Download as pdf or txt

You might also like

- Dispersion TradesDocument41 pagesDispersion TradesLameune100% (1)

- Goldstein Solution 8Document11 pagesGoldstein Solution 8Marcus MacêdoNo ratings yet

- Mechanics SolutionsDocument7 pagesMechanics SolutionsJoelNo ratings yet

- FCM Wave Equation (Cambridge)Document2 pagesFCM Wave Equation (Cambridge)ucaptd3No ratings yet

- Problem Solutions Becker String TheoryDocument129 pagesProblem Solutions Becker String Theorybanedog100% (2)

- Em 6.20Document3 pagesEm 6.20sauciataNo ratings yet

- A Smart Motor Controller For E-Bike Applications PDFDocument4 pagesA Smart Motor Controller For E-Bike Applications PDFaungwinnaing100% (1)

- Rodrigues & Vaz - Subluminal and Superluminal Slution in Vacuum of Maxwell Equations and Massless Dirac Equation 1995Document8 pagesRodrigues & Vaz - Subluminal and Superluminal Slution in Vacuum of Maxwell Equations and Massless Dirac Equation 1995theherbsmithNo ratings yet

- From Boltzmann To Euler, Hilbert 6th Problem (2012) - DoneDocument9 pagesFrom Boltzmann To Euler, Hilbert 6th Problem (2012) - Donedr_s_m_afzali8662No ratings yet

- Ternary For ArxivDocument15 pagesTernary For ArxivPat McGrathNo ratings yet

- Appendix A: Conventions and Signs: 1 Dimensional AnalysisDocument4 pagesAppendix A: Conventions and Signs: 1 Dimensional AnalysisAritra MoitraNo ratings yet

- 16.4. Problem Set Iv 220 Answers: Problem Set IV: D DT MDocument5 pages16.4. Problem Set Iv 220 Answers: Problem Set IV: D DT MShweta SridharNo ratings yet

- Homework 3 So LsDocument13 pagesHomework 3 So LsBrad StokesNo ratings yet

- 11 AbociDocument10 pages11 AbocielectrotehnicaNo ratings yet

- On Sequences Defined by Linear Recurrence Relations : (2) U +K + Aiun+K-X + + Aku A, 0Document9 pagesOn Sequences Defined by Linear Recurrence Relations : (2) U +K + Aiun+K-X + + Aku A, 0Anonymous bk7we8No ratings yet

- Wet OryDocument15 pagesWet OryMatan Even TsurNo ratings yet

- QFT Example Sheet 1 Solutions PDFDocument13 pagesQFT Example Sheet 1 Solutions PDFafaf_physNo ratings yet

- Computing Helmert TransformationsDocument12 pagesComputing Helmert TransformationsNuno MiraNo ratings yet

- A Few Comments On Combination of Variables: in The Liquid, and X 0 Is The Gas-Liquid InterfaceDocument7 pagesA Few Comments On Combination of Variables: in The Liquid, and X 0 Is The Gas-Liquid Interfaceمرتضى عباسNo ratings yet

- Triple 331Document12 pagesTriple 331Ana Clara SalazarNo ratings yet

- Aplication MB 2Document18 pagesAplication MB 2Poundra SetiawanNo ratings yet

- Trigonometric Substitutions: Harvey Mudd College Math TutorialDocument3 pagesTrigonometric Substitutions: Harvey Mudd College Math TutorialArtist RecordingNo ratings yet

- 776 Notes - FFT MethodsDocument7 pages776 Notes - FFT Methodsnemamea1No ratings yet

- Classical 2Document13 pagesClassical 2Zulfian FiskNo ratings yet

- DiracDocument14 pagesDiracRavi BabuNo ratings yet

- Five DimensionsDocument5 pagesFive DimensionsTBoo Techno-bambooNo ratings yet

- Rodrigo Aros and Andres Gomberoff - Counting The Negative Eigenvalues of The Thermalon in Three DimensionsDocument11 pagesRodrigo Aros and Andres Gomberoff - Counting The Negative Eigenvalues of The Thermalon in Three DimensionsUmav24No ratings yet

