Download as doc, pdf, or txt

You might also like

- Edita Food IndustriesDocument36 pagesEdita Food Industriesmohamed aliNo ratings yet

- The Determinants of Budget Deficit in EthiopiaDocument56 pagesThe Determinants of Budget Deficit in Ethiopiaasamino mulugeta91% (23)

- Summary Game TheoryDocument54 pagesSummary Game TheorytNo ratings yet

- Canada Immigration Consultants in BangaloreDocument17 pagesCanada Immigration Consultants in Bangaloreakkam immigrationNo ratings yet

- Project Report On Performance ManagmentDocument5 pagesProject Report On Performance ManagmentClarissa AntaoNo ratings yet

- Document 2Document1 pageDocument 2Mathew Justin RajuNo ratings yet

- Conservation Principle and Balance SheetDocument6 pagesConservation Principle and Balance SheetKumar RajeshNo ratings yet

- Nguyen Dinh KhanhDocument2 pagesNguyen Dinh KhanhDinhkhanh NguyenNo ratings yet

- Accounting Concepts and ConventionsDocument4 pagesAccounting Concepts and ConventionssrinugudaNo ratings yet

- ConservatismDocument2 pagesConservatismNavodit MittalNo ratings yet

- Merged Fa Cwa NotesDocument799 pagesMerged Fa Cwa NotesAkash VaidNo ratings yet

- Accounting Concepts and Conventions Qualitative FeaturesDocument8 pagesAccounting Concepts and Conventions Qualitative FeaturesKhadejai LairdNo ratings yet

- Eleven Key Accounting ConceptsDocument6 pagesEleven Key Accounting ConceptsSyed Ikram Ullah ShahNo ratings yet

- Assignment Fundamentals of Book - Keeping & AccountingDocument19 pagesAssignment Fundamentals of Book - Keeping & AccountingmailonvikasNo ratings yet

- FAQs For F&a InterviewsDocument13 pagesFAQs For F&a InterviewsVamsi Chowdary KolliNo ratings yet

- Chapter 4 AccountingDocument22 pagesChapter 4 AccountingChan Man SeongNo ratings yet

- Overview of Financial Reports: 1. Balance SheetDocument5 pagesOverview of Financial Reports: 1. Balance SheetAhmer SohailNo ratings yet

- Accounting Concepts F5Document7 pagesAccounting Concepts F5Tinevimbo NdlovuNo ratings yet

- Basic Concepts and ConventionsDocument5 pagesBasic Concepts and ConventionsAhmet BabayevNo ratings yet

- What Are The Accounting Concepts and ConventionsDocument3 pagesWhat Are The Accounting Concepts and ConventionsPriyanka PatilNo ratings yet

- Accounting Policies Can Be Used To Legally Manipulate EarningsDocument7 pagesAccounting Policies Can Be Used To Legally Manipulate EarningsKisitu MosesNo ratings yet

- Accounting PrudenceDocument11 pagesAccounting PrudenceloyNo ratings yet

- Accounting Concepts and ConventionsDocument5 pagesAccounting Concepts and ConventionsSam SamNo ratings yet

- The Conservatism PrincipleDocument2 pagesThe Conservatism PrinciplePankaj JindalNo ratings yet

- Finman2b ReportDocument6 pagesFinman2b ReportLey MiclatNo ratings yet

- Aldridge State High School Es6 - Internal ControlsDocument10 pagesAldridge State High School Es6 - Internal ControlsJiim Paoolo BlaascoNo ratings yet

- AccountingDocument7 pagesAccountingShiela RescoNo ratings yet

- 2 Accounting Concepts and ConventionsDocument5 pages2 Accounting Concepts and Conventionsazra khanNo ratings yet

- Types of RisksDocument3 pagesTypes of RisksSalik HussainNo ratings yet

- 3.5 ConceptsDocument7 pages3.5 Conceptsattaelahi804No ratings yet

- LiquidityDocument5 pagesLiquidityMobin ShaleeNo ratings yet

- Accounting Concepts and ConventionsDocument4 pagesAccounting Concepts and ConventionsSaumitra TripathiNo ratings yet

