Romania February 2011

Romania February 2011

You might also like

- France PestleDocument39 pagesFrance PestleAlee LowNo ratings yet

- Example SRL - H1 2012Document9 pagesExample SRL - H1 2012tomideuNo ratings yet

- Egypt EconomicDocument3 pagesEgypt EconomicakshittayalNo ratings yet

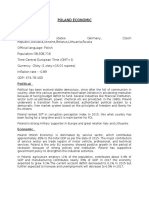

- Poland Economic: PoliticalDocument3 pagesPoland Economic: PoliticaljjnjwdcjNo ratings yet

- 12 For 2012: Why Poland Will Avoid Recession Even If Whole EU Does NotDocument3 pages12 For 2012: Why Poland Will Avoid Recession Even If Whole EU Does NotPeter RheeNo ratings yet

- The Republic of Moldova in The Eastern Partnership: From Poster Child To Problem Child ?Document10 pagesThe Republic of Moldova in The Eastern Partnership: From Poster Child To Problem Child ?Viorica RussuNo ratings yet

- Studii Economice - CofaceDocument2 pagesStudii Economice - CofaceVelicanu Bekk ZsuzsaNo ratings yet

- SEB Report: Italian Elections Likely To Secure Continuation of ReformsDocument3 pagesSEB Report: Italian Elections Likely To Secure Continuation of ReformsSEB GroupNo ratings yet

- Analysis of Netherland EconomyDocument30 pagesAnalysis of Netherland EconomymohitNo ratings yet

- BTI 2014 Laos Country ReportDocument28 pagesBTI 2014 Laos Country ReportPhilip BravoNo ratings yet

- Dambovita Sum Up Research - GrecuDocument8 pagesDambovita Sum Up Research - GrecuCristina CristeaNo ratings yet

- BelgiumDocument2 pagesBelgiumHa VoNo ratings yet

- Slovakia: In-Depth PEST InsightsDocument38 pagesSlovakia: In-Depth PEST Insightskarthik_srinivasa_14No ratings yet

- February 2011 Monetary Policy Statement Lastdoc 2Document36 pagesFebruary 2011 Monetary Policy Statement Lastdoc 2Théotime HabinezaNo ratings yet

- Transformation Index BTI 2012: Regional Findings East-Central and Southeast EuropeFrom EverandTransformation Index BTI 2012: Regional Findings East-Central and Southeast EuropeNo ratings yet

- Why RomaniaDocument40 pagesWhy RomaniascrobNo ratings yet

- Summary2015 PolandDocument26 pagesSummary2015 Polandvincentcpt66No ratings yet

- President Hollande One Year On - What's Next? An Analysis From APCO Worldwide in ParisDocument12 pagesPresident Hollande One Year On - What's Next? An Analysis From APCO Worldwide in ParisAPCO WorldwideNo ratings yet

- Determinants of Economic Growth in V4 Countries and RomaniaDocument14 pagesDeterminants of Economic Growth in V4 Countries and RomaniaJorkosNo ratings yet

- Poland: Presented byDocument13 pagesPoland: Presented byAbhishek AgarwalNo ratings yet

- Pest Analysis of RomaniaDocument15 pagesPest Analysis of Romaniaravicbs100% (1)

- Romania - Nations in Transit 2022 Country Report - Freedom HouseDocument22 pagesRomania - Nations in Transit 2022 Country Report - Freedom HouseAridayanti ArifinNo ratings yet

- Lithuania Long-Term Rating Raised To 'A-' On Expected Adoption of Euro Outlook StableDocument8 pagesLithuania Long-Term Rating Raised To 'A-' On Expected Adoption of Euro Outlook Stableapi-231665846No ratings yet

- Annual Rapport EFOR - Political Errors of 2014 What Is To Be DoneDocument2 pagesAnnual Rapport EFOR - Political Errors of 2014 What Is To Be DoneCiolacuRaduNo ratings yet

- Brief Economic Outlook 2010 - 2014Document5 pagesBrief Economic Outlook 2010 - 2014Aaesta PriyestaNo ratings yet

- Moldova's Political Crisis: Where FromDocument2 pagesMoldova's Political Crisis: Where FromMadlenna's CoutureNo ratings yet

- Romania Diagnostic: Jakov Milatovic and Mateusz Szczurek January 2020Document44 pagesRomania Diagnostic: Jakov Milatovic and Mateusz Szczurek January 2020Cem's ChannelNo ratings yet

