Download as docx, pdf, or txt

You might also like

- Dixie General StoreDocument6 pagesDixie General StoreJoneceNo ratings yet

- Home Page: Online Telephone Directory BSNLDocument3 pagesHome Page: Online Telephone Directory BSNLkamini25% (4)

- Life Insurance Kotak Mahindra Group Old MutualDocument16 pagesLife Insurance Kotak Mahindra Group Old MutualKanchan khedaskerNo ratings yet

- INSURANCE Asss PrachiDocument3 pagesINSURANCE Asss Prachivbs522No ratings yet

- Basic Information About LIC PoliciesDocument6 pagesBasic Information About LIC PoliciesskumarshopperNo ratings yet

- Whole Life InsuranceDocument16 pagesWhole Life Insuranceemilda_samuel211No ratings yet

- My ProjectDocument94 pagesMy ProjectSunil RawatNo ratings yet

- Insurance Products: Debi DattaDocument25 pagesInsurance Products: Debi Dattamav7788No ratings yet

- Company Profile BirlaDocument31 pagesCompany Profile BirlaShivayu VaidNo ratings yet

- A Interim Report 1Document28 pagesA Interim Report 1Mayank MahajanNo ratings yet

- Unit - 3 Bilp Types of Life Insurance - Features - ConditionsDocument9 pagesUnit - 3 Bilp Types of Life Insurance - Features - ConditionsYashika GuptaNo ratings yet

- Project On Insurence MajorDocument81 pagesProject On Insurence MajordarshansinghwaraichNo ratings yet

- Introduction On Insurance Fund ManagementDocument9 pagesIntroduction On Insurance Fund Managementsawariya786No ratings yet

- Meaning of InsuranceDocument7 pagesMeaning of InsuranceSannidhi MukeshNo ratings yet

- InsuranceDocument7 pagesInsuranceAustin MathiasNo ratings yet

- Types of InsuranceDocument2 pagesTypes of InsuranceS GaneshNo ratings yet

- Table & ContentDocument43 pagesTable & Contentsweety coolNo ratings yet

- Internship Report FinalDocument40 pagesInternship Report FinalNeha GaiNo ratings yet

- Presentation: State Life Insurance Corporation of PakistanDocument16 pagesPresentation: State Life Insurance Corporation of PakistanAlee HulioNo ratings yet

- Executive SummaryDocument25 pagesExecutive SummaryRitika MahenNo ratings yet

- Project - Report HDFCDocument73 pagesProject - Report HDFCBaltej singhNo ratings yet

- INSURANCE LAW - ImpromptuDocument7 pagesINSURANCE LAW - ImpromptuDiya MirajNo ratings yet

- 3-Financial Services - Non Banking Products-Part 2Document47 pages3-Financial Services - Non Banking Products-Part 2Kirti GiyamalaniNo ratings yet

- Whole Life InsuranceDocument14 pagesWhole Life InsuranceSushma DudyallaNo ratings yet

- Insurance ....Document8 pagesInsurance ....SanyaNo ratings yet

- Life Insurance ContentDocument60 pagesLife Insurance ContentpiudiNo ratings yet

- 04 Insurance CompanyDocument38 pages04 Insurance CompanyAnuska JayswalNo ratings yet

- Mission and VissionDocument11 pagesMission and VissionPradeep Kumar V PradiNo ratings yet

- Importance of Life and General InsuranceDocument22 pagesImportance of Life and General InsuranceBhavik JainNo ratings yet

- Introduction of Bank: BanksDocument45 pagesIntroduction of Bank: BanksKunal NagNo ratings yet

- Life Insuranc (Sem - LLL)Document20 pagesLife Insuranc (Sem - LLL)Milton Rosario MoraesNo ratings yet

- NavdeepDocument18 pagesNavdeepSnehal LadeNo ratings yet

- Need For Life InsuranceDocument9 pagesNeed For Life InsuranceDeepak NayakNo ratings yet

- Potential of Life Insurance Industry in Sarita Vihar MarketDocument7 pagesPotential of Life Insurance Industry in Sarita Vihar MarketAjeet KumarNo ratings yet

- InsuranceDocument2 pagesInsurancefahim_ibaNo ratings yet

- Project Report ON: University of MumbaiDocument55 pagesProject Report ON: University of MumbaiNayak SandeshNo ratings yet