- Ov Ov Ov OvDocument8 pagesOv Ov Ov Ovdeepak_rathod_5No ratings yet

- ACCA Principles of AccountingDocument6 pagesACCA Principles of Accountingourwork2626No ratings yet

- Accounting ConceptsDocument8 pagesAccounting ConceptsBajra VinayaNo ratings yet

- Auditing NotesDocument73 pagesAuditing Notesvivekrawatsingh9084No ratings yet

- Accounting Concepts and Principles PDFDocument9 pagesAccounting Concepts and Principles PDFDennis LacsonNo ratings yet

- Chapter 3 Analyzing Transactions To Start A BusinessDocument3 pagesChapter 3 Analyzing Transactions To Start A BusinessPaw VerdilloNo ratings yet

- HBS - Financial AccountingDocument3 pagesHBS - Financial Accountingrahul2014mehtaNo ratings yet

- Conventions: Convention of DisclosureDocument5 pagesConventions: Convention of DisclosureAiswarya ShanmugamNo ratings yet

- Financial Health: What Is 'Working Capital'Document6 pagesFinancial Health: What Is 'Working Capital'Abhishek BanerjeeNo ratings yet

- Module 5 - Adjusting AccountsDocument16 pagesModule 5 - Adjusting AccountsMJ San PedroNo ratings yet

- Accounts PresentationDocument22 pagesAccounts PresentationSenthil Kumar N GNo ratings yet

- Table of ContentsDocument57 pagesTable of ContentsAbhishek AbhiNo ratings yet

- Keeping ScoreDocument95 pagesKeeping ScoreVijay KumarNo ratings yet

- Meaning and Nature of Accounting Principle: Veena Madaan M.B.A (Finance)Document25 pagesMeaning and Nature of Accounting Principle: Veena Madaan M.B.A (Finance)JenniferNo ratings yet

- Accounting Concepts: 1. The Entity ConceptDocument3 pagesAccounting Concepts: 1. The Entity ConceptNormanRockfellerNo ratings yet

- Accounting TerminologyDocument71 pagesAccounting TerminologyBiplob K. SannyasiNo ratings yet

- Module 2 - Financial Accounting PrinciplesDocument13 pagesModule 2 - Financial Accounting PrinciplesVimbai MusangeyaNo ratings yet

- Going Concern Concept: Accounting ConceptsDocument4 pagesGoing Concern Concept: Accounting ConceptsDalton McleanNo ratings yet

- Chapter 5Document8 pagesChapter 5Janah MirandaNo ratings yet

- 06 ReceivableDocument104 pages06 Receivablefordan Zodorovic100% (4)

- Accounting PrinciplesDocument12 pagesAccounting PrinciplesTooba HashmiNo ratings yet

- Definition of The 'Going Concern' Concept: AccountingDocument4 pagesDefinition of The 'Going Concern' Concept: Accountingmhrscribd014No ratings yet

- Accounting Concepts and PrinciplesDocument5 pagesAccounting Concepts and PrinciplesKenneth RamosNo ratings yet

- Chapter 3Document7 pagesChapter 3Tasebe GetachewNo ratings yet

- Generally Accepted Accounitng Princinples (GAAP)Document8 pagesGenerally Accepted Accounitng Princinples (GAAP)Eng Abdikarim WalhadNo ratings yet

- Financial Ratio TutorialDocument41 pagesFinancial Ratio Tutorialabhi2244inNo ratings yet

- Advanced Study For Accountancy Week 1Document3 pagesAdvanced Study For Accountancy Week 1Rose Ann GuevarraNo ratings yet

- 6 Accounting Concepts and PrinciplesDocument25 pages6 Accounting Concepts and Principlesapi-26702351283% (6)

- Midterm LecturesDocument21 pagesMidterm LecturesRachel LozadaNo ratings yet

- Accounting Concepts and Conventions.: MaterialityDocument4 pagesAccounting Concepts and Conventions.: MaterialityGuru NathanNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Bookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)From EverandBookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)No ratings yet