- TurkeyDocument2 pagesTurkeyZaf XafNo ratings yet

- Economic Survey of PakistanEconomic Survey of Pakistan Trade and Payments Trade and PaymentsDocument28 pagesEconomic Survey of PakistanEconomic Survey of Pakistan Trade and Payments Trade and PaymentsmadddiuNo ratings yet

- Ce Top 500 2016Document88 pagesCe Top 500 2016Ion PreascaNo ratings yet

- Poland On Its Way To GreeceDocument7 pagesPoland On Its Way To GreeceH5F CommunicationsNo ratings yet

- The Countries: Defining The "Quick Facts"Document3 pagesThe Countries: Defining The "Quick Facts"Jollybelleann MarcosNo ratings yet

- B&H Monthly Economic Report - December 2011Document12 pagesB&H Monthly Economic Report - December 2011Seid OmerovicNo ratings yet

- Country Intelligence: Report: TurkeyDocument27 pagesCountry Intelligence: Report: TurkeyFlorian SarkisNo ratings yet

- Ethiopia EIU (October) : HighlightsDocument10 pagesEthiopia EIU (October) : Highlightsalokgupta87No ratings yet

- Chapter 6Document3 pagesChapter 6perico1962No ratings yet

- On Shaky FoundationDocument27 pagesOn Shaky FoundationAmy HicksNo ratings yet

- Situatia Romaniei 2010Document7 pagesSituatia Romaniei 2010DanaNo ratings yet

- Summary Politic Hungary2014Document28 pagesSummary Politic Hungary2014vincentcpt66No ratings yet

- Forecasting Public Expenditure by Using Feed-Forward Neural NetworksDocument20 pagesForecasting Public Expenditure by Using Feed-Forward Neural NetworksKreator SolusiNo ratings yet

- Efma YearbookDocument72 pagesEfma Yearbooklc1560pintoNo ratings yet

- International Economics: Topic 7Document16 pagesInternational Economics: Topic 7Ngọc Minh NguyễnNo ratings yet

- OxfordAnalytica Prospects2012Document157 pagesOxfordAnalytica Prospects2012krasota_2No ratings yet

- CETOP500 2012 EngDocument104 pagesCETOP500 2012 Engtawhide_islamicNo ratings yet

- EN EN: European CommissionDocument24 pagesEN EN: European Commissionapi-58353949No ratings yet

- Business Sentiment Index: Have We Been Here Before?Document24 pagesBusiness Sentiment Index: Have We Been Here Before?Michal CernichNo ratings yet

- Autumn Statement 2011Document9 pagesAutumn Statement 2011IPPRNo ratings yet

- Flash Comment: Latvia - March 11, 2013Document1 pageFlash Comment: Latvia - March 11, 2013Swedbank AB (publ)No ratings yet

- Weekly Economic Commentary 8/13/2012Document5 pagesWeekly Economic Commentary 8/13/2012monarchadvisorygroupNo ratings yet

- June 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Document70 pagesJune 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Ilya MozyrskiyNo ratings yet

- BTI 2014 MalaysiaDocument32 pagesBTI 2014 MalaysiaCarm TesoroNo ratings yet

- Global Imbalances2Document11 pagesGlobal Imbalances2Amit KumarNo ratings yet

- Welsh Valleys 'Poorer Than Parts of Bulgaria, Romania and Poland'Document4 pagesWelsh Valleys 'Poorer Than Parts of Bulgaria, Romania and Poland'Elena IonNo ratings yet

- Post-Election Expectations of Influentials 2013Document18 pagesPost-Election Expectations of Influentials 2013josefplatilNo ratings yet

- Doing Business in PolandDocument18 pagesDoing Business in PolandczokoludekNo ratings yet

- 2011Document494 pages2011aman.4uNo ratings yet

- Kanhai Goswami 1Document20 pagesKanhai Goswami 1ytrdfghjjhgfdxcfghNo ratings yet

- London Tourism Cluster ReportDocument25 pagesLondon Tourism Cluster ReportShirah FoyNo ratings yet

- Romania Long Term OutlookDocument5 pagesRomania Long Term OutlooksmaneranNo ratings yet

- RBI Policy Dec 2011Document4 pagesRBI Policy Dec 2011Mitesh MahidharNo ratings yet