- 3.8, δ and d notations for changes: Large changes: We use the Greek symbolDocument7 pages3.8, δ and d notations for changes: Large changes: We use the Greek symbolmasyuki1979No ratings yet

- On The Quantization of The N 2 Supersymmetric Non Linear Sigma ModelDocument15 pagesOn The Quantization of The N 2 Supersymmetric Non Linear Sigma ModelhumbertorcNo ratings yet

- Five-Dimensional Warped Geometry With A Bulk Scalar Field: DPNU-01-24 Hep-Th/0109040Document8 pagesFive-Dimensional Warped Geometry With A Bulk Scalar Field: DPNU-01-24 Hep-Th/0109040wendel_physicsNo ratings yet

- Brane Cosmology From Heterotic String Theory: Apostolos Kuiroukidis and Demetrios B. PapadopoulosDocument15 pagesBrane Cosmology From Heterotic String Theory: Apostolos Kuiroukidis and Demetrios B. PapadopoulosmimoraydenNo ratings yet

- The Primitive Root Theorem Amin Witno: AppetizerDocument9 pagesThe Primitive Root Theorem Amin Witno: AppetizerFachni RosyadiNo ratings yet

- Fokker Planck and Path IntegralsDocument13 pagesFokker Planck and Path IntegralssrrisbudNo ratings yet

- Problem Set 9 Problem 1.: DT V R F DDocument2 pagesProblem Set 9 Problem 1.: DT V R F DmkpsrtmNo ratings yet

- Noether's Theorem in Classical Mechanics Revisited: Rubens M Marinho JRDocument7 pagesNoether's Theorem in Classical Mechanics Revisited: Rubens M Marinho JRss_nainamohammedNo ratings yet

- F07 Hw06aDocument13 pagesF07 Hw06aAdam ChanNo ratings yet

- Boltzmann's and Saha's EquationsDocument22 pagesBoltzmann's and Saha's Equationssujayan2005No ratings yet

- Problem EsDocument25 pagesProblem EsJuanjo Peris MontesaNo ratings yet

- Numerical Solutions of The Schrodinger EquationDocument26 pagesNumerical Solutions of The Schrodinger EquationqrrqrbrbrrblbllxNo ratings yet

- D. Klemm Et Al - Universality and A Generalized C-Function in CFTs With AdS DualsDocument21 pagesD. Klemm Et Al - Universality and A Generalized C-Function in CFTs With AdS DualsArsLexiiNo ratings yet

- The Ricci Flow On The 2-Sphere: J. Differential Geometry 33 (1991) 325-334Document10 pagesThe Ricci Flow On The 2-Sphere: J. Differential Geometry 33 (1991) 325-334RenatoSoviéticoNo ratings yet

- tmpD800 TMPDocument12 pagestmpD800 TMPFrontiersNo ratings yet

- Heavens GRDocument37 pagesHeavens GRDavidNo ratings yet

- Finite Difference MethodsDocument15 pagesFinite Difference MethodsRami Mahmoud BakrNo ratings yet

- Carl M. Bender Et Al - Compactons in PT - Symmetric Generalized Korteweg (De Vries EquationsDocument11 pagesCarl M. Bender Et Al - Compactons in PT - Symmetric Generalized Korteweg (De Vries EquationsPomac232No ratings yet

- Luiz C. de Albuquerque and R. M. Cavalcanti - Comment On "Casimir Force in Compact Non-Commutative Extra Dimensions and Radius Stabilization"Document6 pagesLuiz C. de Albuquerque and R. M. Cavalcanti - Comment On "Casimir Force in Compact Non-Commutative Extra Dimensions and Radius Stabilization"JuazmantNo ratings yet

- Solutions To Problems in Quantum Field TheoryDocument7 pagesSolutions To Problems in Quantum Field TheoryPhilip Saad100% (2)

- Phase Transitions in Field Theories at Finite Temperatures: 1 MotivationDocument5 pagesPhase Transitions in Field Theories at Finite Temperatures: 1 MotivationchichieinsteinNo ratings yet

- Homework #6 SolutionsDocument7 pagesHomework #6 SolutionsJr. Lessy Eka PutriNo ratings yet