- Presentation On InsuranceDocument40 pagesPresentation On InsurancedevvratNo ratings yet

- Insurance ServiceDocument31 pagesInsurance Servicepjsv12345No ratings yet

- Stages in Policy IssuanceDocument9 pagesStages in Policy IssuanceNeha AmitNo ratings yet

- Macquarie FutureWiseDocument80 pagesMacquarie FutureWiseLife Insurance AustraliaNo ratings yet

- Need Based Investme NT Solution: Six Weeks Industry TrainingDocument32 pagesNeed Based Investme NT Solution: Six Weeks Industry Trainingshettyaakash66No ratings yet

- What Is Life InsuranceDocument5 pagesWhat Is Life InsuranceTeja AndeNo ratings yet

- Elements of Good Life Insurance PolicyDocument4 pagesElements of Good Life Insurance PolicySaumya JaiswalNo ratings yet

- Fabozzi FoFMI4 CH06Document15 pagesFabozzi FoFMI4 CH06Jion DiazNo ratings yet

- Functions of InsuranceDocument26 pagesFunctions of InsurancenikschopraNo ratings yet

- Insurance Promotion - IIDocument12 pagesInsurance Promotion - IIAditi JainNo ratings yet

- 1 Types of Life Insurance Plans & ULIPSDocument40 pages1 Types of Life Insurance Plans & ULIPSJaswanth Singh RajpurohitNo ratings yet

- Share ICICI PrudentialsDocument63 pagesShare ICICI PrudentialsMadhushreeNo ratings yet

- Insurance AssignmentDocument15 pagesInsurance AssignmentRashdullah Shah 133No ratings yet

- Origin of The Company: Meaning and Definition Nature and Scope Importance of Insurance Objectives of The StudyDocument32 pagesOrigin of The Company: Meaning and Definition Nature and Scope Importance of Insurance Objectives of The Studypav_deshpande8055No ratings yet

- Q1. What Is InsuranceDocument5 pagesQ1. What Is InsuranceDebasis NayakNo ratings yet

- Life InsuranceDocument5 pagesLife InsuranceAditya SharmaNo ratings yet

- Insurance Fm2accDocument4 pagesInsurance Fm2accyabaneifflemaurNo ratings yet

- Introduction To Insurance IndustriesDocument37 pagesIntroduction To Insurance IndustriesNishaTambeNo ratings yet

- Islamic InsuranceDocument22 pagesIslamic InsuranceAbdifatah AbdilahiNo ratings yet

- Chapter - I Introduction and Literature ReviewDocument54 pagesChapter - I Introduction and Literature Reviewabhishek nairNo ratings yet

- Handbook On Life InsuranceDocument17 pagesHandbook On Life InsuranceDeeptiNo ratings yet

- Insurance: Institute of Productivity & ManagementDocument39 pagesInsurance: Institute of Productivity & ManagementishanchughNo ratings yet

- Ibis Unit 03Document28 pagesIbis Unit 03bhagyashripande321No ratings yet

- Product & ServiceDocument11 pagesProduct & ServicefarrukhNo ratings yet

- Hum ADocument119 pagesHum Ajyoti8mishra100% (2)

- History of ORIX Leasing Pakistan LimitedDocument10 pagesHistory of ORIX Leasing Pakistan LimitedAbbasLiaqatQureshiNo ratings yet

- Muhammad Abbas Liaqat: Street #11, House #26, Block T, New Multan, Pakistan - Cell: 03036544590Document1 pageMuhammad Abbas Liaqat: Street #11, House #26, Block T, New Multan, Pakistan - Cell: 03036544590AbbasLiaqatQureshiNo ratings yet

- Report of Meezan BankDocument15 pagesReport of Meezan BankAbbasLiaqatQureshiNo ratings yet

- Foundation of Individual Behaviour: by Joylyn SilveiraDocument25 pagesFoundation of Individual Behaviour: by Joylyn SilveiraAbbasLiaqatQureshiNo ratings yet

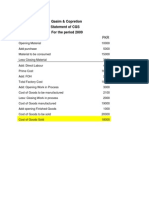

- Qasim & Copretion Statement of CGS For The Period 2009Document1 pageQasim & Copretion Statement of CGS For The Period 2009AbbasLiaqatQureshiNo ratings yet

- Batch 2010-12: Literature of BATADocument18 pagesBatch 2010-12: Literature of BATAAbbasLiaqatQureshiNo ratings yet