- Formular MepiDocument17 pagesFormular MepiIulia ChirilăNo ratings yet

- 08.valentin Maier Dragos Sdrobis PDFDocument10 pages08.valentin Maier Dragos Sdrobis PDFDragoș SdrobișNo ratings yet

- Book of Abstracts LUMEN Conference 2012Document264 pagesBook of Abstracts LUMEN Conference 2012Ingrid BagareanNo ratings yet

- Программа MBW 2019Document13 pagesПрограмма MBW 2019Михаил ШиловNo ratings yet

- Mate Matic ADocument8 pagesMate Matic AAlina Dragomir0% (2)

- The History of Transylvania (E-Book) PDFDocument280 pagesThe History of Transylvania (E-Book) PDFdan200505050% (1)

- Personal Medical de SpecialitateDocument9 pagesPersonal Medical de SpecialitateOana MikyNo ratings yet

- Curriculum Vitae: Claudia - Badulescu@eui - EuDocument8 pagesCurriculum Vitae: Claudia - Badulescu@eui - EuLIBAN ODOWANo ratings yet

- Characterization of The Romanian Rural Area in A European ContextDocument10 pagesCharacterization of The Romanian Rural Area in A European ContextCiurcea Laura LaurentiuNo ratings yet

- Tabel Centralizator - Culturi de PrimavaraDocument70 pagesTabel Centralizator - Culturi de PrimavaraBratosin MihaiNo ratings yet

- 2015 07 10 Pharma Distribution RomaniaDocument2 pages2015 07 10 Pharma Distribution RomaniaVanillaheroineNo ratings yet

- ICEEM07 - Abstract Deadline ExtensionDocument2 pagesICEEM07 - Abstract Deadline ExtensionMoscovici AncaNo ratings yet

- Poverty in Romania - Zamfir, C.Document12 pagesPoverty in Romania - Zamfir, C.Magda V.No ratings yet

- Lista Furnizori Asistenta Medicala Primara - 18.11.2020Document9 pagesLista Furnizori Asistenta Medicala Primara - 18.11.2020Nedelcu NicoletaNo ratings yet

- S.C., P.F. Şi A.F. Care Desfăşoară Activităţi Agricole Pe Raza Comunei CobadinDocument3 pagesS.C., P.F. Şi A.F. Care Desfăşoară Activităţi Agricole Pe Raza Comunei CobadinAnamaria PetrescuNo ratings yet

- Presentation of Romania Erasmus PDFDocument107 pagesPresentation of Romania Erasmus PDFȘtefania SotaeNo ratings yet

- Open Letter To BBC by Ovidiu VuiaDocument10 pagesOpen Letter To BBC by Ovidiu VuiaRita Vuia100% (2)

- Being A - Gypsy - The Worst Social Stigma in Romania - European Roma Rights CentreDocument14 pagesBeing A - Gypsy - The Worst Social Stigma in Romania - European Roma Rights CentredandanacheNo ratings yet

- Catalog RomFilm2015 Preview 051Document92 pagesCatalog RomFilm2015 Preview 051MaireneNo ratings yet

- Early Marriages Romani CRISSDocument127 pagesEarly Marriages Romani CRISSIov Claudia AnamariaNo ratings yet

- Lista Castigatori Tombola E.on - 21Document17 pagesLista Castigatori Tombola E.on - 21AnnaMariaNo ratings yet

- Medicidefamilie 2011Document6 pagesMedicidefamilie 2011Mesaros AlexandruNo ratings yet

- PROGRAM ECAI 2023 Web Lj9saspaDocument36 pagesPROGRAM ECAI 2023 Web Lj9saspaAndrei GheorghiuNo ratings yet

- 11 PremiiDocument1 page11 PremiiMihaela MihaiNo ratings yet

- Discover The Carpathian Garden BrochureDocument33 pagesDiscover The Carpathian Garden BrochureAurelian Corneliu MoraruNo ratings yet

- Diana NASTASIA Diana-Maria CISMARUDocument11 pagesDiana NASTASIA Diana-Maria CISMARUBettina GeorgianaNo ratings yet

- Rencsik Levente CVDocument3 pagesRencsik Levente CVRencsik LeventeNo ratings yet

- Dramatica 1 / 2019Document258 pagesDramatica 1 / 2019tibNo ratings yet

- Yokoso in Roumania!: We Are Here!Document13 pagesYokoso in Roumania!: We Are Here!noname093No ratings yet

- Suprafete - Conturi - Contacte Andreea + GabiDocument21 pagesSuprafete - Conturi - Contacte Andreea + GabiAndreea MustăţeaNo ratings yet

