNo ratings yet

- The Board of Directors or TrusteesDocument5 pagesThe Board of Directors or TrusteesKaty OlidanNo ratings yet

- SBI Life InsuranceDocument38 pagesSBI Life InsuranceParth Bhatt50% (2)

- PDF San Beda College of Law MEMORY AID I PDFDocument106 pagesPDF San Beda College of Law MEMORY AID I PDFGladys ManaliliNo ratings yet

- Project Report ON: "A Study of Agricultural Loan Pro-Vided by Regional Rural Banks (RRBS) in Jharkhand''Document33 pagesProject Report ON: "A Study of Agricultural Loan Pro-Vided by Regional Rural Banks (RRBS) in Jharkhand''Aashik AnsariNo ratings yet

- BAS Vs BSSDocument2 pagesBAS Vs BSSGunjan ShahNo ratings yet

- Chapter 19Document5 pagesChapter 19Tabib HabibNo ratings yet

- FIN 438 - Chapter 15 QuestionsDocument6 pagesFIN 438 - Chapter 15 QuestionsTrần Dương Mai PhươngNo ratings yet

- A Study On Cash Flow Analysis at BEML Limited., KGFDocument61 pagesA Study On Cash Flow Analysis at BEML Limited., KGF28196.rakesh.mba22No ratings yet

- Financial Accounting 4th Edition Spiceland Test Bank 1Document187 pagesFinancial Accounting 4th Edition Spiceland Test Bank 1barbara100% (53)

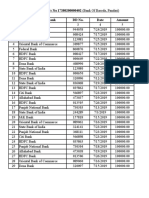

- S.No Name of The Bank DD No. Date AmountDocument14 pagesS.No Name of The Bank DD No. Date Amountsc BhagatNo ratings yet

- Opm Pmac ExampleDocument21 pagesOpm Pmac Exampleענת מדמוני100% (1)

- Your Holiday ConfirmationDocument1 pageYour Holiday Confirmationmaureen.ruane1No ratings yet

- LPMPC Policies and Guidelines 2021Document26 pagesLPMPC Policies and Guidelines 2021Jugger Afrondoza100% (1)

- Performance Highlights: NeutralDocument11 pagesPerformance Highlights: NeutralAngel BrokingNo ratings yet

- Module 13 - (Assignment) Finance and Managing CostsDocument3 pagesModule 13 - (Assignment) Finance and Managing Costsnfarah618No ratings yet

- P7int 2010 Jun ADocument17 pagesP7int 2010 Jun AFzr JamNo ratings yet

- Batch 2 CasesDocument55 pagesBatch 2 CasesCar L MinaNo ratings yet