- Bahasa Inggris Ganjil Kelas X ABCDocument12 pagesBahasa Inggris Ganjil Kelas X ABCNazwarNo ratings yet

- Keerthi Question BankDocument65 pagesKeerthi Question BankKeerthanaNo ratings yet

- Essence: By: Bisma Kalsoom and Adeen MumtaazDocument8 pagesEssence: By: Bisma Kalsoom and Adeen MumtaazBisma KalsoomNo ratings yet

- Business Law ModuleDocument177 pagesBusiness Law ModulePatricia Jiti100% (1)

- Open The Book-Bible Quiz ChildrenDocument4 pagesOpen The Book-Bible Quiz ChildrenradhikaNo ratings yet

- Definition of Science FictionDocument21 pagesDefinition of Science FictionIrene ShatekNo ratings yet

- Province Tourist Destinations Festivals: REGION XI - Davao RegionDocument13 pagesProvince Tourist Destinations Festivals: REGION XI - Davao Regionaaron manaogNo ratings yet

- Mga Bilang 1-100 Tagalog With Symbol and PronunciationDocument2 pagesMga Bilang 1-100 Tagalog With Symbol and PronunciationJanice Tañedo PancipaneNo ratings yet

- Assignment 2 MGT501Document1 pageAssignment 2 MGT501Aamir ShahzadNo ratings yet

- EA and HalachaDocument63 pagesEA and HalachaAvraham EisenbergNo ratings yet

- Turbo-Couplings-Fluid Couplings-with-Constant-Fill - Operating-ManualDocument108 pagesTurbo-Couplings-Fluid Couplings-with-Constant-Fill - Operating-ManualCarollina AzevedoNo ratings yet

- Kemapoxy 150Document2 pagesKemapoxy 150Mosaad KeshkNo ratings yet

- Advisory Board By-LawsDocument3 pagesAdvisory Board By-LawsViola GilbertNo ratings yet

- SG20KTL Data SheetDocument2 pagesSG20KTL Data SheetPaulo Cesar M CostaNo ratings yet

- Micro Mythos - лайт версияDocument2 pagesMicro Mythos - лайт версияKate KozhevnikovaNo ratings yet

- Microbes in Ferment@3Document13 pagesMicrobes in Ferment@3T Vinit ReddyNo ratings yet

- Nursing Care Plan: HyperbilirubinemiaDocument5 pagesNursing Care Plan: HyperbilirubinemiaJanelle Gift SenarloNo ratings yet

- Doctype HTMLDocument30 pagesDoctype HTMLAndreiNo ratings yet

- DPP - (19) 13th IOC - (E) - WADocument1 pageDPP - (19) 13th IOC - (E) - WAassadfNo ratings yet

- UCD Otolayrngology GuideDocument95 pagesUCD Otolayrngology GuideJames EllisNo ratings yet

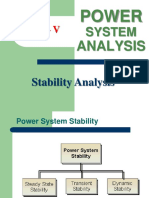

- Unit - V: PowerDocument32 pagesUnit - V: PowerVaira PerumalNo ratings yet

- 14.0 - ELC501 Forum Discussion GuidelinesDocument34 pages14.0 - ELC501 Forum Discussion GuidelinesiraNo ratings yet

- Chikmagalur RtiDocument10 pagesChikmagalur RtiSK Business groupNo ratings yet

- Daily Report DPT & Urugan Tanah BMM - 20 Juni 2023Document1 pageDaily Report DPT & Urugan Tanah BMM - 20 Juni 2023Rumah DesainNo ratings yet

- Writing Is A Great For Money OnlineDocument6 pagesWriting Is A Great For Money OnlineRisna SaidNo ratings yet

- Political Science P2 – Past Papers Analysis (CSS 2016-2020)Document4 pagesPolitical Science P2 – Past Papers Analysis (CSS 2016-2020)Afnan TariqNo ratings yet

- How Payal Kadakia Danced Her Way To A $600 Million Start-Up - The New York TimesDocument4 pagesHow Payal Kadakia Danced Her Way To A $600 Million Start-Up - The New York TimesRadhika SwaroopNo ratings yet

- Bali Tour Package 7 Days 6 Nights ItineraryDocument4 pagesBali Tour Package 7 Days 6 Nights ItineraryHartadi WijayaNo ratings yet