Download as pdf or txt

You might also like

- France PestleDocument39 pagesFrance PestleAlee LowNo ratings yet

- Example SRL - H1 2012Document9 pagesExample SRL - H1 2012tomideuNo ratings yet

- Egypt EconomicDocument3 pagesEgypt EconomicakshittayalNo ratings yet

- Poland Economic: PoliticalDocument3 pagesPoland Economic: PoliticaljjnjwdcjNo ratings yet

- 12 For 2012: Why Poland Will Avoid Recession Even If Whole EU Does NotDocument3 pages12 For 2012: Why Poland Will Avoid Recession Even If Whole EU Does NotPeter RheeNo ratings yet

- The Republic of Moldova in The Eastern Partnership: From Poster Child To Problem Child ?Document10 pagesThe Republic of Moldova in The Eastern Partnership: From Poster Child To Problem Child ?Viorica RussuNo ratings yet

- Studii Economice - CofaceDocument2 pagesStudii Economice - CofaceVelicanu Bekk ZsuzsaNo ratings yet

- SEB Report: Italian Elections Likely To Secure Continuation of ReformsDocument3 pagesSEB Report: Italian Elections Likely To Secure Continuation of ReformsSEB GroupNo ratings yet

- Analysis of Netherland EconomyDocument30 pagesAnalysis of Netherland EconomymohitNo ratings yet

- BTI 2014 Laos Country ReportDocument28 pagesBTI 2014 Laos Country ReportPhilip BravoNo ratings yet

- Dambovita Sum Up Research - GrecuDocument8 pagesDambovita Sum Up Research - GrecuCristina CristeaNo ratings yet

- BelgiumDocument2 pagesBelgiumHa VoNo ratings yet

- Slovakia: In-Depth PEST InsightsDocument38 pagesSlovakia: In-Depth PEST Insightskarthik_srinivasa_14No ratings yet

- February 2011 Monetary Policy Statement Lastdoc 2Document36 pagesFebruary 2011 Monetary Policy Statement Lastdoc 2Théotime HabinezaNo ratings yet

- Transformation Index BTI 2012: Regional Findings East-Central and Southeast EuropeFrom EverandTransformation Index BTI 2012: Regional Findings East-Central and Southeast EuropeNo ratings yet

- Why RomaniaDocument40 pagesWhy RomaniascrobNo ratings yet

- Summary2015 PolandDocument26 pagesSummary2015 Polandvincentcpt66No ratings yet

- President Hollande One Year On - What's Next? An Analysis From APCO Worldwide in ParisDocument12 pagesPresident Hollande One Year On - What's Next? An Analysis From APCO Worldwide in ParisAPCO WorldwideNo ratings yet

- Determinants of Economic Growth in V4 Countries and RomaniaDocument14 pagesDeterminants of Economic Growth in V4 Countries and RomaniaJorkosNo ratings yet

- Poland: Presented byDocument13 pagesPoland: Presented byAbhishek AgarwalNo ratings yet

- Pest Analysis of RomaniaDocument15 pagesPest Analysis of Romaniaravicbs100% (1)

- Romania - Nations in Transit 2022 Country Report - Freedom HouseDocument22 pagesRomania - Nations in Transit 2022 Country Report - Freedom HouseAridayanti ArifinNo ratings yet

- Lithuania Long-Term Rating Raised To 'A-' On Expected Adoption of Euro Outlook StableDocument8 pagesLithuania Long-Term Rating Raised To 'A-' On Expected Adoption of Euro Outlook Stableapi-231665846No ratings yet

- Annual Rapport EFOR - Political Errors of 2014 What Is To Be DoneDocument2 pagesAnnual Rapport EFOR - Political Errors of 2014 What Is To Be DoneCiolacuRaduNo ratings yet

- Brief Economic Outlook 2010 - 2014Document5 pagesBrief Economic Outlook 2010 - 2014Aaesta PriyestaNo ratings yet

- Moldova's Political Crisis: Where FromDocument2 pagesMoldova's Political Crisis: Where FromMadlenna's CoutureNo ratings yet

- Romania Diagnostic: Jakov Milatovic and Mateusz Szczurek January 2020Document44 pagesRomania Diagnostic: Jakov Milatovic and Mateusz Szczurek January 2020Cem's ChannelNo ratings yet