- Calculus 141, Section 8.6 The Trapezoidal Rule & Simpson's RuleDocument4 pagesCalculus 141, Section 8.6 The Trapezoidal Rule & Simpson's RuleChathuranga ManukulaNo ratings yet

- Dupont - Fiber Bundles in Gauge TheoryDocument109 pagesDupont - Fiber Bundles in Gauge TheoryWilfred HulsbergenNo ratings yet

- Eric Bergshoeff and Antoine Van Proeyen - Symmetries of String, M - and F-TheoriesDocument12 pagesEric Bergshoeff and Antoine Van Proeyen - Symmetries of String, M - and F-TheoriesArsLexiiNo ratings yet

- 1 The Dirac Field and Lorentz Invariance: Soper@bovine - Uoregon.eduDocument15 pages1 The Dirac Field and Lorentz Invariance: Soper@bovine - Uoregon.eduFasiMalikNo ratings yet

- The Polynomial Time Algorithm For Testing Primality: George T. GilbertDocument22 pagesThe Polynomial Time Algorithm For Testing Primality: George T. GilbertimnomusNo ratings yet

- Classical Mechanics Notes (4 of 10)Document30 pagesClassical Mechanics Notes (4 of 10)OmegaUserNo ratings yet

- Ejercicios Gregory Capitulo 14Document5 pagesEjercicios Gregory Capitulo 14Gabriel BonomiNo ratings yet

- Convolution and Equidistribution: Sato-Tate Theorems for Finite-Field Mellin Transforms (AM-180)From EverandConvolution and Equidistribution: Sato-Tate Theorems for Finite-Field Mellin Transforms (AM-180)No ratings yet

- A-level Maths Revision: Cheeky Revision ShortcutsFrom EverandA-level Maths Revision: Cheeky Revision ShortcutsRating: 3.5 out of 5 stars3.5/5 (8)

- Brief Therapy - A Problem Solving Model of ChangeDocument4 pagesBrief Therapy - A Problem Solving Model of ChangeLameuneNo ratings yet

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityDocument1 pageA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneNo ratings yet

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyDocument32 pagesPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneNo ratings yet

- Eyde LandDocument54 pagesEyde LandLameuneNo ratings yet

- Network of Options For International Coal & Freight BusinessesDocument20 pagesNetwork of Options For International Coal & Freight BusinessesLameuneNo ratings yet

- Butterfly EconomicsDocument5 pagesButterfly EconomicsLameuneNo ratings yet

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 pagesReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNo ratings yet

- Commodity Hybrids Trading: James Groves, Barclays CapitalDocument21 pagesCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneNo ratings yet

- Jacob BeharallDocument19 pagesJacob BeharallLameuneNo ratings yet

- Andrea RoncoroniDocument27 pagesAndrea RoncoroniLameuneNo ratings yet

- Tristam ScottDocument24 pagesTristam ScottLameuneNo ratings yet

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingDocument25 pagesValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneNo ratings yet

- Day3 Session 1BSternberg PresentationforWebDocument11 pagesDay3 Session 1BSternberg PresentationforWebLameuneNo ratings yet

- Prmia 20111103 NyholmDocument24 pagesPrmia 20111103 NyholmLameuneNo ratings yet

- Marcel ProkopczukDocument28 pagesMarcel ProkopczukLameuneNo ratings yet

- Emmanuel GincbergDocument37 pagesEmmanuel GincbergLameuneNo ratings yet

- Day3 Session 2APaulDocument11 pagesDay3 Session 2APaulLameuneNo ratings yet

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 pagesReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNo ratings yet

- Day3 Session2B StoneDocument11 pagesDay3 Session2B StoneLameuneNo ratings yet

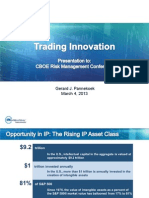

- Gerard J. Pannekoek March 4, 2013Document12 pagesGerard J. Pannekoek March 4, 2013LameuneNo ratings yet

- Day1 Session3 ColeDocument36 pagesDay1 Session3 ColeLameuneNo ratings yet

- Body MechanismDocument31 pagesBody MechanismAnnapurna DangetiNo ratings yet

- Electrical Specification PDFDocument235 pagesElectrical Specification PDFMinhTrieu100% (1)