- Essay On Load Shedding in Pakistan (Rolling Blackout)Document4 pagesEssay On Load Shedding in Pakistan (Rolling Blackout)Sajid HanifNo ratings yet

- Marketing Awareness 2012Document29 pagesMarketing Awareness 2012Vinod Kumar AyilalathNo ratings yet

- Jinja UgandaDocument4 pagesJinja Ugandaxsa ssdsadNo ratings yet

- After Capitalism New Critical TheoryDocument110 pagesAfter Capitalism New Critical TheoryEsteban Arias100% (1)

- Income Taxation Outline and CasesDocument7 pagesIncome Taxation Outline and CasesChicklet ArponNo ratings yet

- CNFC Media PVT LTDDocument21 pagesCNFC Media PVT LTDshekhar_cnfcmedia100% (1)

- Mobile Crane Lifting PermitDocument2 pagesMobile Crane Lifting PermitMusadiq HussainNo ratings yet

- Mohit Dixit Training ReportDocument84 pagesMohit Dixit Training ReportAnonymous DJybroNXNo ratings yet

- Characteristics of The 3rd World CountriesDocument13 pagesCharacteristics of The 3rd World CountriesMaddy Lee80% (5)

- Green Accounting: A Conceptual Framework: Tony Greenham, 24 September 2010Document17 pagesGreen Accounting: A Conceptual Framework: Tony Greenham, 24 September 2010ririanNo ratings yet

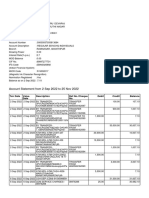

- Account Statement From 2 Sep 2022 To 25 Nov 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 2 Sep 2022 To 25 Nov 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRaju BhaiNo ratings yet

- E 07 H 1 SalaryDocument8 pagesE 07 H 1 SalaryMintNo ratings yet

- MGT520 Mid Term Solved Subjective Downloaded Form VurankDocument4 pagesMGT520 Mid Term Solved Subjective Downloaded Form VurankHamzaNo ratings yet

- Budget Artikel ExcelDocument8 pagesBudget Artikel ExcelnugrahaNo ratings yet

- Homes4Wiltshire To Rent Aug14Document7 pagesHomes4Wiltshire To Rent Aug14nameNo ratings yet

- Jute BAGDocument4 pagesJute BAGETERNAL CONSULTANCY AND SERVICESNo ratings yet

- Third Party and Fourth Party LogisticsDocument113 pagesThird Party and Fourth Party LogisticsHenry Bastian C100% (1)

- Uttam Patra Project NewDocument33 pagesUttam Patra Project NewDeepak KumarNo ratings yet

- Endorsement Schedule: LC0000000619 Intermediary Code Name M/S.Policybazaar Insurance Brokers Private LimitedDocument1 pageEndorsement Schedule: LC0000000619 Intermediary Code Name M/S.Policybazaar Insurance Brokers Private LimitedPrakhar ShuklaNo ratings yet

- NOA 9x8Document5 pagesNOA 9x8David PazmiñoNo ratings yet

- Ent300 Project Assignment: Case StudyDocument70 pagesEnt300 Project Assignment: Case StudyTaqiTazali100% (3)

- EXPRESSCALL, 5 R. Padilla Street, Cebu City, Cebu, Philippines Telephone Nos. (032) 512-7194/ 268-6625/ 262-6687Document12 pagesEXPRESSCALL, 5 R. Padilla Street, Cebu City, Cebu, Philippines Telephone Nos. (032) 512-7194/ 268-6625/ 262-6687Anen Dotcamul BinigayNo ratings yet

- KLD From Gin Girls To ScavengersDocument9 pagesKLD From Gin Girls To ScavengersShipShapeNo ratings yet

- Communication Regarding Corporate RestructuringDocument2 pagesCommunication Regarding Corporate RestructuringANURAG RAJAKNo ratings yet

- Policy Brief On Aquaculture in Ebonyi StateDocument6 pagesPolicy Brief On Aquaculture in Ebonyi StateOkoro Nwenyi100% (1)