- TurkeyDocument2 pagesTurkeyZaf XafNo ratings yet

- Economic Survey of PakistanEconomic Survey of Pakistan Trade and Payments Trade and PaymentsDocument28 pagesEconomic Survey of PakistanEconomic Survey of Pakistan Trade and Payments Trade and PaymentsmadddiuNo ratings yet

- Ce Top 500 2016Document88 pagesCe Top 500 2016Ion PreascaNo ratings yet

- Poland On Its Way To GreeceDocument7 pagesPoland On Its Way To GreeceH5F CommunicationsNo ratings yet

- The Countries: Defining The "Quick Facts"Document3 pagesThe Countries: Defining The "Quick Facts"Jollybelleann MarcosNo ratings yet

- B&H Monthly Economic Report - December 2011Document12 pagesB&H Monthly Economic Report - December 2011Seid OmerovicNo ratings yet

- Country Intelligence: Report: TurkeyDocument27 pagesCountry Intelligence: Report: TurkeyFlorian SarkisNo ratings yet

- Ethiopia EIU (October) : HighlightsDocument10 pagesEthiopia EIU (October) : Highlightsalokgupta87No ratings yet

- Chapter 6Document3 pagesChapter 6perico1962No ratings yet

- On Shaky FoundationDocument27 pagesOn Shaky FoundationAmy HicksNo ratings yet

- Situatia Romaniei 2010Document7 pagesSituatia Romaniei 2010DanaNo ratings yet

- Summary Politic Hungary2014Document28 pagesSummary Politic Hungary2014vincentcpt66No ratings yet

- Forecasting Public Expenditure by Using Feed-Forward Neural NetworksDocument20 pagesForecasting Public Expenditure by Using Feed-Forward Neural NetworksKreator SolusiNo ratings yet

- Efma YearbookDocument72 pagesEfma Yearbooklc1560pintoNo ratings yet

- International Economics: Topic 7Document16 pagesInternational Economics: Topic 7Ngọc Minh NguyễnNo ratings yet

- OxfordAnalytica Prospects2012Document157 pagesOxfordAnalytica Prospects2012krasota_2No ratings yet

- CETOP500 2012 EngDocument104 pagesCETOP500 2012 Engtawhide_islamicNo ratings yet

- EN EN: European CommissionDocument24 pagesEN EN: European Commissionapi-58353949No ratings yet

- Business Sentiment Index: Have We Been Here Before?Document24 pagesBusiness Sentiment Index: Have We Been Here Before?Michal CernichNo ratings yet

- Autumn Statement 2011Document9 pagesAutumn Statement 2011IPPRNo ratings yet

- Flash Comment: Latvia - March 11, 2013Document1 pageFlash Comment: Latvia - March 11, 2013Swedbank AB (publ)No ratings yet

- Weekly Economic Commentary 8/13/2012Document5 pagesWeekly Economic Commentary 8/13/2012monarchadvisorygroupNo ratings yet

- June 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Document70 pagesJune 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Ilya MozyrskiyNo ratings yet

- BTI 2014 MalaysiaDocument32 pagesBTI 2014 MalaysiaCarm TesoroNo ratings yet

- Global Imbalances2Document11 pagesGlobal Imbalances2Amit KumarNo ratings yet

- Welsh Valleys 'Poorer Than Parts of Bulgaria, Romania and Poland'Document4 pagesWelsh Valleys 'Poorer Than Parts of Bulgaria, Romania and Poland'Elena IonNo ratings yet

- Post-Election Expectations of Influentials 2013Document18 pagesPost-Election Expectations of Influentials 2013josefplatilNo ratings yet

- Doing Business in PolandDocument18 pagesDoing Business in PolandczokoludekNo ratings yet

- 2011Document494 pages2011aman.4uNo ratings yet

- Kanhai Goswami 1Document20 pagesKanhai Goswami 1ytrdfghjjhgfdxcfghNo ratings yet

- London Tourism Cluster ReportDocument25 pagesLondon Tourism Cluster ReportShirah FoyNo ratings yet

- Romania Long Term OutlookDocument5 pagesRomania Long Term OutlooksmaneranNo ratings yet

- RBI Policy Dec 2011Document4 pagesRBI Policy Dec 2011Mitesh MahidharNo ratings yet

- Formular MepiDocument17 pagesFormular MepiIulia ChirilăNo ratings yet

- 08.valentin Maier Dragos Sdrobis PDFDocument10 pages08.valentin Maier Dragos Sdrobis PDFDragoș SdrobișNo ratings yet