- 3 PBDocument11 pages3 PBSuci DwiNo ratings yet

- Economists' Corner: Weighing The Procompetitive and Anticompetitive Effects of RPM Under The Rule of ReasonDocument3 pagesEconomists' Corner: Weighing The Procompetitive and Anticompetitive Effects of RPM Under The Rule of ReasonHarsh GandhiNo ratings yet

- Unit 1: A1 Coursebook AudioscriptsDocument39 pagesUnit 1: A1 Coursebook AudioscriptsRaul GaglieroNo ratings yet

- Adverb Worksheet For Class 4 With AnswersDocument10 pagesAdverb Worksheet For Class 4 With Answersrodolfo penaredondoNo ratings yet

- Panasonic LCD TH-L32C30Document72 pagesPanasonic LCD TH-L32C30King King0% (1)

- The Migration Industry and Future Directions For Migration PolicyDocument4 pagesThe Migration Industry and Future Directions For Migration PolicyGabriella VillaçaNo ratings yet

- Atlas Engineering Bar Handbook Rev Jan 2005-Oct 2011Document136 pagesAtlas Engineering Bar Handbook Rev Jan 2005-Oct 2011carlosc19715043No ratings yet

- ScP005 Line GraphsDocument2 pagesScP005 Line GraphsORBeducationNo ratings yet

- Models in The Research ProcessDocument7 pagesModels in The Research ProcesskumarNo ratings yet

- Story As World MakingDocument9 pagesStory As World MakingAugusto ChocobarNo ratings yet

- BobliDocument2 pagesBoblisuman karNo ratings yet

- Mapping PEC 2021-Oct-20 Annex-D Courses Vs PLO Vs TaxonomyDocument2 pagesMapping PEC 2021-Oct-20 Annex-D Courses Vs PLO Vs TaxonomyEngr.Mohsin ShaikhNo ratings yet

- Perinatal Mental Health Policy BriefDocument3 pagesPerinatal Mental Health Policy BriefThe Wilson CenterNo ratings yet

- Pharmacognosy-Large FontDocument35 pagesPharmacognosy-Large FontArantxa HilarioNo ratings yet

- The Effect of Emotional Freedom Technique On Stress and Anxiety in Nursing StudentsDocument119 pagesThe Effect of Emotional Freedom Technique On Stress and Anxiety in Nursing StudentsnguyenhabkNo ratings yet

- Arts Lessonplantemplatevisualarts2019Document18 pagesArts Lessonplantemplatevisualarts2019api-451772183No ratings yet

- Freeplane User Guide PDFDocument31 pagesFreeplane User Guide PDFAlma_Valladare_719No ratings yet

- Distribution Channel of AMULDocument13 pagesDistribution Channel of AMULMeet JivaniNo ratings yet

- TCS AIP Take Home AssignmentDocument16 pagesTCS AIP Take Home AssignmentShruthiSAthreyaNo ratings yet

- CHEMEXCILDocument28 pagesCHEMEXCILAmal JerryNo ratings yet

- S5750E-SI Series L2 Gigabits Dual Stack Intelligent Switch DatasheetDocument7 pagesS5750E-SI Series L2 Gigabits Dual Stack Intelligent Switch DatasheetThe LyricsNo ratings yet

- 5db83ef1f71e482 PDFDocument192 pages5db83ef1f71e482 PDFRajesh RoyNo ratings yet

- Low Voltage Current and Voltage Transformers PDFDocument260 pagesLow Voltage Current and Voltage Transformers PDFGustavo GamezNo ratings yet

- Irda Jun10Document96 pagesIrda Jun10ManiNo ratings yet

- EDTA CHEMICAL CLEANING (BLR) PDFDocument16 pagesEDTA CHEMICAL CLEANING (BLR) PDFAnudeep Chittluri100% (2)

- DT81 Data Logger DatasheetDocument2 pagesDT81 Data Logger DatasheetDuška JarčevićNo ratings yet

- Glory To God Light From Light With LyricsDocument13 pagesGlory To God Light From Light With LyricsRodolfo DeriquitoNo ratings yet