- Book of Abstracts LUMEN Conference 2012Document264 pagesBook of Abstracts LUMEN Conference 2012Ingrid BagareanNo ratings yet

- Программа MBW 2019Document13 pagesПрограмма MBW 2019Михаил ШиловNo ratings yet

- Mate Matic ADocument8 pagesMate Matic AAlina Dragomir0% (2)

- The History of Transylvania (E-Book) PDFDocument280 pagesThe History of Transylvania (E-Book) PDFdan200505050% (1)

- Personal Medical de SpecialitateDocument9 pagesPersonal Medical de SpecialitateOana MikyNo ratings yet

- Curriculum Vitae: Claudia - Badulescu@eui - EuDocument8 pagesCurriculum Vitae: Claudia - Badulescu@eui - EuLIBAN ODOWANo ratings yet

- Characterization of The Romanian Rural Area in A European ContextDocument10 pagesCharacterization of The Romanian Rural Area in A European ContextCiurcea Laura LaurentiuNo ratings yet

- Tabel Centralizator - Culturi de PrimavaraDocument70 pagesTabel Centralizator - Culturi de PrimavaraBratosin MihaiNo ratings yet

- 2015 07 10 Pharma Distribution RomaniaDocument2 pages2015 07 10 Pharma Distribution RomaniaVanillaheroineNo ratings yet

- ICEEM07 - Abstract Deadline ExtensionDocument2 pagesICEEM07 - Abstract Deadline ExtensionMoscovici AncaNo ratings yet

- Poverty in Romania - Zamfir, C.Document12 pagesPoverty in Romania - Zamfir, C.Magda V.No ratings yet

- Lista Furnizori Asistenta Medicala Primara - 18.11.2020Document9 pagesLista Furnizori Asistenta Medicala Primara - 18.11.2020Nedelcu NicoletaNo ratings yet

- S.C., P.F. Şi A.F. Care Desfăşoară Activităţi Agricole Pe Raza Comunei CobadinDocument3 pagesS.C., P.F. Şi A.F. Care Desfăşoară Activităţi Agricole Pe Raza Comunei CobadinAnamaria PetrescuNo ratings yet

- Presentation of Romania Erasmus PDFDocument107 pagesPresentation of Romania Erasmus PDFȘtefania SotaeNo ratings yet

- Open Letter To BBC by Ovidiu VuiaDocument10 pagesOpen Letter To BBC by Ovidiu VuiaRita Vuia100% (2)

- Being A - Gypsy - The Worst Social Stigma in Romania - European Roma Rights CentreDocument14 pagesBeing A - Gypsy - The Worst Social Stigma in Romania - European Roma Rights CentredandanacheNo ratings yet

- Catalog RomFilm2015 Preview 051Document92 pagesCatalog RomFilm2015 Preview 051MaireneNo ratings yet

- Early Marriages Romani CRISSDocument127 pagesEarly Marriages Romani CRISSIov Claudia AnamariaNo ratings yet

- Lista Castigatori Tombola E.on - 21Document17 pagesLista Castigatori Tombola E.on - 21AnnaMariaNo ratings yet

- Medicidefamilie 2011Document6 pagesMedicidefamilie 2011Mesaros AlexandruNo ratings yet

- PROGRAM ECAI 2023 Web Lj9saspaDocument36 pagesPROGRAM ECAI 2023 Web Lj9saspaAndrei GheorghiuNo ratings yet

- 11 PremiiDocument1 page11 PremiiMihaela MihaiNo ratings yet

- Discover The Carpathian Garden BrochureDocument33 pagesDiscover The Carpathian Garden BrochureAurelian Corneliu MoraruNo ratings yet

- Diana NASTASIA Diana-Maria CISMARUDocument11 pagesDiana NASTASIA Diana-Maria CISMARUBettina GeorgianaNo ratings yet

- Rencsik Levente CVDocument3 pagesRencsik Levente CVRencsik LeventeNo ratings yet

- Dramatica 1 / 2019Document258 pagesDramatica 1 / 2019tibNo ratings yet

- Yokoso in Roumania!: We Are Here!Document13 pagesYokoso in Roumania!: We Are Here!noname093No ratings yet

- Suprafete - Conturi - Contacte Andreea + GabiDocument21 pagesSuprafete - Conturi - Contacte Andreea + GabiAndreea MustăţeaNo ratings yet